Wipada Wipawin/iStock via Getty Images

Wipada Wipawin/iStock via Getty Images

Graphic Packaging Holding Company (NYSE:GPK) is a manufacturer of fiber-based packaging and sells its products to a varied group of end markets. On February 20th, the company announced its Q4 and full year results for 2023. Today, I'll be walking through the recent results of the company, evaluate its business strategy, and assess its valuation to see if shares are a good buy today.

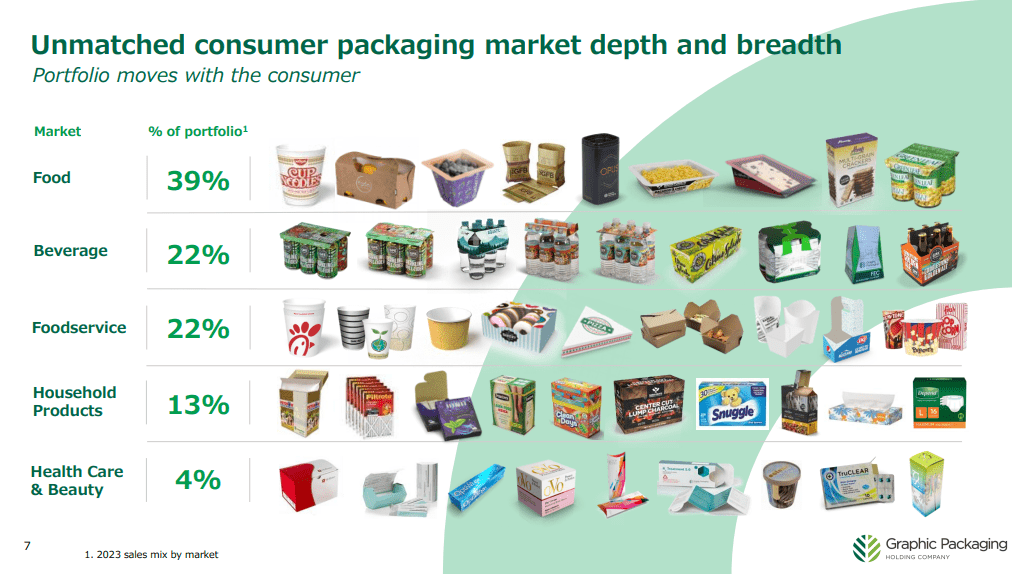

Graphic Packaging makes fiber-based packaging products for food and beverage, healthcare, pharmacy, and other consumer products. This includes everything from folding cartons, foodservice packaging, trays, strength packaging, and paperboard. With over 100 facilities around the world serving thousands of customers, it makes the packaging that can be found on some of the largest global brands. The company operates three primary segments, its Paperboard Mills segment, and its Americas and Europe Paperboard Packaging segments.

Investor Presentation

The Paperboard Mills segment is Graphic Packaging's smallest segment at less than 10% of sales. In this segment, the company owns 8 paperboard mills that make coated recycled paperboard (CRB), coated unbleached kraft paperboard (CUK) and solid bleached sulfate paperboard (SBS). The technical language here isn't important, but most of this paperboard needs to printed, cut, folded, and glued into final products that end up as cartons and containers. This is a relatively slow growing segment and has made up an increasingly smaller portion of revenues over time, as the other two segments outpace it.

In the Americas Paperboard Packaging segment, the company's largest segment at 66% of total revenues, the company produces finished products that are used as cups, lids, food containers, and folding cartons that are sold to consumer products companies, quick-service restaurants, and other foodservice companies. Graphic Packaging does the same thing in Europe too, but Europe has been growing faster as a result of acquisitions and makes up just 21% of revenues.

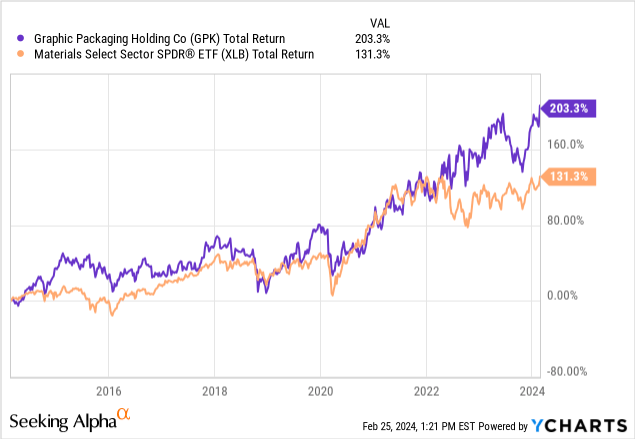

When comparing Graphic Packaging to the rest of the Materials sector, the company has outperformed by a wide margin. In the last ten years, shares have produced a total return of 203.3% compared to the Materials Select Sector SPDR ETF (XLB) which returned a 131.3% over the same time period. Annualizing these returns, Graphic Packaging has delivered an 11.7% compounded annualized return compared to the ETF's return of just 8.7%.

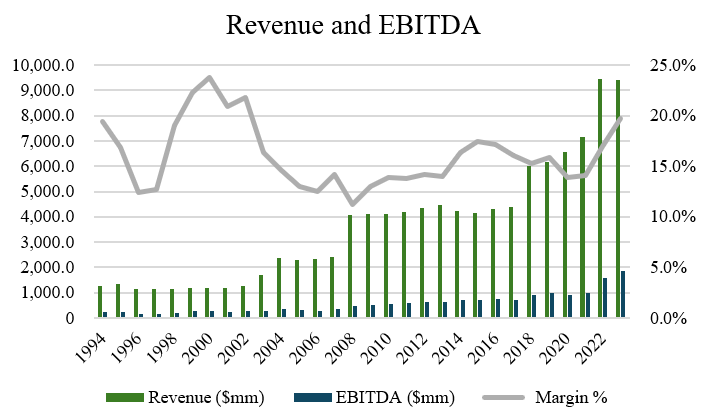

Over its life as a publicly traded company, Graphic Packaging has also had a track record of delivering above-average growth in its financial performance. In the last 20 years, revenue has grown at a CAGR of 9.0% per year and EBITDA has grown at a CAGR of 10.0% per year. In the last decade, revenue and EBITDA have compounded at CAGRs of 7.7% and 11.5%, respectively (source: S&P Capital IQ). With sales growth outpacing growth in EBITDA over both time periods, this demonstrates that Graphic Packaging has experienced margin expansion.

Author, based on data from S&P Capital IQ

Underpinning Graphic Packaging's performance is steady growth in the packaging industry. According to Vantage Market Research, the global paperboard and packaging market is expected to reach $172.5 billion by 2028 at an annual rate of 3.2%. This is a higher growth than was initially seen in the paperboard and packaging market in the five-year period between 2017 and 2021.

In addition to favorable industry tailwinds, a key part of Graphic Packaging's success has been through growth-by-acquisition, buying 13 businesses in the last six years. The largest one of those 13 was its purchase of AR Packaging in November 2021, which added $1.1 billion to the company's top line and $160 million in EBITDA. This acquisition was part of the company's acquisitive strategy in Europe and also opened up new markets in the healthcare and beauty products, diversifying the end-markets that Graphic Packaging serves.

When looking at the recent results for Graphic Packaging, the company announced a miss on revenue, but a beat on EPS. During the quarter, the company had revenues clock in at $2.25 billion, missing estimates by $150 million, and down 5.9% year over year. For the full year, however, sales were actually flat on a year-over-year basis.

While the company didn't announce any major acquisitions during the year, it did sell its Augusta paperboard manufacturing facility to Clearwater Paper (CLW), which brought in $700 million to the company. This sale is expected to close in Q2 2024 and was made subsequent to the quarter, so this isn't reflected in the recent financials.

While the sales figures for the quarter and full year were rather unimpressive, Graphic Packaging did see an improvement in profitability. Q4 EPS beat analysts' estimates of $0.70 by 5 cents and full year EPS of $2.91 was up 25% against last year. Driving this strong EPS growth was the adjusted EBITDA figure, which grew 17% to $1.88 billion for the full year. So it seems underpinning the results for the year was an overall improvement in profitability.

What's been driving this? Well, Graphic Packaging has been able to increase prices to partially offset volume declines during a difficult 2023. It's also gotten more cost efficient at its manufacturing plants, doing a better job at matching supply with demand.

This results in less excess inventory and capturing required demand from customers. And so with demand (volume) being lower year on year, the company did a good job matching that supply to demand, which led to stronger EBITDA margins and a subsequent increase in EPS. Q4 showed somewhat of a recovery and management seemed confident on the earnings call about a return to organic growth from here, with guidance for $200 million of sales in the innovation pipeline for 2024.

So far, 2023 proved to be a heavy capex year and this is expected to continue in 2024. What excites me about this is that while cash flow looks a bit mediocre on a year-over-year basis, many of these capex spending are growth capex, rather than maintenance capex, meaning the company is investing back into its business to support new facilities and acquisitions.

For example, last year, Graphic Packaging spent over $1 billion on a new facility in Waco, Texas where the company developed some 640,000 square feet in production and warehousing facilities, which should add about $80 million in synergies in each of 2026 and 2027. So the capex investments Graphic Packaging has made today aren't yet showing up in the financials. Of the combined $160 million of synergies, $100 million will come for more energy efficient use and better material management and the other $60 million should come from higher organic growth (100 to 200 basis points of improvement) as well as overall optimized mill capacity.

I view these investments as highly significant for Graphic Packaging. Why? Back in 2019, the company was doing less than $1.00 in EPS. Five years later and EPS has since tripled. And it was the same strategy back then too: build out unmatched capacity, system improvements, and optimize costs in order to generate margin expansion.

During the quarter, management also provided guidance on where they see their profitability in 2024. The company now expects between $1.75 billion to $1.95 billion in adjusted EBITDA, which is expected to translate to between $2.50 and $3.00 of EPS for the full year. I think the company has a very reasonable chance of hitting those targets. With a proven track record, I believe the capex investments the company is making today have the potential to spit off a ton of cash flow in the future. Looking back at the previous five years, the company has also had a track record of surprising to the upside on analysts' estimates, so if past performance is any indication, estimates may prove to be too conservative.

Continuing on outlook, I think when we consider Graphic Packaging's ability to make acquisitions and build new facilities, it certainly has the balance sheet to fund it. While year-end leverage is a little high at 2.8x, this is down from 3.2x in the prior year, so it is de-levering as cash flow picks up. Most of the debt is fixed at long maturities, so there isn't an immediate risk to refinance.

Finally, on capital allocation, both dividends and share buybacks should be a key part of Graphic Packaging's strategy for returning capital to shareholders. Since 2018, the company has bought back $900 million of its stock, bringing the share count down and increasing the long-term equity holder's stake in its business, with $76 million worth of shares repurchased in 2023 (source: S&P Capital IQ). And on dividends, while the company hasn't announced a dividend increase in 2023, the payout ratio has slowly come down, and I think that once this capex cycle is complete, there is a reasonable likelihood an increase will be implemented.

Of the 8 sellside analysts who cover Graphic Packaging's stock, there are 6 'buy' ratings, 1 'hold' rating, and 1 'sell' rating. The average price target is $28.75, with a high estimate of $33.00 and a low estimate of $21.00 (source: TD Securities). From the current price to the average price target one year out, this implies approximately 8.9% upside, not including the dividend yield of 1.5%. With total return potential of 10.4% upside over the next year, this suggests that analysts are moderately bullish on the company's near term potential.

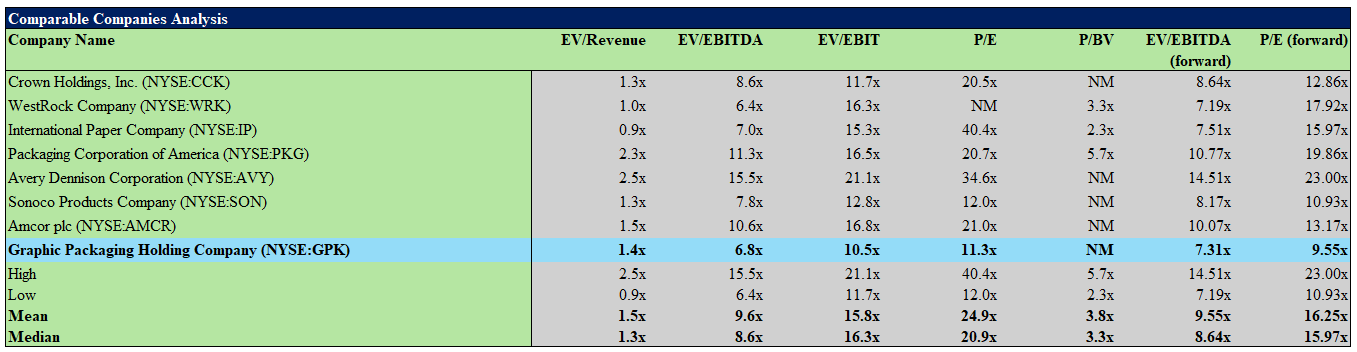

When looking at the company's valuation, Graphic Packaging trades at about 6.8x EV/EBITDA and 11.3x P/E which looks cheap on absolute terms. Investors should keep in mind, however, that they are unlikely to get outsized returns or rapid revenue growth from a company like Graphic Packaging, so it's important to manage expectations.

Comparing the company to peers in the packaging space, Graphic Packaging's valuation seems relatively inexpensive. With the industry average EV/EBITDA ratio of 9.6x and a P/E ratio of 24.9x, Graphic Packaging is trading at a substantial discount to competitors. While the company does have slightly above average debt, its historical growth rate has been higher, and it doesn't have concentration in one end-market. Other possible reasons might be that it's a much smaller company than the rest, but the valuation disconnect is quite unjustified in my view, given its above average growth rates. Thus, shares seem to be undervalued on a relative basis.

Author, based on data from S&P Capital IQ

As for the risks to the investment thesis, the main one would be the risk of raw material prices increasing. The company's costs are sensitive to the prices of energy, secondary fiber, and petroleum-based material, so these cost inputs should be monitored as they could have adverse pressures on margins in highly inflationary periods. As well, as a company in the packaging space with a heavy focus on consumer packaging, Graphic Packaging is sensitive to the overall economic health of the U.S. and European consumer. Thus far, consumers haven't slowed down their spending despite talks of a recession last year, so it seems that this risk is somewhat mitigated in that regard. That said, investors should pay attention to changes in interest rates, inflation, and GDP growth to assess the macro risks at play.

In conclusion, Graphic Packaging's recent performance indicates that it has a resilient business model poised for continued growth. Despite a slight revenue miss in the last quarter on the back of lower volumes, the company seemed to demonstrate very strong profitability improvement during the quarter, fueled by effective cost management and strategic pricing strategies. With a history of above-average growth and a solid track record of acquisitions, I think Graphic Packaging stands to benefit from ongoing industry tailwinds and its own proactive investments in capacity expansion. Trading at a discount to industry peers, I believe Graphic Packaging looks like an excellent buy at today's prices and its shares seem poised to deliver above-average returns long-term given its attractive end-markets, growth-by-acquisition strategy, and investments in capacity expansion.