tadamichi

tadamichi

What a wild few years it has been in the fixed-income markets. The Fed began its rate-hiking campaign about this time in 2022 – a period of rising equity market volatility, surging crude oil prices, and a strengthening dollar. Today, Treasury volatility has eased, with the ICE BofA MOVE Index not far from 52-week lows while the VIX is subdued near 15.

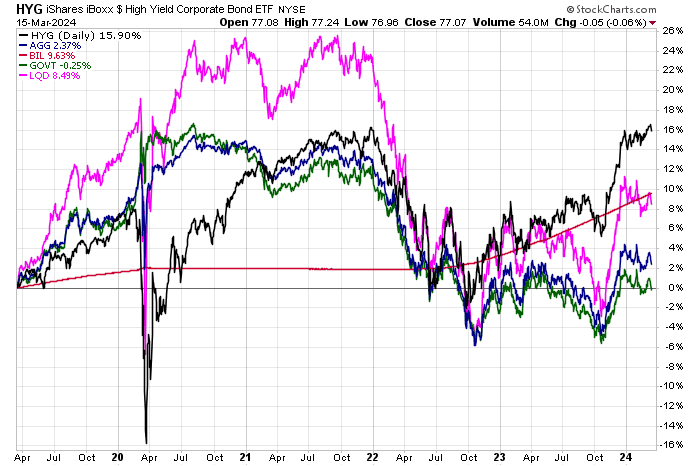

Zoom out, though, and you’ll see a set of varying Treasury and credit returns. Only T-bills and junk bonds are not in total return drawdowns. Let’s home in on the high yield space by analyzing the iShares iBoxx $ High Yield Corporate Bond ETF (NYSEARCA:HYG).

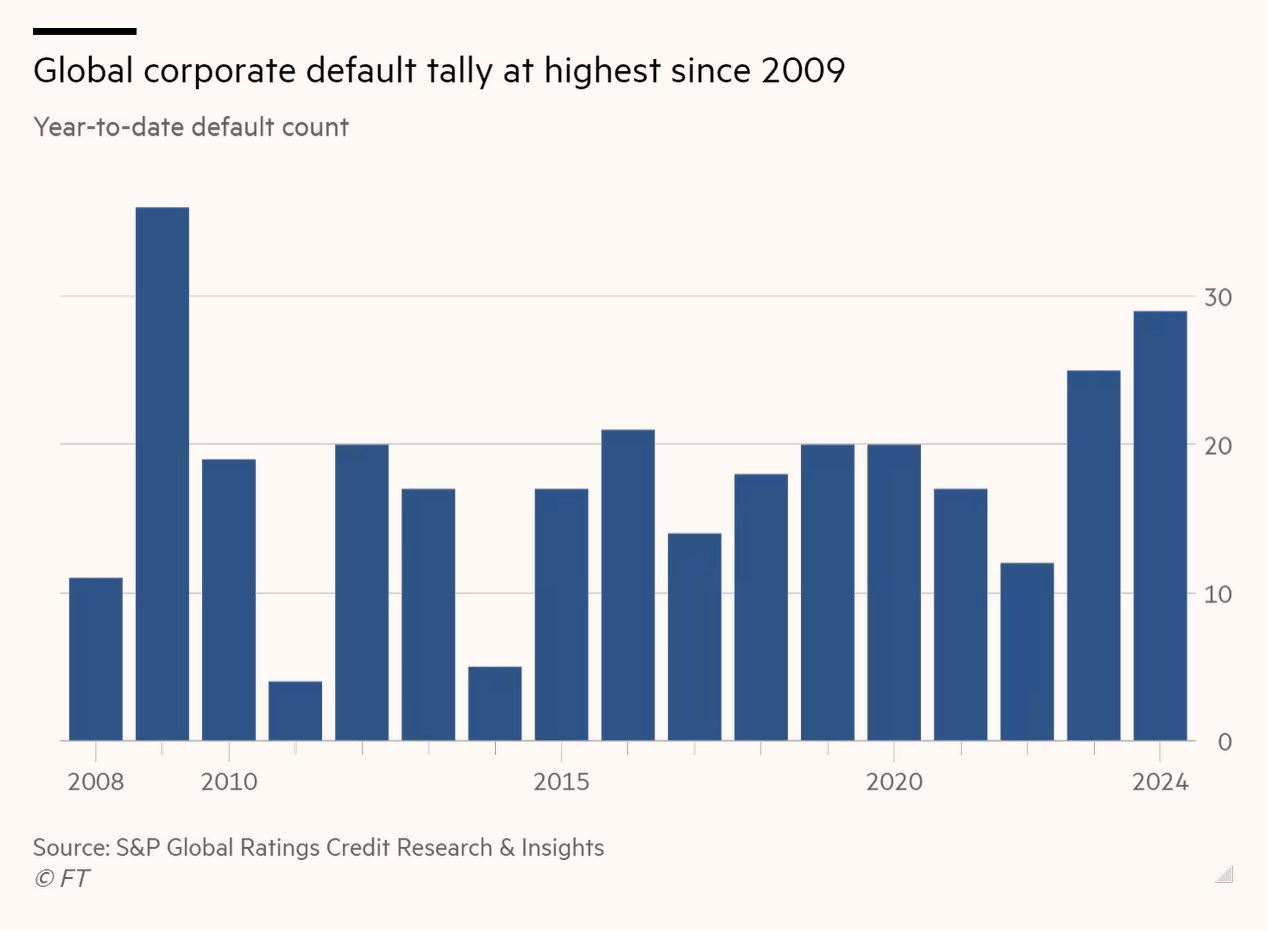

I have a hold rating on the HYG fund – spreads are near cycle tights while corporate defaults are on the rise. That is not a lucrative risk/reward situation for HYG.

Stockcharts.com

FT

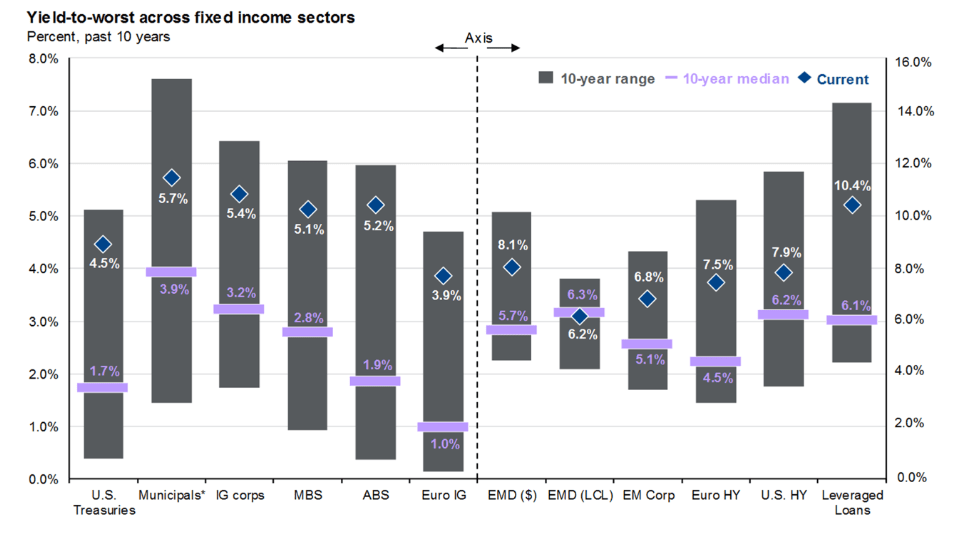

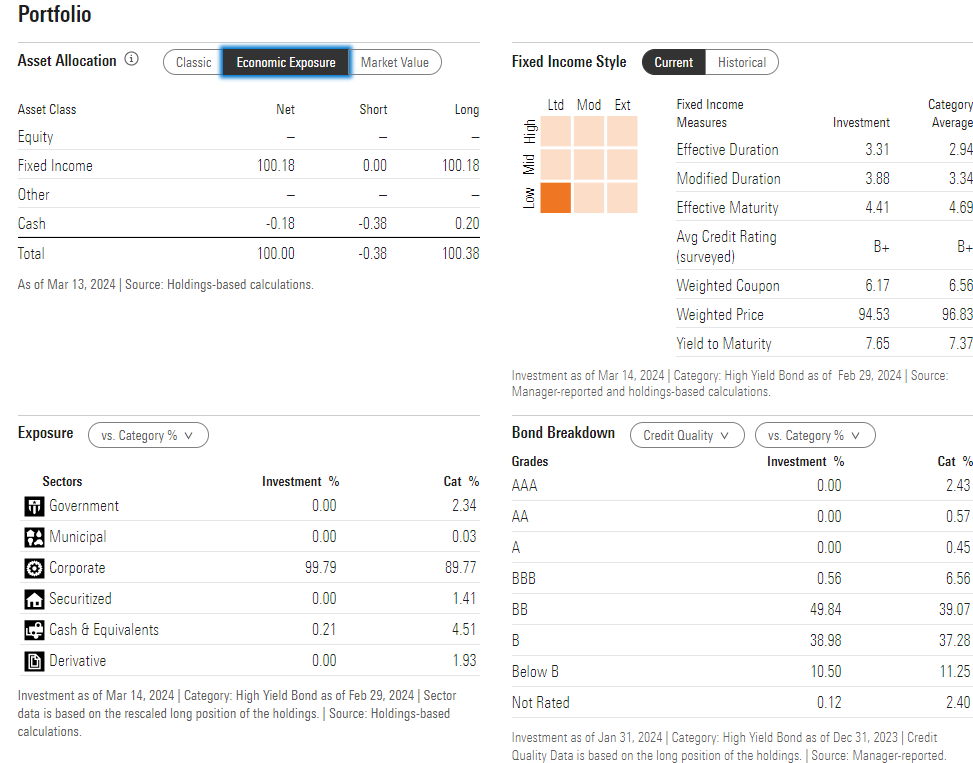

My weekly market review includes a look at the WisdomTree daily dashboard. One of the most telling visuals is a chart with the yield to worst on the y-axis and modified duration on the x-axis. You will find that junk bonds feature a lower duration than investment-grade credit.

The high-yield space currently sports a yield-to-worst of around 7.4% - that’s about two percentage points below where they were during the middle of last year. As market interest rates have ebbed from their 2023 highs and confidence has improved in the riskiest niche of the corporate bond market, there is less yield to be had in something like HYG.

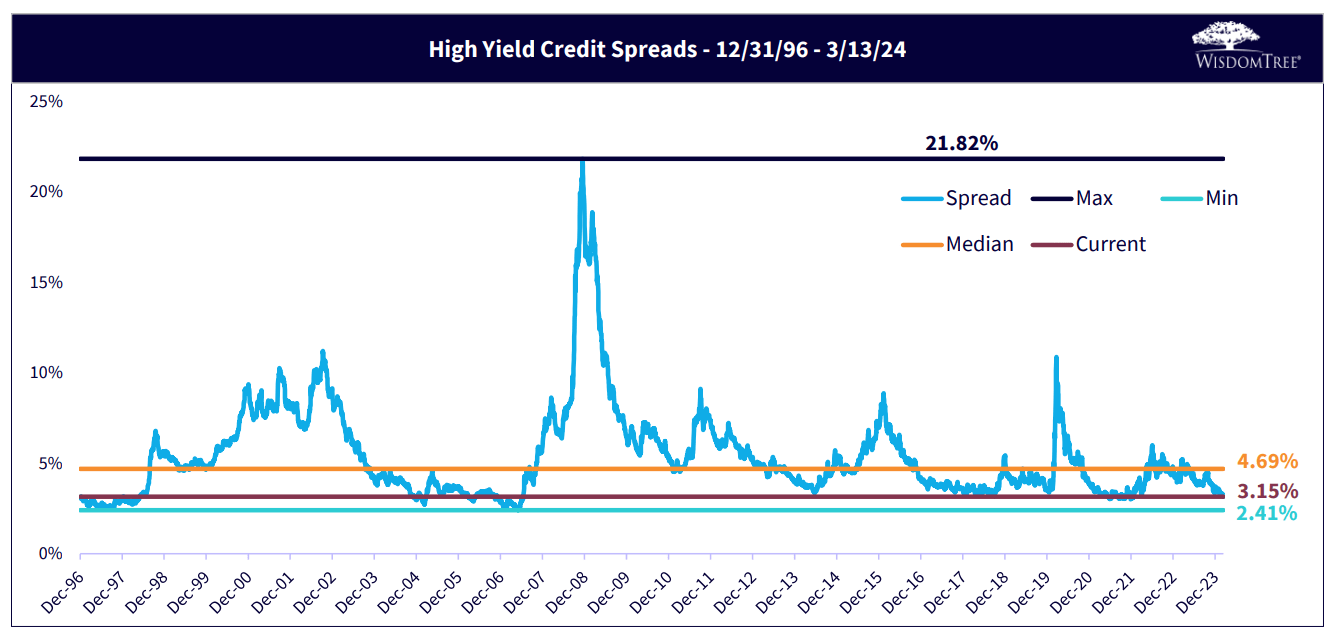

WisdomTree

To illustrate the point, WisdomTree’s data show that high-yield credit spreads are indeed near cycle tights. That is a bullish indicator for stocks, as it underscores high optimism in American corporations' ability to fulfill its debt obligations, but any hiccups in solvency metrics or mere sentiment could result in a significant rise in spreads, which would be bearish high-yield bond prices.

WisdomTree

The good news for diversified bond investors is that most areas of fixed income offer much beefier yield today compared with the average of the 2010s. Over the past 10 years, the average yield to worst on HYG is 6.2% compared with today’s rate above 7%. I encourage investors to consider European high-yield bonds or domestic leveraged loans – both slices of the global fixed-income market are still relatively attractive. If HYG's YTW climbs back toward 10%, then it becomes more attractive. Of course, equities might then be a better value, too.

JPM

As for HYG itself, the 3-star, Neutral-rated ETF by Morningstar plots in the lower left section of the fixed income style box. Its current effective duration is 3.31 years – that's relatively low compared to high-grade credit, so there is significantly less interest rate sensitivity and more credit risk. Expect HYG to have a higher correlation than investment-grade bonds to the stock market. HYG is not the absolute riskiest portfolio, however. Half of the allocation is rated BB, barely below investment grade and just 11% is below B.

Morningstar

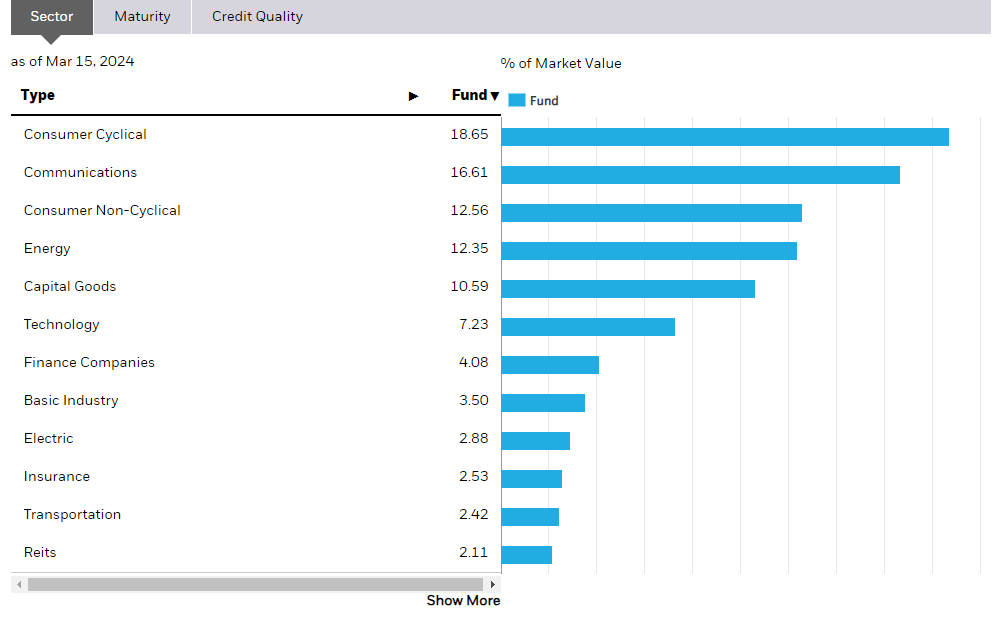

Sector-wise, there’s ample diversification with HYG, helping to limit risk metrics. According to iShares, 19% of the portfolio is comprised of the Consumer Discretionary sector with 17% allocated to Communication Services. Energy was once a large chunk of the junk bond index, but many oil & gas names were consolidated in the late 2010s and early 2020s, and capital discipline is much tighter in that niche of the corporate world.

iShares

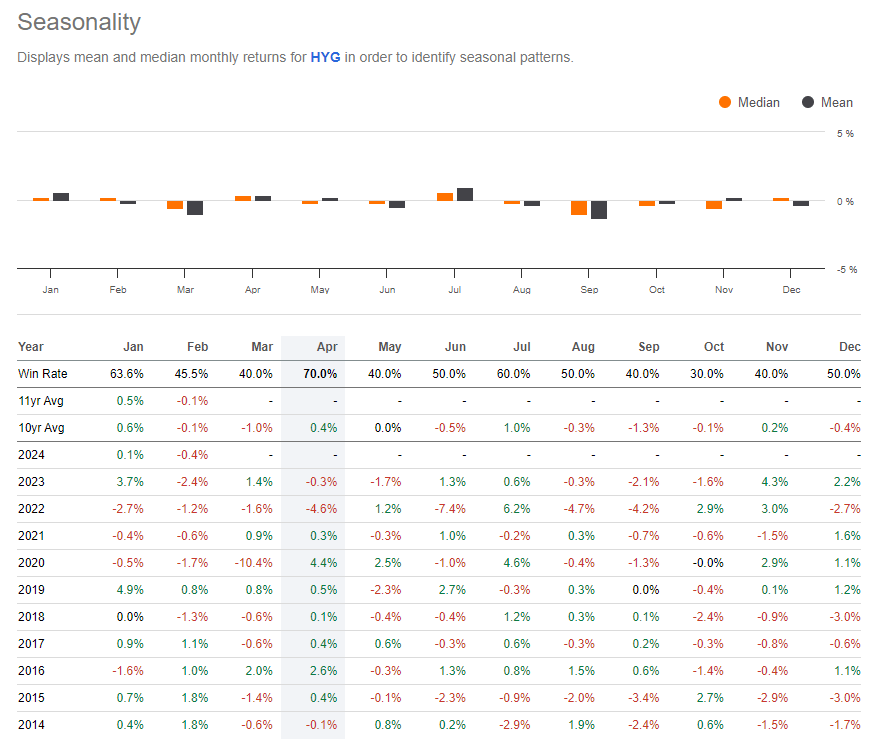

With weak share-price momentum and high liquidity, HYG tends to perform well in April, according to Seeking Alpha’s seasonality tool, but gains are not all that high. Prospective investors should be wary of the August through October stretch, though.

Seeking Alpha

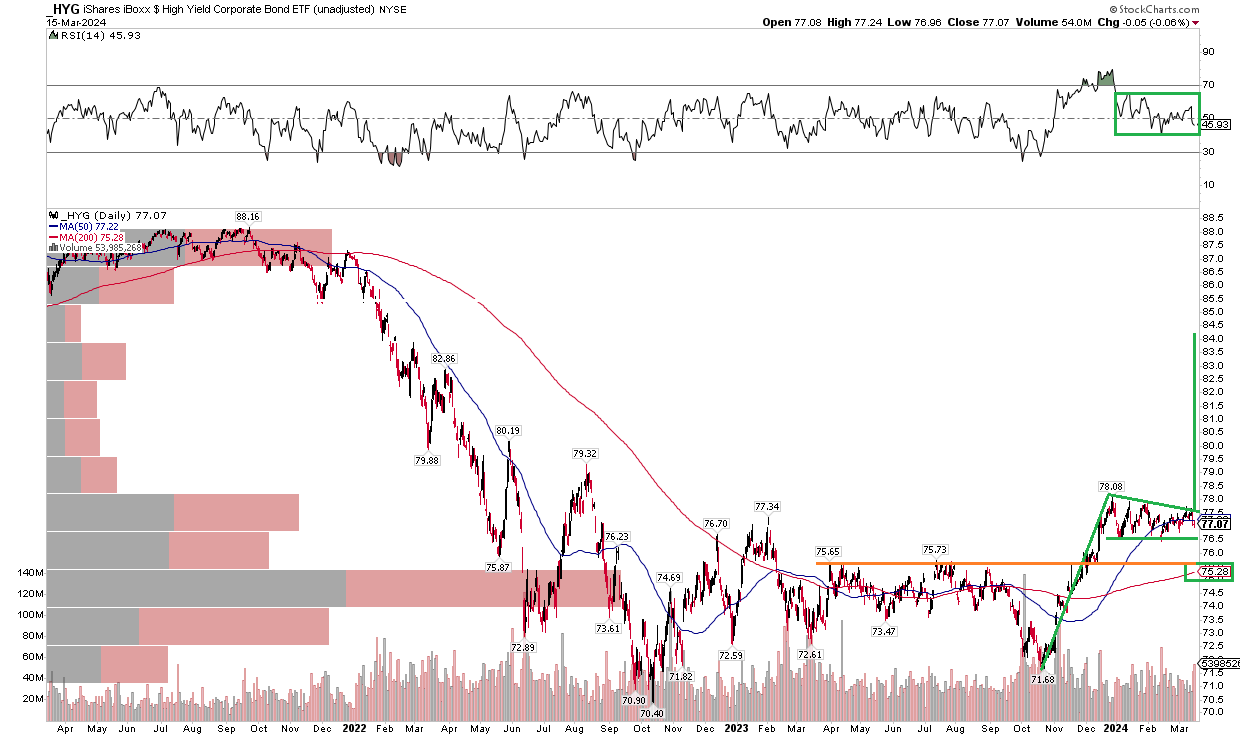

The $16.8 billion ETF looks strong on the chart despite a smaller yield today. Notice in the graph below that shares are in a bullish descending triangle pattern after rallying from lows notched last October. We can project an upside target based on the height of the previous rally, added on top of the potential breakout point. So, take $6.40 and tack that on to about $78 to yield a bullish measured move price objective of $84.60 if we see a breakout transpire. That would bring HYG close to its late 2021 lows – an area of overhead supply that would also be an understandable selling pressure zone.

Also take a look at the RSI momentum gauge at the top of the chart – while it’s off the highs, it has not fallen off too much. So long as the RSI momentum oscillator holds above 40, the bulls should maintain their control. Support that assertion is the rising 200-day moving average. Price is above that trend indicator line and has been since a golden cross pattern took place last December.

Overall, support is seen between $75 and $76, while $78 could be a minor resistance point.

Stockcharts.com

I have a hold rating on iShares iBoxx $ High Yield Corporate Bond ETF. With tight credit spreads and a lower yield compared to a year ago, I would rather reduce default risk with high-grade corporates or by simply allocating my bond sleeve to short or intermediate-term Treasuries. While HYG’s technical chart is solid and the fund is at a total return all-time high, the risk/reward setup is not ideal today.