Matt Winkelmeyer

Matt Winkelmeyer

Canada Goose (NYSE:GOOS) is a Canadian luxury winterwear retailer.

The company's parka became a fashion icon and now sells for about $1,500 at 75% gross retail margins. However, the company's desirable position is not inexpugnable, and it struggles to implement a DTC strategy.

In this article, I review the company's brand position, competition, and risks, plus its DTC strategy and problems.

I believe that considering the company's pros, mainly in brand value, and cons, mainly in execution, the current stock price does not represent an opportunity, especially when compared to the similarly positioned Moncler. For that reason, I rate Goose as a Hold.

Canada Goose's core product is its parkas.

Heavy-weight, goose downfeather filled jackets that retail for about $1,500. When the company went public in 2017, this line represented over 85% of sales; today, it is still above 65% (according to the company's Investor Day Presentation).

The company sells its product line globally, with sales close to evenly divided between Canada, the US, East Asia, and EMEA.

Performance, the dream: Canada Goose started selling heavy-duty parkas to rangers and expeditioners in Canada's Arctic. Of course, the quality of the product had to be outstanding as the task it was used for was potentially deadly.

From that niche, the company's product organically expanded to film crews that had to withstand cold climates for hours while filming.

This extreme quality against the Arctic is what luxury academics call 'The Dream' at the core of the brand. When someone wears the parka, even though they might be in a city where the climate is mild, they are wearing the same gear that countless Arctic expeditions and famous filmers used.

Goose protects this dream in several ways. It controls most of its manufacturing, something unusual for North American apparel brands. More than 75% of the production is done in North America and above 85% for the core products. The company offers a lifetime warranty on its products, and the webstore provides a lot of details on the products' characteristics. The Arctic program is part of the company's logo.

Luxury, the motive: Despite Goose's pride in its product, the people buying its parkas do not go to the Arctic or might not even leave the cities much. The company's parkas are bought for their luxury component. They are exclusive, expensive, and easily noticeable, with their clearly demarcated logo.

Fashion cycle risk: Goose's products seem to align perfectly with a current fashion trend for exaggeration, bling effect, oversized pieces, and techwear.

Without being luxurious, Patagonia's or Columbia's success in this arena shows how attractive performance apparel is in the mass market. Another iconic example is Tesla's cybertruck: extremely functional, cubic, techy, and super expensive.

However, the specificity of this fashion makes Goose's position more risky than other luxury brands with a more established style and heritage. Fashion cycles change every decade or so. I don't think Goose's parkas would fit as much if the fashion trend changed to more stylized and less flashy.

Designer competition: Goose's products are generally compared to Moncler's (OTCPK:MONRF). This Italian company offers luxury jackets at even higher prices, above $2,000, without the performance dream.

Instead, the dream is based on Italian design. It is much more flexible, offering different styles to customers, including baggier or skinnier, flashy or sober, with more or less relevance to the brand logo.

Moncler pays homage to the European fashion gods by organizing catwalks in Milan and doing heavy celebrity advertising.

Although the market is big enough for two brands, I believe Moncler's proposal is more durable because it is less based on a fashion cycle and more on traditional creativity and heritage competition in luxury.

When the company went public in early 2017, less than 28% of its sales were DTC (according to its 4Q17 earnings call). As of the latest report for 3Q24 (Goose's fiscal year ends in April), the company will generate 70% of revenues from DTC this year.

This has been part of the company's strategy since going public, moving from no stores (it opened the first two flagship stores in 2017) to close to 70 by the end of this calendar year. In the meantime, it has reduced the weight given to wholesalers as it starts competing with them in local markets. The company sells locally in 57 countries via physical stores or e-commerce.

Mixed results: The expected result of moving downstream is increasing gross margins and revenues at the expense of growing SG&A as a percentage of revenues. The ideal result is higher operating profitability because the company can generate more sales and profits from its stores than its costs. In the long term, controlling the point of sale helps nurture the brand and customer experience. Additionally, flagship stores in the world's capitals are great advertising for the affluent public that buys Goose's products.

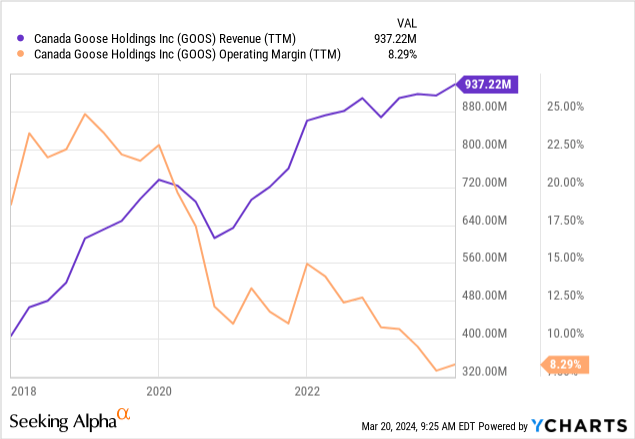

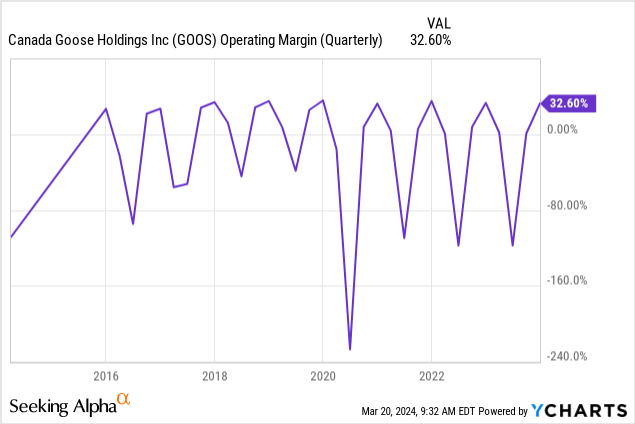

Unfortunately, Goose has not been able to materialize the move in higher operating margins yet, quite the contrary.

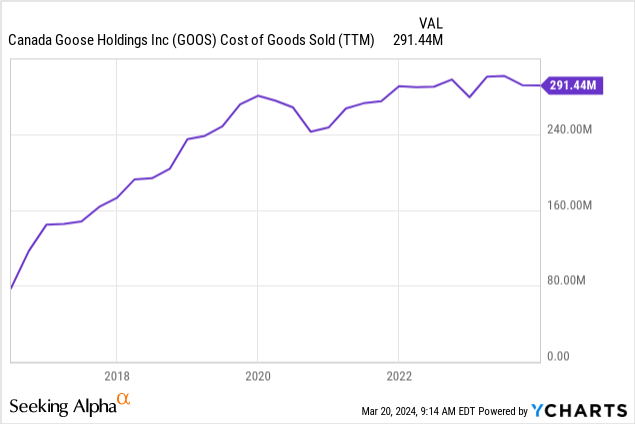

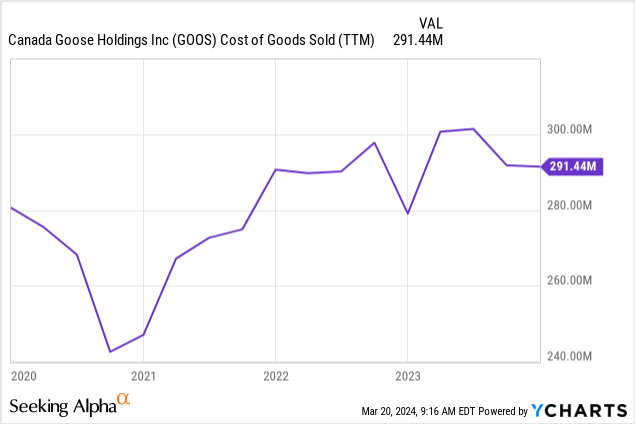

Cannibalization: The company's gross margins expanded, and so did revenues. I believe gross margin expansion caused the revenue expansion without significantly increasing volume sales. The company cannibalized its wholesale sales by transferring them to DTC.

My belief is sustained by the fact that after 2019, when the company still had 11 stores, Goose's CoGS remained flattish. This could mean that the company is now able to produce more apparel with the same costs or that it is simply selling the same number of pieces at higher prices because it is selling in retail and not wholesale. I believe in the second explanation.

Winter lines and store utilization: Goose is a luxury product that must be sold at luxury locations. This includes exclusive malls in the world's capital. The stores are relatively large, averaging 3,000 square feet, some including Cold rooms reaching -15 degrees Celsius for customers to feel the Arctic dream, plus knowledgeable salespeople prepared to sell a $1,500 jacket.

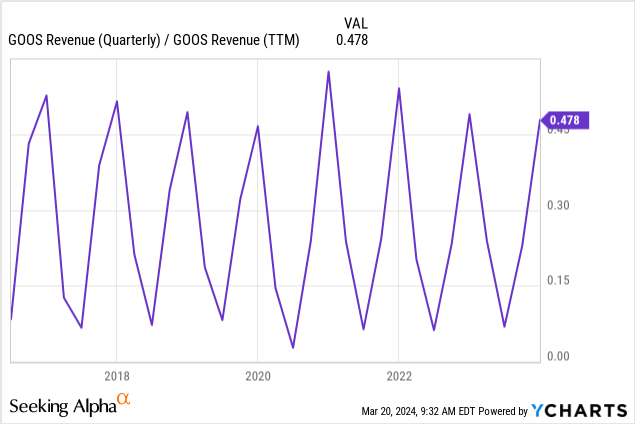

The company must pay a high fixed cost to place a store. However, the company's products are sold for winter. The company's Q3 (Holiday season) represents 50% of sales. This heavy seasonal pattern means the stores (and the company) are unprofitable for most of the year.

This problem did not exist when the company was wholesaling. The main evidence is that operating margins were negative during low-season before the pandemic store expansion, but not even close to today's level of losses.

The company's response was to launch new lines that could be sold outside of the winter season. For example, heavy jackets represented 85% of sales in 2017 but now represent about 65%, which is still a high number but lower. The company's lighter jackets have had some success. However, this is still a winter product, so seasonality has not changed much.

Corporate expenses: Since the pre-pandemic period, Goose has lost 14 percentage points of operating margin. Interestingly, most of that loss (8 percentage points) came from corporate expenses, not lower store profitability. Corporate expenses (categorized in the financial statements as Other SG&A) grew from 20% of revenues in fiscal 2020 to 28% in fiscal 2023.

There are other signs of this problem. In fiscal 2018, the company had 6 B&M stores, 12 e-commerce stores, and 267 retail employees. By 2023, it had close to 51 B&M stores and 57 e-commerce stores, but only 881 retail employees. Six times more overall stores (nine times more B&M) with three times more employees. That could be called efficiency.

However, corporate employees are multiplied by three without generating any gain in operating income. Goose has more corporate than retail employees. The company also moved to a more luxurious headquarters in Toronto. The company's original headquarters was in one of its factories on the city outskirts. In contrast, the new ones are in a glass building by the river downtown, adorned with marble, art, a museum, and several cafeterias.

Finally, maybe the company is really investing in brand marketing, a very important investment that gets expenses because of its accounting treatment. This is recorded in corporate SG&A as well. However, tracking the change in marketing expenditures (the absolute figure is not provided) from the company's MD&A since fiscal 2020 (when it was released) shows that the increase in corporate SG&A has been CAD 186 million, but only CAD 45 million went to marketing.

On its 2023 Investor Day, Goose shared that it plans to double its store count by 2028. This would be coupled with line expansion to increase store utilization. The result would be to triple revenues to CAD 3 billion and multiply EBIT by 10 to CAD 1 billion, with EBIT margins of 30%.

It makes no sense to believe in this guidance, given that the company has not shown that it can perform at those levels. We should start from today and observe the situation unfold in the future.

On the positive side, Goose has a sought-after brand and product. Without these attributes, it could not sell $1,500 jackets. The company sells globally, meaning the product has a multicultural appeal, and the potential market can be considerable.

On the negative side, Goose's revenue growth has come from cannibalization, its retail model has a fundamental flaw in store utilization, it has increased corporate expenses as a percentage of revenues by 8 percentage points, and its products' relevance is tied to a specific fashion cycle.

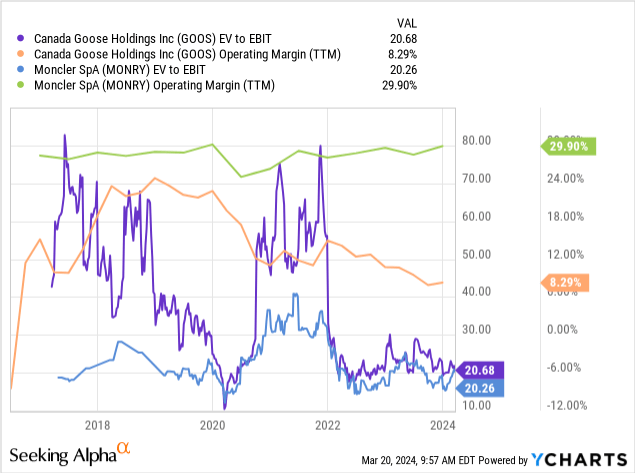

Against this, Goose trades today at an EV/EBIT multiple of 20x. I believe this is excessive. To eventually obtain a 10% earnings yield from this price, the company should double its revenues, or double its operating margins.

For example, with double the revenues and 9% operating margins, plus 25% income taxes, the company could generate $130 million in NOPAT against a current EV of about $1.3 billion. The same would occur with double the margins and similar revenues.

I believe these expectations are high and, above all, not justified by the company's current performance. As a comparison, the similarly positioned Moncler trades at the same multiple but has growing operating margins that are three times those of Canada Goose.

Overall, I believe Canada Goose is not an opportunity at these prices. The EV/NOPAT multiple should be at least below 15x to reconsider. This would represent an EV closer to $700 million, which at current net debt levels implies a stock price of around $6 to $7.

In the future, I would like to see lower seasonality, more weight given to non-core products (especially lower weight to heavy parkas), and lower corporate expenses as a percentage of revenue. The company does not face enormous risks, given it is profitable and its brand is sought-after. In the longer-term, it could face fashion cycle risks if logo-heavy techy winterwear goes out of fashion.

In the meantime, I can wait for improvements or lower prices.