ryasick

ryasick

In January of 2023 Gladstone Commercial (NASDAQ:GOOD) cut its dividend, which had been at approximately $0.125 per month since 2008 to $.10 per month. As I pointed out in 2022 in both Gladstone Commercial Beats Estimates on $4.3 Million In Non-Recurring Accelerated Rents (November 2022) and Gladstone Commercial: My Calculations Imply Rising Rates Will Show It Is Swimming Naked, (July 2022) GOOD’s dividend was unsustainable, and a dividend cut was the natural outcome of having overpaid the dividend relative to cash flow for years. On the earnings call following the cut, the CEO, David Gladstone, claimed it was likely the dividend would be raised within a year.

GOOD Earnings Call 4Q22

As I look at GOOD’s financial situation heading into 2024, not only do I think it is highly unlikely that they will be able to raise the dividend, I think there is a possibility the dividend may have to be cut again due to liquidity challenges. On its 4Q22 earnings call GOOD stated its intention with cutting the dividend was to retain capital and put the REIT in a more stable position, given the uncertain economic outlook at the beginning of 2023.

GOOD Earnings Call 4Q22

While the economy performed well in 2023, and the recession that was anticipated due to higher rates never materialized, GOOD’s financial position continues to look precarious in my opinion.

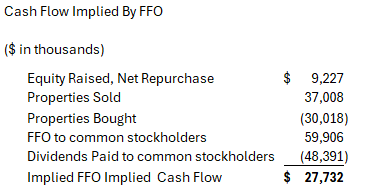

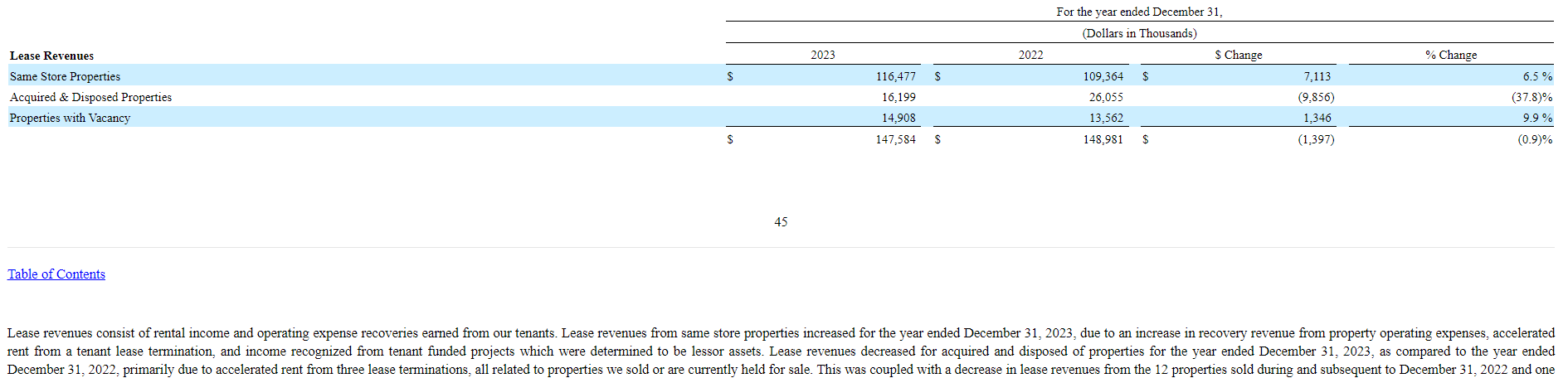

In 2023 GOOD spent $30 million on new properties and sold $37.0 million in properties from its existing portfolio. (GOOD 2023 10-K Face of Statement of Cash Flows) Additionally, they raised over $9.2 million in equity. (GOOD 2023 10-K Face of Statement of Cash Flows – nets out repurchases) They also reported FFO of over $59.9 million versus a dividend (at $0.10 per month to common shareholders) of 47.9 million. (GOOD 4Q23 Supplemental Financial) As shown below, this should have led to a decrease in net debt for GOOD of $27.7 million.

GOOD 4Q23 Financial Supplement and 2023 10K

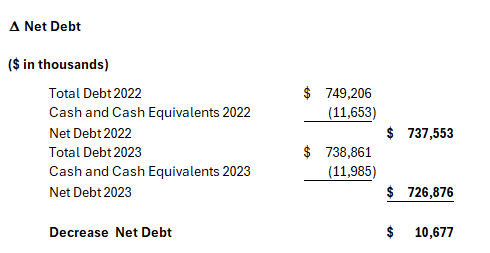

In fact, GOOD’s net debt only went down by $10.7 million as shown below.

GOOD 2023 and 2022 4Q Supplemental Financial Information

The question investors should be asking is what happened to the other $17 million of the cash. GOOD’s cash flow statement provides some of the answers. $6.7 million and $2.3 million went into property improvements and leasing commissions, respectively. These are expenses that most REITs include in their AFFO calculation which they use to set dividend policy. GOOD ignores these expenses and only provides investors with an FFO payout ratio in its financial disclosures. Additionally, GOOD’s cash flow statement shows a $3.2 million increase in deferred rent receivable. This means GOOD is booking rents in excess of the cash it receives from tenants. Consistent with Generally Accepted Accounting Principles (GAAP), GOOD is straight-lining the rent it receives from tenants over the life of the lease. This means if a tenant on a 3 year lease pays $3 in year 1, $5 in year 2 and $7 in year 3, in all 3 years the lessor would book $5 of revenue. While appropriate from a GAAP perspective, straight-line rents cannot be used to pay dividends or other expenses. This is why most REITs adjust their AFFO calculation for straight-line rents.

As I wrote about in Gladstone Commercial Hits Numbers With Rarely Used Accounting, While A Debt Maturity Looms (May, 2023) and in Gladstone Commercial Tops Consensus With Non-Recurring Termination Fees, While Financial Statement Errors Highlight Its Unusual Accounting, (August 2023) GOOD has an unusual policy of booking revenue for tenant improvements paid for by tenants. This means revenue is being booked even though no cash is being received. This item was large enough that it is specifically mentioned in the 10-K as one of the drivers for same-store revenue growth.

GOOD 10K 2023

I suspect it is the main driver as same-store revenues were up by $7.113 million and the other items listed as explanations can only explain a small portion of the increase. For NNN lease properties, landlords generally collect 100% of expenses from tenants as reimbursements and GOOD had 100% collection in both 2023 and 2022. (Gladstone Commercial Investor Presentation 2022 and 2023.) This means reimbursements can only account for $1.04 million of the increase as shown below.

GOOD 10K 2023

In 2023, there were only $2.13 million in accelerated rents in total. (GOOD 2023 10-K p. 37) This leaves $4 million which is likely almost entirely attributable to recognizing revenue from tenant-funded improvements. This partially explains the $7.457 million shown as amortization of deferred rent assets and liabilities deduction to cash flow on the 2023 Cash Flow Statement.

An investor listening to the conference call might have missed the importance of revenue recognized from tenant-funded improvements contribution to revenue growth. While it is listed in the 10-K as an explanation for revenue growth (see above), this item was omitted from management's prepared remarks on the conference call.

GOOD 4Q23 Earnings Call

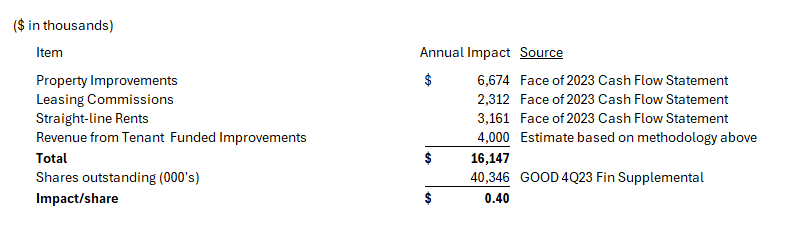

(Recoveries refers to recoveries from operating expenses, not tenant funded improvements.) The items mentioned above total over $16 million, or $0.40 per share, as shown below. GOOD’s FFO only exceeded its reduced dividend by $0.26 per share in 2023.

GOOD 10K 2023 and 4Q23 Supplemental Financial Information

While GOOD is producing far less cash flow than its FFO would imply, its business continues to face operational pressures in 2024 due to lost income from sold properties, releasing challenges and expiring interest rate caps.

GOOD’s management team has made it clear that part of its strategic vision is to reduce its office exposure. In their investor presentation and on their conference calls they highlight the decrease in the percentage of its portfolio represented by office assets. Given the trouble in the office market, this is probably a logical course of action. However, selling office properties that previously provided NOI for relatively low prices, given the market, leaves a hole in FFO that needs to be addressed. GOOD's held for sale properties are listed on p. 75 of the 2023 10K. One of them, a 115,000 sqft. office building Columbus OH was sold for $4.5 million in January of 2024. It provided almost $1.4 million in annual rental revenue in 2023 before its lease expired on December 31st. This means GOOD is selling the asset at a 31% yield on 2023 income. It will be impossible to redeploy the capital at a similar yield. (GOOD purchased the property for $11.8 million in 2014.) In addition to the Columbus property, GOOD has an office property in Richardson, TX listed as held for sale. Clearly, the sale process is moving slowly, as it has been listed as a held for sale property since June 30, 2023. (GOOD 2Q23 10Q)

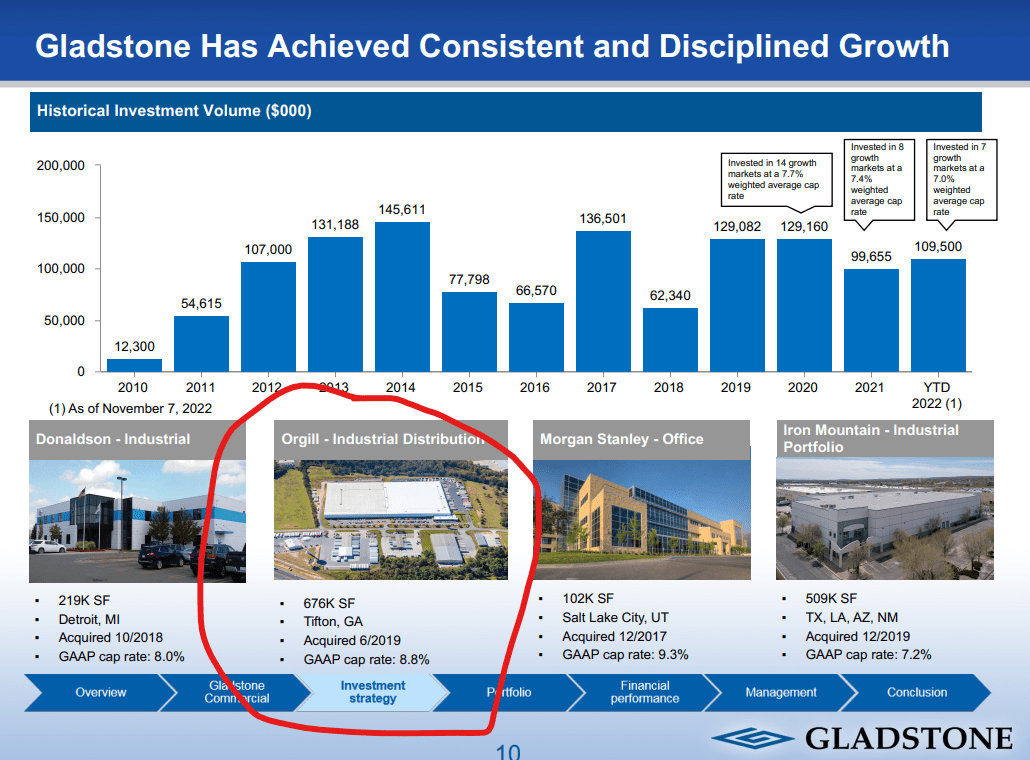

GOOD’s third held for sale property is particularly intriguing. It is a 676,000 sqft. industrial property in Tifton, GA that was purchased in 2019. (GOOD 10K 2023) It is hard for me to imagine why it no longer fits with GOOD’s overall strategy. The property was purchased in 2019, and it is still pictured in their most recent Investor Presentation on a slide labeled Consistent and Disciplined Growth.

GOOD Investor Presentation Feb. 2024

The June 2019 press release announcing the purchase said there were 8.5 years remaining on the lease, which would imply a lease expiration date of 2028. The property schedule associated with GOOD’s Line of Credit Amendment in 2022 shows the lease expiring in April of 2024. (Filed with the SEC on August 19, 2022) I can only speculate on the reasons for the variance; perhaps there was an early termination clause. It looks as though GOOD was able to get the tenant, Orgill – a third-party logistics firm, to agree to a short-term extension as leasing brochures for the property show availability as of 4Q24. When this property is sold, not only will GOOD lose the $1.5 million income associated with this property but it will also be required to repay the $7.5 million mortgage securing the property, which has an interest rate of 4.35%.(Schedule 6.25 of Amended and Restated Credit Agreement filed with SEC on August, 19 2022.) This means GOOD will lose the benefit of the below market debt.

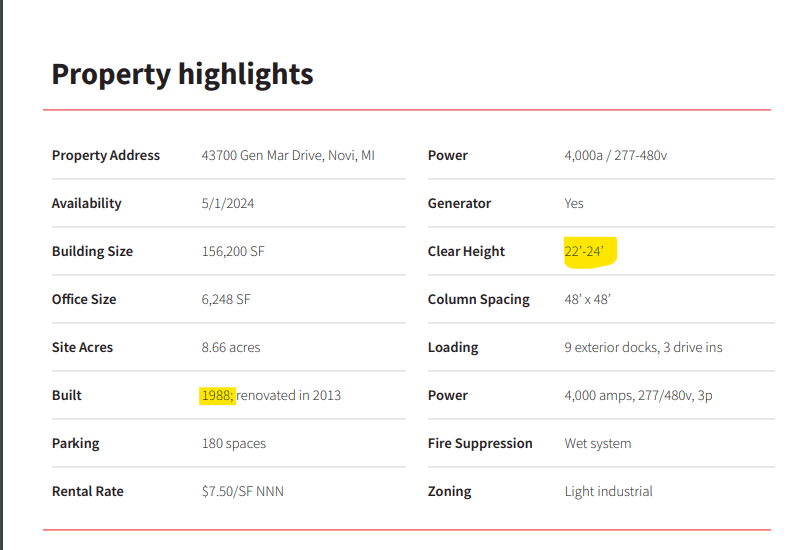

While leasing NNN office in the current environment is extremely difficult, as GOOD has demonstrated over the past several years, leasing older industrial product can also be an expensive and time consuming process. I foresee two properties with leases expiring this year that I expect will be challenging for GOOD to release: a 156,000 sqft. property in Novi, MI and a 956,000 sqft. property in Taylor, PA. The property in Novi, MI was built in 1988 and has clear heights of only 22’-24’.

JLL Leasing Brochure for 43700 Gen Mar Drive

Today, most tenants want clear heights of over 32’ feet. The property is available as of May 1, 2024. (See above) Given the amount of time it takes to complete a lease, it is highly unlikely this property will be leased without a period of vacancy. Based on Schedule 6.25 from the Amended Credit facility and the increase in the property’s NOI from 2021 to 2022, it looks as though this property produced $1 million of NOI in 2023.

The second property is in Taylor, PA , was built in 2000 and has clear heights of 30 feet, which would have been impressive when the property was built.

Cushman & Wakefield Leasing Brochure for 6 Kane Lane

Today 30’ is below average. The facility is leased by Kane Logistics, a third-party logistics firm. (Schedule 6.25 of Amended and Restated Credit Agreement filed with SEC on August, 19 2022.) Kane Logistics was bought by ID Logistics, a French logistics firm in 2022. ID Logistics has three distribution centers in Scranton. I believe they decided GOOD’s property was the least attractive; hence, they are letting the lease expire. Based on Schedule 6.25 from the Amended Credit Facility filed with SEC on August 19, 2022, and the increase in the property’s NOI from 2021 to 2022, it looks as though this property produced $3.6 million of NOI in 2023. I suspect it will take time to find a user that wants almost a million square feet of space near Scranton, and a new tenant will no doubt ask GOOD to pay for significant improvements. Therefore, I believe this property will be a drag on GOOD’s earnings in 2024 and possibly beyond.

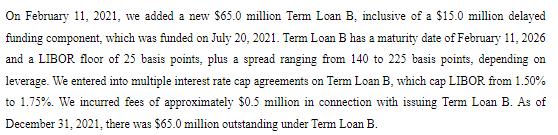

While GOOD only has $15 million of mortgages maturing in 2024 (4Q23 GOOD Investor Financial Supplement), I believe it is still exposed to higher rates as I think $65 million in interest rate caps it put in place in 2021 will expire this year. As described in GOOD’s 2021 10K, multiple interest rap cap agreements were used to limit GOOD’s exposure to rising rates on its $65 million Term Loan B.

GOOD 10K 2021 p. 79

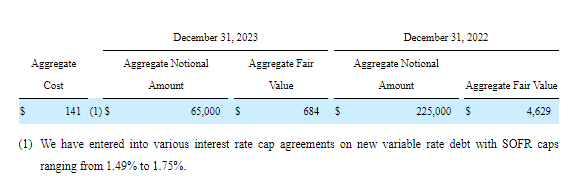

Based on GOOD’s disclosure on their interest caps and specifically their low Aggregate Fair Value, in its most recent 10-K, it looks as though these interest rate caps will expire in the first half of this year.

GOOD 10K 2023 p. 78

The notional amount of the interest rate caps is $65 million and their rate is 1.49% to 1.75%. Both items match the Term Loan B from 2021. The highest interest caps at 1.75% are saving GOOD over 3.5% versus SOFR which is currently at 5.31%. My math indicates the savings on the caps at lower levels are even more valuable. I believe the Aggregate Fair Value of $684,000 indicates an expiration relatively early in 2024. Saving 3.5% on $65 million over the course of a year would be worth $2.275 million, based on my math. However, the table above shows an Aggregate Fair Value that is only slightly more than a quarter of the annual savings. This implies, in my opinion, that the caps are likely to expire early in 2Q24, and GOOD would lose the benefit of these caps going forward.

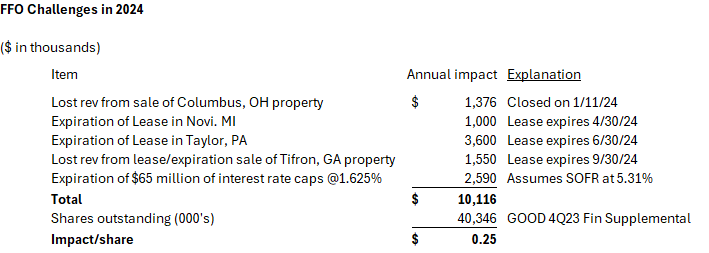

The chart below highlights some of the major items that I anticipate will weigh on FFO in 2024.

See above for leasing brochures, GOOD 2023 10K and Amended Credit Facility Filed on 8/19/22

While not all of these items will impact FFO in the next quarter or two, I think as analysts and investors begin to focus on 2025 numbers for valuation purposes in the coming months these items will begin to hit their radar screen. Given that consensus, the FFO estimate for 2024 is only $1.38. A $0.25 hit-to-run rate FFO would be very significant for GOOD’s valuation.

I do not see GOOD’s dividend coming under pressure in the next quarter or two. Nonetheless, the stress on the business model from both an FFO/share and liquidity perspective is continuing to grow.

When GOOD cut its dividend at the beginning of 2023, I believe it was hoping to use the extra retained cash flow for the acquisition of industrial properties. Instead, it looks to me as though the bulk of the savings was simply used to cover the difference between GOOD’s dividend (at the new rate) and free cash flow as I outlined above. I think they will face similar issues in 2024. On December 31st, 2023 GOOD had available liquidity of $56.5 million consisting $12 million in cash and cash equivalents and $44.5 million in borrowing capacity. (GOOD 2023 10-K p. 47.) By February 22, the date of their earnings call, liquidity had dropped to $54.9 million, consisting of $3.4 million in cash and cash equivalents and $51.5 million in borrowing capacity. (GOOD 4Q23 Conference Call) This drop in liquidity took place, despite GOOD selling their Columbus, OH property for $4.5 million. (2023 GOOD 10K p. 37) Over the course of 2024, many of the same items that decreased cash flow in 2023 are likely to recur. In 2023, GOOD spent $8.9 million on property improvements and leasing commissions extending or modifying 1.4 million square feet. (GOOD 2023 10-K Cash Flow Statement and 10K p.38) In 2024, GOOD has 1.8 million square feet of expiring leases, and it is possible that, as in prior years, some leases that expire in future years will be renewed in 2024; as such, I would expect to see these expenditures go up significantly in 2024. (GOOD 4Q23 Financial Supplement p. 19) GOOD’s FFO for 2024 is also likely to include non-cash revenue associated with tenant improvements and straight-line rents as discussed earlier. Given the amortization schedule for deferred rents and tenant improvements, I would anticipate the amounts in 2024 would be similar to 2023, which I estimate to be about $3.2 million and $4.0 million respectively. (See above analysis) In my opinion, it is likely that GOOD’s FFO will barely cover the dividend in 2024. This means any non-cash revenue or expenditures that are not included in FFO will need to be funded by debt. If this is the case, I believe GOOD is going to be forced to use a significant portion of its remaining liquidity simply to fund the dividend, property improvements, and leasing commissions, which will further limit its financial flexibility in 2025 and beyond. As 2024 progresses, I think the challenges for GOOD’s model will become apparent to more analysts and investors.

It is important for short sellers to realize that GOOD is a volatile stock. It could move sharply higher based on falling interest rates, selling a non-core property for more than the market expects, signing a big lease, or other events that the market views in a favorable light. Any of these events could cause the stock spike price to spike temporarily. A short seller without sufficient capital could be forced to liquidate their position at a loss in this scenario. Additionally, GOOD will likely continue to pay its reduced dividend ($0.10/month) until its lenders tell them they need to stop. Not only does the dividend represent a cost to a short seller, I believe the dividend will put a floor on the stock price for some time as there will always be investors who are seeking yield. In other words, I believe someone shorting GOOD needs to have the patience and capital to wait until the market has a clear picture of the challenges facing the business model going forward.