Franco Ercolino

Franco Ercolino

I am revisiting my previous analysis of Gogo, Inc. (NASDAQ:GOGO), in light of Q4 and full-year 2023 earnings.

In my Q3 analysis, I rated Gogo a buy with a price target of $18.70. My buy rating was supported by the following:

Since then, Gogo is down nearly 16% while the S&P 500 is up more than 14%. This continues a downward trend, with Gogo falling more than 40% over the past year.

Gogo Price Trend (Seeking Alpha)

Despite a short-term blip from lower equipment revenue and strategic investments, Gogo's future looks as strong as ever. Cash flow is back on track in 2025 with additional upside possible from government reimbursement. The service business, a stable source of revenue, continues to grow on both the topline and bottom line. Competition also looks priced in, and Gogo still maintains a sizeable competitive advantage.

With the above in mind, I reiterate a DCF-generated price target of $18 and raise my rating from buy to strong buy due to the increased potential at the current, lower stock price.

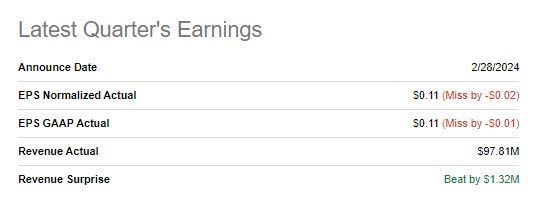

Gogo released Q4 and Full Year 2023 earnings on February 28th. Normalized EPS missed by -$0.02 and revenue beat by $1.32 million.

Gogo Earnings Surprise (Seeking Alpha)

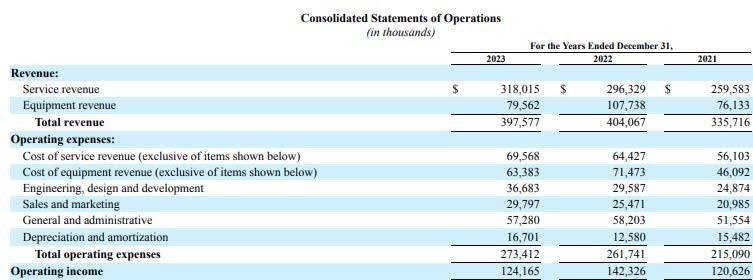

The year-over-year decrease was unsurprising due to the spike in equipment installs in 2022 following Covid. I pay much more attention to the service business, which had a phenomenal quarter, growing 5% year-over-year and 2% sequentially in addition to margin growth.

Revenue and Expense Breakout (GOGO Investor Relations)

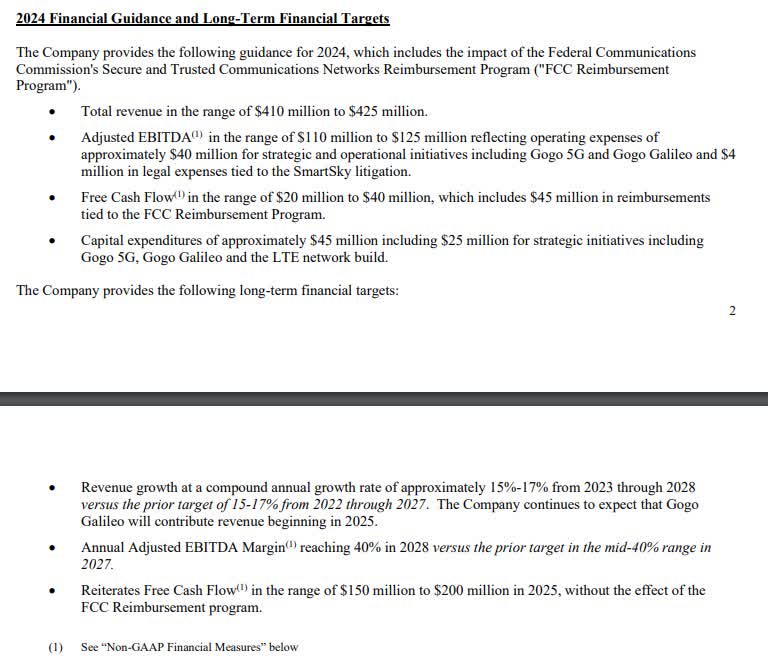

2024 and long-term guidance largely kept the company on track with prior guidance.

GOGO Guidance (GOGO Investor Relations)

Overall, it was a solid earnings report that didn't materially change the long-term prospects. Equipment revenue will continue to be volatile across quarters, but the stability of the service revenue business is the key driver of long-term cash flow. Certainly, between capital expense timing and revenue, investors had to digest a challenging set of numbers. However, this continues to be a growing business with strong demographic tailwinds.

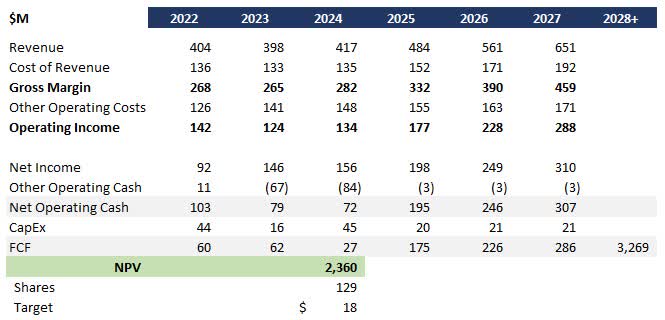

I updated my ongoing DCF analysis and, despite the near-term changes, came within $0.30 of my previous model due to the strong guidance. I made the following underlying assumptions in the model:

This analysis generated a price target of $18.40, down slightly from the prior target of $18.70.

GOGO DCF (Data: SA; Analysis: Mike Dion)

Wall Street analysts are also bullish on Gogo, although slightly less so, with a price target of $13.40.

Wall Street Rating (Seeking Alpha)

I look at Gogo's growth opportunities in two ways. First, Gogo needs to create a large customer base for its service base by installing equipment. Second, Gogo needs to take advantage of demographic trends.

As management continuously reiterates during earnings calls, revenue volatility is driven largely by the timing of equipment installs which relies on supply chain and equipment installers. This is not Gogo's core business. Their core business is providing services to people with their equipment installed.

Aside from the already solid uptick in service revenue covered above, Gogo has set up its service business for explosive growth. Instead of tying equipment to a specific service, like an old flip phone locked onto AT&T's network, Gogo is building a platform that can be quickly upgraded with software to work on multiple networks, including its new 5G network—an unlocked iPhone of the skies.

Gogo Avance (Gogo Air)

This technology can be used to upsell newer, faster services, such as the Galileo satellite network and 5G air-to-ground services. No other carrier today offers this, or is even close to offering this. It's the epitome of a monopoly service and much like telecom, equipment margins are razor-thin to support a service business where margins are sky-high (airplane pun intended).

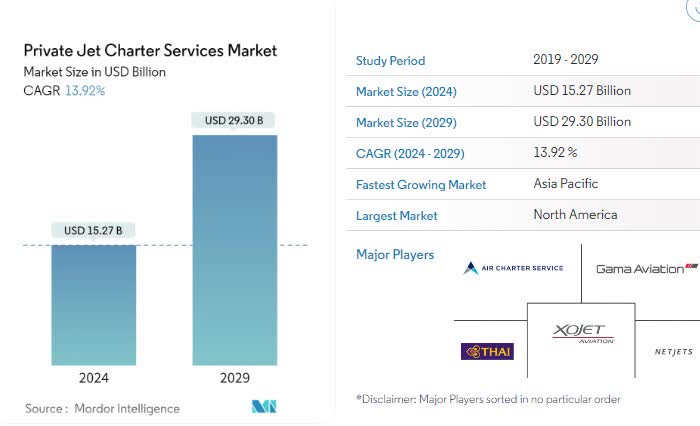

Beyond the service offering, demographic trends continue to accelerate in Gogo's favor. Private jet charter services, a key customer, are now expected to grow at a nearly 14% CAGR through 2029.

Private Jet Charter Market (Mordor Intelligence)

As younger generations turn to air travel, demand for connectivity is also increasing. Management mentioned in earnings that "all ages want better in-flight connectivity, demand for connectivity increases as the flyer age decreases." From Q3 earnings, the demand was noted as follows:

This played out in Q4, when data usage spiked 15% from the prior year and 74% from 2019. And penetration in the space continues to be low. More than 70% of private planes do not have internet today, and Gogo is the only provider with equipment that fits on turboprops and small jets.

Higher-margin services, plus increasing demand plus low penetration, easily support management guidance over the next five years.

Competition from Starlink is the primary downside risk to Gogo's business. No other competitors are close to launching a similar product at this time. A lot of time was spent on this topic in the earnings call, with the following key call-outs:

The good news is that some competitive activity is baked in. Of course, Starlink could exceed expectations and take a bigger share. On the flip side, they may not even choose to enter the space.

The secondary risk to Gogo's business is a downturn in the private jet industry. While unlikely given the growth projections mentioned above, it's always a risk when serving a single market.

I believe that the market continues to look down on Gogo due to the volatility in its equipment business and the slow roll-out of 5G. This was compounded in Q4 due to a sharp drop in revenue year-over-year.

However, Gogo's service business continues to post strong growth and Gogo Galileo is nearing the finish line. Gogo has all demographic trends working in their favor and today they have no competitors. There is competition risk in two years from Starlink, although they have made no formal announcement, but Gogo management has included this in guidance.

With strong fundamentals, a DCF generated price target of $18.40 and a suppressed stock price, I raise my rating from buy to strong buy.