LSOphoto/iStock via Getty Images

LSOphoto/iStock via Getty Images

Global Medical REIT (NYSE:GMRE) is an internally managed REIT focusing on healthcare facilities which are leased out to physicians and other healthcare-related groups.

GMRE Investor Relations

The REIT owns 185 buildings in 34 states with a 5.8 year WALT. Unlike other healthcare REITs, Global Medical’s tenants appear to be well-managed, as the portfolio rent coverage ratio exceeds 4. A strong ratio, but this excludes the tenants where the data was not immediately available (representing 17% of the rental income). About 20% of its annualized base rent is up for renewal in 2024 and 2025, so it will be interesting to see the lease spreads on lease renewals. Also, an important feature: about 41.5% of its annualized base rent is only up for renewal from 2030 on, so the visibility on future rental income and cash flows should be pretty strong.

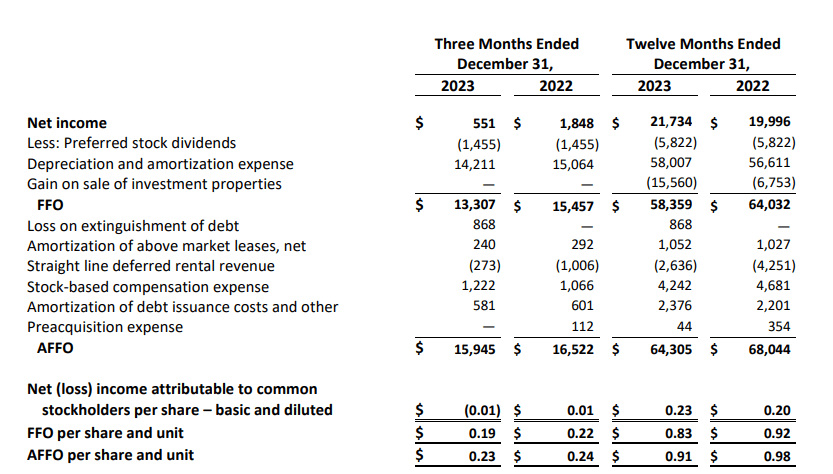

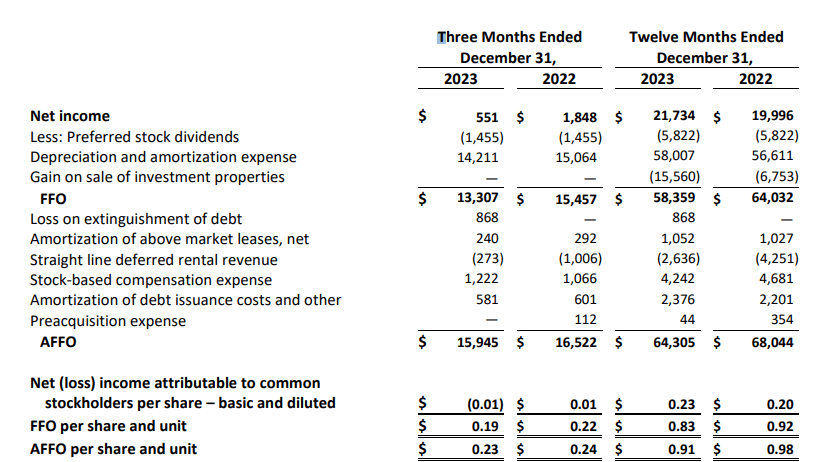

As the reported net income is relatively irrelevant for a REIT, I wanted to dive right into the FFO and AFFO performance. As you can see below, Global Medical REIT announced a total FFO of $13.3M in the fourth quarter of the year while the total AFFO was approximately $15.9M after adding back the value of the stock-based compensation and some other non-cash and/or non-recurring items.

GMRE Investor Relations

So while the bottom line of the income statement shows a net loss of $0.01 per share, Global Medical’s FFO and AFFO came in at $0.19 and $0.23 per share respectively.

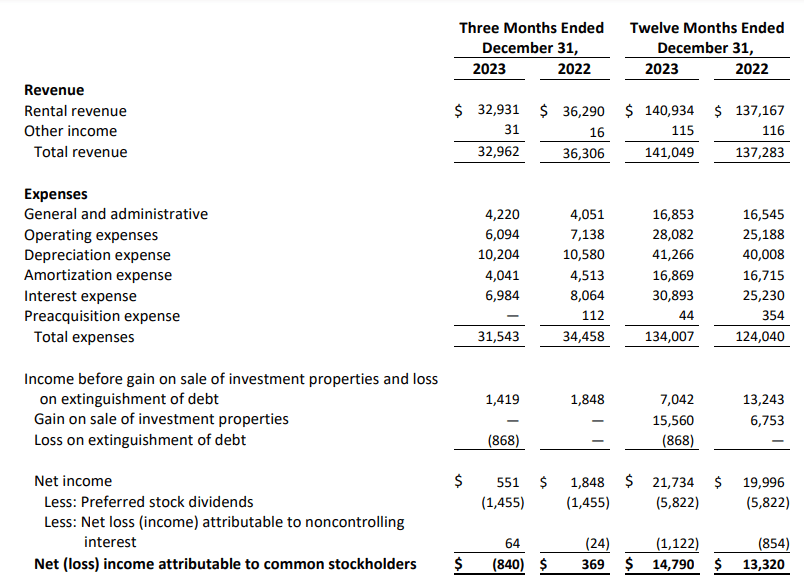

Looking at the REIT’s full-year result, the total AFFO was approximately $64.3M for an AFFO/share of $0.91. You immediately see that’s respectively approximately $3.7M and $0.07 per share lower than in 2022, but that’s not necessarily a big issue. First of all, although the interest expenses were lower in Q4, they were substantially higher throughout 2023 as the full-year interest expense came in at almost $31M compared to just over $25M in 2022. The interest expenses decreased in the fourth quarter to an annualized run rate of just around $28M, but the lower interest expenses were directly related to asset sales during Q2 and Q3. And selling assets obviously weighs on the rental revenue.

GMRE Investor Relations

So while the FFO and AFFO decreased during 2023, the REIT has actually become safer. In March, it sold a $4.4M medical office building including a $0.5M gain, while the two sales in June and August for a total of $76.1M including a gain of $15.1M.

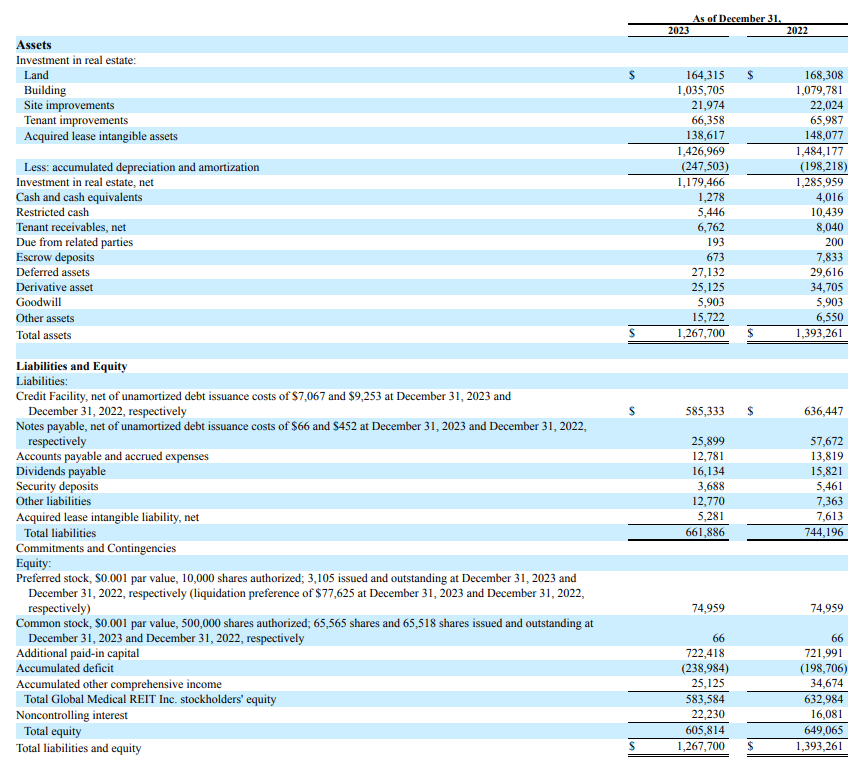

Needless to say, those sales provided a nice boost to the balance sheet. As you can see below, the total book value of the remaining real estate assets was $1.18B but more importantly, the total financial debt decreased from almost $695M to $610M. If we would also deduct the almost $7M in cash and restricted cash from the equation, the net debt was just $598M, representing 50.7% of the book value of the assets. That book value already includes almost $250M in accumulated depreciation.

GMRE Investor Relations

If we would use the book value of the assets, the existing equity value of just under $584M provides an excellent safety net for the preferred shares. As you can see above, there are only 3.1M preferred shares outstanding and the principal value of $25 per preferred share indicates the total amount of preferred capital is $77.5M. This means there is almost $510M in common equity that ranks junior to the preferred capital. Or in other words, even if Global Medial REIT would have to sell all of its assets at a 40% discount to the book value, the preferred shareholders would still be made whole.

The preferred shares are trading with [[GMRE.PR.A]] as ticker symbol and offer a cumulative dividend of $1.875 per year, payable in four equal quarterly installments of $0.46875. The preferred shares can be called at any time, and I had expected the REIT to call them in 2022. Global Medical REIT elected to not call the preferred shares and in hindsight, that likely was a good idea as it helped to avoid the market starting to speculate against Global Medical.

I already discussed the asset coverage level but it’s obviously also important to ensure the preferred dividends can be paid. Pulling up the FFO and AFFO calculation helps to explain this.

GMRE Investor Relations

As you can see above, the Q4 AFFO was $15.95M but this already included $1.46M in preferred dividends. This means the net AFFO before preferred dividends was approximately $17.4M, which means the REIT only needed approximately 8.6% of its AFFO to cover the preferred dividends.

And looking at the full-year results, Global Medical REIT only needed approximately $9.6M of capital expenditures on its asset portfolio. This means that even if you would deduct this from the full-year AFFO of $64.3M, Global Medical REIT would still generate a pre-dividend adjusted AFFO of $60.5M ($64.3M minus the $9.6M capex plus the $5.8M in preferred dividends) which means the payout ratio remains comfortably below 10%. The capex will increase in 2024 to $12-14M, but this has hardly any impact on the preferred dividend coverage ratio.

I currently have a small long position in Global Medical REIT and wouldn’t mind adding to this position (subject to having cash available). The preferred dividend coverage ratio is pretty strong, while the asset coverage ratio indicates there is plenty of common equity on the balance sheet that is providing a safety net.

The 9.3% yielding common shares are also interesting but the additional layer of safety offered by the preferred shares is more appealing to me.