Love Employee

Love Employee

It has only been a little over a month since my last Genmab A/S (GMAB) article, where I discussed three trends that I believe investors need to track over 2024. I stressed how important it was for the global biotech juggernaut, to show growth from EPKINLY (epcoritamab) and Darazalex, as well as continue to keep the pedal down with their pipeline efforts. Although I still believe those trends are key in 2024, I wanted to point out how the company’s Annual Report for 2023 has indicated that Genmab is capable of achieving those goals and supports the company’s growth narrative.

I intend to provide a brief background on Genmab and will recap their 2023 annual report. In addition, I will point out why I believe 2023 has set the company up for continued growth in 2024 and beyond. Then, I readdress some downside risks that investors need to consider. Finally, I reveal my updated GMAB strategy to help deal with the relentless selling pressure.

Genmab's focus is on the development of monoclonal antibodies, which are engineered molecules designed to target specific proteins associated with disease courses. Over the years, the company has proven itself as a monoclonal antibody dynamo, establishing strategic partnerships with big pharma and primary biotech firms to advance innovative candidates.

Genmab's achievements have been the result of their state-of-the-art platform technology. Genmab employs exclusive technologies termed DuoBody, HexaBody, DuoHexaBody, and HexElect. These exclusive platforms support the conception of cutting-edge antibodies that have pluses over contemporary monoclonal antibodies. Thus, allowing providers some versatility and additional options in their patients’ treatment plans.

At the moment, Genmab's strategic collaborations and partnerships have been their primary source of income as they receive payments and royalties for their efforts to discover some of the most vital antibodies on the market. Genmab has partnered with industry behemoths, including Johnson & Johnson (JNJ) (Janssen Biotech), Novartis (NVS), Seagen (SGEN), AbbVie (ABBV), and Bristol Myers Squibb (BMY).

Genmab's expansive pipeline includes Darzalex, the company's flagship product, developed and licensed from Genmab by Janssen Biotech. Darzalex has not only redefined the treatment paradigm for multiple myeloma but has also secured global regulatory approvals.

Genmab Pipeline and Portfolio Overview Genmab Pipeline and Portfolio Overview (Genmab)

Genmab’s pipeline proprietary candidates and collaboration pipeline is filled with promising antibodies addressing a diverse array of cancers including cervical cancer, solid tumors, and various lymphomas, progressing through the intricate stages of pre-clinical development to Phase I, Phase II, and Phase III clinical trials.

Genmab had a strong 2023 with several positive marks from crucial clinical trials and notable accomplishments. Notably, Genmab was able to report a number of regulatory approvals for EPKINLY/TEPKINLY with their partner, AbbVie, in the U.S. and Japan. Furthermore, the company reported encouraging topline results EPKINLY from the follicular lymphoma (FL) from pivotal the NHL-1 study, resulting in regulatory submissions. Genmab and Pfizer (PFE) reported topline marks from the innovaTV 301 and innovaTV 207 studies for tisotumab vedotin. Moreover, Janssen's TALVEY became Genmab’s eighth approved medicine.

Genmab also expanded their list of collaborations with argenx (ARGX), focusing on antibodies in the fields of oncology and immunology.

Simultaneously, the company strengthened its organizational infrastructure, opened a new HQ, and expanded their R&D center in the Netherlands, highlighting their efforts to maintain a growth stasis.

Genmab's 2023 performance revealed the company was able to maintain growth across key metrics. Genmab’s net sales and royalty revenue grew thanks to DARZALEX’s net sales surging to $9.744B in 2023, a 22% increase over 2022. EPKINLY had $64M in net product sales, with the U.S. market representing $55M of the total. The royalty revenue reported an 18% increase, reaching around $2.1B, with DARZALEX and Kesimpta royalties leading the pack.

Genmab's total revenue for 2023 came in around $2.5B, a notable 14% increase over 2022. The company's OpEx surged by 33%, hitting $1.7B, due to the company's labors to advance epcoritamab, acasunlimab, and other pipeline programs, alongside efforts to enhance their manufacturing capacity. Ultimately, Genmab's reported $825M in operating profit for 2023, verifying their ability to cultivate growth while maintaining a profitable bottom line.

In terms of cash, Genmab finished 2023 with about $4.167B in cash and short-term investments, up from $3.214B at the end of 2022.

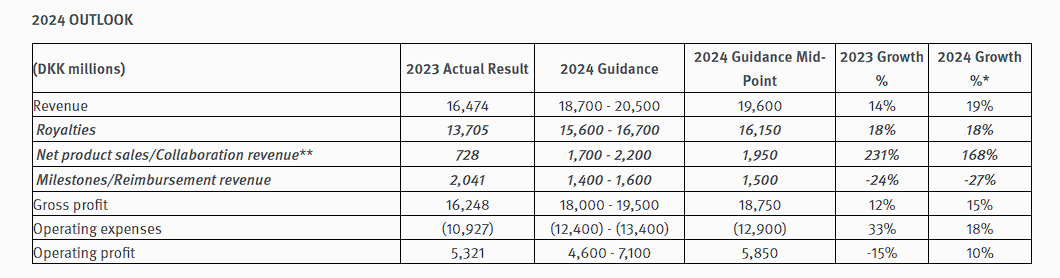

Genmab also provided their outlook for 2024, which points to additional growth and efforts to sustain innovation. Genmab projects their 2024 revenue will come in the range of $2.9B - $3.1B, fueled by net product sales, higher royalty payments, and partner revenue. OpEx is projected to be between $1.9B and $2.1B, in order to keep the pipeline moving and finance anticipated product launches. In terms of profit, Genmab expects their full-year 2024 operating profit to be between $700M and $1.1B.

Another important update for 2024, is that Genmab has initiated a share buyback program of up to 190K shares, or about $540M.

It looks as if Genmab is anticipating strong double-digit growth in revenue and gross profit in 2024.

Genmab 2024 Outlook in DKK Millions (Genmab)

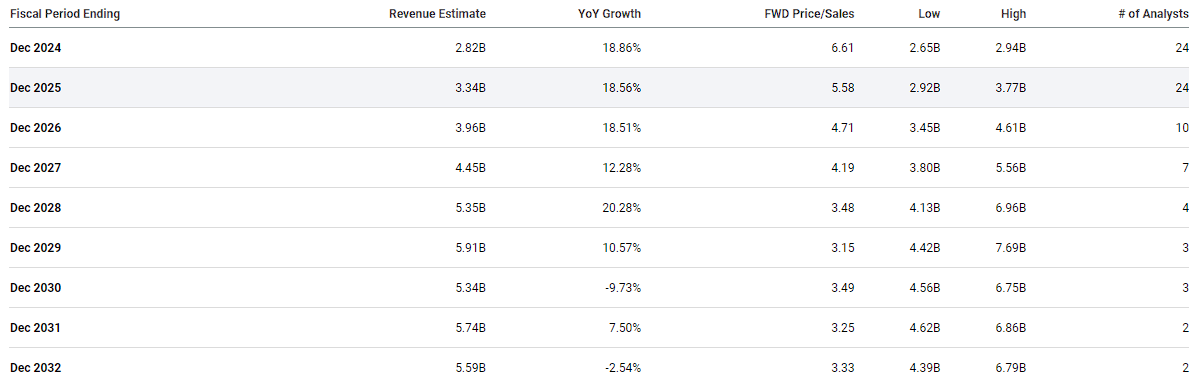

As for the Street, analysts are projecting similar results in 2024 for revenue and EPS.

Genmab Annual Revenue Estimates (Seeking Alpha) Genmab Annual EPS Estimates (Seeking Alpha)

Furthermore, the Street is forecasting Genmab to continue this growth record for the next few years for EPS and until the end of the decade for annual revenue.

Then Why Is GMAB Under Selling Pressure?

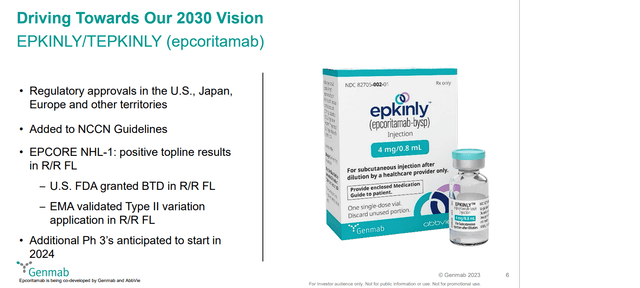

Well, I will continue to point to the negative headlines associated with the DARZALEX litigation and the Street being disgruntled over the company not getting a bigger piece of the pie. Yes, I agree that the market is not wrong in removing some of the premium off GMAB as DARZALEX's partnership peak revenues have been amputated. However, Genmab has additional growth drivers to help ease the concerns from the moderated growth trajectory. Notably, Genmab’s first wholly-owned medicine EPKINLY/TEPKINLY is now in markets outside of the U.S. and has recently secured approvals in Canada and the UK. Furthermore, EPKINLY/TEPKINLY is now in the NCCN Guidelines. Moreover, Genmab's portfolio expansion includes plans for three Phase III trials for EPKINLY/TEPKINLY this year.

Genmab Epcoritamab (Genmab)

If EPKINLY/TEPKINLY (epcoritamab) can become a foundational therapy across various B-cell malignancies, it is possible the Street can return to a more bullish outlook for Genmab in the second half of this decade.

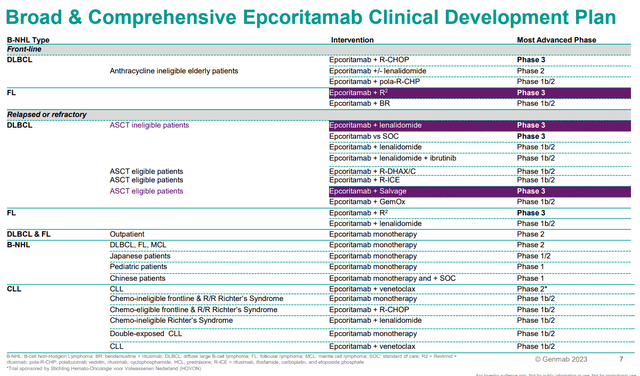

Genmab Epcoritamab Development (Genmab)

Beyond EPKINLY/TEPKINLY, Genmab's pipeline includes promising candidates such as DuoBody-CD40x4-1BB, DuoBody-EpCAMx4-1BB, and HexaBody-OX40. Genmab’s acasunlimab (GEN1046) is ready to initiate a Phase III study in second-line NSCLC. These programs are still in play, and if successful, could expand Genmab’s proprietary product portfolio, further diluting DARZALEX’s domination of the bull thesis.

While Genmab has had plenty of success, investors need to accept the innate risks associated with the biotech arena including competition, clinical trial results, regulatory challenges, IP threats, and market dynamics. These hazards could have a momentous impact on the company’s operations and long-term positions.

Genmab finds itself engaged in a notable legal skirmish with their partner, Johnson & Johnson, over DARZALEX licensing and royalties. Thus, adding a layer of complexity to the investment and growth prospects. The specifics of the legal dispute remain a focal point as investors attempt to forecast the timing of peak sales for DARZALEX, which could be the start of the downturn for the ticker. Therefore, any additional updates associated with DARZALEX and the legal battle will be a critical factor in shaping GMAB’s trajectory in 2024 and beyond.

Although Genmab is a proven company with solid fundamentals, one of these risks could be enough to cast doubt over the ticker for a prolonged period of time. However, in the face of these risks, I am still maintaining my GMAB conviction level at 4 out of 5.

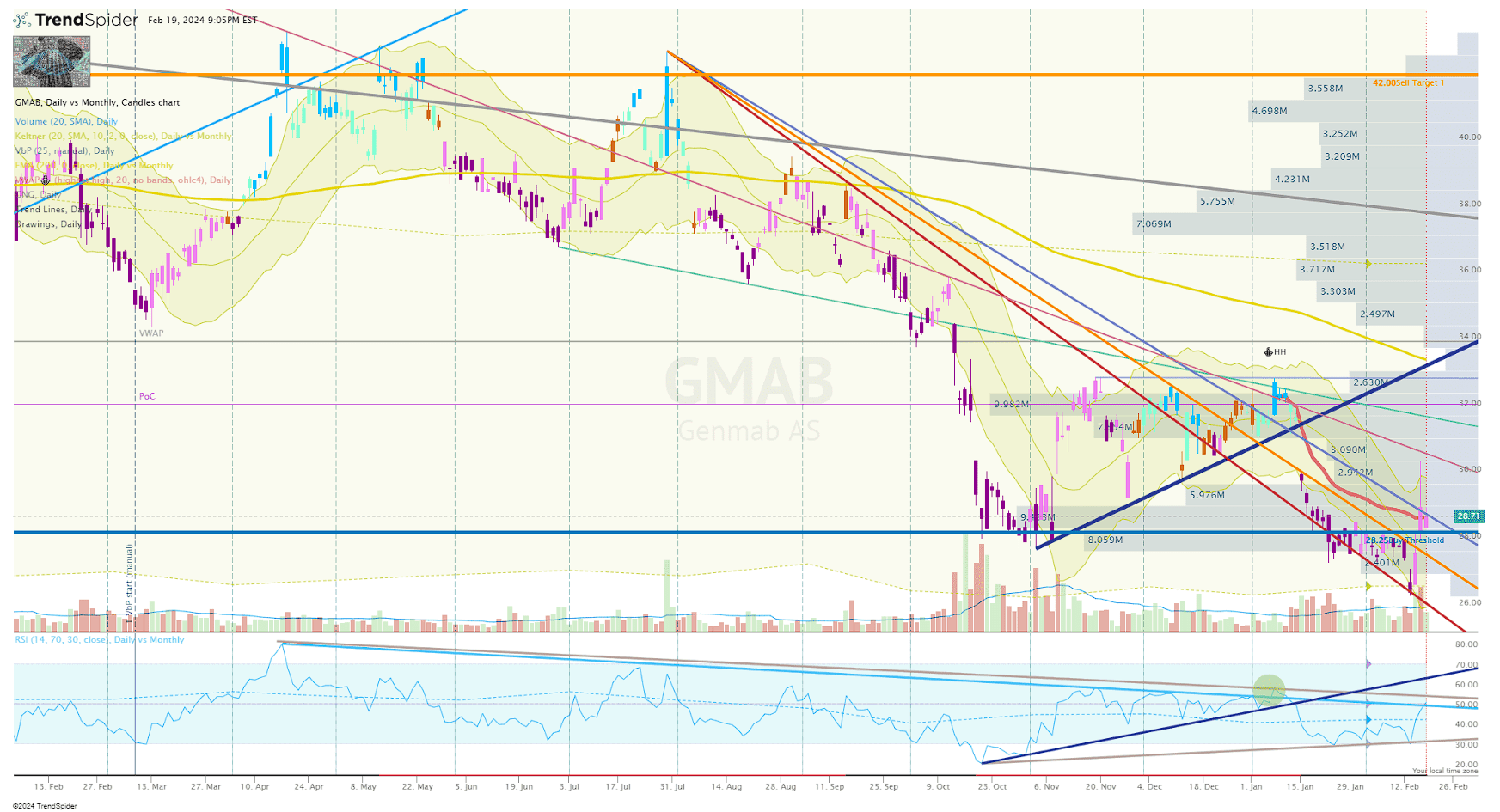

Genmab's 2023 Annual Report reveals an account of notable milestones, financial performance, and continued clinical success. However, the positive earnings were not able to create enough bullish drive to break out of the drown trend ray that dominated the ticker since July of 2023.

GMAB Daily Chart (Trendspider)

However, I do see some positive signals on the GMAB Daily chart for the longs to make note of. Firstly, we are seeing a bullish divergence in the RSI, which tends to be the initial condition of a potential reversal. In addition, we have seen a solid spike in trading volume on positive moves following the earnings, which also bodes well for a possible rebound. So, I would say some of the conditions are present for change in the tide.

Admittedly, a few bullish indicators or conditions are not enough for me to haphazardly pull the trigger on GMAB. However, I will also note that GMAB is trading near my Buy Threshold of $28.25 per share, which is the maximum price I will pay for GMAB. So, I will be looking for an opportunity to add in the coming days or weeks.

Indeed, this is how I typically manage my positions… however, I am lowering my Buy Target 1 and Buy Target 2 levels for GMAB, which are price points where I typically increase the share sizing and frequency.

Why?

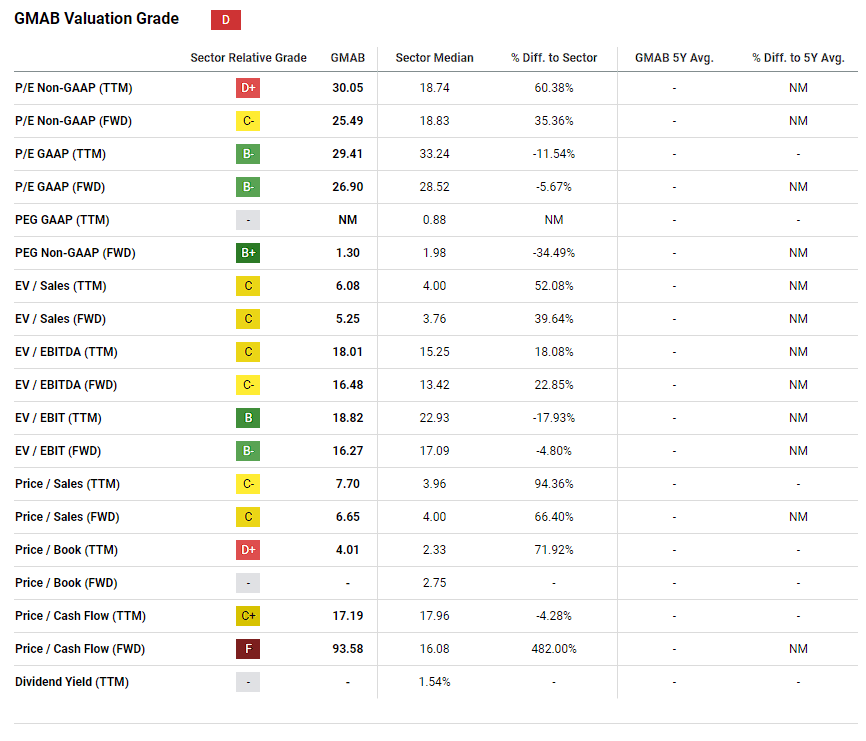

Well, GMAB’s technical rating is not appealing and the ticker is not mature enough to have resilient historical support to rely on. One might be confused about this decision, but I am simply looking at the technical conditions and accepting the path of least resistance might be lower. Plus, GMAB is still trading with a bit of premium when you look at some specific valuation metrics, which could justify a lower share price for its current state.

GMAB Valuation Grades (Seeking Alpha)

This is a rare situation where I am preparing for one of my “Top Ideas” to continue its plunge, but my bullish outlook on the company is near an all-time high.

The share buyback program should provide some support for the share price. In addition, GMAB could benefit from positive updates from EPKINLY/TEPKINLY's growth as it has shown impressive performance and secured regulatory approvals in multiple regions. Furthermore, DARZALEX continues to be a significant revenue driver that should help fund the company’s pipeline full of promising candidates to take the company into the next decade. Yet, GMAB struggles to hold any positive gains. For me, GMAB has me in that state of being “cautiously optimistic” and I will maintain this stance until positive updates produce enduring positive reactions in the share price.

Long-term, I still intend on managing the GMAB position for the foreseeable future and will carry on trading the ticker to grow a “house money” position for a long-term investment.