VioletaStoimenova

VioletaStoimenova

Globant (NYSE:GLOB) is a technology services company headquartered in Luxembourg City, Luxembourg, with operational headquarters in Buenos Aires, Argentina. Founded in 2003, Globant specializes in providing digital transformation and software development services to clients across various industries, including technology, finance, healthcare, and retail.

Globant

We believe GLOB is a fantastic business, which has exploited opportunities within its industry to gain market share and grow its brand. Whilst many of its peers have focused on the West, the company has developed rapidly in LatAm and APAC, leveraging this to then expand into the West through M&A. GLOB has built a strong foundation from which M&A has enhanced its scale and capabilities.

This translates to its financial performance, with industry-leading growth and respectable margins. We see scope for GLOB to maintain its current trajectory, illustrated by its consistent new customer wins and longtail for revenue generation at a client level.

Despite our bullish view on GLOB, we are not convinced about its attractiveness as an investment with upside. The company is trading at a FCF yield of ~2%, requiring the delivery of at least double-digit growth to create shareholder value. Given this execution risk, we are GLOB a hold.

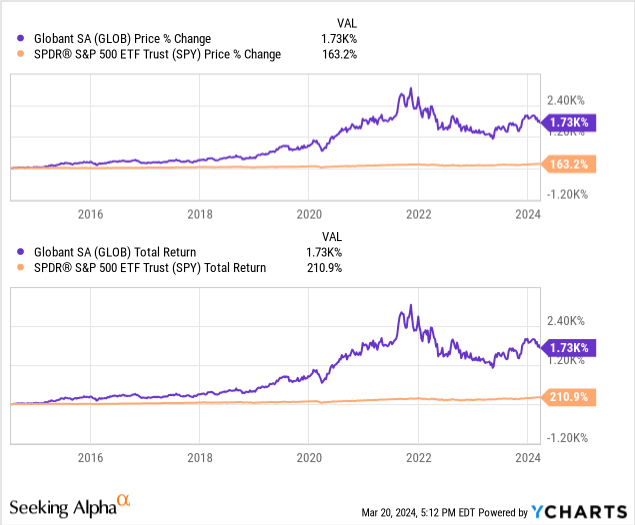

GLOB's share price performance has been exceptional, with over 1,800% returns while the S&P500 has achieved ~150%. This is a reflection of its impressive financial performance, alongside the expectation of considerable future accretive gains.

Capital IQ

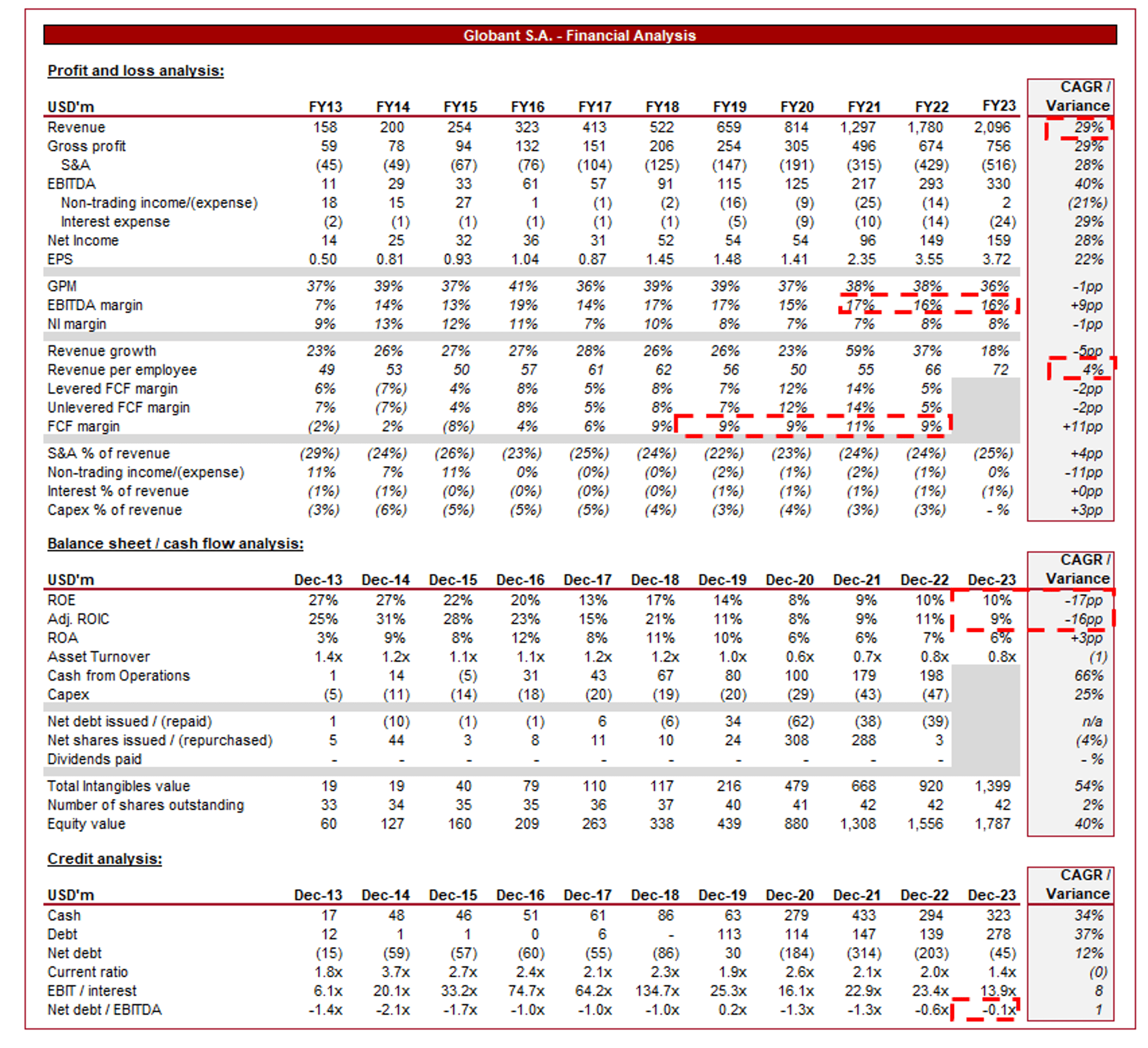

Presented above are GLOB's financial results.

GLOB's revenue has grown at a CAGR of +29%, with its lowest YoY growth rate being 23%. As if this was not impressive enough, its EBITDA growth has exceeded this at +40%.

Globant

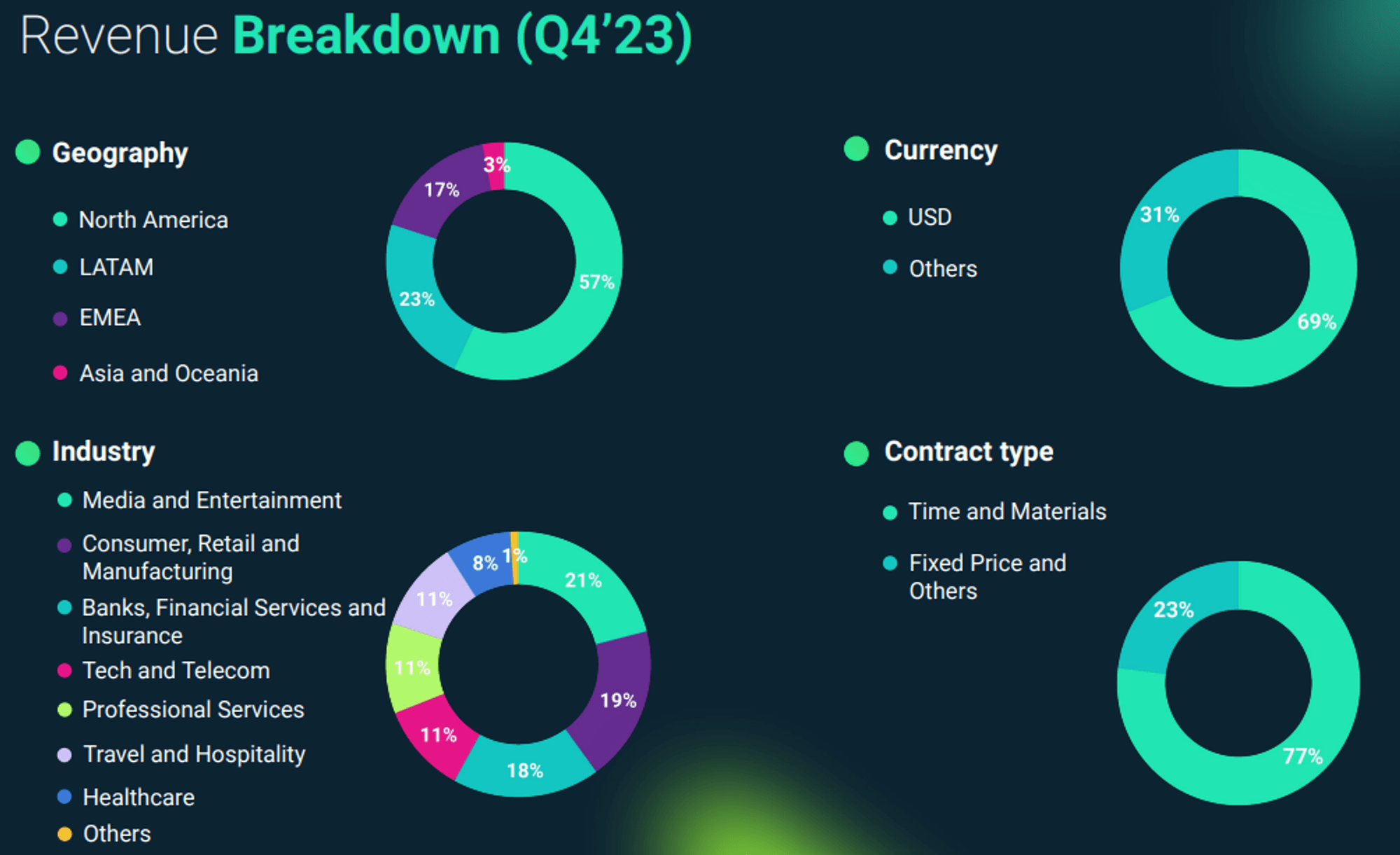

GLOB specializes in providing digital transformation services to clients globally, albeit has a larger market presence in the Americas. It offers a range of solutions encompassing digital strategy consulting, user experience (UX) design, software development, and implementation of emerging technologies such as artificial intelligence (AI), blockchain, and cloud computing. These segments have experienced considerable growth during the last two decades as digitalization infects all aspects of society. As the complexity of these technologies increases, the dependency on consultants has grown, lifting demand for GLOB's services.

Whilst this partially explains GLOB growth, it clearly is not the reason for its >25% trajectory. We believe GLOB's focus on non-western regions, namely LatAm and APAC, cannot be understated. The biggest barrier to growth in this industry is competition, which is lower and less formalized in these regions, allowing GLOB to gain market share. In addition to these factors, we believe GLOB's approach to its work, which we will discuss now, also differentiates the business relative to its peers.

GLOB adopts an industry-focused approach, tailoring its services to meet the specific needs and challenges of clients across various sectors, including banking and financial services, Media, retail, and technology. Its development of industry specialism, through strategic acquisitions and senior recruitment, has allowed GLOB to foster long-term relationships with multinationals.

GLOB operates through a network of "studios," each specializing in different technologies, methodologies, and industry verticals. These studios act as specialized units within the organization, fostering innovation, collaboration, and expertise in specific domains while leveraging synergies across the entire company. The consulting industry can be seen as commoditized by some, in that with access to public information and the internet, consultants will all come to the same idea. While this argument has merit, life is a lot more complex and so differentiation through ideas and knowledge is critical to this industry.

Globant

As a fast-growing disruptor, GLOB has prioritized talent acquisition, development, and retention as key pillars of its business model. It attracts top-tier professionals across disciplines, fostering a culture of innovation and excellence. We consider this an underappreciated strategy within talent-driven industries such as consulting, with industry relationships and expertise allowing each senior staff recruited to mirror the acquisition of a business. With its brand now developed, it is far easier to execute this while also acquiring top-tier junior talent to train.

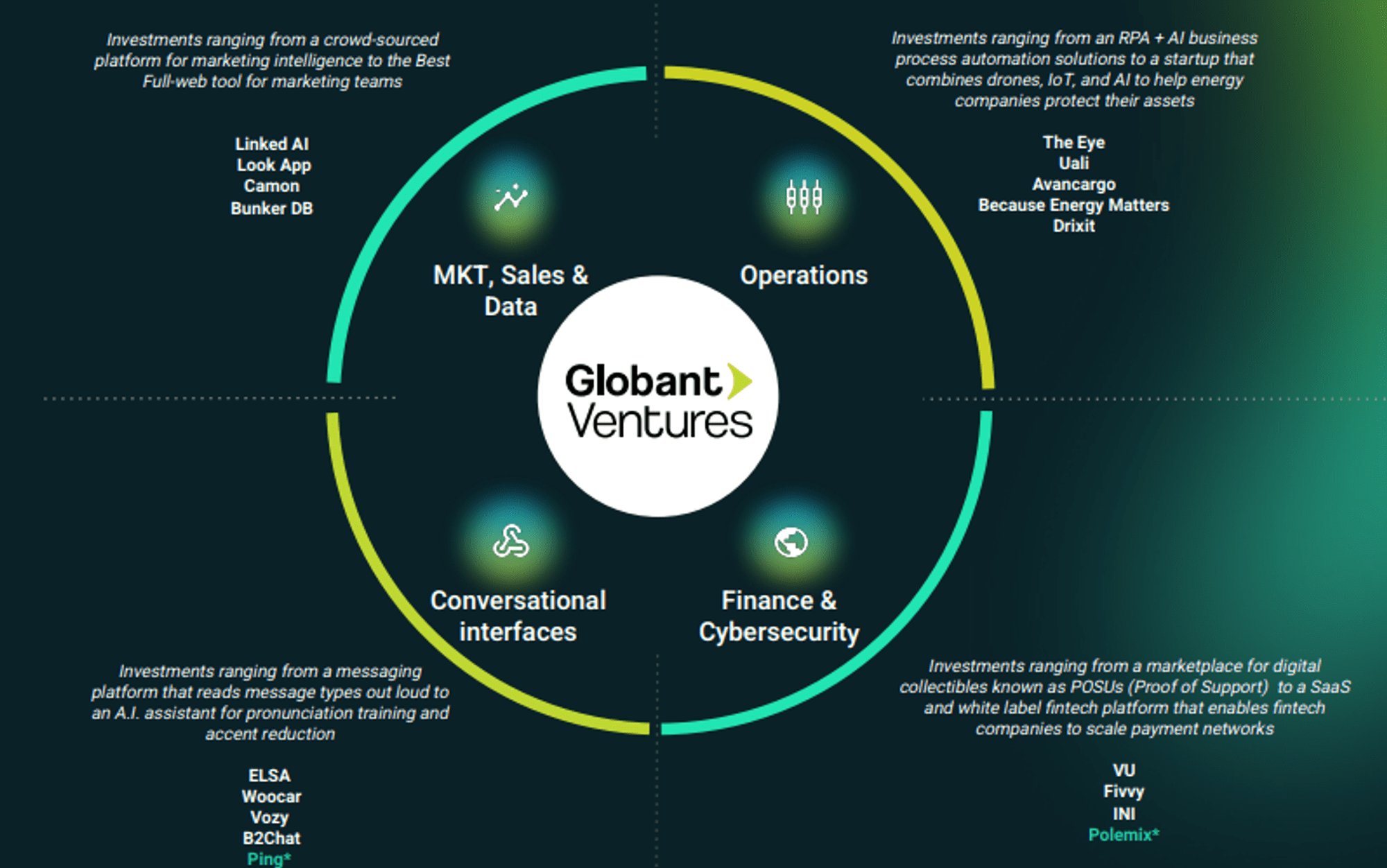

In addition to client projects, GLOB develops proprietary digital platforms and products aimed at addressing market needs and driving innovation. These platforms encompass areas such as AI-driven customer experience (CX), digital marketing, e-commerce, and workplace collaboration, offering additional revenue streams. This is a different approach from many of its peers, allowing for higher margins and more consistent revenue generation (less reliant on project wins).

Alongside delivering quality work, recruiting connected individuals, and marketing efforts, the business collaborates with leading technology providers, academia, startups, and industry consortia to access cutting-edge expertise, leverage emerging technologies, and grow its brand. These strategic partnerships enable GLOB to enhance its service offerings as most potential clients will look for relationships between its potential consultant and institutions/software providers to ensure the necessary expertise is available.

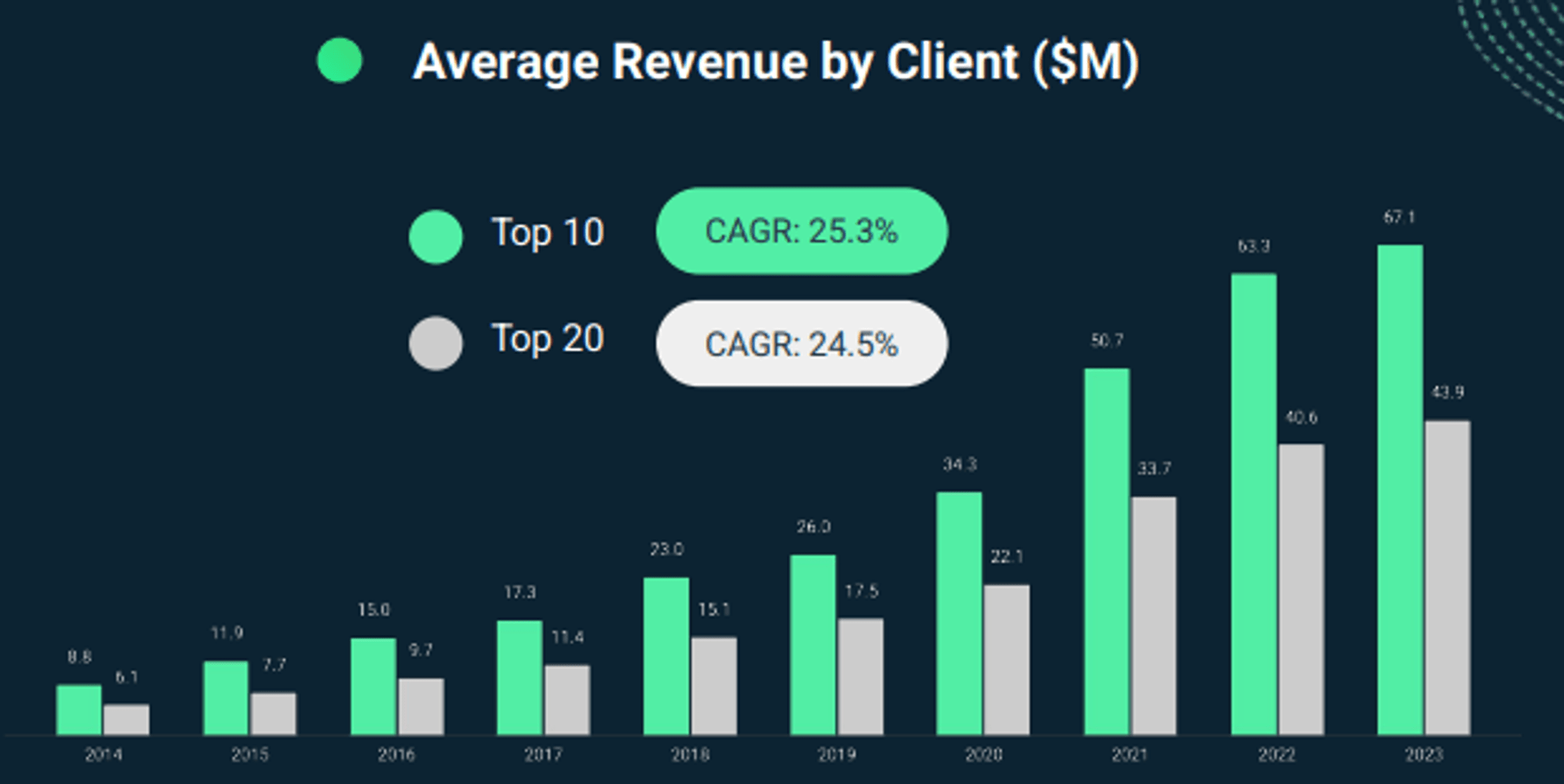

We believe the following financial metrics perfectly illustrate the factors discussed. GLOB has shown an impressive ability to upsell its existing customers over time, reflecting both the happiness of its clients within existing services and GLOB's breadth of services. This longtail enhances the lifetime value of its clients and thus runway for growth over time.

Globant

GLOB's recent performance has been strong, with top-line growth of +17.7%, +15.9%, +18.8%, and +18.3% in its last four quarters. Alongside this, margins appear to have stabilized. This is a reflection of "business as usual", with continued new customer wins and upselling, alongside expansion into new markets. Management continues to execute against its strategic imperatives to gain tangible market share, with limited evidence to suggest the company is moving toward maturity.

Supporting this growth has been M&A, with the acquisition of GUT contributing to its financial results in Q4. GUT is an independent creative agency, bolstering GLOB's capabilities in this segment and further broadening its offering.

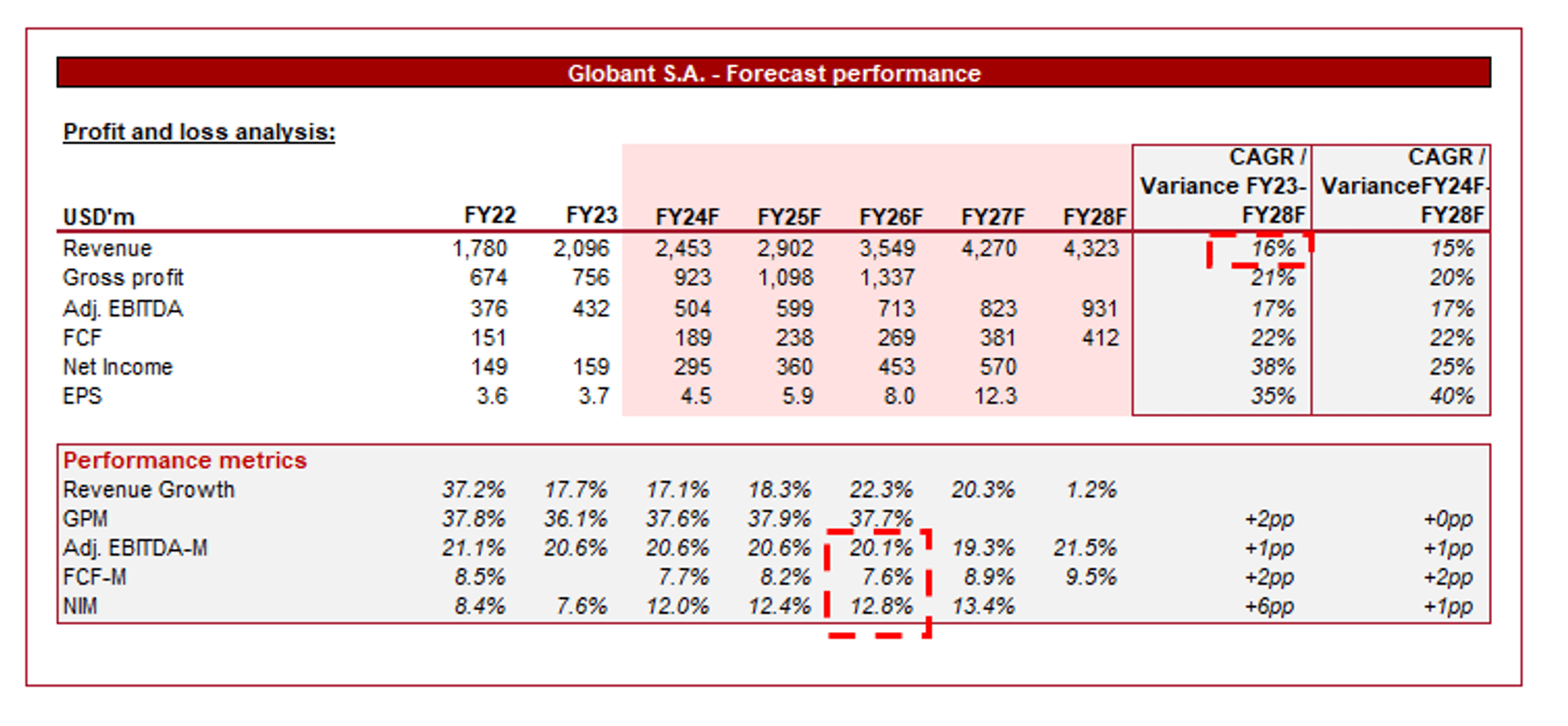

Looking ahead, we suspect GLOB can maintain its current ~15-20% growth trajectory, as industry tailwinds and continued execution deliver market share growth. We do believe there are heightened risks associated with this given the level of market share gained, as GLOB could quickly "hit a wall" in its pursuit of more growth. At revenue of ~$2b, we are not overly concerned.

Analysts are forecasting a growth rate of 16% alongside flat margins, which we consider reasonable. Whilst margin appreciation would be preferable, GLOB must maintain competitive pricing and retain talent to ensure growth.

Capital IQ

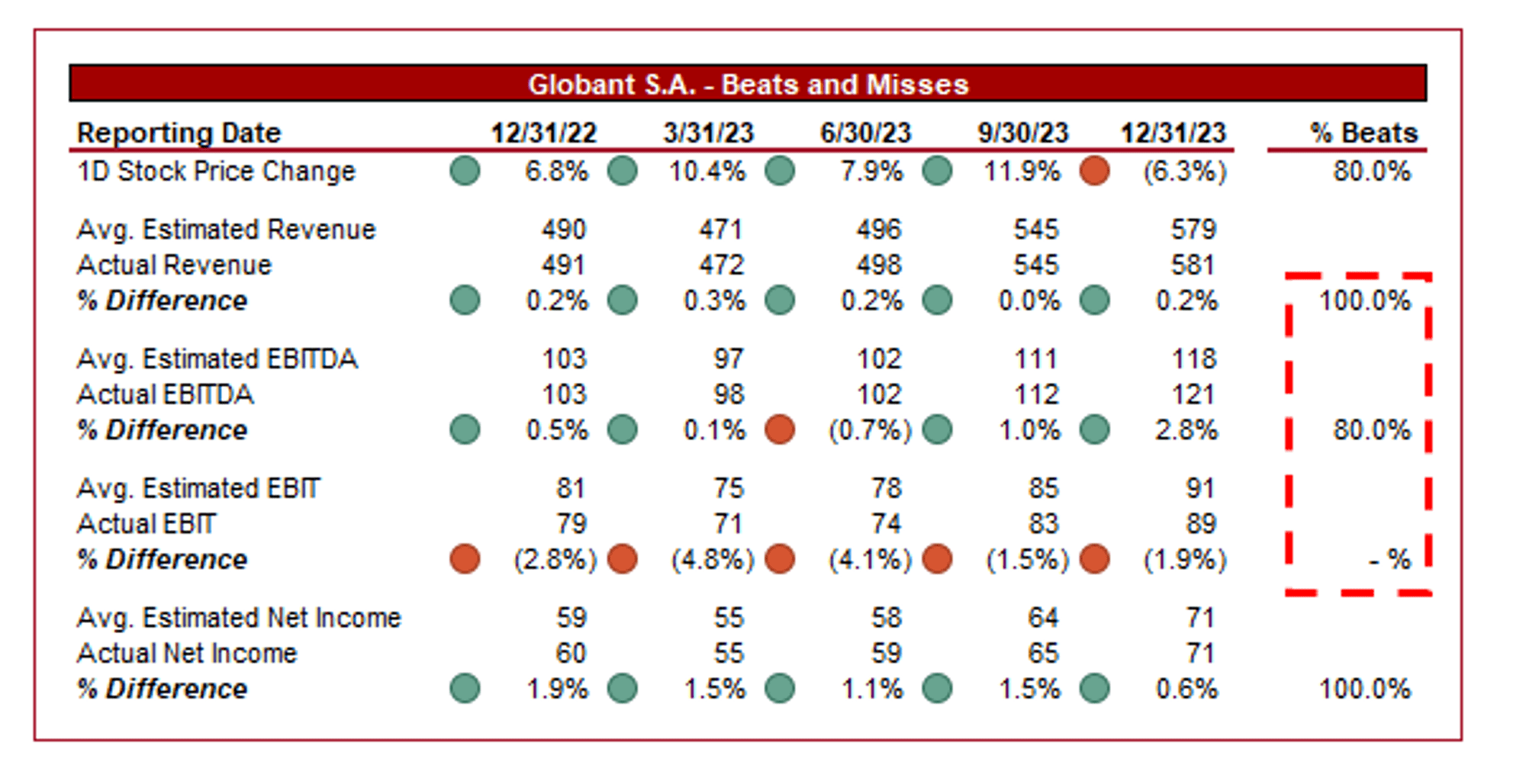

Analysts have broadly been accurate with forecasts, owing to the contractual nature of GLOB's services and the consistency with which it is able to win new contracts.

Capital IQ

We believe the following will allow GLOB to maintain and potentially expand its current growth trajectory:

Globant

Globant

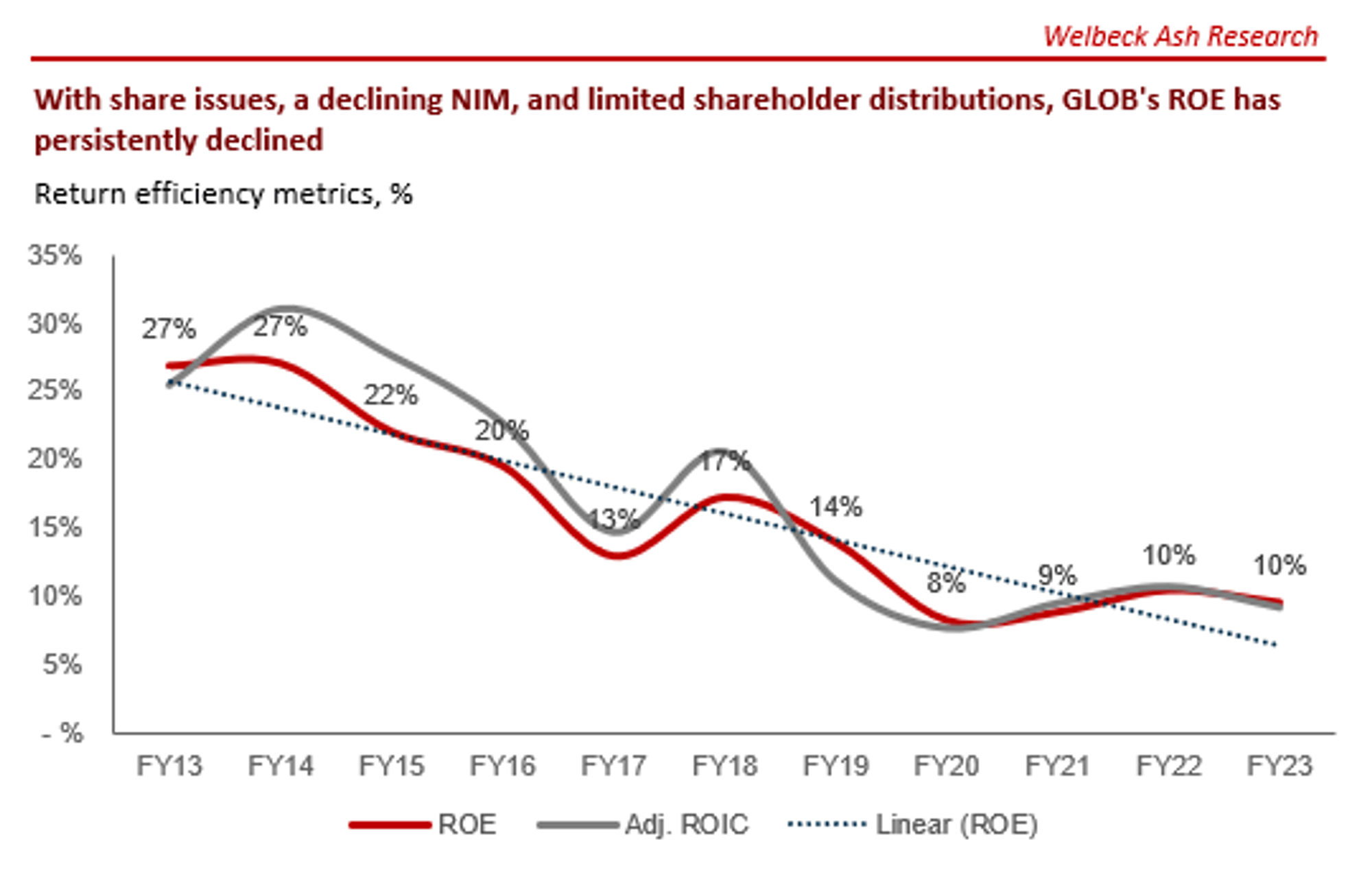

Whilst we are supportive of GLOB's M&A strategy, it has contributed to a decline in the company's ROE, implying it has been dilutive relative to incremental returns. When ROE exceeded 20%, this was less of a criticism but at a ROE of 10%, investors may feel they are better at allocating capital than Management.

Capital IQ

Seeking Alpha

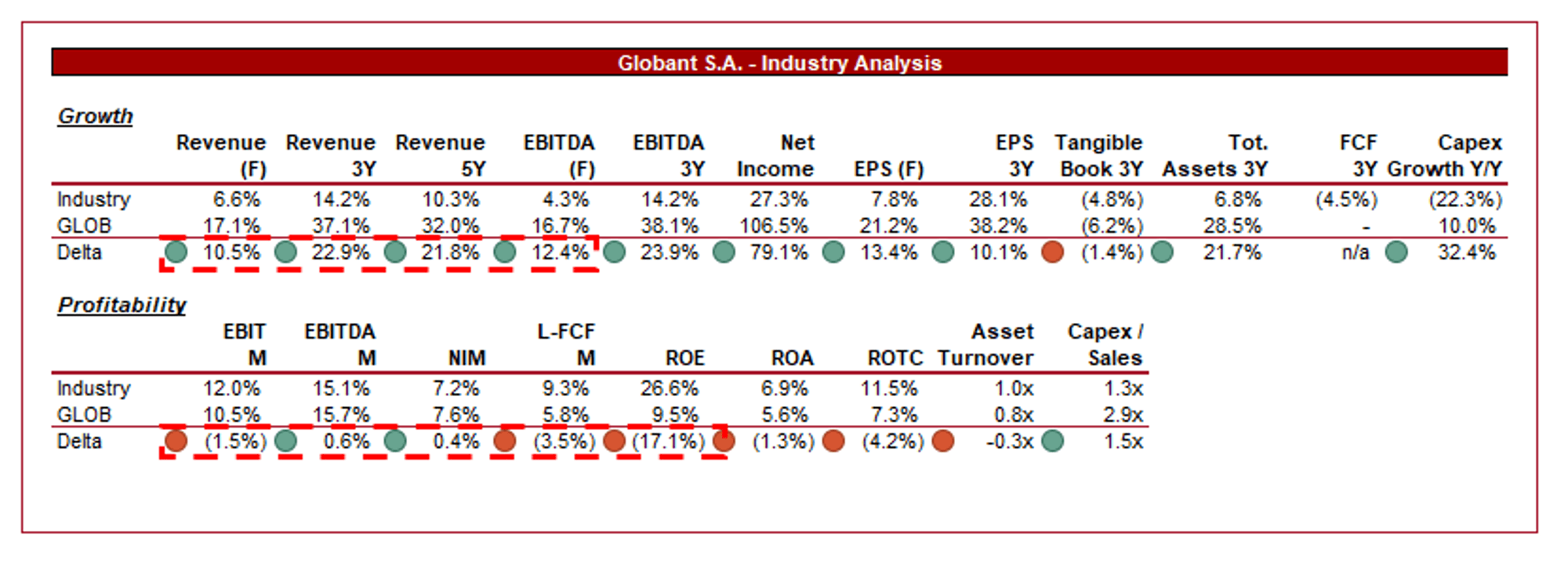

Presented above is a comparison of GLOB's growth and profitability to the average of its industry, as defined by Seeking Alpha (20 companies).

GLOB performs well relative to its peers. The company has noticeably better growth while boasting comparable margins. We attribute its growth superiority to its go-to-market strategy and differentiated approach to its operations. With the company already aligned with its peers on margins with better growth potential, we are comforted that its position can at least be maintained.

Capital IQ

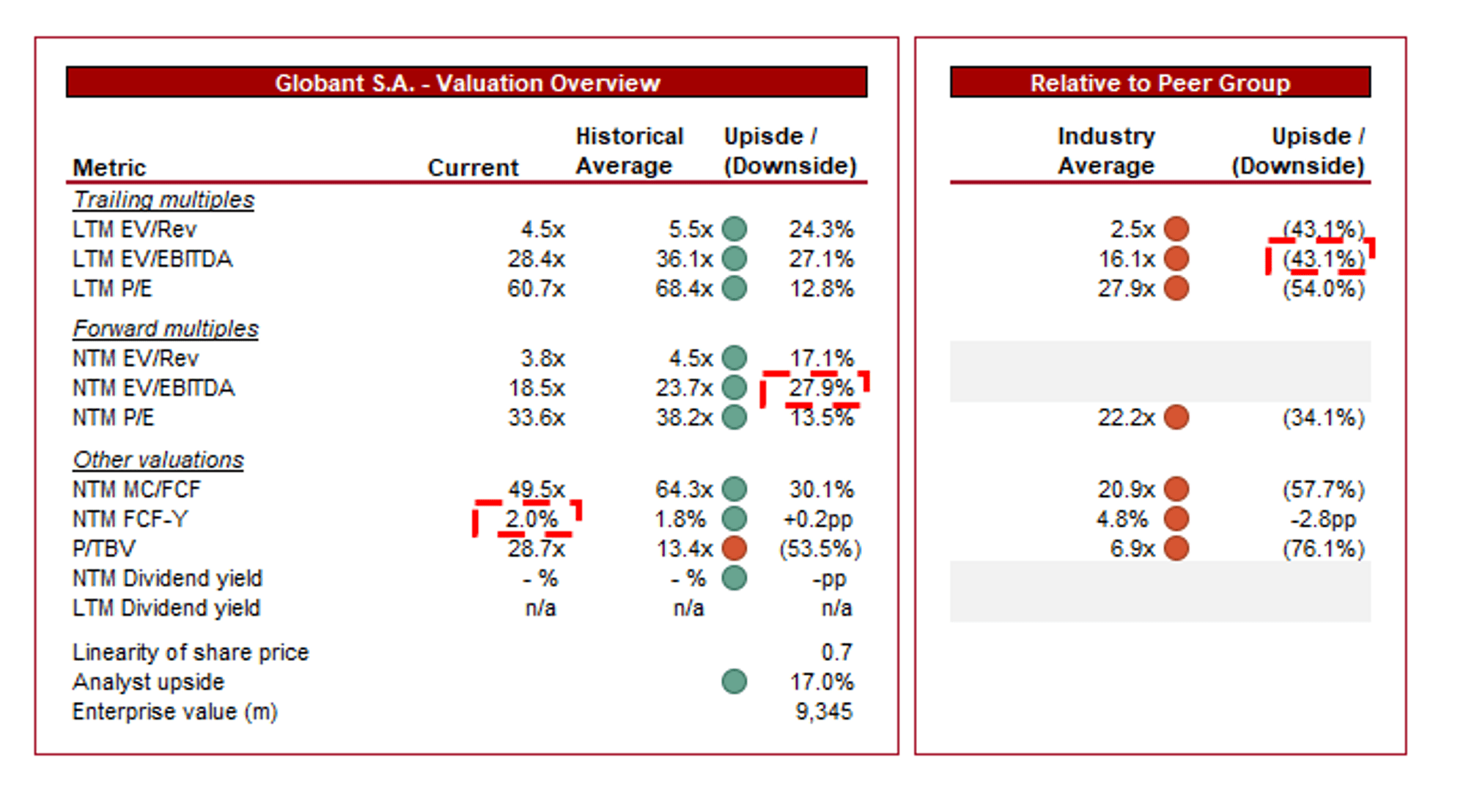

GLOB is currently trading at 28x LTM EBITDA and 19x NTM EBITDA. This is a discount to its historical average.

A discount to its historical average is reasonable in our view, owing to its slowing margin improvement and deceleration of growth rate below 20%. Whilst this is not overly problematic from an absolute basis, investors between 2020-2022 priced in a higher trajectory. A discount of ~30% on an EBITDA basis appears reasonable.

Further, GLOB is trading at a considerable premium to its peer group, namely ~43% on an LTM EBITDA basis and ~34% on a NTM P/E basis. This is a punchy valuation, which prices in strong growth in the coming years. Reflecting this is its NTM FCF yield, which is only 2% and so can only yield alpha if growth is sufficient to uplift this.

With limited immediate scope for margin improvement, we believe GLOB is likely trading at its fair value, given the execution risk associated with delivering purely growth to drive value. We do not believe GLOB is a good risk-adjusted investment today.

The risks to our current thesis are:

GLOB is an impressive business. Looking at its industry from a purely theoretical perspective, GLOB should have almost zero chance of delivering what it has. The industry is comprised of several established global names, alongside expert boutiques, which together means impressive growth is unlikely and outsized margins are unlikely. Yet GLOB has thrived and continues to do so at an impressive scale. This can only be attributed to Management's ability to do things differently and identify areas to exploit.

Whilst we do believe its ~15-20% forecast growth rate can be maintained, it would be foolish not to appreciate the risks associated with this given the fundamental characteristics of the industry. GLOB's valuation does not leave investors with much margin for error, which is the reason for our hold rating.