Cicy

Cicy

Global-e Online Ltd. (NASDAQ:GLBE) is a company providing a platform to help retailers and brands with end-to-end e-commerce solutions, ranging from big data analytics, localisation, to logistics.

Share performance has been relatively moderate since going public in 2021 at the price of $26.8 per share. It reached a peak of $80 per share later in the same year, though the stock trended down to the $30 level and moved sideways for most of 2022 and 2023. Today, GLBE is trading at $34 per share, up 21% over the past year, though down -12% YTD.

I initiate my coverage with a buy rating. My 1-year price target of $41.3 presents an 18% upside from $34.7 today.

YCharts

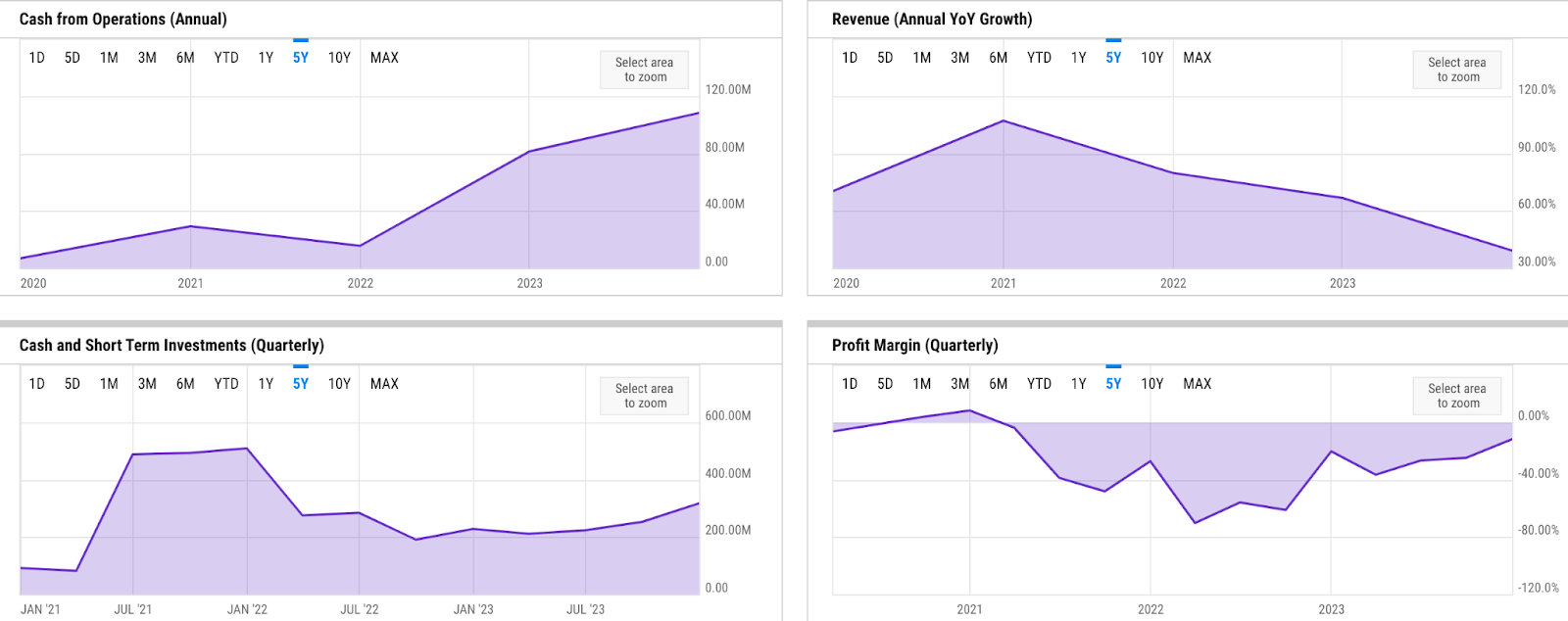

GLBE's fundamentals are relatively decent and improving. While revenue growth has normalized from over 100% in 2021 to 39% as of FY 2023, GAAP losses have narrowed. In FY 2023, the net loss margin was -23%, already narrowing from -48% the prior FY. Furthermore, the slowdown in revenue growth has also been offset by the uptrend in operating cash flow generation / OCF. In FY 2023, GLBE generated over $108 million of OCF, almost 7x higher than in 2021, when GLBE went public.

Balance sheet is relatively solid. GLBE raised $375 million in its IPO in 2021, and despite using the proceeds extensively the following year, partly for an acquisition of a cross-border e-commerce platform Borderfree, GLBE's improving OCF has helped maintain a steady and improving cash outlook. In FY 2023, cash and short-term investments even increased to $317 million, up from over $200 million the prior year. Another positive thing I have noticed is that GLBE has no debt.

In my opinion, there are some potential catalysts that could help GLBE achieve its goal for FY 2024, which is to deliver a 30% GMV and revenue growth. These catalysts include Shopify Market Pro / SMP integration and a sustained growth in demand for cross-border e-commerce.

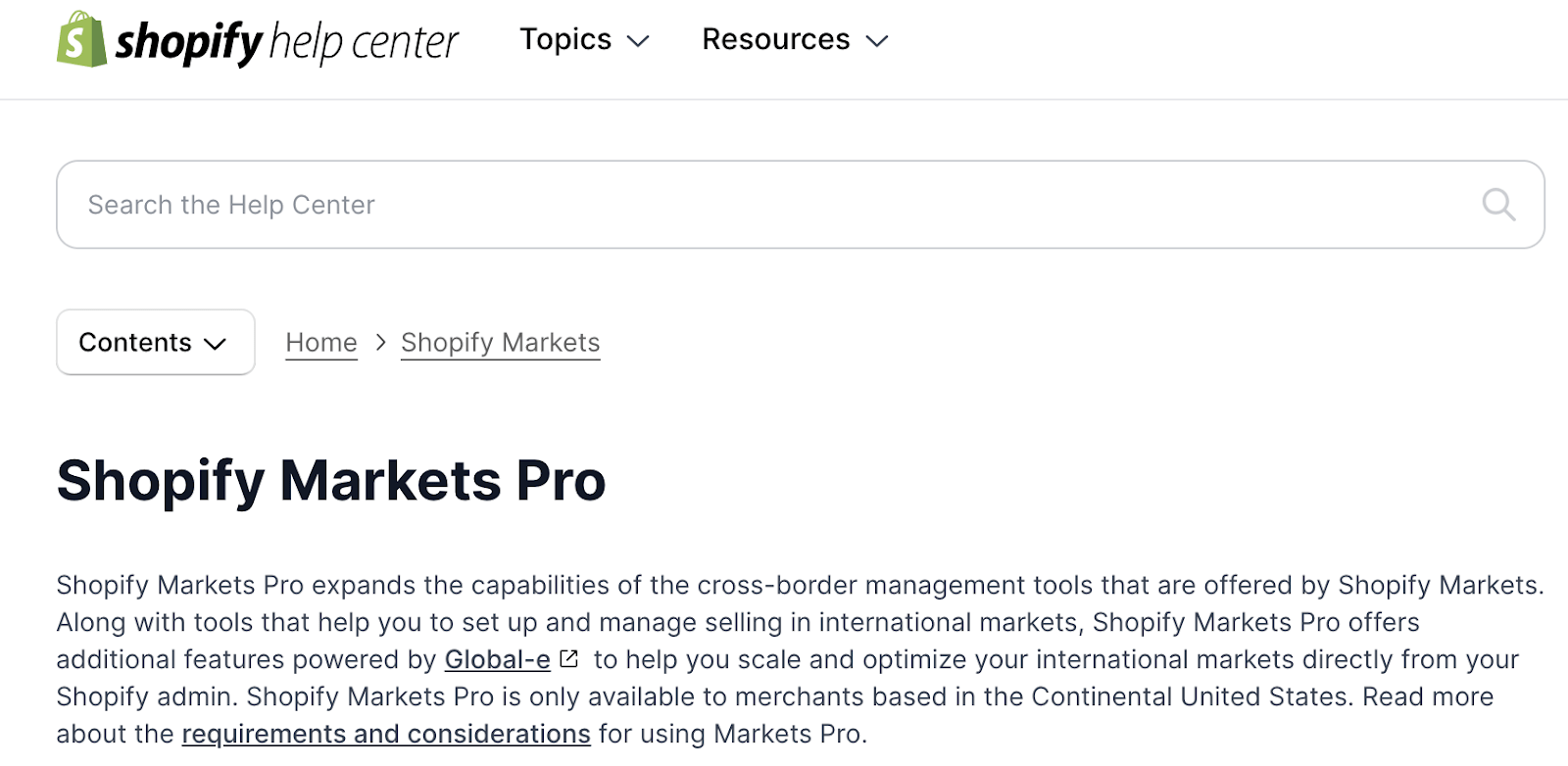

Having only been launched in September last year, I believe SMP integration is a strategic initiative that could bring in not only attractive future revenue growth opportunities for GLBE but also efficient merchant acquisitions.

Shopify

One key reason is the relatively strong user experience SMP provides for Shopify's merchants looking to sell globally, which should help drive adoptions. As mentioned a couple of times during the Q4 earnings call, SMP integration will enable Shopify's merchants to sell internationally without having a physical presence in the countries they are selling to. GLBE provides this seamless experience by becoming a "merchant of record" for Shopify's merchants:

When you use Shopify Markets Pro, Global-e becomes the merchant of record. A merchant of record is the legal entity responsible for selling products to a customer, and for adhering to local laws and regulations in another region or country. Unless another party like Global-e is hired to take on these responsibilities, most merchants act as their own merchants of record. When you act as your own merchant of record, you're responsible for registering for and remitting taxes, arranging to accept local methods of payment, and organizing shipping and fulfillment.

Source: Shopify.

The go-to-market motion with large e-commerce platforms such as Shopify is also a highly strategic move for GLBE, in my opinion. Shopify is among the largest e-commerce platforms in the world, possibly second only to Amazon. Through the SMP integration, GLBE is now accessible to over 4.8 million Shopify online merchants globally, further enabling GLBE to scale up its merchant acquisition initiative efficiently.

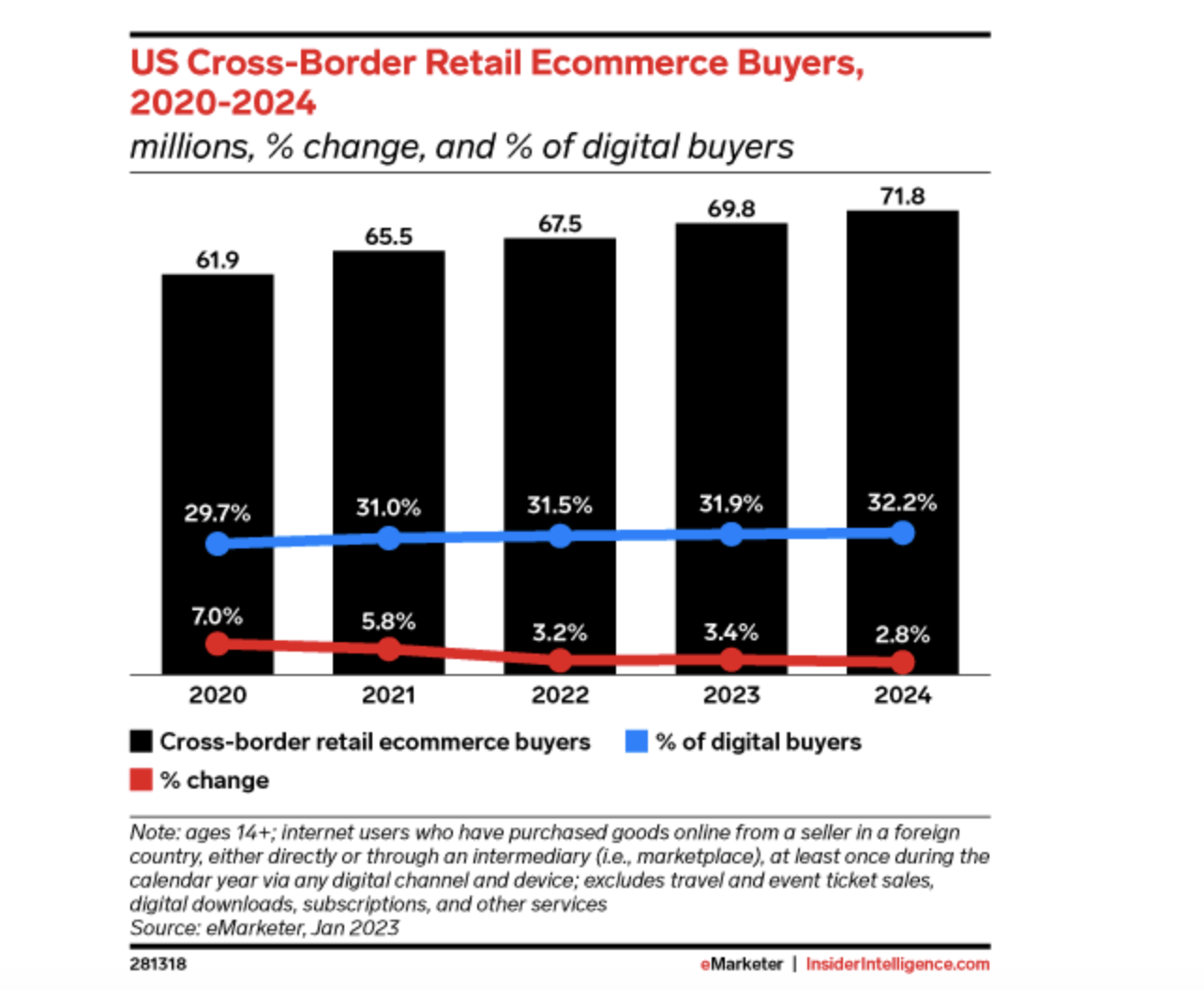

Furthermore, I would also expect GLBE to see a steady demand for its platform in 2024 and beyond, driven mostly by the sustained growth in cross-border e-commerce consumer demand within its largest market, the US. As of FY 2023, the US activities make up half of GLBE's revenues.

eMarketer

Though YoY growth of cross-border e-commerce has been slowing down since COVID 19 likely due to the persisting macro weakness, as reported by eMarketer, there are two positive data points from the report that may indicate not only resilience but also steady industry demand. First off, we continue to see an increasing share of digital cross-border buyers. Secondly, at 2.8% YoY growth in 2024, growth could be close to bottoming out. In my view, the continued strength in industry demand is already demonstrated by the strong pipeline of large merchants GLBE aims to convert in Q4, which should translate into future revenue growth in FY 2024:

We have seen record bookings in 2023, and we are excited about the strength of the pipeline that is going to support our growth throughout 2024 and into 2025. Within it, we have a couple of very large merchants that are expected to launch in the back half of the year.

Source: Q4 earnings call.

I believe risk remains minimal to moderate. In particular, there is a good possibility of a macro slowdown in the US and UK to continue for most of 2024, which may put pressure on e-commerce consumer spending activities:

Yes, thank you for your question. It's Nir. I would say that in February, we don't see a specific vertical that is down. However, on geographies, we do see slowdowns around different parts of the world. Our inbound into the U.S. has slowed down a bit. Same-store sales not growing as fast as they did in January or the previous year. The same goes for the U.K. that officially went into recession just earlier this year. And same, we've seen some slowness in APAC.

Source: Q4 earnings call.

Eventually, the lower e-commerce spending would also impact cross-border purchase activities, which are driving GLBE's GMV / gross merchandise volume, and effectively, fulfillment revenue. Though still making up more than half of GLBE's total revenue, fulfillment revenue share has declined as of late. In FY 2023 fulfillment revenue share saw a slight drop to 54% from 56% in FY 2022.

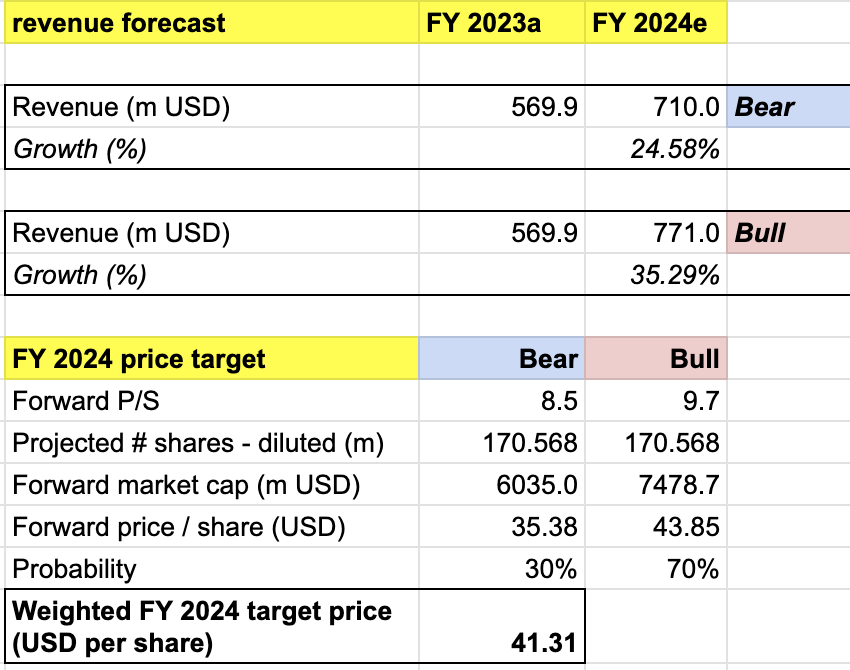

My target price for GLBE is driven by the following assumptions for the bull vs bear scenarios of the FY 2024 projection:

Bull scenario (70% probability) assumptions - GLBE to achieve its FY 2024 revenue of $771 million, a 35% growth, at the high end of the guidance. I assign GLBE a forward P/S of 9.7x, which implies a share price appreciation to $44, surpassing the YTD's high of $42. I believe this should be a fair projection, considering the top-line growth acceleration to 35%.

Bear scenario (30% probability) assumptions - GLBE to deliver FY 2024 revenue of $710 million, a 24.6% growth YoY, missing the low-end range of its guidance by over $20 million. In this scenario, I expect GLBE to see very minimal upward price action, as reflected in the P/S of 8.5x.

own analysis

Consolidating all the information above into my model, I arrived at an FY 2024 weighted target price of $41.3 per share, presenting a potential upside of 18% from the current level. At this point, I would give the stock a buy rating.

GLBE presents an attractive buy opportunity due to its strong positioning in a growing cross-border e-commerce industry. In my view, it is manifested in the strong pipeline into 2024 despite the expectation of a persisting macro slowdown across geographies. In my opinion, the top-line growth guidance of over 30% under the current macro situation suggests a promising outlook. Furthermore, the SMP integration with Shopify may serve as a near-term catalyst for the stock. I set a 1-year price target of $41.3, rating the stock a buy.