Colleen Michaels/iStock Editorial via Getty Images

Colleen Michaels/iStock Editorial via Getty Images

I rated Gladstone Capital (NASDAQ:GLAD) as a buy when I last covered the business development company. Total returns since then have been marginally positive, at just over 6%. The BDC just reported fiscal 2024 first-quarter earnings, ending December 31st, 2023, with total and net investment income underperforming versus consensus estimates. Total investment income for the first quarter at $23.2 million dipped by $600,000 sequentially but grew by 20.4% over its year-ago comp. The BDC also declared a monthly cash dividend of $0.0825 per share, kept unchanged from the prior month and $0.99 per share annualized, for a 9.6% dividend yield. Critically, first-quarter NII per share at $0.274 means the BDC currently covers the 3-month aggregate of its monthly distribution by 110%, a roughly 90% payout ratio.

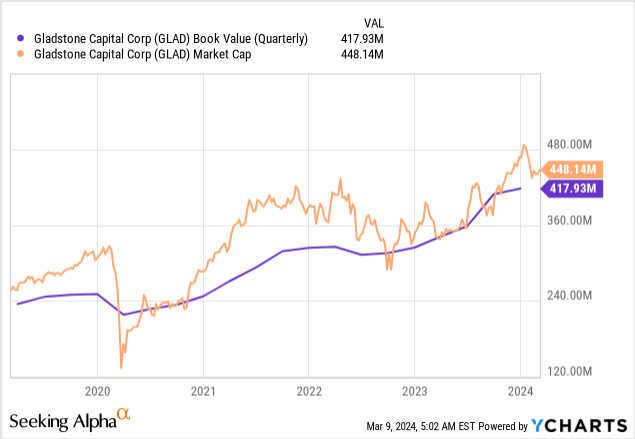

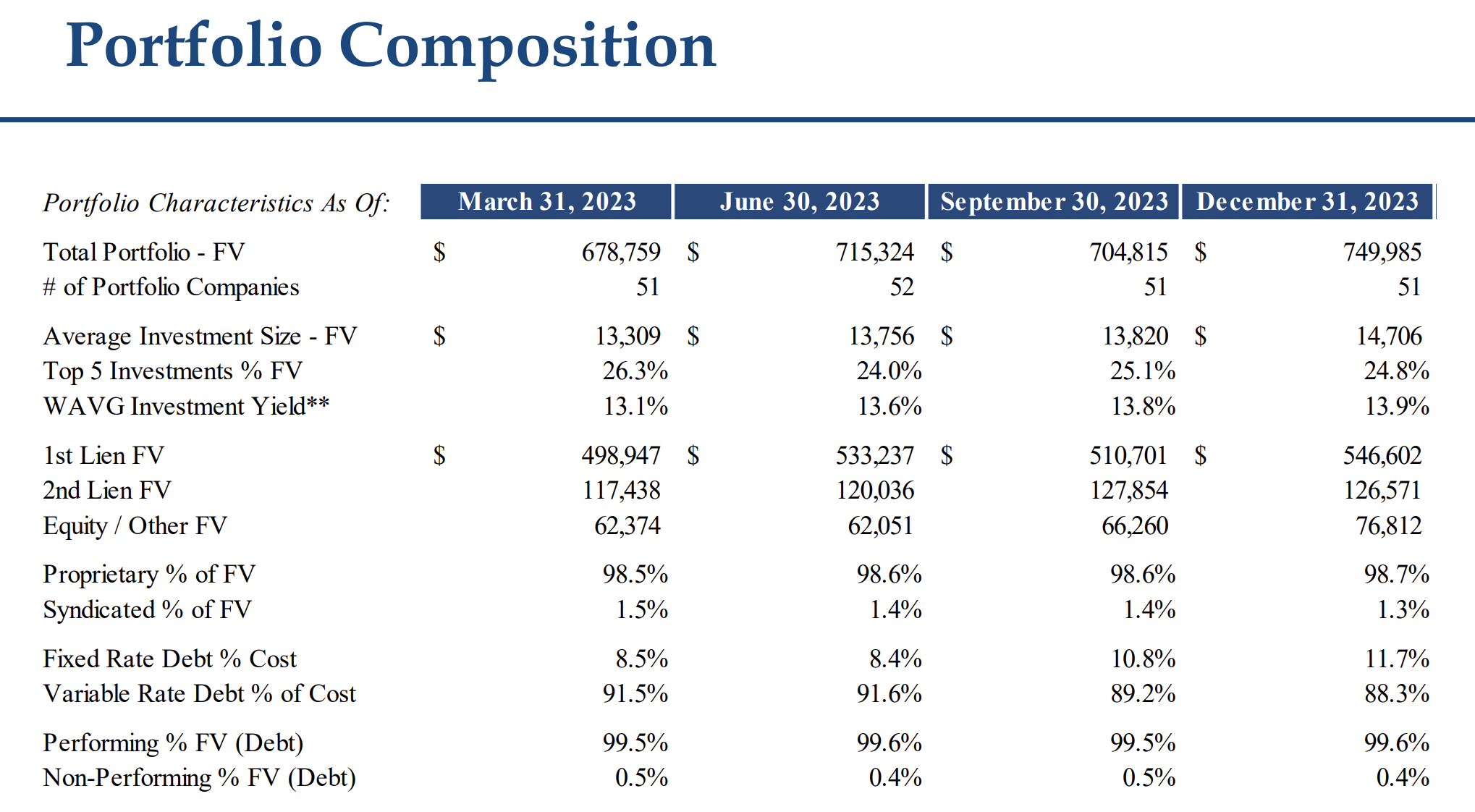

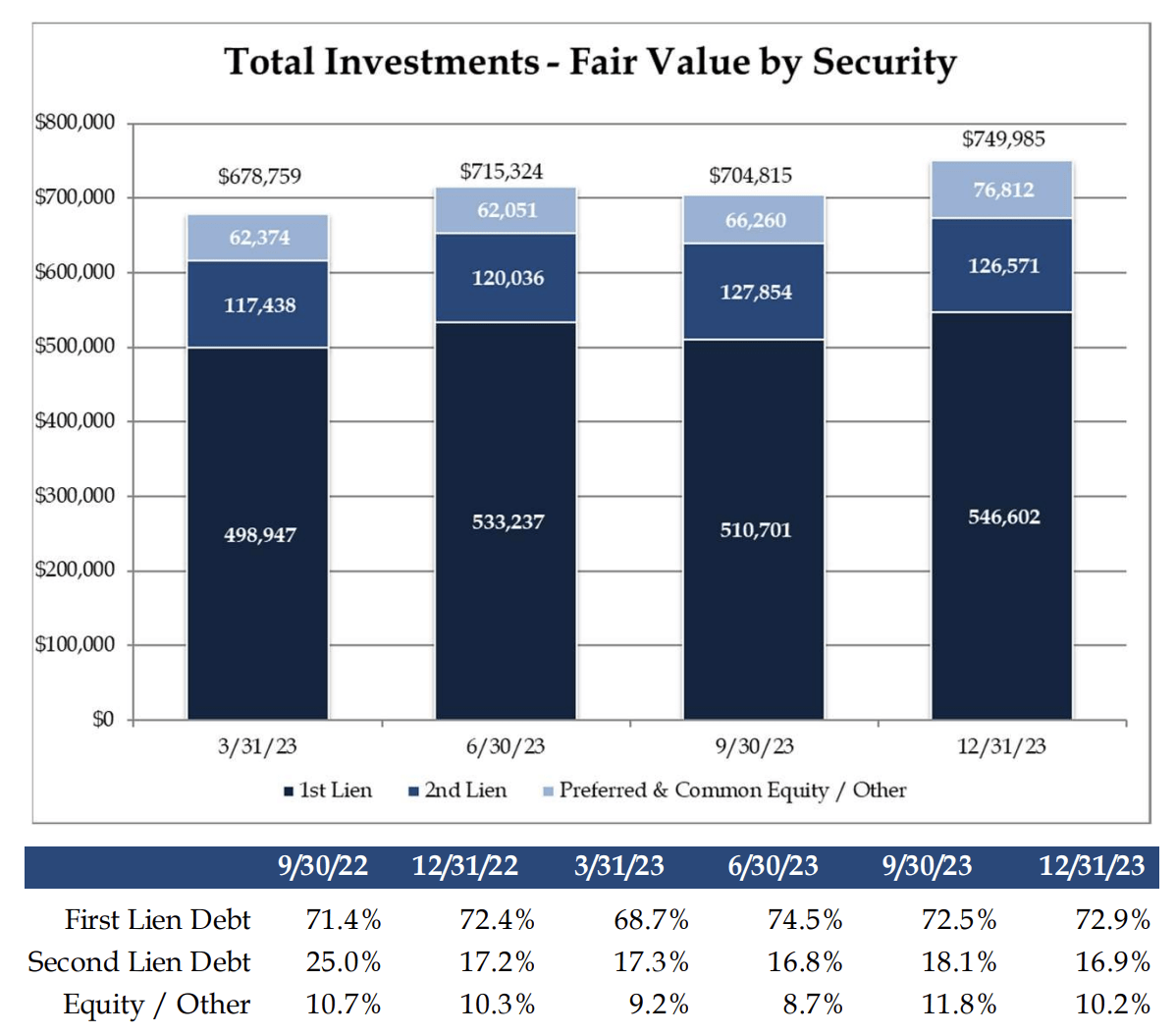

With GLAD over-earning its dividend, the BDC has been able to feed excess income into its net asset value. NAV at the end of the first quarter came in at $9.61 per share, growing by 22 cents per share or around 2.3% sequentially. The common shares at $10.30 per share are currently trading at a 7.2% premium to NAV after a dip from January's all-time highs. GLAD's first quarter-end portfolio at fair value stood at $749.98 million spread across 51 companies and at a weighted average yield on interest-bearing investments of 13.9%, up 10 basis points sequentially.

Gladstone Capital Fiscal 2024 First Quarter Presentation

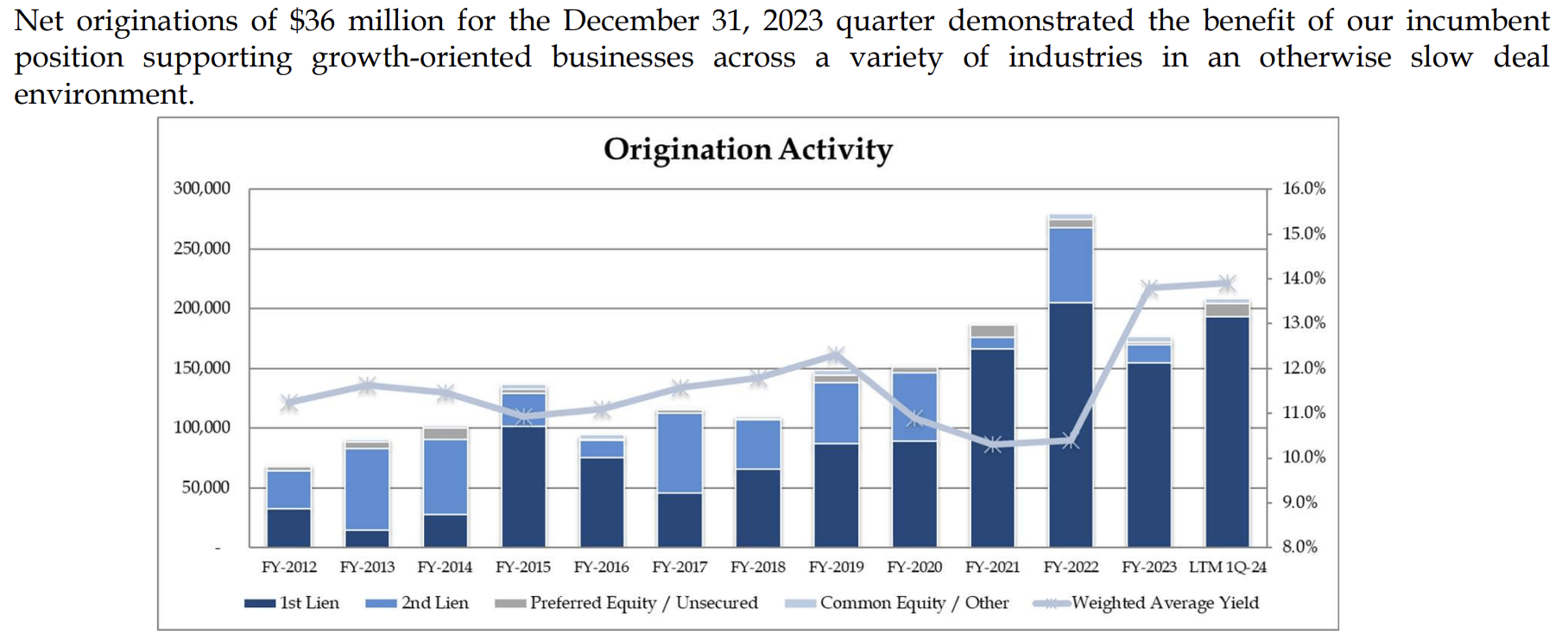

GLAD's portfolio has seen steady sequential growth over the last four quarters, with continued positive portfolio investment activity. The BDC invested $58 million in the first quarter ahead of total repayments of $22 million. Further, only 19% of the investment made during the quarter was to a new portfolio company, with the remainder invested into GLAD's existing portfolio companies. The mix of continued NAV growth, a fully covered dividend, and total portfolio growth at fair value renders the common shares a compelling investment. However, the BDC faces a gradual end of the golden age for BDCs, with Fed rate cuts looming for later this year against a possibly more disruptive macroeconomic backdrop for middle market businesses.

Gladstone Capital Fiscal 2024 First Quarter Presentation

GLAD has been ramping originations, with activity for the trailing 12 months as of the end of the first quarter the second highest over the last decade. What's also stark is the BDC's now near-singular focus on secured first lien assets, with second lien debt investments essentially removed from GLAD's new origination activity. First lien assets currently form 72.9% of GLAD's total debt investments, with a 16.9% allocation to second lien debt and a 10.2% to equity. This means GLAD is creating an intrinsically safer debt portfolio while ramping originations and driving sustained NAV gains at the same clip.

Gladstone Capital Fiscal 2024 First Quarter Presentation

NII did underperform consensus estimates by 1 cent, with a 1.6% sequential dip in the weighted average principal balance of interest-bearing investments to $657.6 million. The bearish sentiment here is that GLAD will have to maintain this momentum in a year when the Fed is expected to cut base interest rate by at least 75 basis points. Why is this important? GLAD has roughly 88.3% of its loan portfolio subject to floating rates with minimum SOFR floors. Hence, the BDC will see its weighted average yield on interest-bearing investments move in the opposite direction than it has realized over the last two years. Against this backdrop, credit quality becomes integral.

Gladstone Capital Fiscal 2024 First Quarter Form 10-Q

GLAD's debt investments have a risk rating scale that starts at 10. This is the best risk rating and is described in the BDC's first quarter form 10-Q as equivalent to a BBB from a nationally recognized statistical rating organization. The BDC's weighted average risk rating stood at 7.6 at the end of its first quarter, an improvement from 7.5 in the prior fourth quarter, with its lowest risk rating remaining at 3. This risk rating covers 98.3% of all debt investments in GLAD's portfolio at the end of the quarter. Non-performing debt investments as a percent of GLAD's total loan portfolio stood at 0.4% at the end of the first quarter, a 100 basis points decrease sequentially.

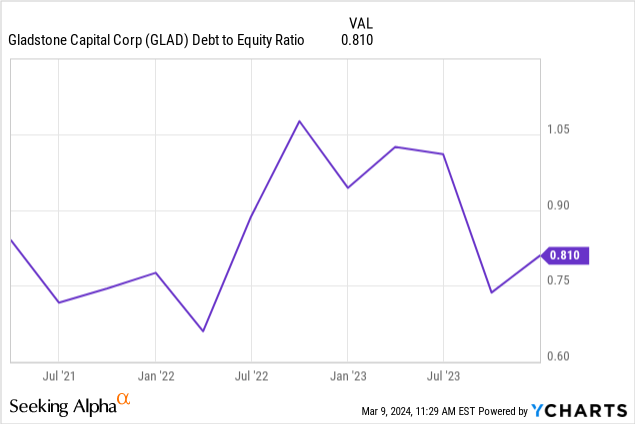

The low percentage of underperforming loans comes with the BDC's leverage being maintained at a prudent range, with a debt-to-equity ratio that stood at 0.81x at the end of the first quarter. A ratio less than 1x is generally perceived to be safe. Hence, GLAD has prioritized safety with a sole focus on first lien loans in new originations, is operating within a prudent leverage range, and fully covers its near-double digit dividend yield through NII. The sustained growth of NAV is a positive, with the commons remaining a buy.