Bloomberg/Bloomberg via Getty Images

Bloomberg/Bloomberg via Getty Images

I continue to see Gildan Activewear (NYSE:GIL) ("the company") as an attractive investment, that despite a softer demand affecting the whole industry, it is capable of delivering strong execution.

In my previous article back in January 2024, I argued that Gildan Activewear has the potential for further upside, supported by a compelling valuation, a strong value proposition, anticipated input cost deflation, and new leadership.

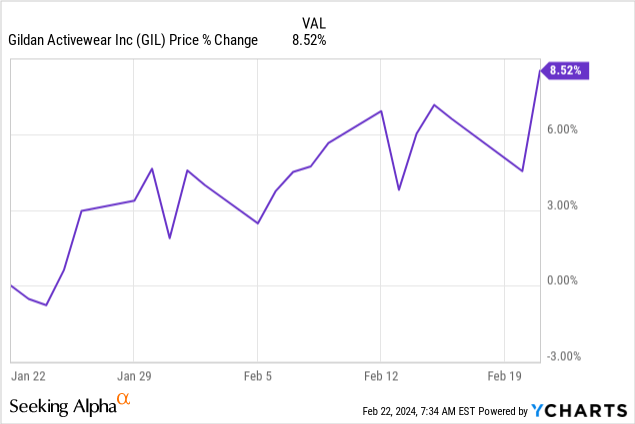

Since then, despite a relatively short period, the stock performance has been positive, able to deliver alpha relatively to the S&P500:

After Gildan Activewear reported the 4Q 2023 fiscal results the market reacted with shares rising ~4% in response to such developments.

Author's Estimates

For Q4, revenues came in at $783M, up ~ 8.8% over the prior year, slightly above the consensus of $761M, but down on a full-year basis by about ~1.4% due to negative performance in the activewear segment (down ~ 3.4%) and partially offset by the hosiery and underwear segment (up ~ 10.5%). However, the slowdown is not company-specific, but it is hindering the whole industry. From Under Armour (UAA) to Hanesbrands (HBI), and Primark (OTCPK:ASBFY) "softer demand" was the key theme during the latest earnings reports as macroeconomic pressures continue to weigh on consumer demand, particularly in International Markets.

I do expect the inflationary pressure to weigh also going into 2024, with "frugality" still being a key topic affecting consumers' purchasing patterns.

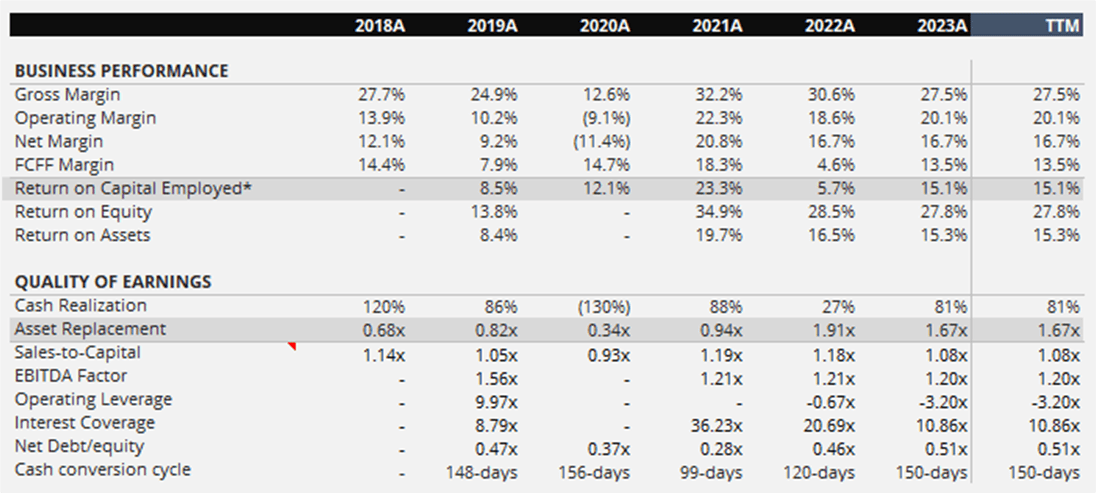

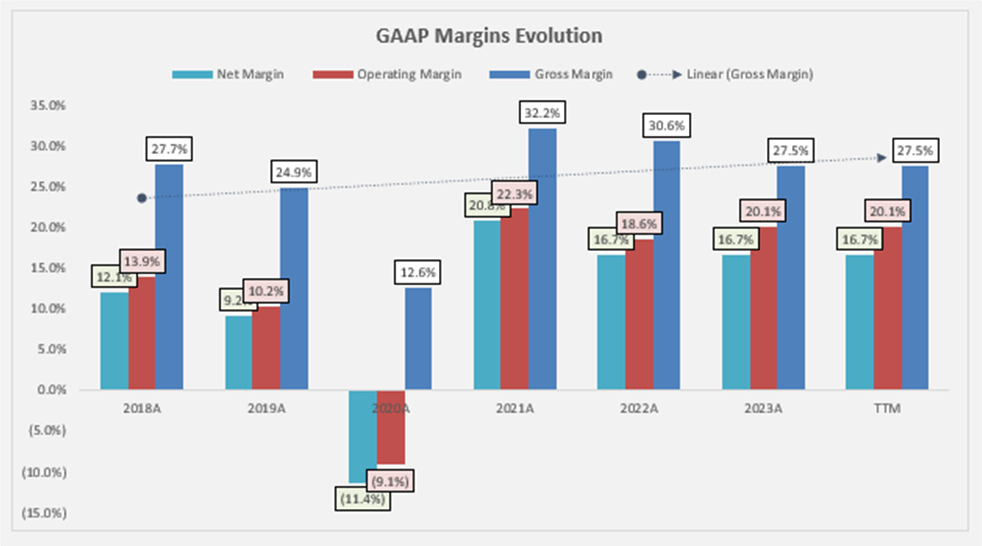

That said, the margins look healthy, with operating margins in line with the management range target of 18%-20%.

Author's Estimates

Gross margins decreased to 27.5%, primarily due to higher input costs, which currently act as a tailwind on the bottom line. Moreover, the ramp-up of the new Bangladesh facility, which is currently at a capacity run rate of 25%, will be an additional tailwind going forward.

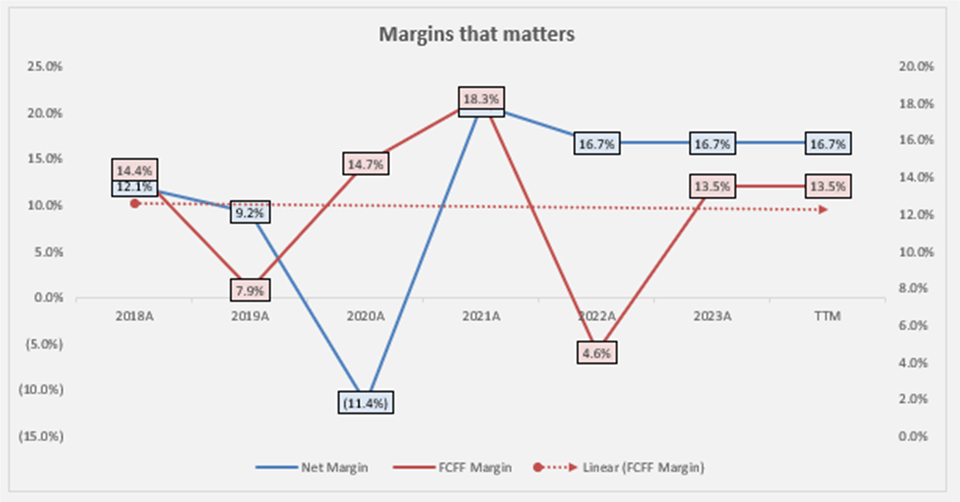

While, for what concerning FCFF margins, the picture is even better, as the company posted an FCFF margin of 13.5% up from 4.6% a year before. The significant improvement is driven by lower CapEx and in particular by lower working capital investments (mainly driven by lower inventory level). A similar picture can be observed in its closest peer, Hanesbrands, which posted the same improvement on the free cash flow front.

Author's Estimates

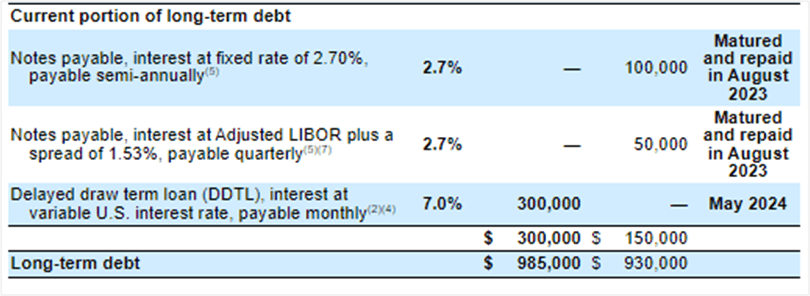

Finally, the balance sheet remains healthy. It is worth noting that the company has a term loan of $300M expiring this May, but I don't foresee any issue on the debt front given Gildan Activewear's strong financial position boasting a net Debt/EBITDA of 1.34x and an Interest Coverage ratio of 10.86x TTM.

Gildan Activewear FY report

On the performance side, ROA is above the historical norm and currently stands at approximately 15.3%. Meanwhile, ROE is around 27.8%, exceeding the cost of equity at approximately 13.6%, albeit down from 28.5% a year before. This decline is attributed to a lower total asset turnover, partially offset by higher financial leverage.

I reaffirm my previous "Buy" rating with a fair value of $44.85/share, driven by the previously stated catalyst. Having said that, I want to provide an update on the risks side, particularly on the Global minimum tax rate and the dispute between major shareholders and Gildan's BoD.

First, despite the timing of the enactment of legislation related to the Global Minimum Tax in Canada remains uncertain, the company has started to reflect the higher effective tax rate into its guidance. As stated during the 4Q23 earnings call, the net impact of the Global minimum tax rate on the company P&L is not as bad as initially anticipated:

In parallel with the enactment of GMT, our effective tax rate will move up to just below 18%. That will be the consequence of GMT rolling through Canada and other jurisdictions. However, there are other benefits that we expect to see related to tax reform that are expected to yield credits that will flow through our SG&A line. And the simplest way to think about that is that the quantum of those credits will probably reduce our SG&A as a percentage of sales by about 80 basis points

Second, regarding the dispute between major shareholders and Gildan Activewear's BoD. This is a point of concern to many investors because it translates into additional operating expenses for the company as well as distracts the management from its duties. In particular, the letter, issued by Brownie West, received a lot of attention from investors since it questioned the managerial abilities of the current CEO to run a global company. In my opinion, it may have been slightly exaggerated and, in certain parts, taken out of context. For example, the point related to:

During Mr. Tyra’s tenure as President of Retail and Activewear at Fruit of the Loom from 1997 to 2000, its share price declined by 99%

In my opinion, the above statement is not particularly accurate.

Fruit of the Loom filed for Chapter 11 later in 1999, with Vincent Tyra serving as President from 1998 to 2000. While it is true that Fruit of the Loom's share price decreased by 99% during Tyra’s tenure, Vincent Tyra is unlikely to be the root of the cause. The reasons behind such a negative price performance, in my opinion, should be attributed to a combination of factors such as a high debt level (due to the heavy expansion Fruit of the Loom did during the 80'-90'), and the North American Free Trade Agreement of 90', among others.

However, as a famous saying says: “Render to Caesar what is Caesar's.” I do agree that some of the points they raised, like Vincent Tyra's ability to manage a global large-scale company, are worth consideration. I see Vince Tyra as a good choice, and his industry expertise is a good fit for this role. However, I was expecting to hear something more from him about his strategic vision for Gildan Activewear during the earnings call. For this reason, I am following the situation very closely.

Gildan Activewear is an attractive investment opportunity with a compelling valuation, strong cash flow generation, and potential catalysts for market share expansion and margin improvement.

The dispute between major shareholders and the company's BoD is a point of concern to many investors and a headwind for the company's bottom line due to additional legal costs to handle shareholder matters. That said, I expect the company to continue to gain market share and the bottom line to expand driven by cooling input inflation, and lower cost of production thanks to its new facility in Bangladesh, among others.