angelp/iStock via Getty Images

Editor's note: Seeking Alpha is proud to welcome Kevin Murphy as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

angelp/iStock via Getty Images

Guardant Health (NASDAQ:GH) has come under recent stock price pressure, unjustly based on the assumption that their Shield product will be uncompetitive in the CRC market and from fears of competitors data. I believe there is ~30% upside in the name from EV/Sales multiple expansion which can be unlocked through consistent performance in the next 9 months as Shield gets approved and rolled out in the market.

Guardant Health is a precision oncology company focused on the diagnosis and analysis of various solid tumors. The Company provides their services in three segments: precision oncology, development services and screening. The precision oncology segment includes their therapy selection products for advanced-stage cancers and MRD tests for residual/recurring early-stage cancers. Their development services segment includes a suite of products used by drug developers to accelerate tumor analysis and drug development. Their newest segment, screening, will encompass their forthcoming SHIELD LDT product, a novel blood-based screen for early colorectal cancer (CRC).

Despite having a strong Precision Oncology business growing at 20-30% YoY, and expected to continue growing at least 20% in 2024, GH’s new CRC focused Shield product is overwhelmingly driving the story in the stock and thus will be the focus of the article. Specifically, I identify 3 main themes in the stock, 1) Will a competitor’s (Freenome) upcoming, 1H24, data prove better than GH’s Shield data? 2) Does the FDA approve Shield at its upcoming PMA meeting in late 1H24? And 3) If Shield is approved, can it compete in the real world given its inferior data to existing CRC screens?

GH’s Shield product is a blood-based CRC screening test that detects colorectal cancer signals in the bloodstream from DNA that is shed by tumors. Specifically, the test identifies specific characteristics of the DNA that may indicate the presence of cancer. In May 2023, GH published data from their 20,000 patient ECLIPSE trial showing 84% sensitivity with specificity of 90%, below competitor Cologuard’s 94% sensitivity at 91% specificity but widely assumed to be enough for FDA approval and Medicare reimbursement as it falls within performance of other non-invasive screening guidelines (FIT). At GH’s investor day in September 2023, they announced non-trial data with an improved algorithm that improved CRC sensitivity to 91% which they plan to submit as a supplemental PMA in 2025.

The U.S. CRC market is a massive market with the NIH estimating the total average-risk population is between 102.1m-106.5m people, of whom 43.4m-45.2m people are eligible for colorectal cancer screening and GH estimating over 50m eligible Americans do not get recommended screenings for colorectal cancer, putting the estimated market size at ~45m-50m. GH estimates that 80-90% of this unscreened population already receives bloodwork on a yearly basis.

Due to the lower sensitivity, the Company has shifted their marketing towards the higher adherence rates doctors can achieve with patients using Shield over currently available alternatives. GH has put out data stating of the >10,000 Shield tests already run, patient adherence has been 90% vs 38% for colonoscopy, 43% for FIT and 65%-70% for Cologuard. The argument being that even with lower sensitivity, you can generate more patient impact and higher sales per prescription from a test with a higher adherence rate.

On GH’s FY23 earnings call it was announced that the expected PMA date was being moved from Shield’s PMA timing was pushed from mid-1H24 to late 1H24 (likely June). The Company clarified this change in their Q&A segment stating the change was due to scheduling for the panel members and not an issue with their submission.

Additionally, on March 13, 2024 GH announced publication of the ECLIPSE trial in the New England Journal of Medicine(NEJM), largely considered amongst the most prestigious peer-reviewed medical journals (NYT).While not necessary for FDA approval, the nod from NEJM helps validate the data from the trial and should give investors some confidence going into the PMA meeting.

Based on all the data highlighted above, I put an 80% likelihood of approval in the PMA meeting later this year for GH’s Shield product. The current sensitivity and specificity data fits within currently approved screening tests included in CRC screening guidelines and the increased adherence rate shows a clear benefit from having a blood-based screen available to patients.

In my mind, there is no doubt the increased adherence and, at-minimum passable, clinical data will allow the product to generate a strong launch and capture even a small percentage of the 50m unscreened market. The potential for increased sensitivity in a year’s time with their v2 data only drives the likelihood of doctors choosing Shield more and more as the product is rolled out and gains payer coverage. Ultimately, it seems counterintuitive to think that an easier to use product that captures more patients with acceptable and potentially improving sensitivity would not be competitive in a market dominated by a product who dictates patients must send their feces in the mail. Below, I dive deeper into my different scenarios of the Shield launch.

Freenome is a private company developing a competing blood-based CRC screening test who is estimated to complete their PREEMPT CRC study in May 2024 (originally expected YE23 but updated per clinicaltrials on February 28, 2024). Freenome was communicating in 2023 that they planned to release the data and IPO off the back of the data without a crossover but raised a down round of $254m led by existing strategic investors in late February. The data is still expected to be shared in 1H24 per the Company’s website. Assuming normal approval time it will take 2-3 years to bring the test to commercialization which puts any competitive launch as a 2026-2027 timeline.

As an investor, it’s hard to get any edge on the data until it is released by the Company. Based on the new trial completion date at the end of May 2024, it would not surprise me if the data readout is pushed to 2H24 by Freenome, extending this overhang for the full year but causing investors to question the strength of Freenome’s data.

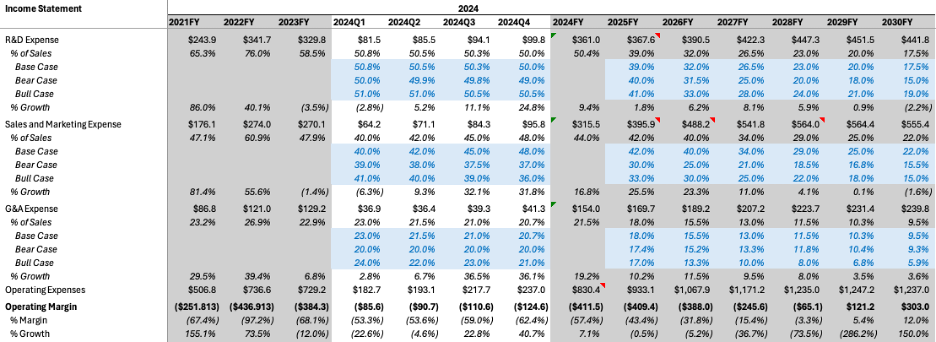

For this article I built a full three statement model whose assumptions drive my valuation on a comps multiple standpoint and via DCF analysis. The street will largely look at this from a comps standpoint as in order to get any cash flow to derive a DCF value I need to project out 7 years for a fast-growing diagnostic company. Nonetheless, I have included both models and my assumptions for the three cases below:

My topline cases contemplated three main scenarios, a calculated but not explosive rollout of Shield and continued strength in core precision oncology businesses (Base), a faster than anticipated launch of Shield with higher demand for precision oncology business than guided (Bull), and no Shield launch with expectations in the core business in line to slightly below expectations. The Company believes they can do over 1m Shield tests by 2028, my base case has them coming in slightly below this while my bull case has them significantly above that mark.

Proprietary Excel Model

For gross margins I erred on the side of caution with precision oncology margins remaining lower than historically but maintaining the 60% corporate average…I struggle to find real levers of upside on their precision oncology margins. I took a similar approach with the developmental services business which has proven to be quite lumpy in both topline and gross margin historically. On Shield, I have them achieving gross margin positivity in 2025 and slowly building to their ~60% target by 2028 with further improvements in the later years. This margin is driven by the belief they can achieve a $500 ASP on $200 cogs at scale of over 1m tests per their analyst day. Until that is achieved, Shield will be dilutive to overall gross margins.

GH Company Filings

My Base and Bull case operating expenses assumptions contemplate a shift in expenses from R&D to Sales and Marketing given Shields shift from clinical trials to a full scale launch, with the Bull case being more conservative on GH’s ability to control expenses through the launch and leverage more sales per dollar spend. The Shield program alone is responsible for ~$200m a year in expenses until 2028. Uniquely, my Bear case contemplates significant cuts in spending brought on by the ending of the Shield program without FDA approval which saves ~$200m in expenses per year driving significant increases in operating margin.

GH Company Filings

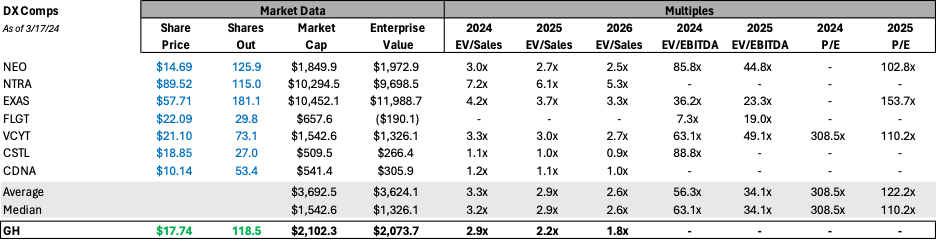

GH falls into the broader diagnostics comp set; however I view Exact Sciences (EXAS) and Natera (NTRA) as the two purest comps in the set given comparable product offerings and end-markets served. The table below outlines my comp set and their trading multiples as of March 17, 2024. It is worth noting that GH is currently trading a turn and a half below EXAS’ 3.7x EV/ 2025 Sales and even further below NTRA’s 6.1x EV/ 2025 Sales. NTRA has been very in-favor as of late, winning several patent cases against them and with significant runway on their portfolio of tests with limited competitors. EXAS has seen similar pressures on their multiple as GH, largely driven by lower rates and the overhang from Freenome’s data with investors wary to step in front of the stock ahead of that black-box event.

Public Company Filings

Historically, GH has been one of the stronger names in the diagnostics group, trading at a premium to EXAS ahead of the ECLIPSE readout and relatively in-line in 2023 after that. However, currently GH is at more than 1.5 standard deviations from the typical discount to EXAS.

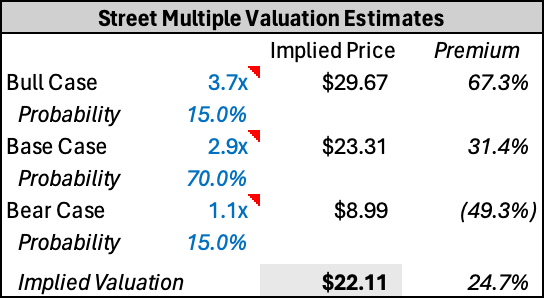

I believe a rerate in the multiple to historical levels is the most likely way to make money in the name. Just re-rating to the comps average of 2.9x EV/ 2025 Sales would imply ~30% upside to current trading levels. A rerate could come on the back of FDA approval or less than stellar Freenome data in 1H24. Additionally, strong Shield launch data could dispel the uncompetitive narrative some investors have in the name and push the multiple even closer to EXAS 3.7x and the historical discount to EXAS.

Downside to the name implies further multiple compression to the bottom end of the comp group despite having a very near-term topline catalyst in a patient rich market as noted above.

Finally, as it is a growthy name, any indication of rate cuts could help GH and the broader groups multiples rebound. With recent inflation data paired with comments from Fed Chair Powell regarding potential future trouble in the small to mid-sized banking space I have decided I'm not in the business of predicting rate cuts or hikes but would keep it on my watch list if the pathway to cuts becomes clearer.

Proprietary Excel Model

GH Company Filings

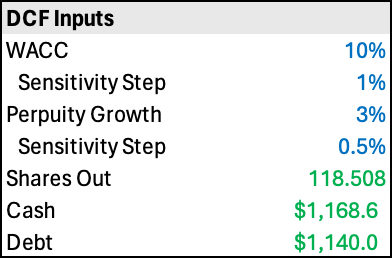

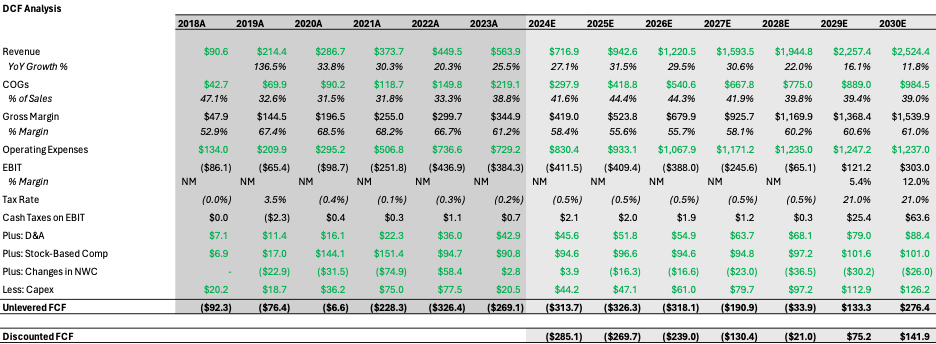

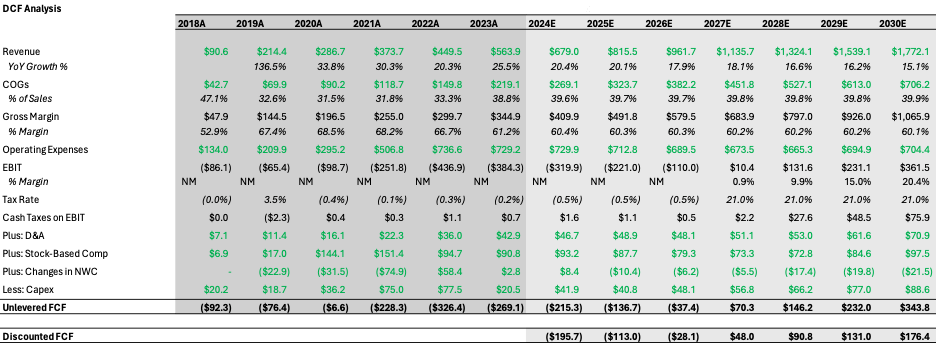

Despite it not being the primary valuation tool for the name, I ran a DCF analysis on GH using the DCF assumptions highlighted above, and my Base case assumptions noted earlier in the article. Due to poor EBIT or EBITDA comps multiples and GH’s long road to profitability, I stuck with the perpetuity growth method rather than slapping an arbitrary exit multiple on my 2030 EBIT number.

GH Company Filings

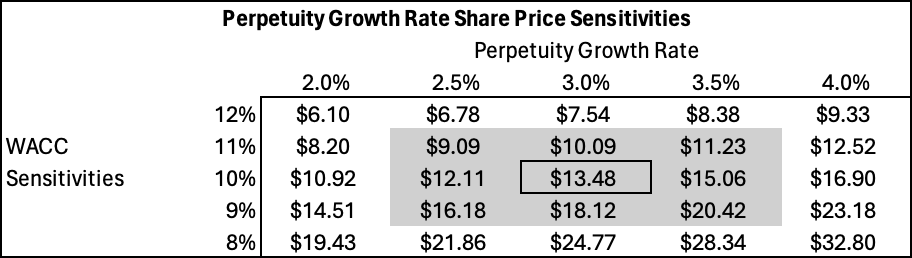

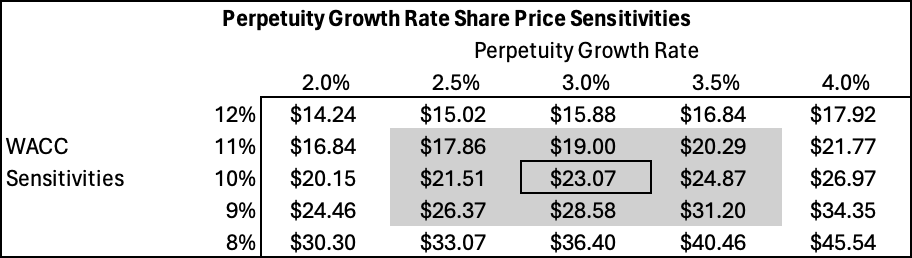

The table above shows GH's cash flow breakeven in 2029 with significant growth in profitability from there with a more mature Shield product. When sensitizing the WACC and perpetuity growth rate (below) I come up with a ~$14 stock at present value. I believe this does not fully encapsulate the true value of the product portfolio as they must overcome well over $1b in negative cash flow over the next 4 years with this method.

Proprietary Excel Model

My analysis would be biased if I only contemplated the possibility that Shield is approved by the FDA. In GH’s FY 2023 earnings call, the Company was asked if they would stick with Shield and keep pushing if met with setbacks from the FDA. Management effectively stated they believe their product would be approved but that they are not in the business of burning $1b just because they have it and they would discontinue the Shield product if they felt it was the best option. Below I try to model the consequences this decision would have.

I assume killing the Shield program would obviously forfeit any future profits from the program, reduce $1b in expenses between now and 2028 mostly from the sales and marketing line-item given their stated milestone driven sales expansion for the product, and reduce R&D given a lack of need for further trials to improve specificity or expand the product line.

GH Company Filings

Assuming the same DCF assumptions as above, it’s clear that discontinuing Shield actually pulls cash flow positivity forward by ~2 years given the lower expense rate and higher gross margins without the Shield dilution. This scenario would imply that GH is currently trading at levels that imply no Shield, a 2.5% perpetuity rate and an 11% WACC on my DCF as seen below.

Proprietary Excel Model

Discontinuing Shield is actually cash flow accretive and would imply potential upside of 30% to current trading levels with a 3% perpetuity growth rate and a 10% WACC.

GH has a competitive product with what should be a clear path to FDA approval and market launch in 2024. From a DCF analysis it is probably fairly valued, but since when has that been how we’ve valued high growth, cash flow negative stocks. The most direct route to profit with this name is through a revaluation in the Company’s trading multiple, something that could be seen with FDA approval and strong launch numbers proving the competitive product thesis. Ultimately, I see a 30% increase in value if GH starts to get given credit for their opportunities ahead and diversified portfolio. This will come down to execution over the next twelve months, and until that is proven, the competitive Freenome data will still be an overhang on the stock until it is seen.