Joey Ingelhart/E+ via Getty Images

Joey Ingelhart/E+ via Getty Images

I started coverage of GEO Group (NYSE:GEO) last March with a “Buy” rating based on its cheap valuation and the expected positive impact from the expiration of Title 42, taking it “Strong Buy” later in May. Mostly recently in November I wrote that while its Q3 results were lackluster, it still had a lot of upside potential and that a compromise border bill would help the company if it materialized. The stock is up over 40% since my initial write-up. Let's catch up on the name.

As a refresher, GEO owns, leases, and manages prisons, processing centers, and community reentry facilities in the U.S., It also manages facilities in Australia and South Africa, and has transport services in the U.K. It also provides electric monitoring and post-release support services. About 54% of its 2023 revenue came from owned and leased facilities, 24% from managed only facilities, and 22% from services.

The U.S. Immigration and Customs Enforcement ("ICE") is GEO’s largest customer, representing 43% in 2023. Individual states represented 25% of GEO's revenue, with Arizona and Florida the two largest.

For the quarter reported in mid-February, GEO posted a -2% decline in revenue to $608.3 million. That was ahead of the $597.5 million consensus.

Owned and Leased Secure Service revenue rose over 4% to $292.2 million, while the net operating income was $81.5 million, up 6%. Owned and Leased Reentry Service revenue jumped 11% to $41.6 million, while its NOI rose 5% to $10.8 million.

Managed Only revenue leapt nearly 18% to $153.1 million, while its NOI surged 66% to $28.8 million. Electronic Monitoring and Supervision Service revenue sank -39% to $90.7 million, while its NOI dipped -38% to $52.9 million. Non-residential service revenue climbed 32% to $30.1 million, while its NOI jumped 30% to $5.8 million.

GEO’s ISAP program was steady in Q4 ranging from 190,000 to 195,000 individuals. It currently sits at approximately 187,000 participants.

Adjusted EBITDA fell -11% to $129.0 million. Adjusted EPS came in at 29 cents versus 33 cents a year earlier. That was 12 cents ahead of analyst expectations.

Turning to its balance sheet, the company ended 2023 with $1.78 billion in debt. It had $94 million in cash.

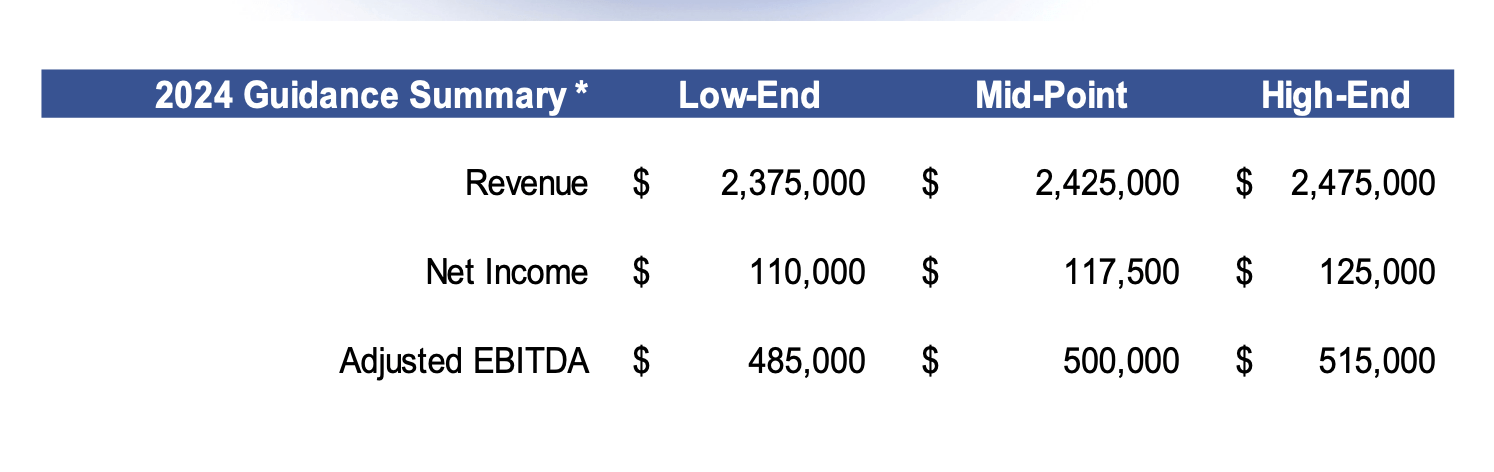

Looking ahead, GEO guided for 2024 revenue of between $2.38-2.48 billion.

The company forecast adjusted EBITDA to be between $485-515 million. It is looking for net income of between $110-125 million.

GEO noted that the high-end of guidance assumes moderate increases in utilization of ICE processing center beds and electronic monitoring services, while the low-end of guidance assumes reductions.

Company Presentation

For Q1, GEO is projecting revenue to come between $600-610 million. That bracketed the $604.3 million consensus at the time.

The company is looking for Q1 adjusted EBITDA of between $117-122 million versus a $130.9 million a year ago. It's looking for net income of between $22-24 million.

GEO plans to reduce debt by between $175-200 million a year going forward, taking it to $1.6 billion at year-end 2024. It is also looking to refinance its debt to lower its interest rates.

On its Q4 earnings call, executive chairman George Zoley said:

“We believe that ICE continues to face budgetary pressures, and the outcome and timing of ongoing federal budget discussions in Congress remains uncertain. Since October 1, the Department of Homeland Security and ISAP funded under a short-term continuing resolution, which has been extended twice and is currently set to expire on March 8. Last week, a group of US senators released a proposed supplemental appropriations bill, which included additional funding for border security. However, that bill was voted down by the full Senate. The bill has provided funding for 50,000 ICE detention beds, which represents an increase of 16,000 beds from the current funding level for 34,000 beds. Additionally, the bill would have increased the annual funding for alternatives to detention programs to approximately $1.3 billion from the current funding level of $440 million. If Congress is unable to reach an agreement on appropriations package prior to March 8, the federal government could continue to be funded under a continued resolution or face the prospect of government shutdown.”

For the most part, GEO turned in a solid quarter that was just above expectations. The one area of continued weakness that has hurt the company is its Electronic Monitoring and Supervision Service, which saw revenue once again plunge, as ISAP participation remains weak.

The irony, though, is that electronic monitoring is the biggest potential catalyst for GEO. Its BI subsidiary is the leader in the space and the only company that has a contract with ICE for electronic monitoring. Republicans have been pushing for a much wider use of the program, but as their efforts have stalled, the program continues to feel pressure from budgetary issues revolving around ICE, as it continues to be funded through short-term continuing resolutions.

Outside of electronic monitoring, the company’s other segments have performed well. It also has an additional 9,000 unoccupied beds if ICE funding in general goes up.

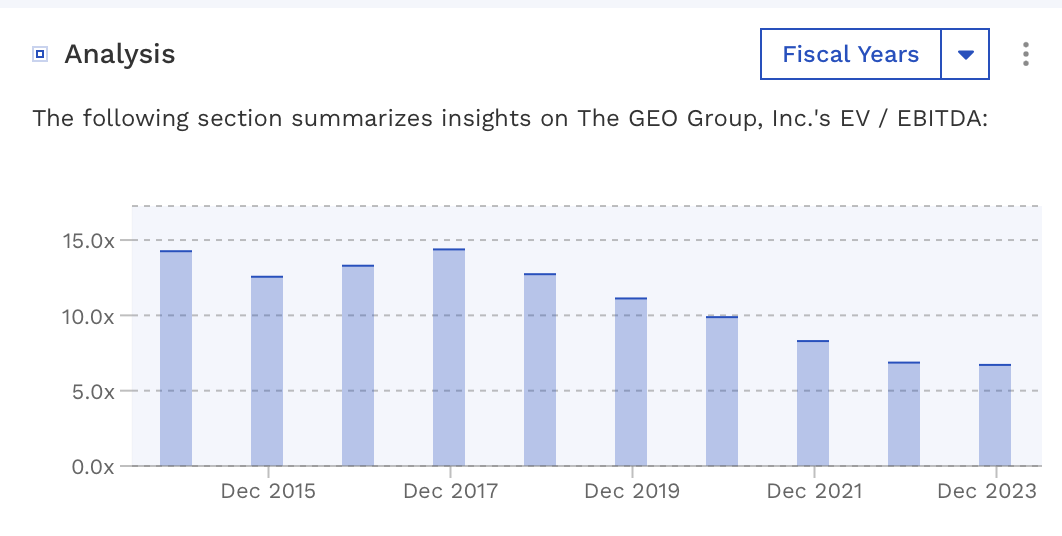

GEO trades at a 6.5x EV/EBITDA multiple based on the 2024 EBITDA consensus of $500.5 million. Based on the 2025 EBITDA consensus of $536.5 million, it trades at around 6.1x.

It trades at 12.8x forward EPS, with analysts projecting 2024 EPS of 95 cents Based on 2025 EPS of $1.28, it trades at 9.5x.

It's projected to see under 1% growth in 2024, accelerating to 3% growth in 2025.

Fellow detention operator CoreCivic (CXW) trades at 9x 2024 EBITDA. CXW doesn't have the ISAP exposure of GEO and carries less leverage.

GEO Historical Valuation (FinBox)

With ISAP at the very least looking to have leveled out, I’d value GEO at between 8-10x 2025 EBITDA, while reducing debt over the next year by $200 million. That put the stock between $22-31. Note that the stock traded between 10-14x EBITDA before the pandemic, so while that value range may look high, it’s at a much lower multiple than it's traded at in the past.

GEO remains one the most interesting stocks out there in my view. It has a very inexpensive valuation versus both its nearest competitor as well as from a historical perspective. At the same time, it comes with a huge lottery ticket with its monitoring unit. If some of the numbers the House has kicked around ever get into law, and both parties do seemingly want some type of action regarding border security, GEO could be a massive winner.

I continue to rate GEO a “Strong Buy.” My target is $22, but I feel under certain scenarios, the stock could go much higher than that price.

The biggest risk to the stock is any backlash against private prisons that would prevent usage of them from ICE or state governments. The continued decline in the ISAP program is another risk.

Investors should continue to monitor what the government plans to do about border security and its allocated budget towards ICE, as that would likely drive GEO’s stock.