Riska/E+ via Getty Images

Riska/E+ via Getty Images

Genius Sports (NYSE:GENI) is a leading global sports data provider. I have covered the stock before in June 2023, when I gave it a buy rating due to potential undervaluation and strong catalysts. Since then, GENI has been up 6.6%, confirming my bullish call.

Nonetheless, despite being up 26% over the past year, the current trading price of $6.3 is still a bit far from my $10 price target. YTD, GENI is also up by around 6.79%, suggesting that the stock has been gaining some momentum into 2024.

I maintain my coverage with a buy rating. My 1-year price target of $7.5 presents a 19% upside from $6.3 today.

YCharts

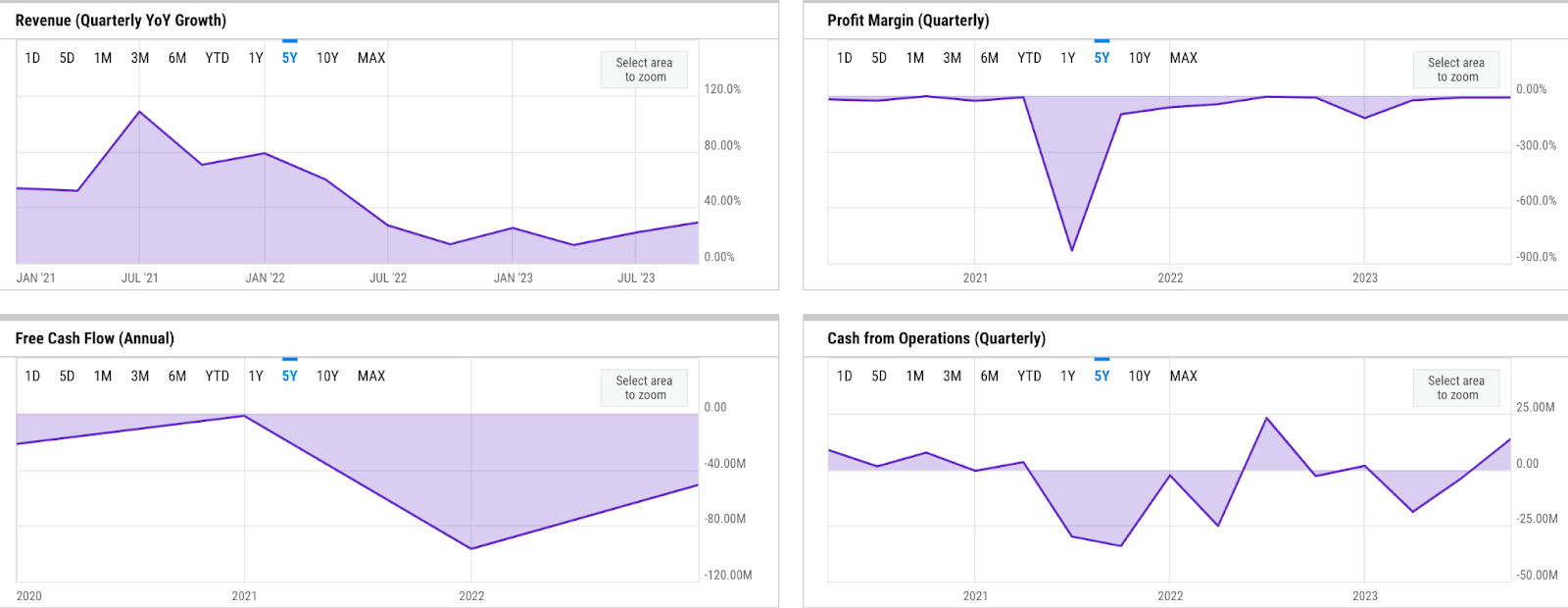

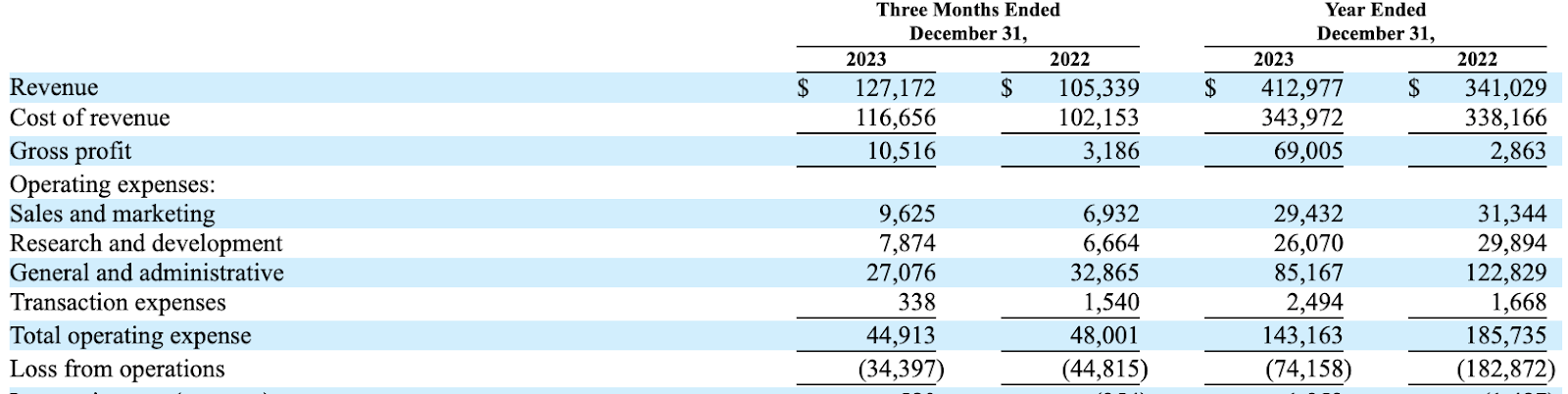

Fundamentals are mixed, but improving considerably. GENI's revenue growth has declined from over 75% in 2021 to just a little less than 30% in FY 2022. However, the spike in 2021 was partly due to inorganic revenue from several acquisitions made at that time. As guided by the management in the Q4 2023 earnings call, it seems that revenue growth should decline further to the 16% range in FY 2024. In FY 2023, GENI finished the year with a revenue of $413 million, realizing a 21% annual growth while beating its guidance of $391 million.

Nonetheless, GENI's focus going forward seems to be profitable growth. Despite the declining growth rate, I would note that the bottom-line improvements have been significant. Operating Cash Flow / OCF has reached break-even since last quarter in September 2023, while adjusted EBITDA / aEBITDA has more than tripled to $53 million, expanding aEBITDA margin by 800 bps to 13% in Q4. All of these improvements are driven by improving net loss, which narrowed by almost 70% YoY.

6-K

In my opinion, the bottom-line improvement should also help GENI strengthen its balance sheet since the increase in OCF should help offset the downtrend in cash balance. In FY 2023, GENI delivered over $14.8 million of OCF, a stark contrast from last year, when GENI pretty much burned through -$3.5 million of OCF. Overall, I would conclude that liquidity remains decent. Moreover, GENI also virtually has no debt - GENI has zero long-term / LT debt with a minimal amount left in the current portion.

As I touched on earlier, the management has guided for 16% revenue growth in FY 2024, which translates to a revenue of $480 million. Furthermore, it also expects to deliver around $75 million of aEBITDA, an over 41% increase from FY 2023, while also maintaining positive OCF.

In my opinion, the growth guidance appears conservative, since I believe GENI is benefitting from multiple strong catalysts into 2024. First off, the increasing legalization of sports betting across states in the US, as I covered in my previous analysis, should remain the ongoing growth catalyst for the stock. Moreover, I would expect GENI to see strong adoption of BetVision, driven by the in-play betting demand. In the end, I see potential room for more upside in operating cost optimization, which should help GENI unlock margin expansions, in line with its target.

GENI's presentation

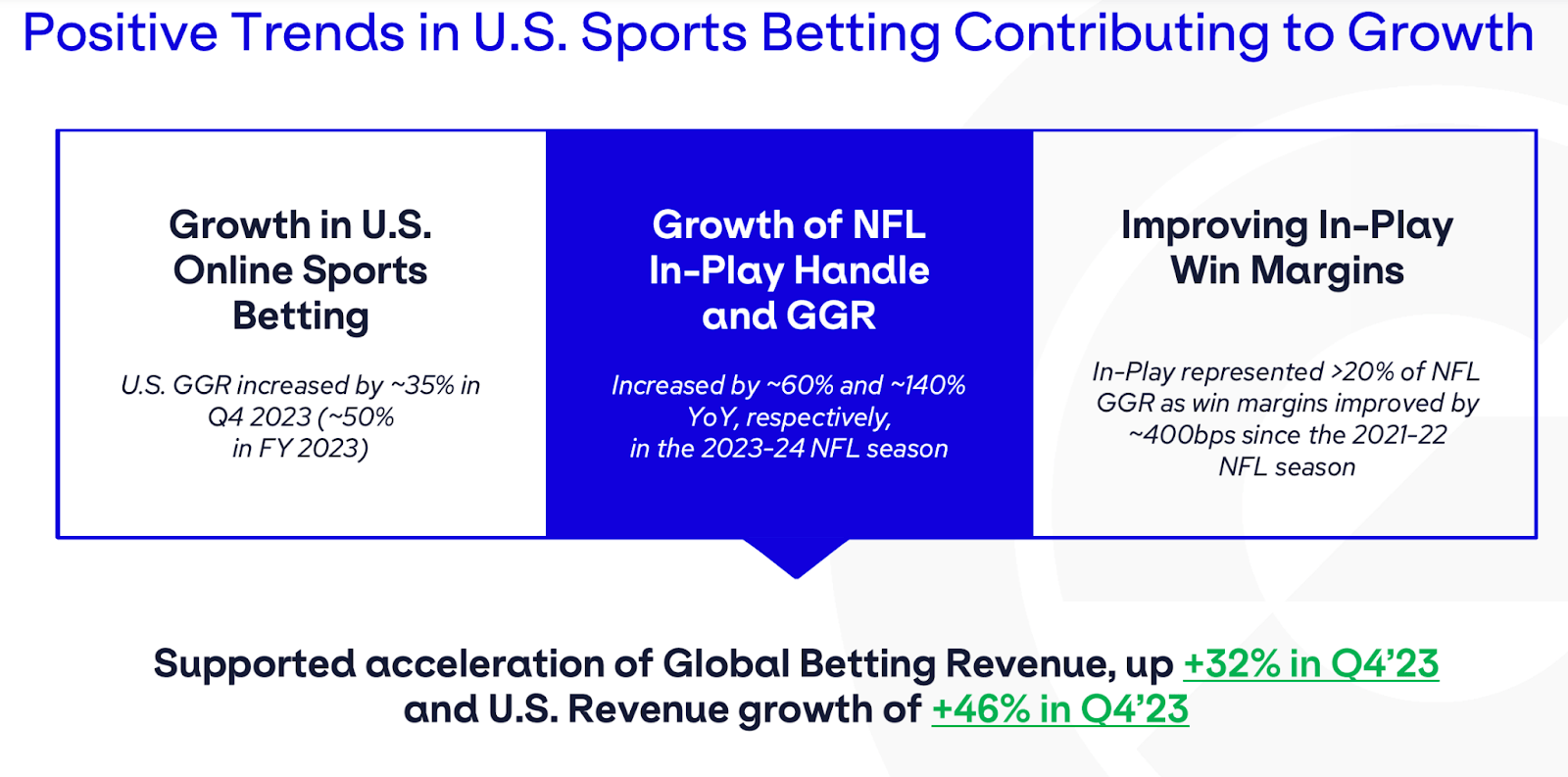

I believe the highly strong NFL in-play betting trends seen in the US in FY 2023 suggest that the market for online sports betting here is relatively early, as demonstrated by the relatively high growth at present. With over 60% and 140% increases in NFL in-play handle and GGR / Gross Gaming Revenue, there appears to be room for more upside the before growth rate normalizes, in my opinion. The upside here is mostly driven by the continuation of more US states opening up to online sports betting:

Yes. Hi, Eric. Look, we take a market view in terms of new states coming on board, and we take an average of that, and therefore we're not particularly beholden to requiring one particular state as we sit here. I think North Carolina opens up, I think it's next week, I think. So that's obviously baked into our numbers. Florida, we continue to be cautious with, but that's baked into 2024, if that continues.

Source: Q4 earnings call.

GENI's website

Furthermore, I believe GENI's push towards in-play betting with BetVision is also a step in the right direction - aside from the proven success with NFL, in-play betting has historically been the largest driver of GGR in mature markets such as the UK. In my opinion, the US's online sports betting market could potentially look a lot like that of the UK in the future, meaning that investing in in-play technology today is crucial for future growth.

6-K

On the profitability side, I see more room for cost optimizations, particularly in G&A, which indicates that GENI is in a good position to achieve its margin expansion target. Despite decreasing by over 30% in FY 2023, G&A still makes up over 20% of revenue. At 20% of revenue, GENI's G&A is relatively high by any standards and is still far away from GENI's target of 6-7% at maturity. This means G&A can go down even further. Moreover, there appears to be an indication that GENI can maintain its growth trajectory with lower expense level, which suggests that the optimization could be sustainable:

Equally, all other total operating expenses beneath cost of revenue, as presented on a non-GAAP basis on Slide 19, have remained relatively steady over the last year, even as we've significantly increased revenue in that time. We expect this will be the case in 2024 as well.

Source: Q4 earnings call.

Risk remains minimal, in my opinion. I would note that despite the increase in the number of US states legalizing online sports betting, each state could have its own regulations that may limit its growth potential. A good example would be Florida. As covered by Forbes, Hard Rock Bet is currently the only online sportsbook allowed in the state:

In summary, the only legal sports betting app in Florida is Hard Rock Bet. The platform is available on iOS and Android. Other betting apps from Florida pari-mutuel companies are expected in the future. However, we also recommend top fantasy sports sites such as Thrive Fantasy, Parlay Play, Boom Fantasy and Underdog Fantasy for all your wagering needs. Other online sports betting platforms licensed in other U.S. states are not allowed. Popular sports betting sites like FanDuel Sportsbook and DraftKings Sportsbook can't be used in Florida.

Source: Forbes.

Florida remains the top three most populated states in the US and therefore should remain a key market for GENI, in my view. However, the limitation put in place by the state has so far resulted in the loss of opportunities for GENI. DraftKings, for instance, is one of many GENI's sportsbook customers not allowed in Florida that could have unlocked higher growth for the company.

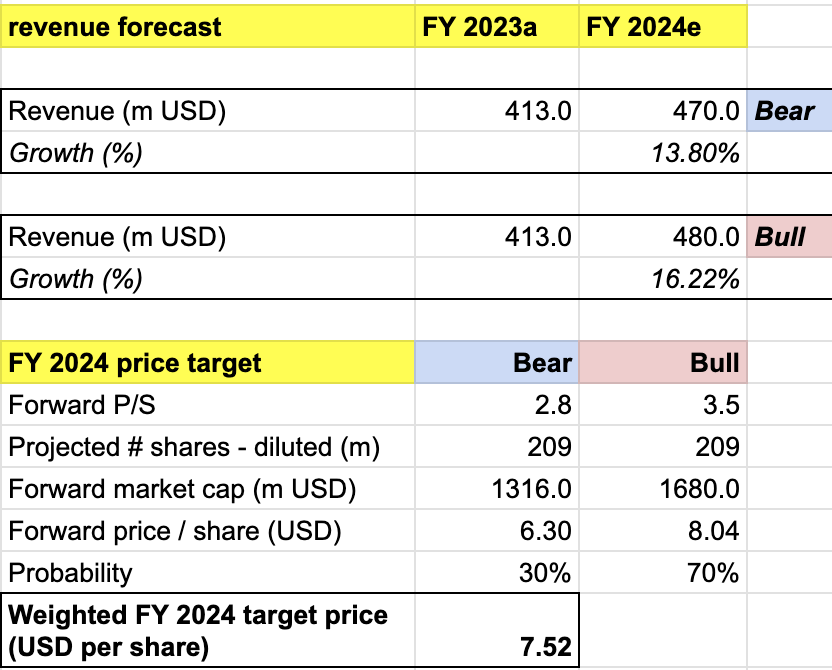

My target price for GENI is driven by the following assumptions for the bull vs. bear scenarios of the FY 2024 projection:

Bull scenario (70% probability) assumptions - GENI to achieve FY 2024 revenue of $480 million, a 16% growth, at the high end of the guidance. I conservatively assign GENI a forward P/S of 3.5x, where it is trading at the moment. This projection assumes strong BetVision adoption among sportsbooks across more US states, which should help drive higher in-play NFL revenue for the FY.

Bear scenario (30% probability) assumptions - GENI to deliver FY 2024 revenue of $470 million, a 13.8% growth YoY. This means GENI would miss its low-end guidance, effectively resulting in a correction to $6.3 or sideways price action. As discussed in the risk section, I would project the cautious opening of more US states to slow down the growth trajectory of GENI.

price target (own analysis)

Consolidating all the information above into my model, I arrived at an FY 2024 weighted target price of $7.5 per share, presenting a potential upside of 19% from the current level. At this point, I would give the stock a buy rating.

Since my first coverage last June, my bullish call has been proven right, with GENI up 6.6% as of today. Continuing legalization of online sports betting across more US states remains an ongoing catalyst, along with the strong adoption of in-play betting offering, BetVision, in my opinion. GENI is also in a good position to see margin expansions in 2024. I maintain my buy rating for GENI with a price target of $7.5, implying a 19% upside from the current level.