Sushiman

Sushiman

Last year, I started to put a lot more emphasis on the impressive turnaround of General Electric (NYSE:GE), a company that has gone through a lot in the past ten years.

Fortunately for its investors, the company has found a way to generate value, by spinning off business segments and benefitting from the massive rebound in aerospace demand.

My most recent article on the stock was written on October 29, titled "General Electric's Comeback: Up 60% YTD And Room For Double-Digit Annual Returns."

GE's improved guidance, strong performance across segments, and attractive valuation make it an enticing investment opportunity.

Despite a 60% rally year-to-date, the stock remains appealing, with potential for significant growth in the coming years.

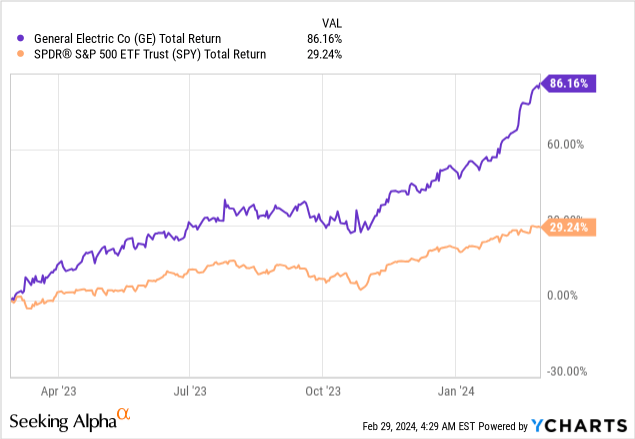

Since then, the stock is up another 45%, twice the already impressive 22% return of the S&P 500!

In fact, the GE ticker is now up close to 90% over the past twelve months.

In this article, I will explain why the stock still has room to run, despite this massive rally, as the company continues to benefit from strong demand, innovation, and secular growth, strong free cash flow conversion, and so much more.

So, let's get to it!

Roughly a quarter of my portfolio is invested in aerospace and defense stocks.

Here's what I learned from my research over the past few months:

General Electric seems to benefit from the tailwinds without suffering from the headwinds.

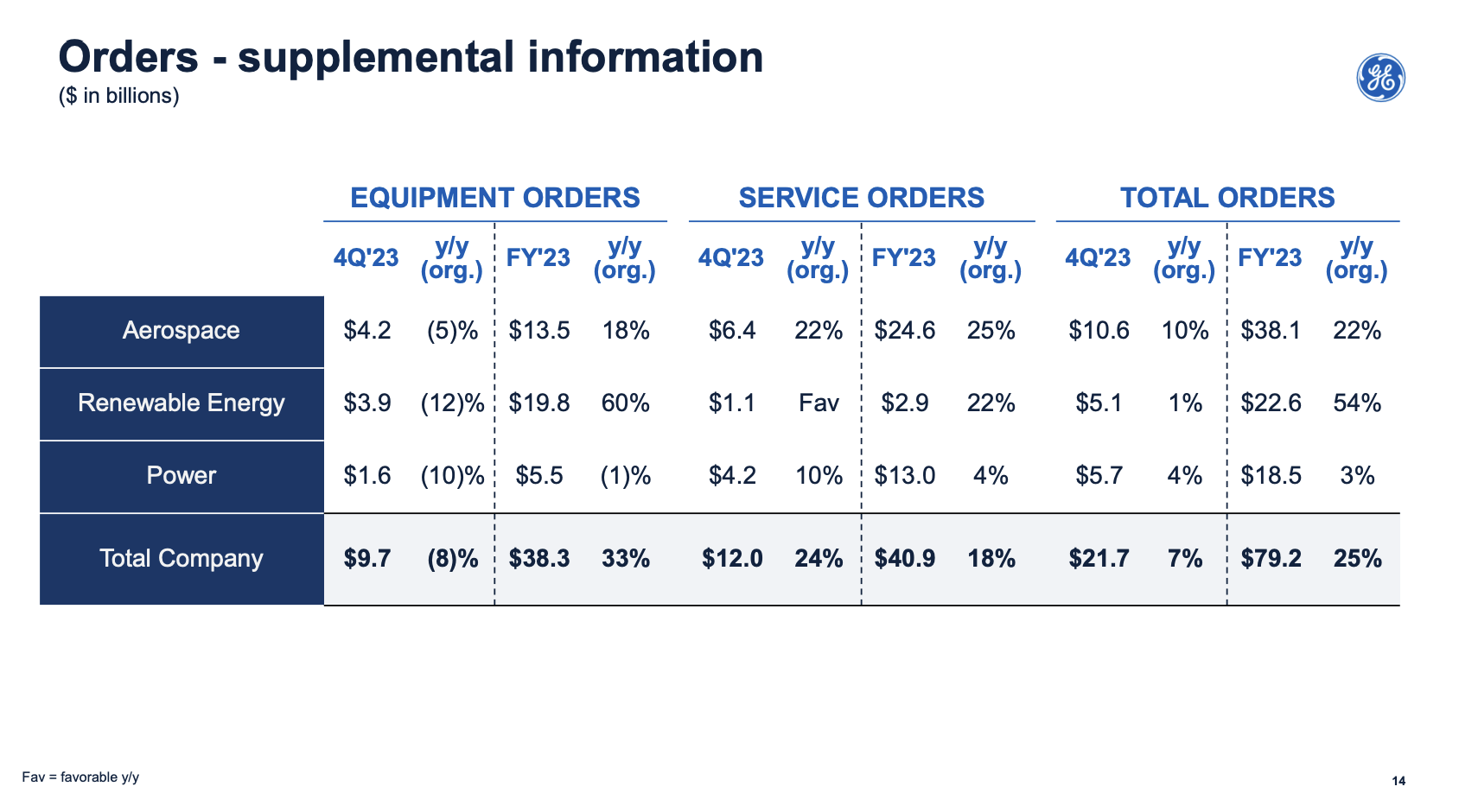

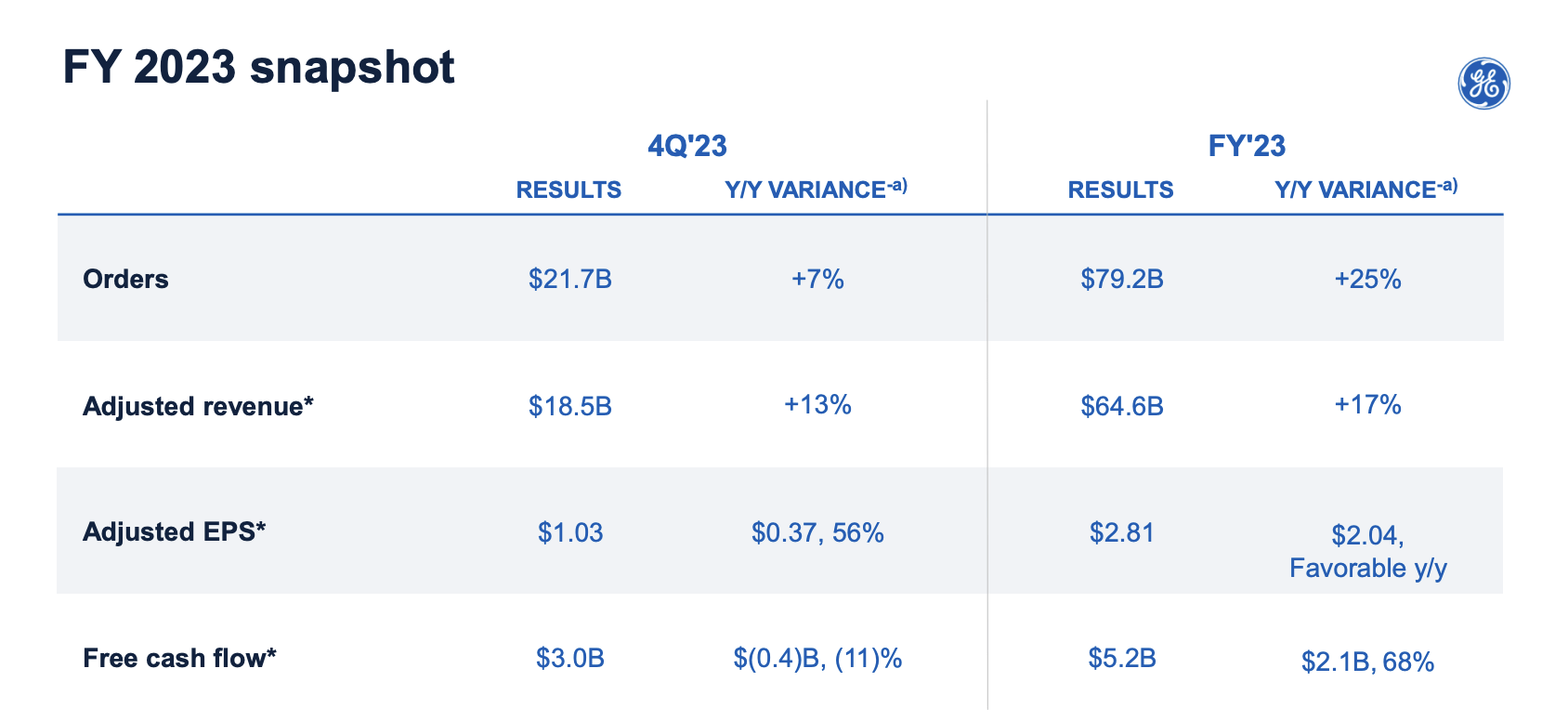

For example, in the fourth quarter of 2023, the company reported strong results on an organic basis across all segments.

Orders increased by 7%, with service orders reporting 24% growth.

General Electric

Revenue saw a 13% increase, driven by double-digit growth in all segments.

Moreover, with regard to my aforementioned margin comments, the company's adjusted operating profit rose by 20%, supported by a margin expansion of 50 basis points.

Adjusted EPS reached $1.03, which translates to a 56% increase.

Free cash flow came in at $3 billion, primarily due to stronger earnings and positive working capital, partially offset by some actions that were taken to support suppliers.

General Electric

Adding to that, as we can see in the chart above, on a full-year basis, revenue increased by 17%, orders improved by 25%, and profit, EPS, and cash generation all exceeded the high end of the company's guidance.

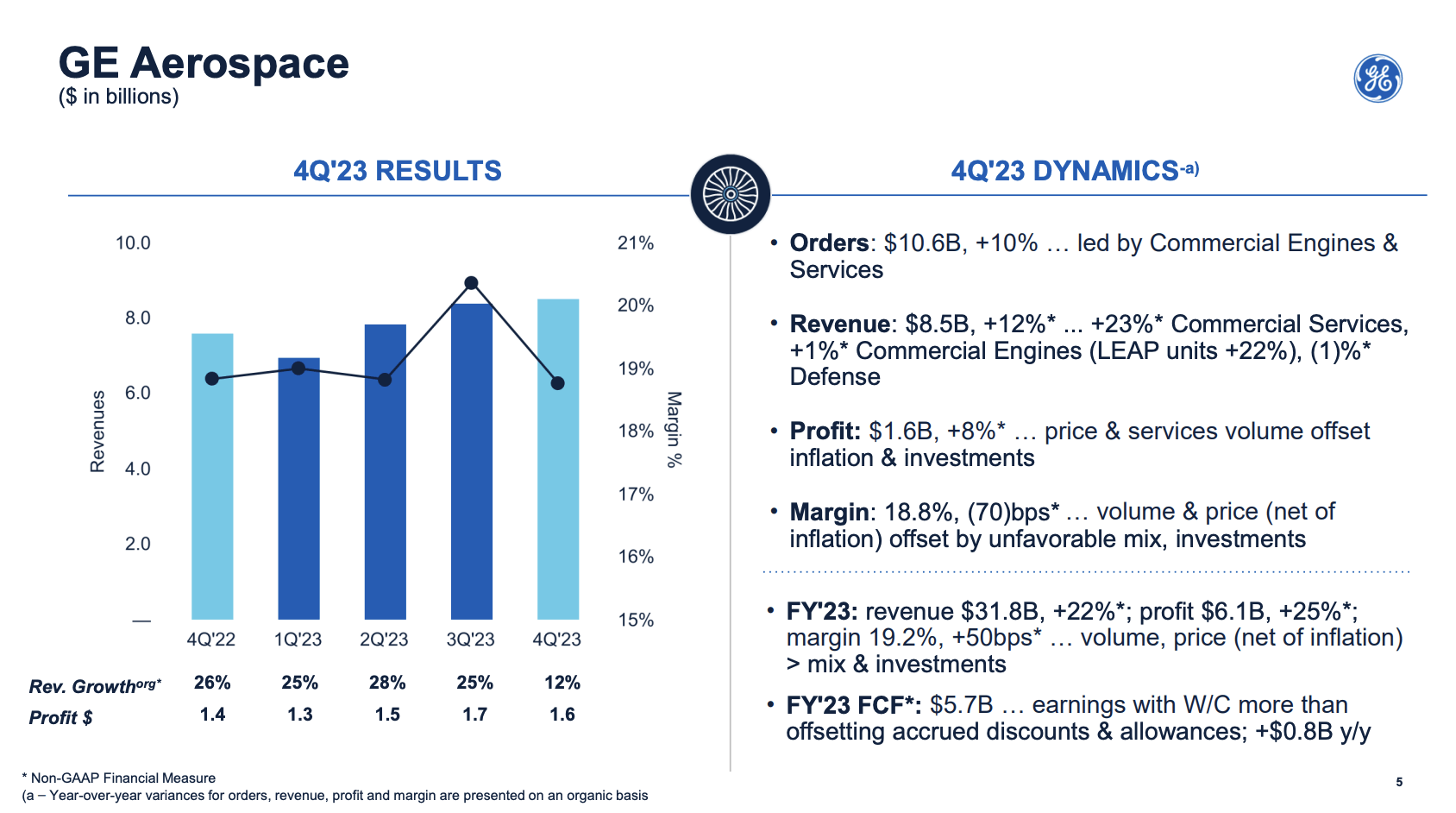

With all of this in mind, the biggest driver of growth is the company's bread and butter, the Aerospace segment.

After all, roughly 46 cents of every dollar in revenue in 4Q23 came from this segment, which benefited from strong demand as orders soared by 10%.

Revenue in this segment grew by 12%, mainly fueled by commercial operations.

Profit saw an 8% increase, which the company said was due to higher services volume and pricing, partially offset by unfavorable equipment mix and higher investments.

As a result, margins remained relatively flat compared to 4Q22.

General Electric

Digging a bit deeper, we find that in the commercial sector, services revenue increased by 23%, driven by both volume and pricing.

According to the company, external spare parts also saw a significant increase, which I can confirm from the countless earnings calls from peers I have listened to in recent months.

Meanwhile, lean initiatives enabled capacity expansion and cost reduction, which is valuable at a time when inflation is still sticky.

Moving over to the anti-cyclical division, defense, the company reported that revenue in this area decreased by 1%, primarily due to lower service revenue.

However, equipment grew by double digits from higher combat engine deliveries.

On a full-year basis, the Aerospace segment reported a 22% increase in revenue. Commercial services grew by 30%, and commercial engines saw a 21% increase.

Defense revenue grew by 7%, with a book-to-bill ratio of approximately 1.2x, which indicates that for every $1.00 in finished work, the company received $1.20 in new orders. This is indicative of higher revenue growth in the future, as there's always a delay between order growth and revenue growth.

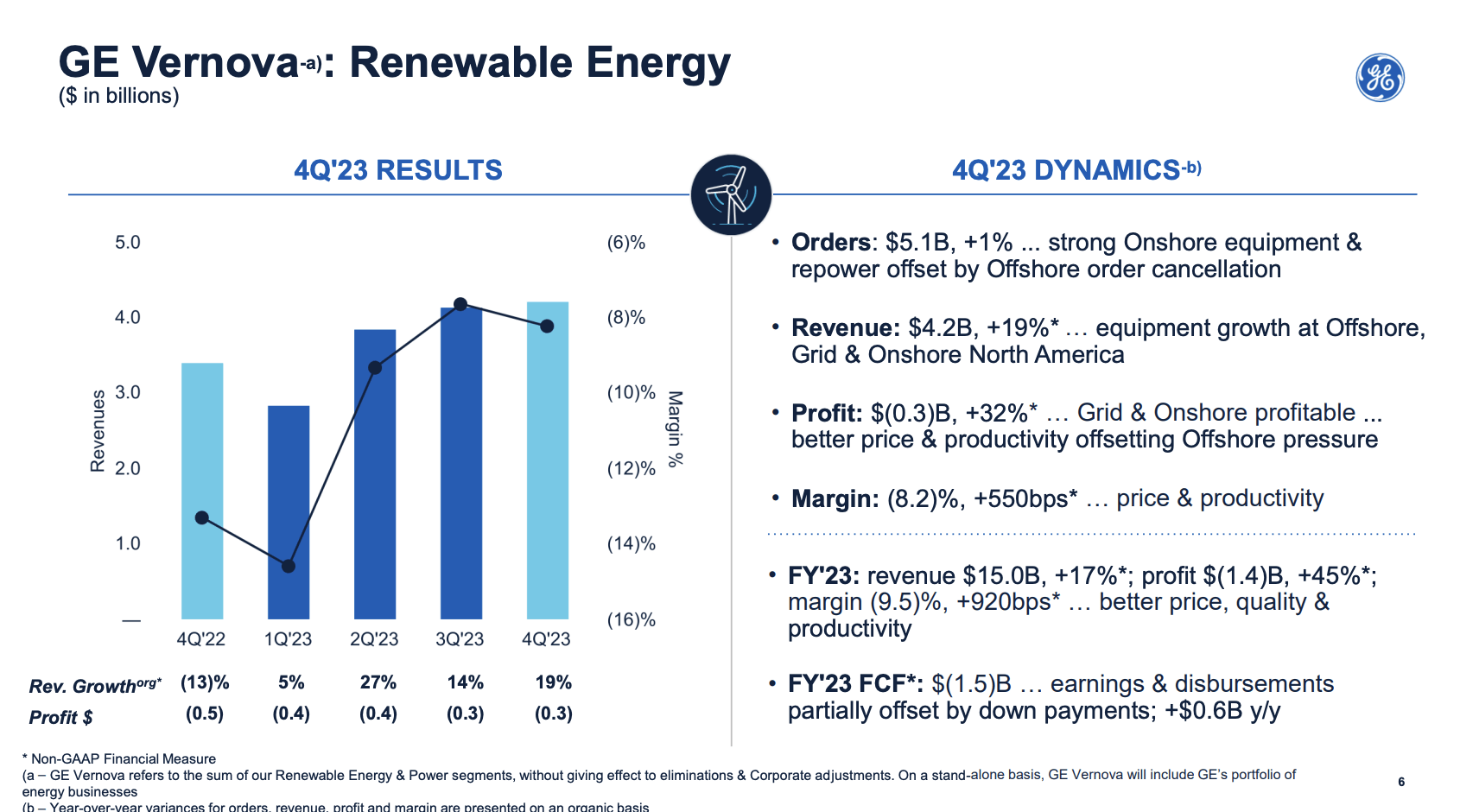

GE Vernova Renewable Energy, a segment that will be spun off, also performed well, with revenue improving by 19%. Profit soared by 32%.

General Electric

According to General Electric, the Renewable Energy segment of Vernova, saw a significant operational turnaround, leading to substantial improvements.

Orders in the fourth quarter exceeded $5 billion, with double-digit revenue growth and notable profitability in certain segments such as Onshore and Grid.

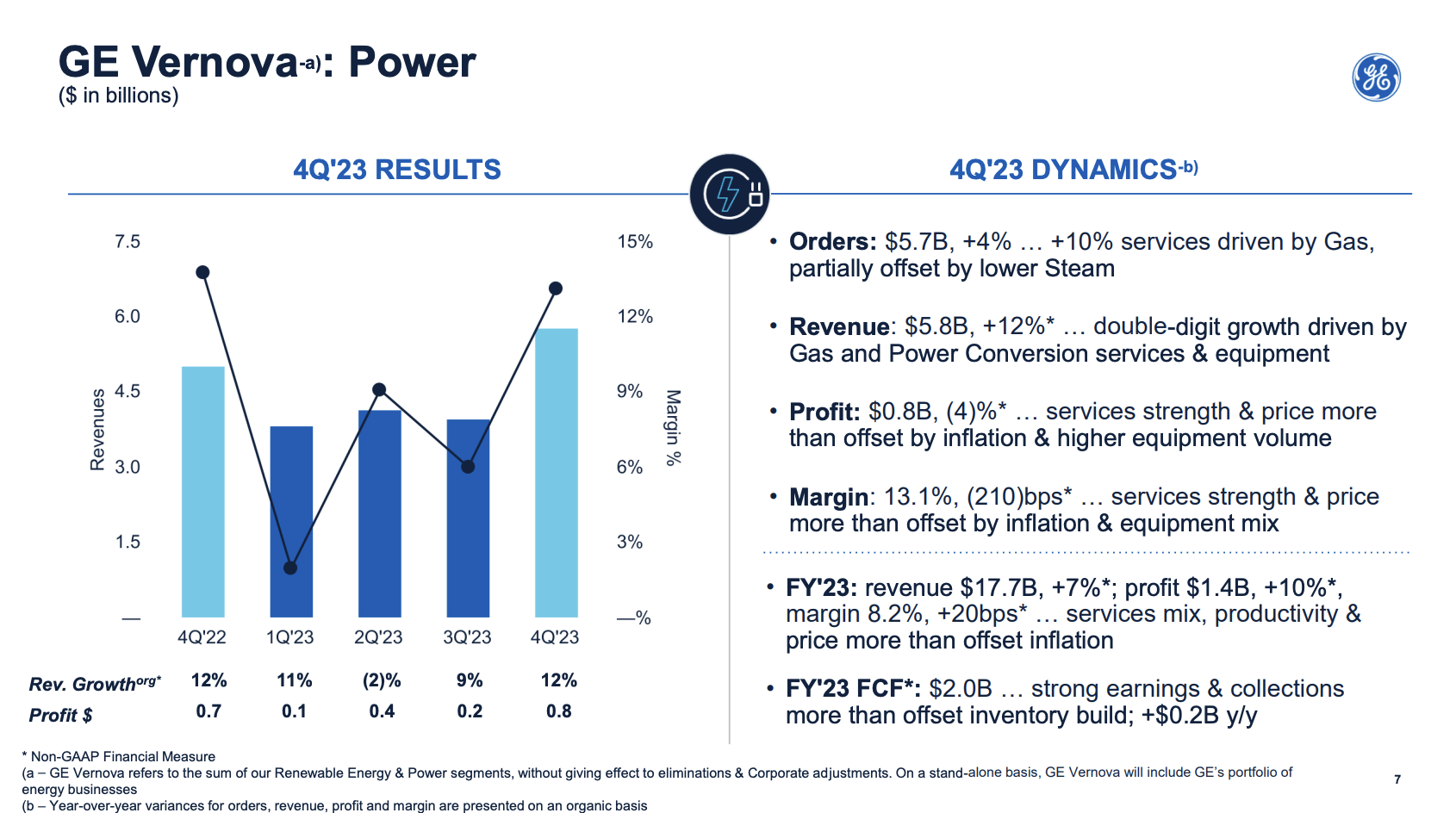

Its peer, the Power business, also reported a strong performance, with a 4% increase in orders and 12% revenue growth.

Services, mainly gas services, drove profitability, although margins contracted due to higher equipment volume.

General Electric

So far, I'm impressed by the company's performance, which shows a rebound in renewables and impressive strength in its flagship segment, aerospace.

The best news is that this is expected to continue.

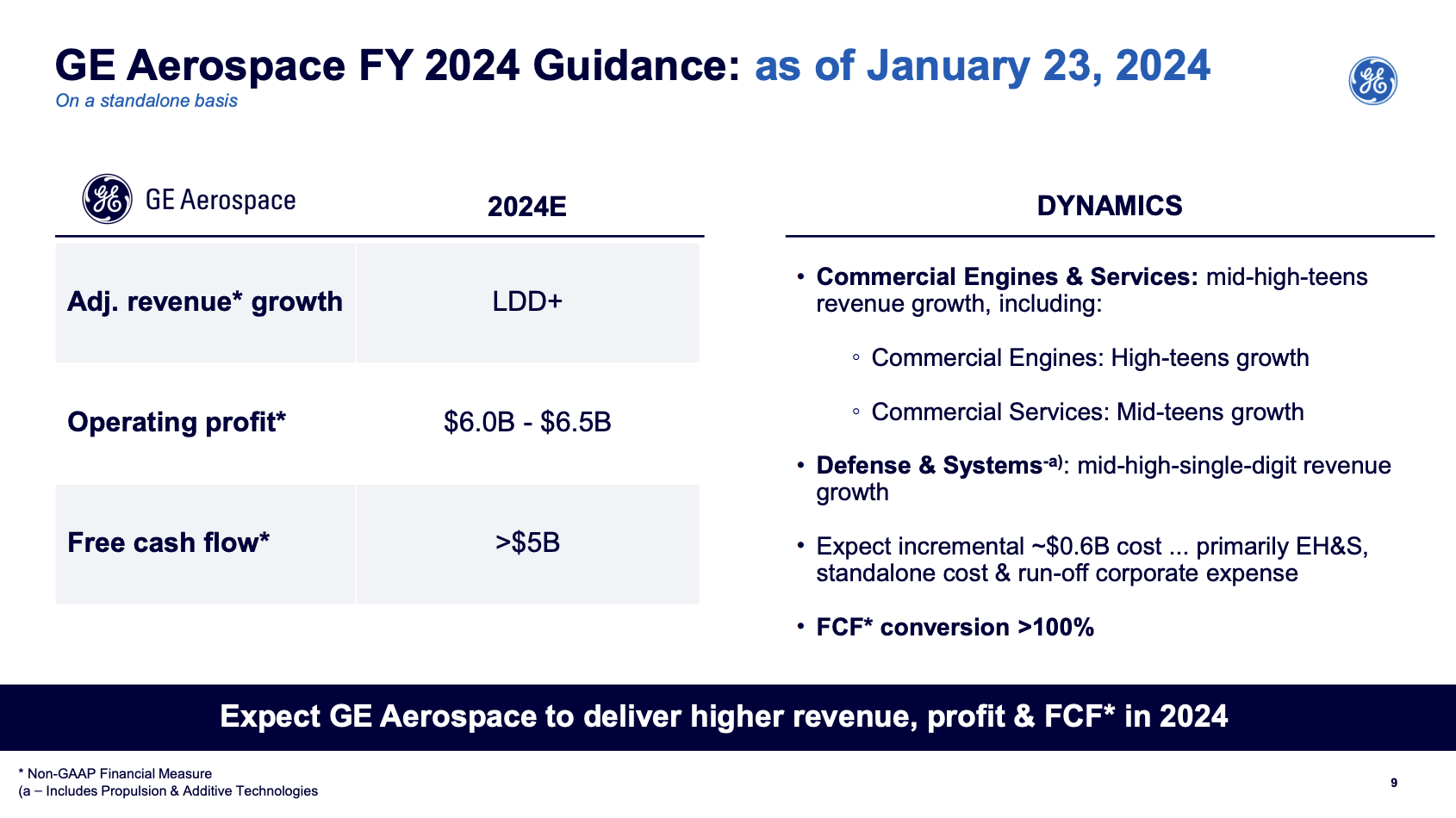

The guidance for GE Aerospace forecasts solid revenue growth, particularly in the commercial, defense, and systems segments. In other words, in all areas that matter!

For example, commercial growth is expected to be driven by engines and services, while defense and systems segments are projected to see mid to high single-digit growth.

Meanwhile, operating profit is expected to improve by double digits at the midpoint of the company's guidance range, with investments in growth areas such as LEAP and the 777X platform.

This is what the company said during its earnings call with regard to LEAP demand.

Myles, I think from a from a CES or commercial engine and services perspective. We're going to see engines lead the way, engines will be up high teens plus, I think you're going to see services in the mid-teens area. Specific to your question from a LEAP perspective, what we anticipate right now is a 20% to 25% increase in unit growth, I think we'll see installs get ahead of spares so that spares ratio will begin to moderate, more in line with the historic average of a typical lifecycle. So that's really where we are with respect to the narrowbody specifics you have there. - GE 4Q23 Earnings Call

Free cash flow is expected to end up north of $5 billion, boosted by a strong earnings conversion rate of more than 100%, which is a sign of high-quality earnings.

General Electric

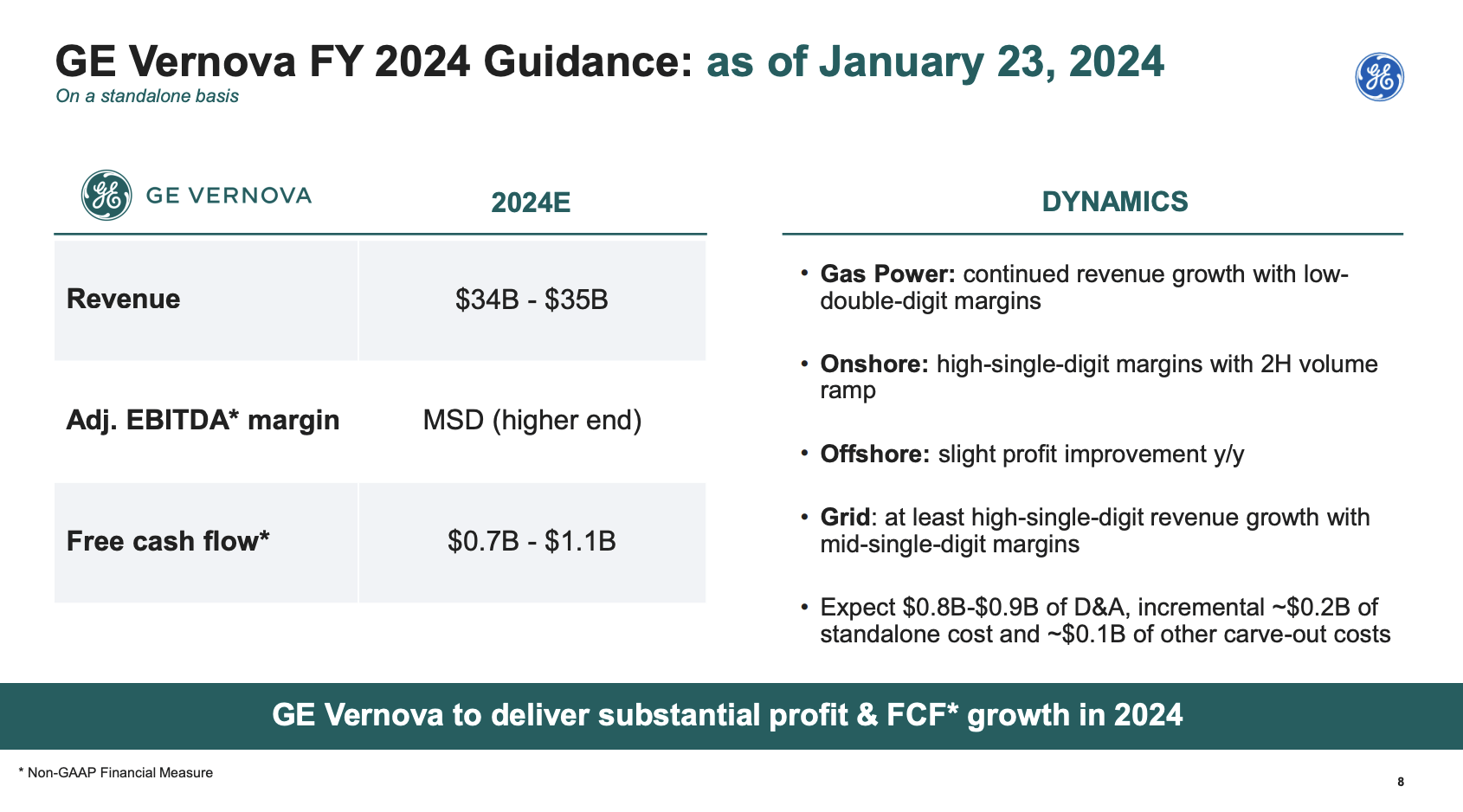

4Q23 was also the last time that GE included Vernova numbers in its financials.

While we will get a lot more color during the March Investor Conference, the company is guiding for at least $34 billion in segment revenue this year, fueled by growth in gas, onshore, offshore, and grid operations.

Personally, I'm very bullish on grid operations, as I expect that the next two decades will be all about improving grid capacities for the energy transition and the demand that comes with data center electricity requirements.

General Electric

On top of benefitting from strong demand and improving margins, the company also fully exited its equity stake in AerCap.

Furthermore, with regard to its dividend, the company's March Investor Conference will include a full overview of its capital priorities, which is a lot easier to establish once the spin-off has been finalized.

This is what Mr. Larry Culp said during the earnings call:

I think in aerospace, that you should assume that we're going to have a compelling dividend. That buybacks are going to be an important part of that overall effort beyond just covering dilution. And we'll certainly look to do meaningful value accretive M&A, the mix, the timing, those details to come. I really want the GE Aerospace board to have more time with those important questions.

A "compelling dividend!"

According to Merriam-Webster, "compelling" means "convincing," which is all we have to guess what the company's future dividend may look like.

Currently, GE yields less than 0.3%.

The good news is that we have some data to work with, which shows that the dividend could, indeed, become "compelling" in the years ahead.

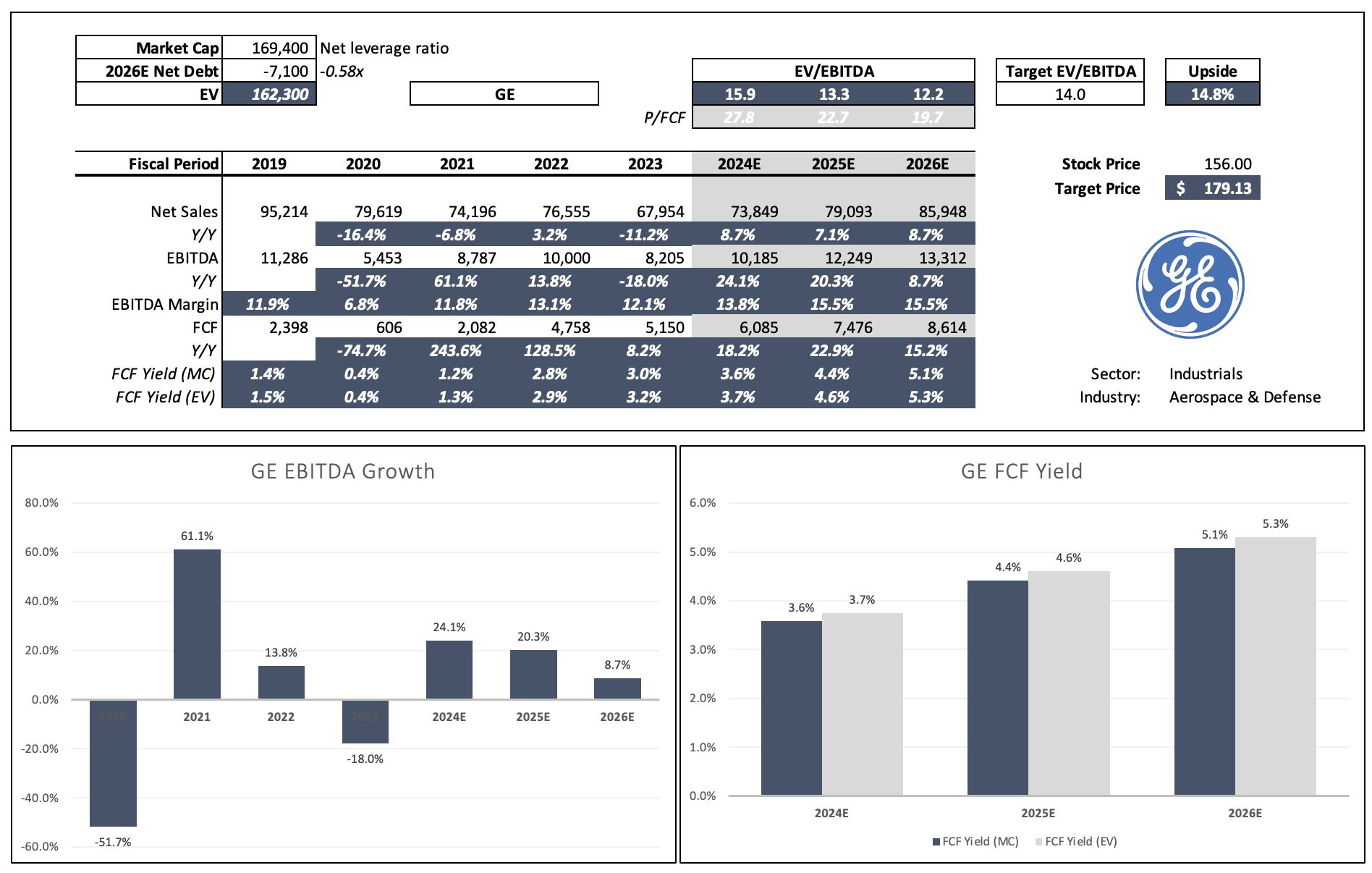

Looking at the data below, we see that analysts agree with the company when it comes to future growth expectations.

The company is expected to maintain >20% annual EBITDA growth in both 2024 and 2025, potentially followed by high-single-digit growth in 2026.

Free cash flow is expected to grow to $8.6 billion in 2026, which would translate to a free cash flow yield of more than 5%.

In other words, if the company were to spend all of its free cash flow on shareholders, it could pay a dividend of 5%. That won't happen, but it shows that there's a lot of room for future distributions.

Moreover, the company is expected to end up with more than $7 billion in net cash in 2026, which means that it is expected to have more cash than gross debt. This supports my expectations that a lot of free cash flow will end up in investors' pockets in the years ahead.

Leo Nelissen - Based On Analyst Estimates

Furthermore, if we apply a 14x EBITDA multiple, which I believe is totally fair for this growth profile, we get a fair price target of roughly $179, which is 15% above the current price.

The current consensus price target is $158, which makes me a bit more bullish than the average analyst.

Having said all of this, I remain bullish on GE. I still like the valuation and believe that the company has the right business model to maintain elevated growth on a long-term basis. This also bodes well for shareholders, as it is rapidly generating cash.

However, because the stock is up more than 40% since my most recent article, I'm going with a Buy rating instead of a Strong Buy rating.

While this is technically a downgrade, I see it as a sign that I would wait for a correction before deploying a "large amount" of cash on GE stock.

On a long-term basis, I also have little doubt that it can continue to outperform the S&P 500.

Now, I'm looking forward to the March Investor Days, which will reveal a lot about the future of GE as a standalone company and what investors can expect in terms of capital returns.

My takeaway from diving into General Electric's recent performance and future prospects is clear: GE is not just back on track; it's racing (or flying?) ahead.

Despite a staggering 60% rally last year, GE's stock still has room to soar.

Why?

Because the company is firing on all cylinders, particularly in its aerospace segment, which accounts for nearly half of its revenue.

With strong demand, margin expansion, and impressive growth in both commercial and defense sectors, GE is poised for continued success.

It also has the right products for the right customers, which helps tremendously.

Meanwhile, the guidance for future growth, coupled with interesting dividend comments, makes GE an enticing investment opportunity.

While I'm slightly lowering my enthusiasm due to the recent surge in stock price, I maintain a bullish outlook on GE's long-term potential.

Pros:

Cons: