Win McNamee

Win McNamee

There is no doubt that we're in the age of the Internet. When you look back over the past few decades, virtually everything has changed, and industries that were once rock solid simply don't work the way they used to.

The obvious example of this is newspapers. Gannett Co., Inc. (NYSE:GCI), the publishers of hundreds of daily newspapers as well as USA TODAY, has gone from a publishing powerhouse to a company desperately trying to redefine itself around digital media, with online publications and LocaliQ digital marketing looking like the company's real future, and print media, to the extent that it will continue to exist, will become more a niche.

That's not to say that Gannett, with its highly respected news outlets, can't make it as a digital media company. Having freshly released the Q4 and FY2023 earnings release, we see a miss over what was expected in earnings, but very healthy growth in the digital segment. So long as the company continues to execute we will be looking at a very unrecognizable Gannett, all told, but potentially a fairly profitable one that remains at the forefront of American news.

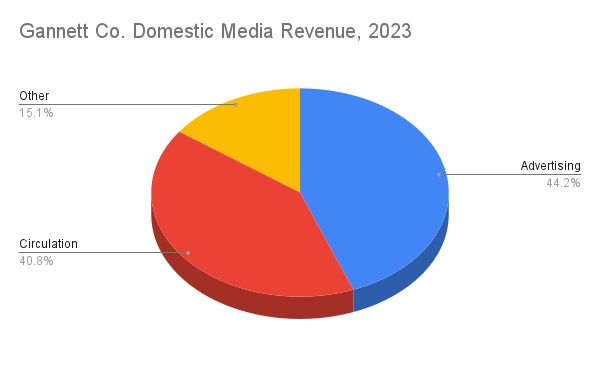

Gannett is a lot more than just USA TODAY, even though clearly that is what they are best known for. Small market local newspapers are the real bread and butter of nationwide circulation, reaching some 220 local markets in 43 states around the country.

10-K

This amounts to 1.2 million print subscribers in America, a pretty healthy number in spite of all that has already happened to the weaker market for print publications. That's not even most of the sales, either, as the company continues to enjoy strong circulation of single-copy sales in stores around the nation, especially for USA Today.

In the United Kingdom, the model is much the same, only print media appears somewhat more robust there. Gannett's wholly-owned subsidiary, Newsquest has hundreds of small and medium-sized newspapers and digital media brands, from the Eastern Daily Press of Norwich to any number of newspapers like The Herald in Glasgow, Scotland.

In the UK, Gannett reaches an average of 4.2 million print readers per week, which is pretty significant. There again, the trend is toward digitizing content and serving publications online to readers.

Doing that requires not just online subscriptions, but a fairly robust online advertising effort. Here we see Gannett doing quite well, with LocaliQ showing steady growth, 20% year over year on digital ad revenue.

What was meant to be a Q4 with 8 cents of earnings ended up a 16 cent loss. That's a nasty surprise, but given the state of the newspaper industry, no negative news can ever really be called a surprise.

It's not all bad though, as the conference call clarified a number of points on which the overall year ended on a fairly upbeat note, and looking forward to being a digital platform with double-digit growth.

On the plus side, they enjoyed record highs in digital-only subscription revenue and ad revenue, and with 187 million unique monthly visitors, they commented that "more people are ready and watching us than ever before."

One of the important new customer bases is their "core platform" customers, an estimated 15,000 people on which they enjoy double-digit margins and a retention rate of more than 95%.

All that growth toward record digital levels isn't over, either, with an expectation of 2024 enjoying even higher growth on that front than 2023. The conference call projected double-digit growth.

Analysts were projecting 2024 revenue to be down a few percent from 2023, and it could well be that we're in for a bit more upside than expected, especially given this is an election year, always good for the media. 2025 is where they are supposed to experience both growth and a return to profitability.

| Cash and Equivalents | $100 million |

| Total Current Assets | $444 million |

| Total Assets | $2.181 billion |

| Total Current Liabilities | $533 million |

| Long Term Debt | $565 million |

| Convertible Debt | $416 million |

| Total Liabilities | $1.86 billion |

| Shareholder Equity | $317 million |

(source: most recent 10-K from SEC)

When we start to look at the financial state of Gannett, we find things aren't nearly so dire. Over $100 million in cash on hand, and a fairly substantial debt balance that's declined in 2023, and according to the conference call, should drop another $110 million this year.

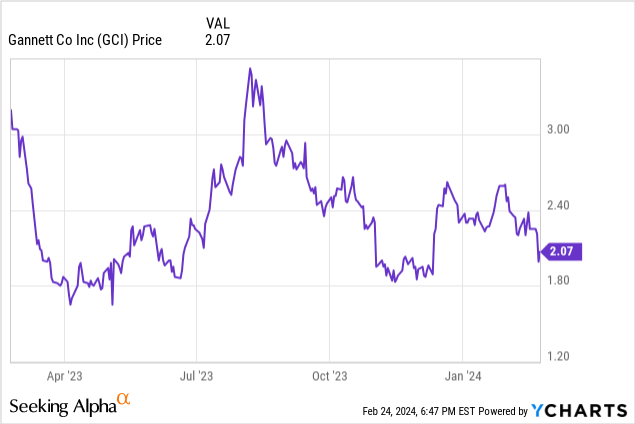

A good start on making the value case for Gannett though is price/book value, which is 0.93. Any time we can get a price/book below one it's always a good sign, it means we can buy assets at a discount. Market pessimism has driven the price down to the point where here too that's an option.

| 2021 | 2022 | 2023 | |

| Revenue | $3.2 billion | $2.9 billion | $2.66 billion |

| Op Income | $109 million | ($34 million) | $86 million |

| diluted EPS | ($1.00) | ($0.57) | ($0.20) |

(source: most recent 10-K from SEC)

Here we can see the decline in revenue, but also luckily, the decline in diluted losses per share. What's really an eye-opener is if we look at analysts' projections for 2024 and 2025. Revenue bottoms out in the first year and starts growing again in 2025. EPS too is in the same direction, trending to an even smaller loss of a mere 6 cents per share in 2024, and by 2025, a profit of 26 cents.

That's a very forward-looking PE to be talking about, but if the 26 cents pans out, we have a forward PE ratio of 7.69. Between that and the book value, we're squarely in value territory, if we're willing to buy and wait.

Vying for eyeballs in the digital space is highly competitive, and while reputation means a lot, continuing to build a digital media empire is not a sure thing, where they're definitely going to be successful.

Another open question is if traditional advertising revenue can truly be replaced by digital ads. Early growth and margins suggest it very much might be, and there are plenty of large digital companies for which digital advertising content is very much paying the bills.

But where we stand in the economic cycle could be an issue, as a worse economy could mean less advertising and less value to the ads they do get. The economy seems fairly strong right now, but it is important for the company to grow while the opportunity presents itself so it can weather the inevitable downtimes with a strong market presence.

The debt, which as I mentioned before they are paying down, is a concern. It doesn't come due until 2026 and 2027, respectively, but this again is very important for the company to grow into managing it before it becomes due, otherwise, they might need to replace it with an even worse deal with higher rates of interest.

There are a lot of risks, but at these prices, it seems like they may be a risk worth taking. A P/E ratio in the 7s and a price/book value below one may look reasonable for a company in a distressed industry. If they recover like I'd argue they're poised to, I believe it is an absolute bargain.

We also have a lot of recent insider transactions on the bullish side. Clearly, these people also believe that a purchase within the $2 range, give or take, is a risk worth taking. I wouldn't dedicate a huge amount of portfolio space to such a risky stock, but there is definitely room in some portfolios to take a flier on it.