????? ???????/iStock via Getty Images

????? ???????/iStock via Getty Images

It's been just over a month since I suggested that GATX Corporation (NYSE:GATX) was "closer, but not yet." Since then, the shares are basically flat against a 3% gain for the S&P 500. Since the company has released earnings again, it's time to see whether the shares have arrived. I'll review the financials, and the valuation to see if it makes sense to buy today or not. In particular, I want to see if the shares are cheap relative to their own history and the overall market, but also in relation to alternatives available to investors.

Those who read me regularly know that I put a thesis statement at the beginning of each of my articles. This gives readers the opportunity to get the highlights of my thinking about a given name, and then get out again before my writing becomes insufferable as it's been known to do. You're welcome. Although I think the latest financial results were decent enough, too much of this year's earnings related to gains on the disposition of assets, which is obviously not as sustainable as other sources of income. More pressingly, the level of indebtedness is up by about 50% over the past 5 years, which is quite a remarkable feat. This has led to an inevitable uptick in interest expenses, and I think this is ultimately bad news for those assuming dividend growth will continue at the relatively healthy pace it's enjoyed over the past decade. Most troubling of all, in my view, is that the risk free Treasury Note offers significantly higher returns than does this stock. I remember reading years ago that people would buy stocks because "there is no alternative." That may have made sense when interest rates were much lower than they are now but makes zero sense today. The wheel of fortune has changed, and Treasuries offer much less risk and much greater return potential than stocks at least at the moment. Given that, why would an investor buy this? Put another way, this stock offers lower returns and higher risk than an alternative that is freely available. Given that, it makes no sense to buy GATX in my view.

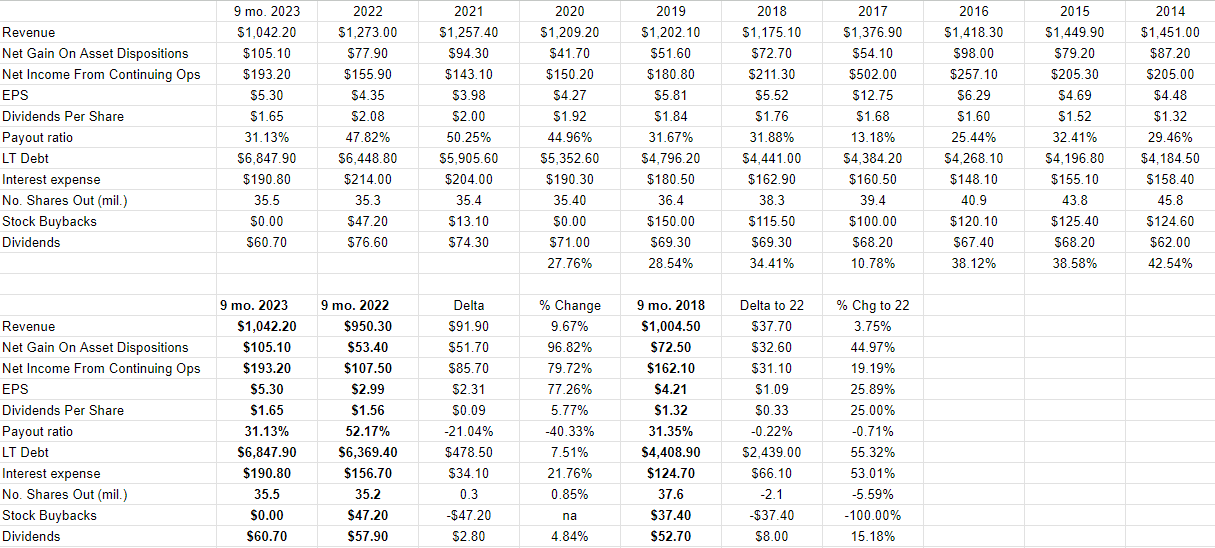

The financial performance over the past year has been reasonably good in my estimation, though not as good as it might at first appear. Specifically, revenue and net income are higher by about 9.7% and just shy of 80% respectively when compared to the same period in 2022. Before we get too excited, though, I feel compelled to point out that about $51.7 million of the $85.7 million improvement came in the form of a net gain on asset dispositions. These are, by their nature, non-recurring, so I think it prudent to take these results with a grain of salt. My "glass half empty" reading of these results, aside, though, we can't help but notice that earnings are up nicely from the same period a year ago. Management has rewarded shareholders by increasing the dividend by about 5.8%.

My biggest source of concern here relates to the capital structure, given that long-term debt is higher by $479 million, or 7.5% relative to the same period a year ago. Worse, long-term debt is about $2.4 billion, or 55% higher than it was in 2018. This might go some way in explaining why interest expense is up about $34 million or about 22% when compared to 2022 and is fully 53% higher than it was in 2018. The level of indebtedness is heading in the wrong direction in my view, and I think it unreasonable to continue to expect growing dividends in the teeth of growing debt and the resulting interest expenses.

GATX Financials (GATX investor relations)

In my view, investors don't seek "returns." investors seek "risk-adjusted" returns, and that means that when we choose to buy X, we are, by definition, eschewing any number of Ys. We would buy the "X" in the example above if we think it offers us a better risk-adjusted return. The implication of this is that if an investment offers less risk, but more return than a given stock, why would you buy the stock?

With that small sermon as a preamble, I want to compare GATX to a risk-free investment to see if investors are currently being adequately compensated for the risks associated with the stock. After all, if an investor can earn 4.4% on a risk-free, 10-year Treasury Note, The reasons for investing in this particular stock with its 2.2% dividend yield become far less obvious. As I've said many times recently, TINA doesn't live here anymore.

Because I'm a math nerd, I feel compelled to calculate exactly how much investors would need from the capital gains on this stock to simply match the cash flows they'll get with the risk-free investment. Note, that a stock should offer more than a risk-free investment, so these are bare minimum implications, but I think the exercise is worthwhile. I'm going to pose a specific question: by what amount will the dividend need to grow for the stockholders to receive the same amount of cash as the Noteholders over the next decade? I've produced the answer to this question for your enjoyment and edification in a table below.

GATX v Treasury Note (author calculations)

As I calculate in the table above for you, the dividend will need to grow at a CAGR of about 13.2% over the next decade for stock investors to simply match the interest income offered to Treasury holders. This obviously doesn't take into account the time value of money, but if we did, things would look even worse for the stock since the fast-growing dividend doesn't overtake the amount received by the Treasury Note until year 6, and then only barely. Finally, I feel compelled to point out yet again that an investor in any stock should demand higher compensation for a risky stock, so a growth rate of "only" 13% barely gets us to the starting line in the competition between these two. Lastly, I feel compelled to point out that the dividend has grown at a CAGR of only 5.9% over the past decade. This is impressive in my view, but I doubt the company can maintain this growth rate, especially given the current state of the capital structure.

Since everything in the domain of investing is relative, I would recommend continuing to avoid this name in favour of the much less risky, much more "returny" Treasury Note.