imaginima

imaginima

Rising rates have impacted asset classes across the board, ushering in an unprecedented era of investing. A rapidly rising Federal Funds rate impacted income-producing investments across the board as valuation pressure proved inescapable.

However, one sector remained insulated. In fact, rising rates served as a significant tailwind for these lenders in general. The past two years have put a spotlight on business development companies, or BDCs.

BDCs are specialty finance companies that act as capital providers for middle market companies. Middle market companies are generally too small to interact with investment banks or traditional financial institutions. Given the risks associated with investing in the middle market, BDCs usually make senior secured loans with high interest rates to offset the risks of working with these uncreditworthy borrowers.

So, why have rising rates benefitted these specialty lenders? Typically, income producing investments like REITs and bond funds invest in fixed rate assets. Investments with a fixed coupon or capitalization rate are negatively impacted when interest rates rise due to opportunity costs. As rates rise, value is negatively impacted. Compounding the pain, these investors are now forced to refinance their debt at higher interest rates, meaning rising interest expenses.

However, BDCs typically issue debt at a fixed rate and invest the proceeds into floating rate loans. As liquidity and lending activity spiked coming out of the pandemic, BDCs issued long term, fixed rate debt at rock bottom interest rates. The proceeds were invested in floating rate loans buoyed by SOFR. As the federal funds rate increased, SOFR increased. For BDCs, this meant increasing interest income while their interest expense remained steady.

The Goldilocks scenario translated to a strong performance. The past two years have been exceptional for BDCs.

However, rates appear to have levelled off, meaning there is little room left to run. With the tailwind dying down, BDCs may not have much juice left in terms of gains on existing loans. Going further, the conversations around rate cuts mean there is a possibility interest income could begin to decline as soon as this year. While a benefit to other investments, BDCs may struggle with the same factors that fueled their success.

BDCs are complex companies with intricate strategies and operations. They can be comparable at a high level to REITs, but are more complex at the operational level. As with other similar investments, not all BDCs are created equal.

Today, we are going to follow up on one of the best BDCs in the business. Gladstone Investment (NASDAQ:GAIN) is a BDC with an entirely unique strategy. Focusing largely on buyouts and equity investments, we will explore why GAIN is positioned to thrive, even if interest rates begin to fall.

Gladstone Investment is a publicly traded BDC focused on the acquisition, recapitalization, and ongoing management of mature, middle market companies across three segments, manufacturing, consumer products, and business/consumer services. GAIN does not invest in startup or venture capital targets.

GAIN typically makes debt investments between $5 million and $30 million and equity investments between $10 million and $40 million. GAIN actively targets companies with revenue in the range of $20 million and $100 million and EBITDA from $4 million to $15 million. GAIN seeks minority ownership of targets and prefers to hold a board seat. GAIN's typical hold period is seven years with an exit via recapitalization, initial public offering, or sale to a third party.

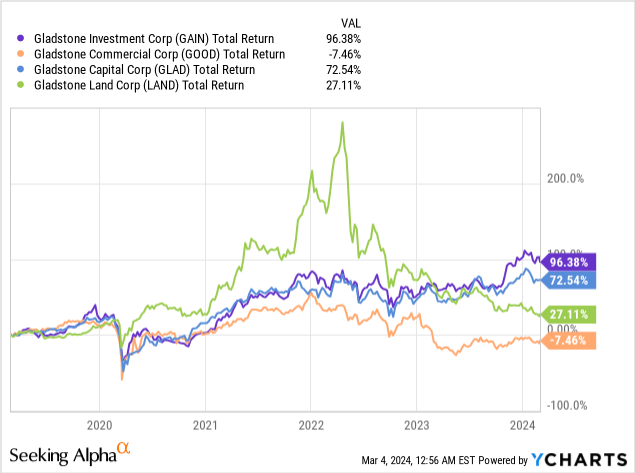

GAIN is a smaller BDC with a market capitalization of $500 million and an enterprise value of nearly $1 billion. GAIN is one of four externally managed, publicly traded funds sponsored by Gladstone Companies. Gladstone also manages Gladstone Commercial (GOOD), Gladstone Land (LAND), and Gladstone Capital (GLAD). The Gladstone lineup are externally managed companies and famous for distributing monthly dividends. GAIN remains the strongest performer in the lineup by a significant margin.

GAIN emphasizes recession-resistant companies that have proven themselves through thick and thin. GAIN's strategy focuses on acting as a turnkey provider of equity and secured debt to effect "change of control buyouts". GAIN wants an opportunity to affect change at the operational level. GAIN typically targets an investment mix of 25% equity/75% debt at cost/origination.

GAIN

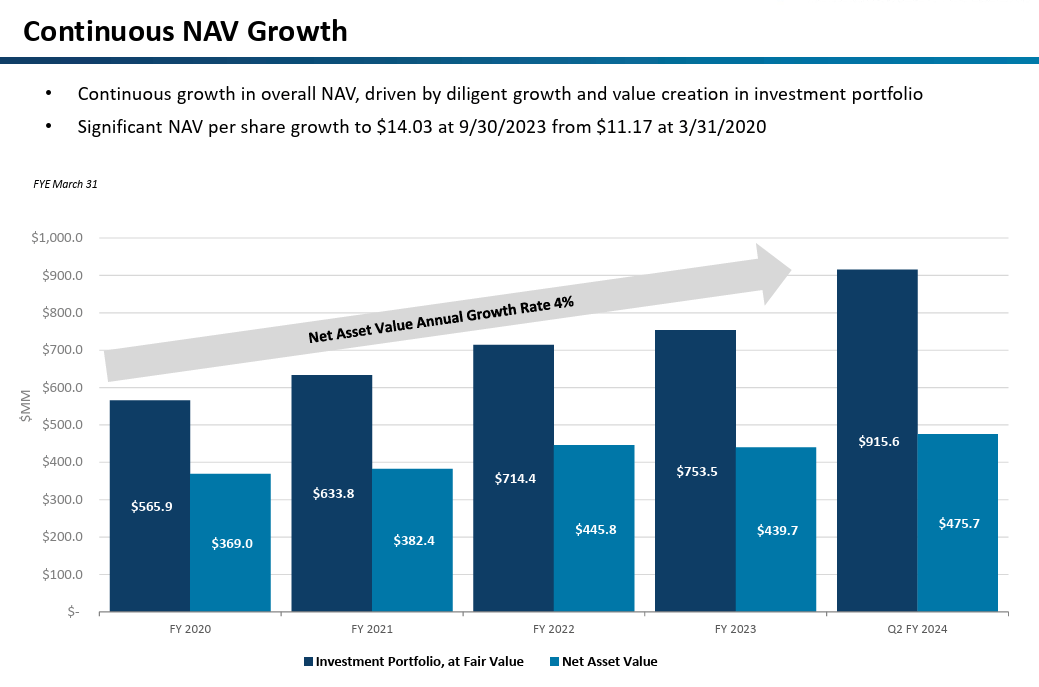

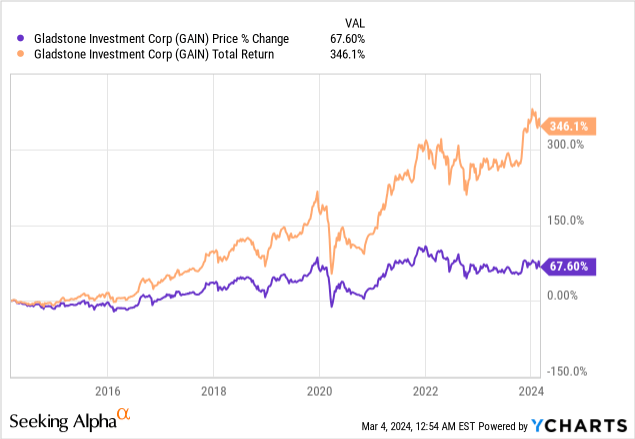

GAIN's mix of debt and equity investing has been largely successful, contributing to a growing dividend and net asset value. Over the past five years, GAIN has grown enterprise value significantly while also creating value at the share level. Since 2019, GAIN has exited from at least 13 companies, generating $354 million in total proceeds including meaningful gains.

GAIN

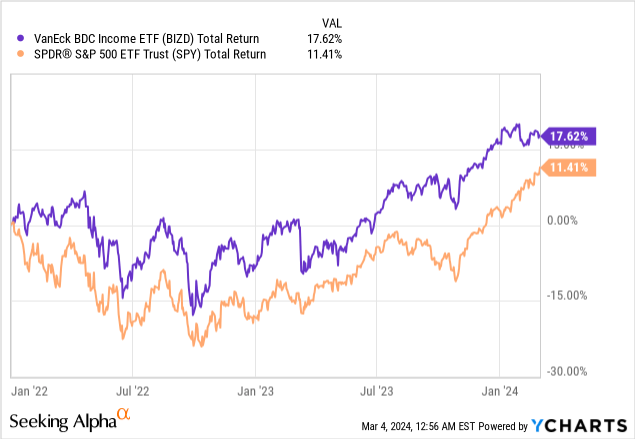

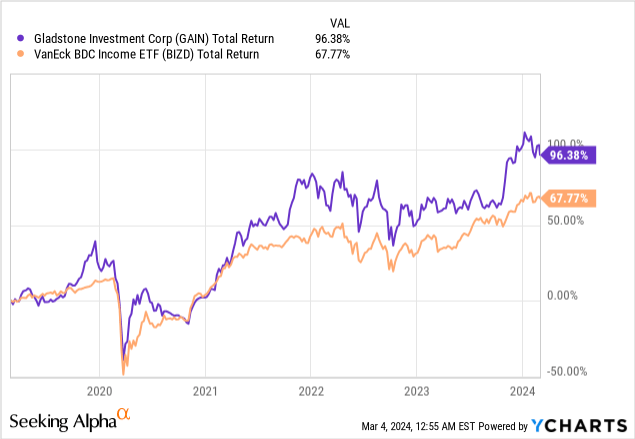

The BDC sector has been a powerhouse over the past two years. The macroeconomic environment has been favorable across the board. That said, rising rates would act as a particular benefit for debt-heavy BDCs with the largest floating rate allocations. Even still, GAIN continues to lead the sector, beating the index by a noteworthy margin.

GAIN's blend of equity and debt means shareholders receive routine cash flow from interest income, supplemented by larger capital gains from the exit of portfolio companies. The strategy is evident in GAIN's dividend distributions. GAIN pays a $0.08 per share monthly dividend. GAIN supplements the monthly distribution with special dividends, typically on a quarterly basis. While shares of GAIN have appreciated due to NAV accretion, most of the return is powered by the company's dividend payments.

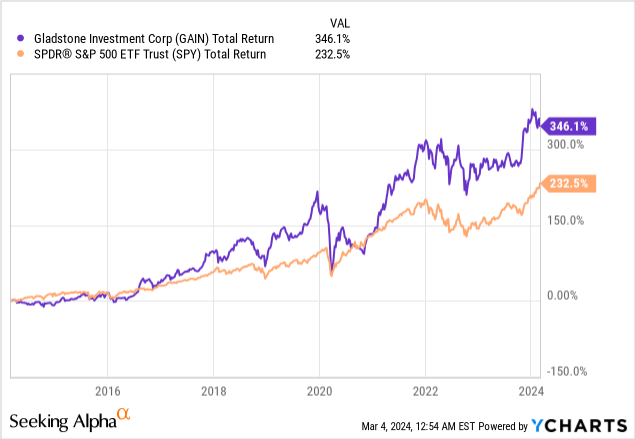

Looking further back, we will see that GAIN has an impressive track record. Since the Great Financial Crisis, GAIN has outpaced the S&P 500 by a significant margin in terms of total return. This highlights the accommodative environment which has benefitted private investors over the past decade.

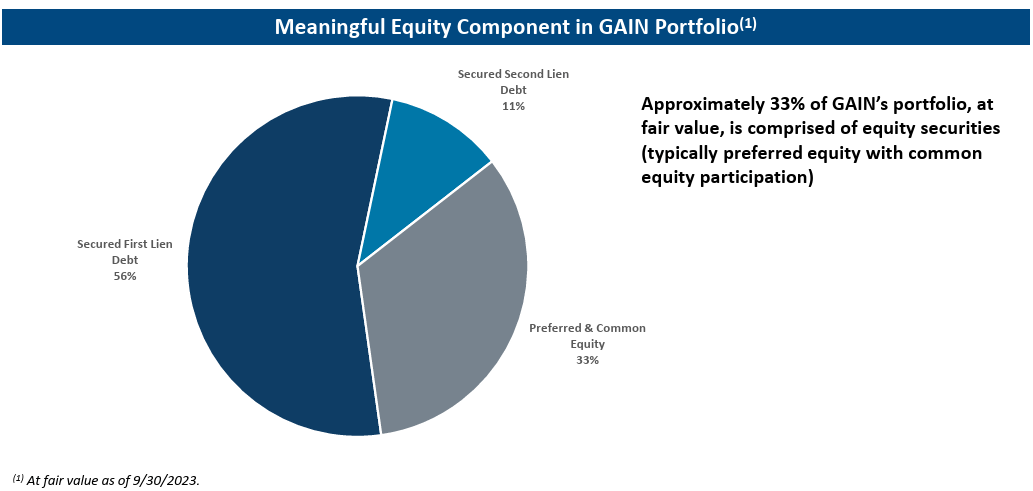

GAIN has a "not so secret" weapon that sets it apart from the broader BDC competition. The firm has a private equity-oriented strategy, focusing largely on the growth of target investments. Most BDCs are debt investors who collect interest income. While common for BDCs to seek an equity kicker in their investments, GAIN prioritizes equity investments in their strategy. Currently, equity investments stand at 33% of the portfolio.

GAIN

The debt portion of GAIN's investment is allocated through senior secured first and second lien debt. The equity portion of the portfolio is comprised of common and preferred stock. The preferred equity investment typically participates and has a coupon dividend of around 8%.

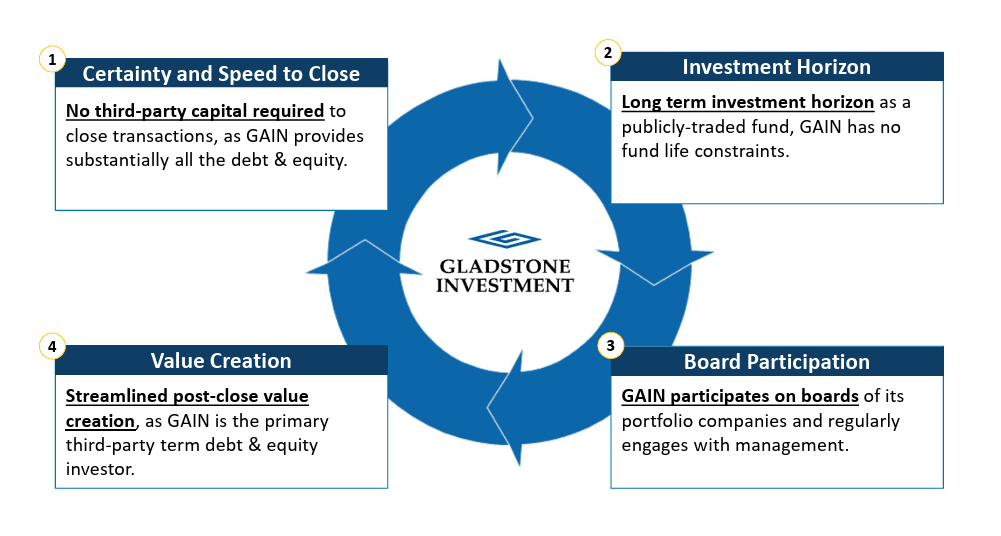

GAIN is unique against private equity competitors due to the Evergreen structure. GAIN is a perpetual investment, meaning it is not subject to capital calls, dissolution dates, or fundraising requirements. GAIN can issue capital at its discretion, creating significant shareholder alignment. Most private equity funds are launched with a fixed term. A fixed term means managers must invest capital at a rapid rate, recapitalize target companies quickly, and exit their position, all within a restricted time frame.

For fund management, this creates unwelcome pressure. In contrast, GAIN makes long-term decisions, irrespective of a potential dissolution date. This allows GAIN to be selective in their investments and disposition timing.

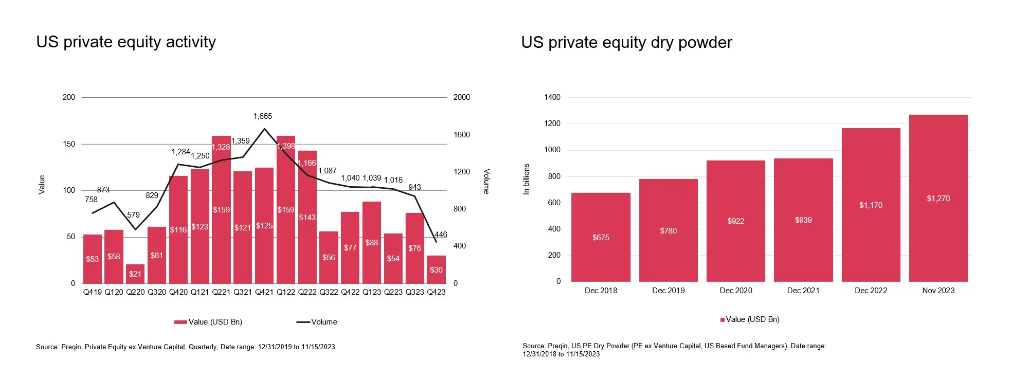

As we mentioned, GAIN is uncharacteristically dependent upon private equity in their strategy. GAIN has performed well despite fundamental weakness in the private equity sector over the past two years. Rising rates have materially halted the venture capital and growth markets due to a restrictive fundraising environment. In general, the private equity market was weak in 2023. PWC described the weakness in a recent report.

In 2023, private equity (PE) activity remained sharply down from its pandemic peak, reflecting stubbornly high inflation and correspondingly elevated interest rates and capital costs. Despite sitting on unprecedented capital, investors remained cautious, awaiting reductions in asset valuations to reflect cooler demand and tighter financing. Vendors, for their part, are willing to wait for the right suitor, extending hold periods to maximize exit value.

Putting this together, we see three key trends which will define private equity for 2024 and beyond:

A blurring of the lines between investor and operator: The critical need to drive value creation - both top line and bottom line - will take many PEs beyond their traditional comfort zone, forcing a more hands-on approach with a corresponding need for greater operating capacity and capability.

A relentless focus on cash and profitability: While continuing to drive growth, management teams will need to have an ever-closer eye on cash and operations, requiring CEOs to deliver margin expansion whilst continuing to drive growth, and further elevating the CFO role.

An increased need for creativity and flexibility in dealmaking: With credit continuing to be expensive, investors will need to be creative, focusing on smaller deals or minority investments, and potentially increasing equity checks.

Slowing activity has not decreased the rate at which dry powder amassed. Investable capital continues to accumulate in the hands of large institutional investors. Should the private markets begin to accelerate, investors will feel more comfortable deploying the capital.

PWC

The amassing cash waits for a crack in the ice that has kept the IPO market largely frozen. Encouragingly, the IPO market is beginning to thaw. With several large offerings on the horizon, large funds continue to accumulate capital and position themselves for the next wave of activity.

EQT just raised $24 billion for its largest ever private fund. Following the disclosure, we learned that the fund is already invested in a handful of global companies across pharmaceuticals and other growing industries. Additionally, other high profile names are eyeing the public market, including online platform Reddit, which is targeting a valuation of approximately $6.5 billion. Although GAIN does not invest in VC, acceleration in the private markets would be a significant tailwind for GAIN to begin exiting investments made during the pandemic era.

GAIN is one of few truly unique operators in the BDC space. While business development companies are typically a dime a dozen, GAIN is a private equity investor hiding as a public company. For shareholders, this means an opportunity to capitlaize on private investments in a liquid, scalable, and transparent format.

GAIN continues to trade at a small premium to net asset value, currently 1.06x. However, this premium/discount is more complex than meets the eye. Given the large allocation to equity investments, GAIN's portfolio is likely worth more than current NAV would suggest. GAIN continues to be a 'buy' off of strong tailwinds and an impressive strategy that continues to deliver.