AzmanL/E+ via Getty Images

AzmanL/E+ via Getty Images

As a stock picker, I have always been an advocate for examining a company's historical performance as that is a proxy indicator of many qualities, which include measurable metrics like revenue growth, income growth, operating margins, and qualitative factors like management's ability to grow the business and the moat of a business, whether it has been able to grow market share.

Genpact Limited (NYSE:G) is a strangely tough call for me to decide between a tentative BUY (i.e., DCA only) or a HOLD (i.e. do not buy).

Before I go into details, a brief look at the company's business.

According to the 2022 10K,

Genpact is a global professional services firm that... drive digital-led innovation and run digitally enabled intelligent operations for our clients, guided by our experience over time running thousands of processes for hundreds of Fortune Global 500 companies...

We serve more than 800 clients across many industries and geographies. Our clients include some of the biggest brands in the world, many of which are leaders in their industries, including about one fifth of the Fortune Global 500...

Genpact Cora, our AI-based platform, integrates our proprietary automation, analytics and AI technologies with those of our strategic partners into a unified offering...

We work with clients across our chosen industry verticals, which... are grouped within our three reportable segments, namely:

(1) Financial Services,

(2) Consumer and Healthcare, and

(3) High Tech and Manufacturing.

Why do these Fortune 500 companies seek Genpact's services? The larger a company grows, the more complex and intricate its processes become. With millions of data points at any one time, it will be difficult for any management team to improve its processes while simultaneously directing operations to win market share in a competitive landscape. Genpact helps its clients identify pain points and develop solutions to improve their efficiency, effectiveness, and agility.

In this case study, G helped a global snack manufacturer face challenges that come from changes in consumers' tastes, growing business volatility, predicting demand, and balancing its inventory to improve forecast accuracy is up by 25%, reduce excess inventory by more than 20%, and increase productivity by 40%. In another case study, through insights that G provided to help this insurer prioritize improvements, identify steps in the company's internal processes that led to late payments, and work closely with different divisions in the insurer, the client now has more favorable payment terms and better real-time visibility of reinsurance submissions.

Next, the three reportable business verticals will be given some details with added management commentary from the latest Q4 2023 earnings call.

Our Financial Services segment covers services we provide to clients in the banking, capital markets and insurance sectors. Our banking and capital markets clients include retail, investment and commercial banks, mortgage lenders, equipment and lease financing providers, fintech companies, payment providers, wealth and asset management firms, broker/dealers, exchanges, auto finance providers, clearing and settlement organizations, renewable energy lenders and other financial services companies.

According to CFO Mark Weiner in the Q4 2023 earnings call,

Financial Services revenue increased 4% year-over-year, largely due to large deal ramps, partly offset by continued pressure around client discretionary tax debt.

Our Consumer and Healthcare segment covers services we provide to clients in the consumer goods, retail, life sciences and healthcare sectors. Our consumer goods and retail clients include companies in the food and beverage, household goods, consumer health and beauty and apparel industries, as well as grocery chains and general and specialty retailers.

According to CFO Mark Weiner in the Q4 2023 earnings call,

Consumer and Healthcare revenue increased 2% year-over-year, largely due to ramping of finance and accounting and supply chain engagements, partially offset by pressure and discretionary tech spending, as well as the impact of the recent divestiture of business classified as held for sale last year.

Our High Tech and Manufacturing segment covers services we provide to clients in the high tech, manufacturing and services sectors. Our clients in the high tech industry vertical include companies in the information and digital technology, software, digital platform, electronics, semiconductor, and enterprise technology sectors. For our Data-Tech-AI services, we typically enter into software-as-a-service and/or consulting agreements with our clients depending on the scope of the services to be performed.

According to CFO Mark Weiner in the Q4 2023 earnings call,

High Tech and Manufacturing revenue increased 6% year-over-year, primarily driven by ramp of new logos within finance and accounting engagements across both Digital Operations and Data Tech and AI services, partly offset by the impact of reduction of scope from a High Tech client in early 2023.

In his presentation, outgoing CEO Tiger Tyagarajan proudly presented the company's full-year results,

Bookings for the full year reached $4.9 billion, up a strong 26% on a year-over-year basis, as we signed a record 14 new large deals, each with total contract value greater than $50 million. Inflows remained healthy, resulting in a high-quality pipeline that reached near-record levels as we exited the year. Win rates increased to 60% versus 51% in the prior year and we added 91 new logos. Sole sourced deals represented 40% of bookings below our typical 50% level, reflecting the much higher number of large deal wins, which tend to be more competitive.

On the surface, business is growing and all is well at Genpact.

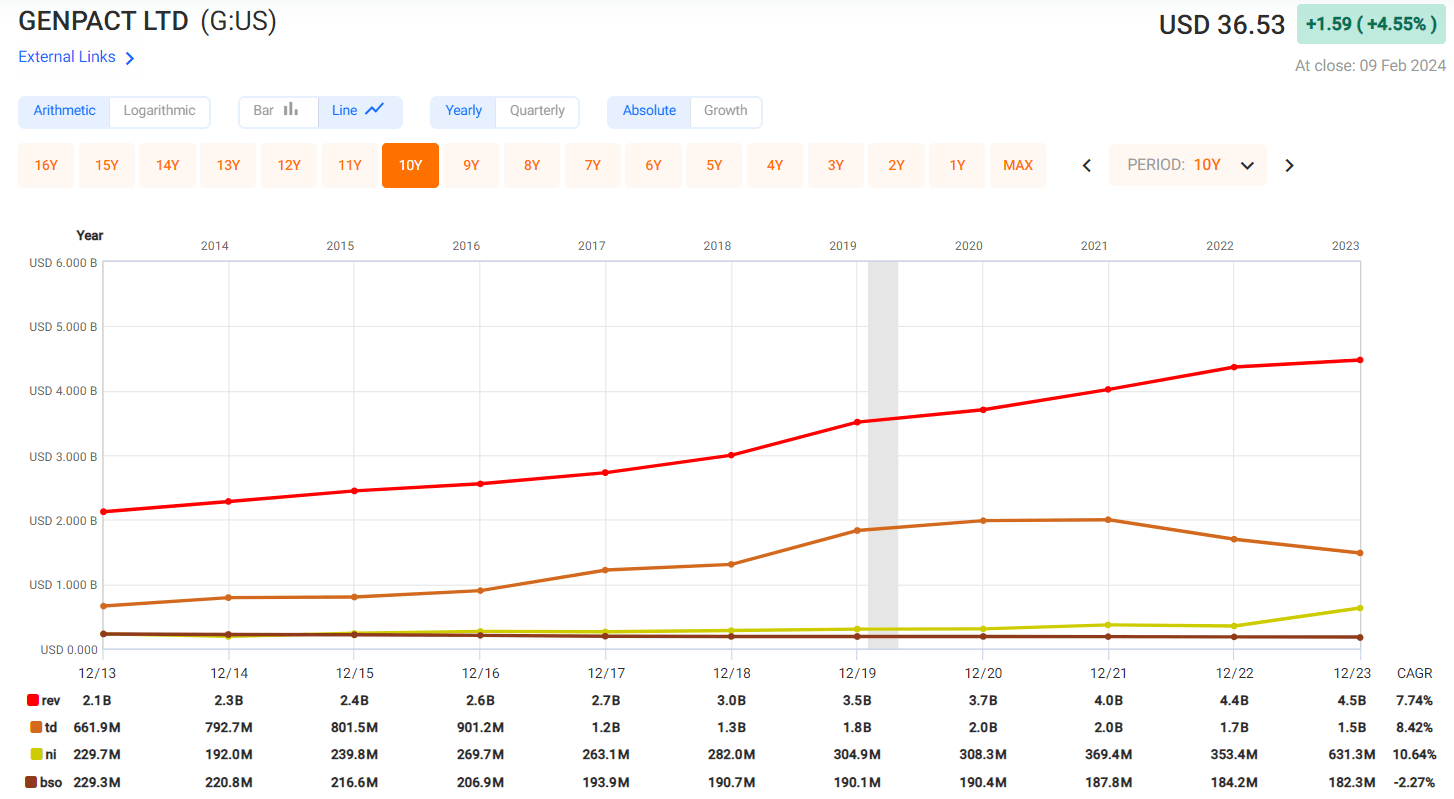

Firstly, this business can generate a growing and very predictable revenue and earnings. For the past ten years, revenue has grown at a CAGR of 7.74% while net income has grown 10.64%.

FAST Graphs

This is a healthy and growing business and is certainly not a value trap.

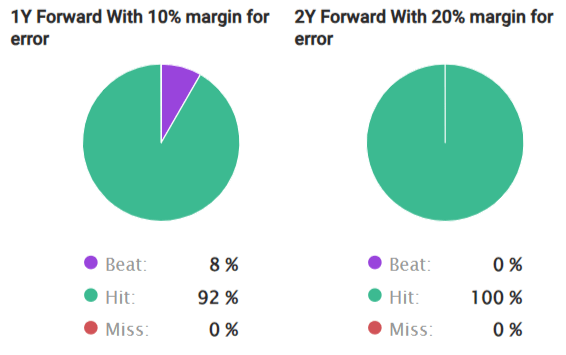

During these 10 years, management led by the outgoing CEO Tiger Tyagarajan has always provided accurate guidance, helping FactSet analysts achieve perfect estimates of Genpact's revenue and earnings.

FactSet Analysts 1-year and 2-year Revenue Estimates for G FactSet Analysts 1-year and 2-year Adjusted Operating Earnings Estimates for G

Growing, predictable revenue and net income. What is not to like?

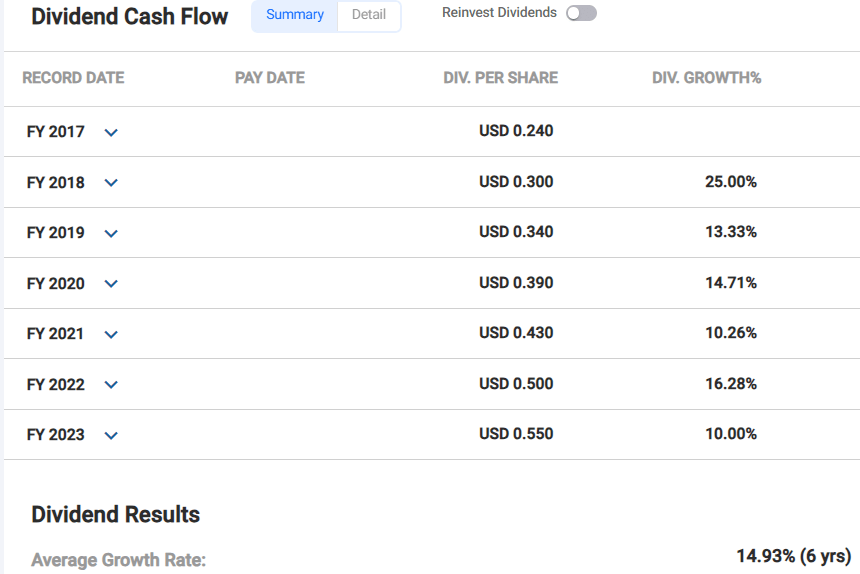

Secondly, I like that management has shown that it is friendly towards shareholders. Since it started paying a dividend in 2017, G has been growing the dividends at double-digit rates annually, even through the COVID-19 pandemic, averaging an annual average growth rate of 14.93%.

FAST Graphs G's Dividend Growth Rate

In addition, G has been buying back shares over the past decade to boost shareholders' returns. In 2023 alone, G has returned $100 million to shareholders in the form of dividends and $325 million in the form of share buybacks.

Regarding dividends and buybacks, CFO Mike Weiner gave this assurance in the Q4 2023 earnings call,

... we remain committed to returning capital to shareholders through our regular cadence of buyback and quarterly dividend payments. We currently anticipate approximately 30% cash flow from operations for share repurchases during 2024. Additionally, our Board of directors approved 11% increase in our regular dividend to $0.153 per quarter or $0.61 on an annual basis. Our dividends increased at a compounded growth rate of approximately 15% since we began paying dividends in the first quarter of 2017. With this expected activity, we plan to distribute 50% of our operating cash flow to shareholders during the year.

FactSet analysts expect G to generate $2.94 of operating cash flow in 2024. There are 179 million shares outstanding which works out to $526 million of expected operating cash flow in 2024. 50% of that is $263 million.

These are good news for shareholders. What is not to like?

Thirdly, outgoing CEO Tiger has been future-proofing Genpact's business through significant investments in the Data-Tech-AI segment, which also grew a lot faster than the Digital Operations segment from 2020 to 2022. He has also been building AI partnerships with Google Cloud (GOOGL) to accelerate AI adoption for the enterprise, and with Microsoft (MSFT) "to leverage Microsoft Azure OpenAI Service technology to enhance the speed-to-market of leading-edge solutions that help companies use data and AI's power to drive actionable business insights".

To date, Genpact already has several AI/ML solutions addressing different needs, from using its Responsible AI framework "to create and implement fair and ethical AI and ML solutions" to "optimizing business performance and commercializing data opportunities" through its Advanced analytics CoE managed services. These efforts are recognized and Genpact just earned the highest ranking in the inaugural 2023 HFS Generative Enterprise Services Horizon report. According to the press release,

This is the industry's first competitive assessment of professional services firms with enterprise clients adopting and experimenting with generative AI technologies. The evaluation reviewed the capabilities of 35 providers across categories such as value proposition, execution and innovation, go-to-market strategy, customer feedback, and alignment with HFS Horizons' proprietary criteria. Genpact is praised for using emerging technology to the highest level of innovation, uncovering key insights, spotting trends earlier in business cycles, and developing new solutions based on embedding generative AI.

In his prepared remarks, incoming CEO BK Kaira is going to continue in his predecessor's footsteps. He stated that one of his key actions as CEO will be to strengthen G's partner relationships to deliver holistic solutions, to further leverage G's domain and industry expertise, access to Data and CXO relationships to deliver improved performance for its clients and improve revenue growth and profitability for Genpact.

Genpact is an AI-first company in an era increasingly defined and molded by the ever-evolving capabilities and use cases of AI and LLMs. What is not to like?

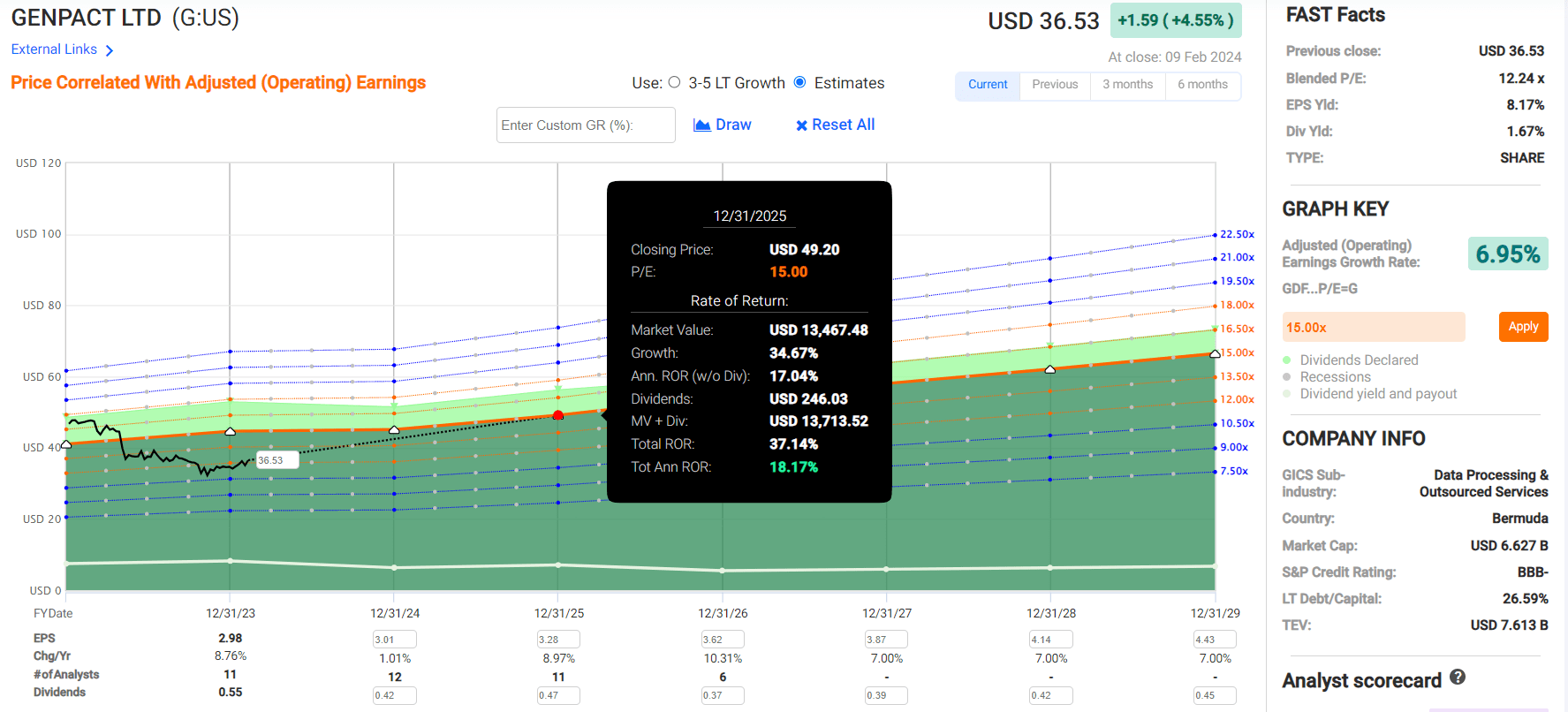

Fourthly, I believe that the shares are undervalued at the moment. Genpact's shares have the potential for a 34% gain if the shares start to trade towards a more normal valuation range of between a blended P/E of 14 to 18; its current blended P/E is 12.09.

FAST Graphs

For context, the only periods since 2007 when Genpact traded around or under a blended P/E of 12 were:

As can be seen above, Genpact does not usually trade around a blended P/E of 12 so its current valuation is considered to be low. Besides, management expects year-over-year revenue to be higher in the second half of the year compared to the first half, which is in line with its historical patterns. This increases the possibility of G reporting revenue and earnings in Q4 2024 or Q1 2025 that meet or beat analysts' expectations, thus increasing its attractiveness to potential investors.

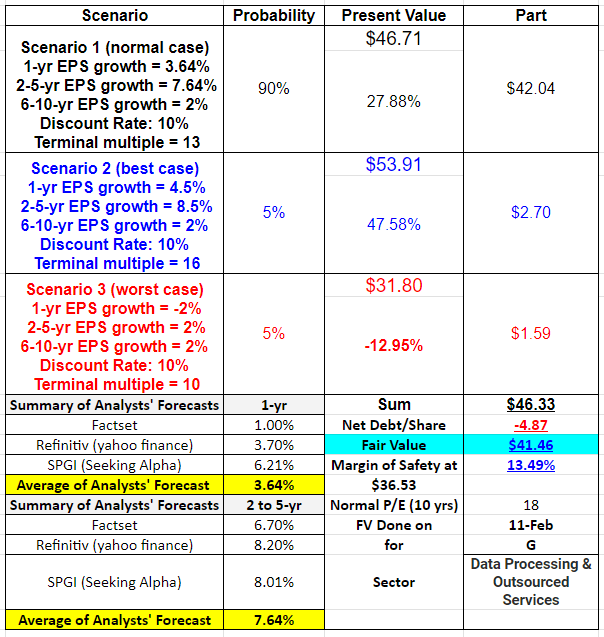

My fair value estimate of G's shares is $41.46, offering investors a 13.49% margin of safety.

Author's Fair Value Estimate

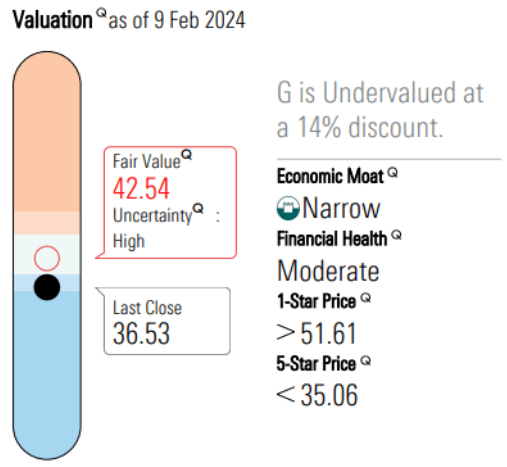

Morningstar analyst agrees, giving narrow moat Genpact a fair value of $42.54.

Morningstar

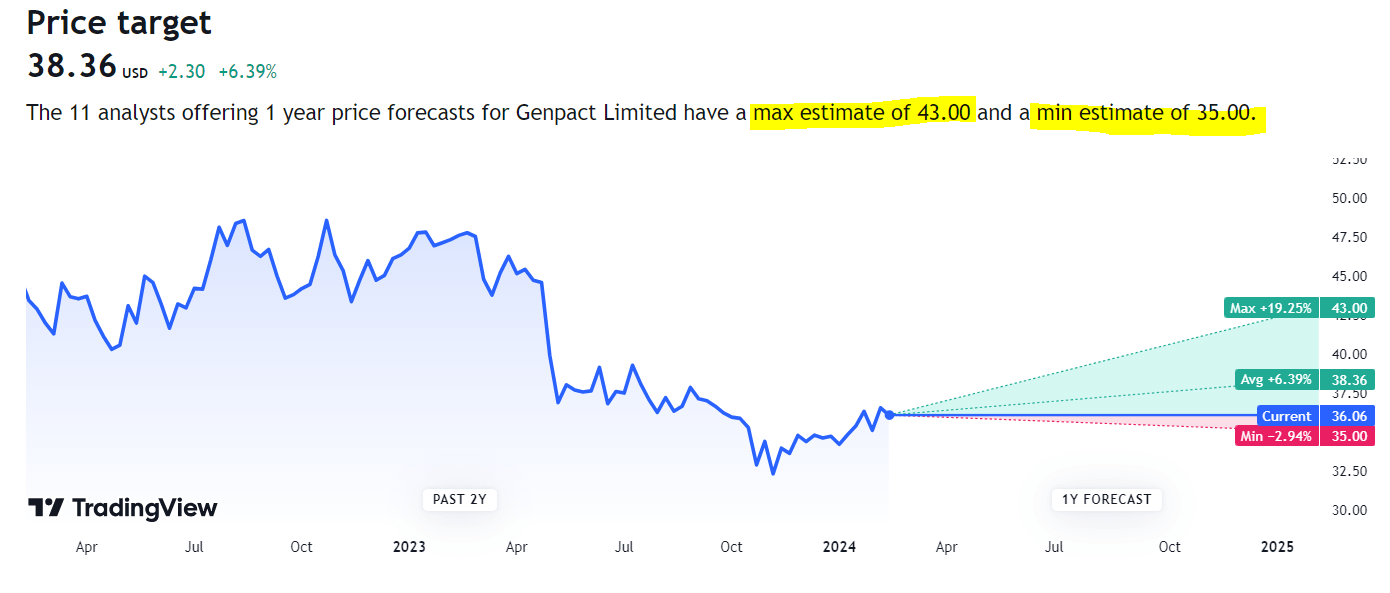

According to TradingView, the 11 analysts that follow Genpact have a consensus estimate of $38.36, ranging from a low of $35 to a high of $43.

TradingView

So, Genpact is not just cheap now, it is profitable, and it is a narrow-moat company (according to Morningstar). What is not to like?

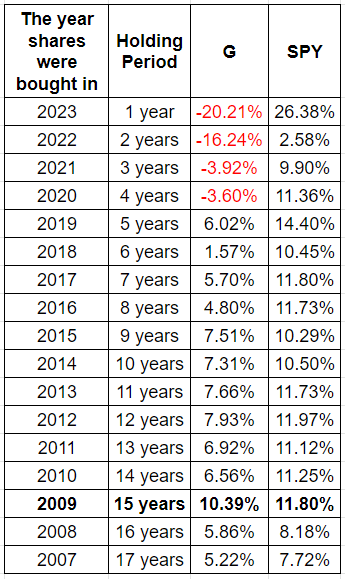

Firstly, Genpact's performance has never once bested the S&P 500 (SPY). I tracked hypothetical buy-and-hold periods from 2007 to 2023 for G and SPY and the only time G's performance came close to SPY was if its shares were purchased in 2009 during the Great Financial Crisis and held for 15 years.

Author's table with data from FAST Graphs

As a stock picker, the whole point of being one is to outperform the market and if the G has never outperformed the market, why consider it?

I do not like this.

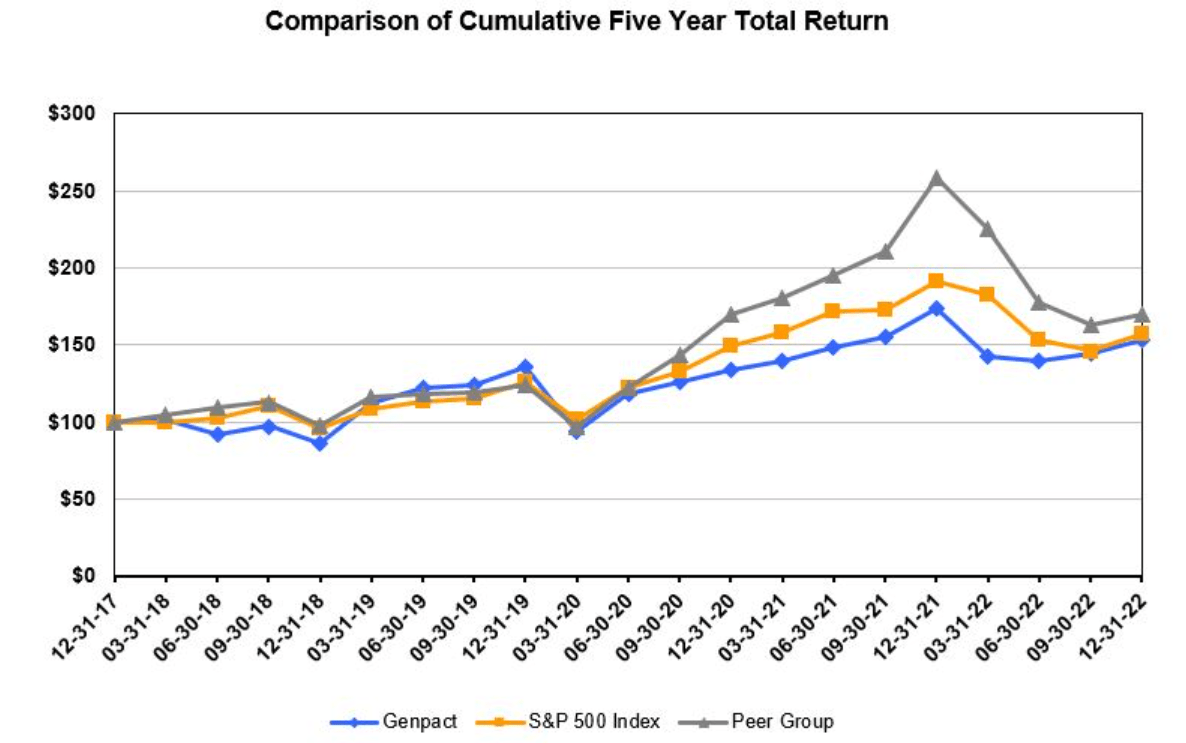

Secondly, G underperforms its peer group. The following chart from the company's 2022 10K says it all too clearly.

G's comparative underperformance from 2017 to 2022

An investment in Genpact's shares since 2017 when the company paid its first dividend would have underperformed both the S&P 500 as well as its selected peer group: Accenture (ACN), Cognizant Technology Solutions Corp (CTSH), ExlService Holdings (EXLS), Infosys Limited (INFY), Wipro Limited (WIT), and WNS (WNS).

I do not like this.

Thirdly, revenue growth slowed from 2022 to 2023. Let's dive into each of the three business verticals a little bit more. Typically, this company files its SEC filings on the 1st of March. Although the company just reported Q4 2023 earnings a few days ago, it has not filed its 2023 10K. Hence, some of the figures used below to compare the growth in these three business segments come only from the 2020 to 2022 10Ks. I will update the table after the 2023 10K is available.

Author's table, data drawn from 2020 to 2022 10Ks

Are these three segments growing revenue? The picture is a little mixed.

Although the revenue for Data-Tech-AI and Digital Operations grew from 2020 to 2022, especially in the smaller revenue contributor Data-Tech-AI, growing 21.45% from 2020 to 2021, and another 17.97% from 2021 to 2022, the combined revenue growth for both Data-Tech-AI and Digital Operations has slowed to just 0.83% from 2022 to 2023.

I do not like this.

Fourthly, the company's guidance for 2024 was less than exciting.

During the Q4 2023 earnings call, CFO Mark Weiner said,

Full year gross margin of approximately 35%, full year adjusted income from operation margin of approximately 17% and full year adjusted EPS in the range of $3 to $3.03. This is -- this represents year-over-year growth of 1% to 2%...

In other words, "growth" is still expected but only in the super low single-digit range.

I do not like this.

Incoming President and CEO BK Kalra is not new to Genpact. He was part of the pioneer team that founded Genpact. Before taking on the CEO role, he had led several verticals in the company. He once led the Global Head of Financial Services, Consumers, and Healthcare businesses at Genpact.

However, leadership change always increases uncertainties.

According to the 2022 10K,

In 2022, more than 70% of our revenues were derived from clients based in North America and more than 15% of our revenues were derived from clients based in Europe. Additionally, more than 25% of our revenues were derived from clients in the financial services and insurance industries.

In an earlier segment, I stated that the group of clients that made up 25% of Genpact's revenue include retail, investment and commercial banks, mortgage lenders, equipment and lease financing providers, fintech companies, payment providers, wealth and asset management firms, broker/dealers, exchanges, auto finance providers, clearing and settlement organizations, renewable energy lenders and other financial services companies.

There are several changes in Genpact's operating landscape that investors should be aware of.

The first will be the changes coming to Basel III. If the changes lead to imposing tougher restrictions on banks, that could cause much higher costs for banks that rely heavily on non-interest fee income, such as credit card and investment banking fees, thus reducing their net income.

Secondly, banks derive much of their net interest income from credit card loans and housing loans. According to this report from CNBC, "credit card delinquencies surged more than 50% in 2023 as total consumer debt swelled to $17.5 trillion." Many experts are also concerned about a housing-bubble. According to the author, "experts say that the combination of high mortgage rates, inflated home values and scarce inventory suggest that 2024 could remain a challenging year for the housing market". If the high property prices and low inventory keep buyers away, fewer buyers mean fewer people taking up home loans, albeit at a higher mortgage rate.

In short, if banks' earnings are reduced, they may have to cut back on the services they are getting from Genpact.

In the 2022 10K (page 23), the following was stated:

... in recent years, as a result of a number of factors, including changing client preferences, an increase in Data-Tech-AI services and economic pressures that can cause delays or reductions in client purchasing decisions, the percentage of our revenues from consulting and other short-cycle engagements has increased. The increased share of our revenues derived from these engagements makes business forecasting more complex given that they are for services that are more discretionary and non-recurring than our traditional services. Our contracts for consulting and other short-cycle engagements typically permit our clients to terminate the agreement with less notice than is required under our longer-term contracts for our Digital Operations services and without paying termination fees.

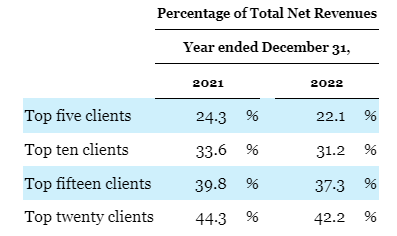

Genpact did not name its clients. Based on what was reported in the 2022 10K, the top 20 clients make up 42.2% of its 2022 revenue.

Genpact 2022 10K

We also know that 25% of its clients are from the financial service and insurance sector, and if the banks make up 15% to 25% of that number, which translates to 6.3% to 10.5% of G's 2022 revenue, and a portion may be negatively hit in a worst-case scenario.

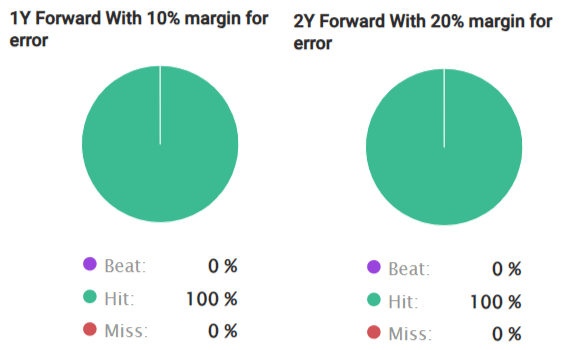

There are many things to like about Genpact, especially with its valuation as low as it has been for a long time. Although revenue growth in 2024 is expected to be in the low single-digits, that is also expected to pick up in 2025 and 2026 at almost 10% each year. With FactSet analysts' 100% accuracy rate with its 2-year forecast of G's revenue and adjusted operating earnings (within a 20% margin of error), I will say this is a good time to start accumulating some shares in a profitable investment grade (BBB-) company, led by an "AI-first", shareholder-friendly management that is growing dividends at double-digit rates every year since 2017 and has been consistently buying back shares since 2013. The yield is nothing to shout about but it means G has plenty of room to keep growing the dividends; the yield-on-cost a few years from now will be significant.

For investors who are comfortable with a 13% margin of safety, G could be a BUY.

Genpact is not a Strong Buy for me though as I would prefer the margin of safety to exceed 20% (i.e., under $29.22) before I start buying heavily. After all, cheap can get cheaper; I am concerned about G's heavy focus on the US market and the financial service sector for its revenue, and am wary of the effects of Basel III, credit delinquency, and the state of the housing market on the fortunes of the banking sector. Another point that held me back from a Strong Buy will be G's chronic underperformance compared to SPY. Of course, with the fast-growing Magnificent 7 making up 29% of S&P 500's market capitalization, it is natural for SPY to outperform a slow and steady performer like G.

I intend to start buying some shares from 13 February 2024 and will add slowly.