pingingz

pingingz

My recommendation for Frontier Communications Parent (NASDAQ:FYBR) is a buy rating, as I expect EBITDA growth to turn positive over the coming years. My previous concern regarding ARPU growth should not be an issue moving forward, as FYBR sees increasing 5G and value-added service adoption. Lastly, because of the change in EBTIDA growth trajectory, I expect FYBR to trade at a premium to its historical valuation. Note that I previously rated a hold rating for FYBR on 22 November 2023 as unit economics (ARPU) remain soft, and its legacy product revenue should continue to drag down overall business performance. While the stock rallied, my concerns on the ARPU softness was right as 4Q23 results showed that ARPU remained soft.

FYBR 4Q23 results were released on 23 February 2024, and I thought they were alright. The business reported revenue of ~$1.43 billion, down ~1% y/y, but EBITDA was up 4% to $549. On a FY23 basis, both revenue and adj EBITDA ($5.751 billion and adj EBITDA of $2.217 billion) were somewhat in line with my FY23 estimates of $5.575 billion and $2.126 billion. My key takeaways from FY23 performance is that the worst might be over (when compared to the outlook for FY24 and beyond). Hence, I think the focus should not be on FY23, but rather on the positive outlook that has made me turn bullish on the stock.

In terms of fiber footprint, FYBR expanded its footprint by another 333k locations, sustaining the previous quarter's record of >300 locations per quarter. FYBR also saw net additions of 84,000 fiber subscribers. Importantly, FYBR disclosed penetration rates for the 4Q21 cohort at 25%, which is tracking well in line with the 24-month penetration guide of 25–30%, suggesting that underlying demand is going as expected and FYBR is on point on execution. The same demand profile is seen in the 4Q22 cohort of 381,000 passings, which is tracking well against expectation (18% penetration so far vs. the 12-month expected penetration rate of 15 to 20%). Understanding and tracking these data is crucial because, based on this trendline, I expect FYBR to see fiber net add acceleration as it continues to scale because the 4Q20 cohort (86,000 homes) has reached 35% penetration, a strong precedent for the 4Q21/22 cohort. In 2024, management expects fiber net adds to accelerate throughout the year, despite seasonal headwinds in 2Q. On fiber-added expansion, while it is expected to stay at the same run rate, I do think that it was the right strategic decision by management to maintain its pace of 1.3 million as it would not risk a situation of oversupply.

One of the key concerns I had previously was the weak ARPU unit economics. In 4Q23, FYBR continued to report mixed ARPU trends, with Fiber Consumer Broadband ARPU of $64.16 (down 0.5% sequentially but up 4.8% y/y), but Copper Consumer Broadband ARPU was up 11.3% to $54.22. While 4Q23 was mixed, I shifted my attention to FY24, where fiber ARPU is expected to grow by 3-4%. I think this goal is within reach because new fiber connections increase ARPU, with about 60% of new connections opting for speeds of 1 Gbps or higher (higher ARPU) and about 45% of subscribers buying value-added services. On the latter, I expect it to continue contributing to ARPU growth in 2024, as they were only unbundled in mid-2023, and the adoption rate so far is very encouraging.

As a result, nearly 60% of our new customers are taking speeds of 1-gig or faster, and roughly 45% of customers purchased at least one value-added service. Consumer fiber broadband churn also improved to 1.20% in the quarter. From: 4Q2023 earnings call

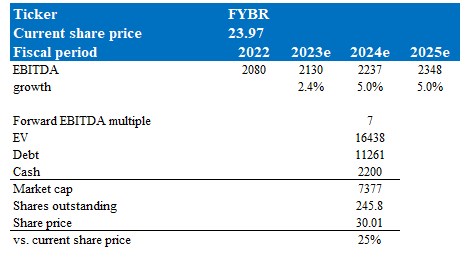

This ARPU growth is a key part of the EBITDA growth equation. If we look back at FYBR's historical performance over the past few years, it has always been negative. But from FY24 onwards, I expect the situation to turnaround. Management is now expecting EBITDA acceleration in the coming years, which I think has a very high chance of happening, as follows:

In terms of guidance, management is expecting 2024 EBITDA growth of at least 5%, with y/y margin expansion expected in each quarter of 2024.

Author's valuation model

According to my model, FYBR is valued at $30 in FY24, representing a 25% increase. This target price is based on my EBITDA growth forecast of 5% over the next 2 years, in line with management guidance. I believe this 5% is possible because ARPU is already expected to grow at 3 to 4%, and combining this with the increased penetration in existing cohorts, revenue should grow mid-single-digits easily. Also, since an increase in penetration carries a high incremental margin, EBITDA should grow faster than the top line. Hence, I note here that this 5% growth expectation is at the minimum, and any upside surprise will add on to the upside.

The key variable here is the forward EBITDA multiple. I believe FYBR has entered a new valuation paradigm as it starts to show positive EBITDA growth. Hence, unlike its past, which traded within a range of 5.6x to 6.4x, I believe it should trade higher. The market has also shown its willingness to rerate FYBR, as seen from the recent increase in valuation to 6.6x forward EBITDA. If FYBR really shows EBITDA growth, I think it can go higher, and I am assuming FYBR to trade at 7x (just modestly above the recent high). If we compare FYBR to T-Mobile (TMUS), I believe FYBR is trading at a discount because of its slower growth and lower margins. TMUS is expected to grow at mid-single-digits for next year and has a higher EBITDA margin (41% vs 33%). Looking ahead, as FYBR closes this gap, its valuation should move towards TMUS level as well (currently 8.5x forward EBITDA).

The risk/bear case is that although the 4Q20 cohort is a strong precedent for the 4Q21/22 cohort for growing penetration, it is not to say that 4Q21/22 will follow 4Q20’s trend. The underlying consumer base might not sign up as expected, which will be detrimental for FYBR growth and margins.

I'm upgrading my recommendation for FYBR to buy due to its improving financial outlook and potential for positive EBITDA growth. FYBR's expanding fiber footprint and increasing adoption of higher-margin services like 1 Gbps speeds and value-added services should drive ARPU and EBITDA growth. In turn, this makes management guidance for at least 5% EBITDA growth in 2024 is achievable, marking a turnaround from past negative trends. As FYBR demonstrates its ability to generate positive EBITDA, it is likely to be valued at a higher multiple than its historical average.