champpixs

champpixs

UP Fintech Holding Limited (NASDAQ:TIGR) has been caught in a long-term consolidation formation since the end of 2021, predominantly trading between $3 and $5. The company's financials have lately shown positive momentum, but China's economic problems and regulatory risks are weighing heavily on the performance of the entire market and the online brokerage sector in particular. However, TIGR's upcoming results might represent an opportunity for the shares to close in on the upper end of its trading range again. The opportunity for the company in its markets is promising, and continuous product innovation keeps generating sustained customer interest. Therefore, I believe the stock will be able to break out sooner or later and subsequently unleash its upside potential.

UP Fintech operates an online brokerage platform in Asia, with most of its existing and new customers in Singapore. Tiger Broker is also the city state's leading online broker in terms of trading volume. Additionally, Tiger Broker is available in the US, Australia and New Zealand, Hong Kong, and China. However, due to regulatory intervention, the company can effectively no longer accept new customers on the Chinese mainland since the end of 2022. Detailed information on the geographic distribution of TIGR's revenues is unfortunately not being published.

The company offers its customers comprehensive brokerage and value-added services, including trade order placement and execution, margin financing, IPO subscription, ESOP management, investor education, community discussion, and customer support. Altogether, it generates revenue predominantly through brokerage commissions and interest income (mostly from securities lending and margin financing). Lately, the proportion of these two key revenue contributors shifted due to the rising interest rate environment (see the table below), leading to reduced growth in trading activity but increased interest proceeds.

| Revenue Type (Q3 2023) | USD million | YoY change |

| Commissions | $23.2 | 5.4% |

| Financing Service Fees | $3.3 | 54.2% |

| Interest Income | $38.3 | 54.4% |

| Other | $5.4 | 35.1% |

| Total | $70.1 | 26.6% |

TIGR's further business is growing but accounts for a much smaller share of its revenues. The CEO commented the following on this:

Our 2B business continues to perform well. In investment banking, we underwrote four U.S. and Hong Kong IPOs in the third quarter, including Earlyworks and Keep. In our ESOP business, we added 27 new clients in the third quarter, bringing the total number of ESOP clients served to 505 for the end of the third quarter of 2023, increased by 29% year-over-year. (Tianhua Wu, CEO and Chairman, at the Q3 earnings call)

By Q3 2023, Singapore was still the largest growth driver for the company, accounting for 55% of the newly funded accounts, while accounts in Hong Kong, Australia and New Zealand, and the United States added about 15% share each. Moreover, TIGR keeps innovating and adding new features to its platform: in Q3 2023, the company introduced Trading Sparks, a social feature where users can follow best-performing traders and leverage their ideas for investment opportunities. In Q2 2023, UP Fintech additionally released an AI investment assistant called TigerGPT.

As I will show in more detail, UP Fintech trades at a valuation lower than its peers and much lower than US peers, which is predominantly due to the fact that it is a Chinese company. Aside from the general risk of investments in Chinese companies, TIGR's discount can in my view additionally be attributed to the current economic situation in China and a regulation-driven sector-specific risk of Chinese fintechs.

Even though UP Fintech diversified (not entirely by its own choice) its revenues from mainland China, it is still a Chinese company and valued according to country-specific risks. Subsequently, the lately worsening economic situation in China further depreciated the entire Chinese stock market in the past months and affected TIGR as well.

China has lately experienced decade-low growth rates in the aftermath of the COVID-pandemic. There are multiple reasons for this, but most notably:

Chinese investments will probably keep being influenced by these developments. Any deterioration of these catalysts could thus further drag TIGR's share price down. On the other hand, improvements might also induce some positive momentum. Nevertheless, volatility and uncertainty surrounding Chinese stocks can be expected to stay elevated for the time being.

Chinese online brokers are moreover experiencing pressure from the country's regulators. In 2021, China initiated a wave of regulatory interventions regarding new online business models, which went as far as banning for profit operations in the online education sector. Online brokerage also came under scrutiny at that time.

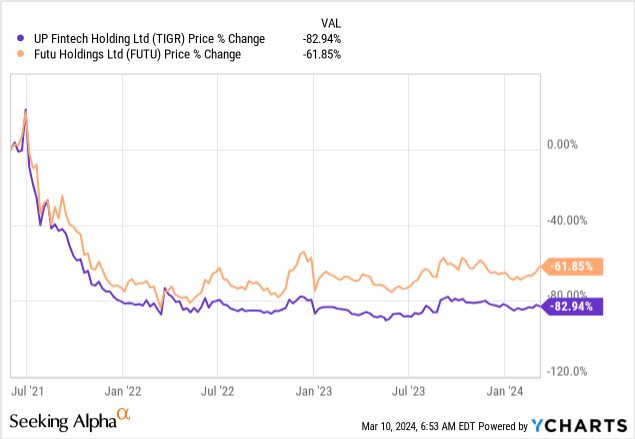

Regulators noted that they were giving Chinese customers the means to take investments outside of the country ("illegal cross-border trading"), leading to significant uncertainty and a contraction of TIGR's (and similarly Futu's (FUTU)) share price in 2021. At the end of 2022, the CRSC (the regulatory body) announced that both companies had conducted unlawful securities business and would be banned from opening new accounts from Chinese mainland investors, which led to another sharp drop in share prices (see below).

You can find a more detailed account of this topic in this nice article from Bamboo Works, a fellow SA author who discussed these events in depth. By now, TIGR seems to have calmed relations with the CSRC, yet the ban remains in place and will probably not be lifted in the near future:

After the CSRC announcement on December 30 [2022], Tiger Brokers made a prompt response and a comprehensive effort to comply with the regulatory requirements set forth by the CSRC. Subsequently, the Beijing Securities Regulatory Bureau conducted an onsite inspection four weeks before the Chinese New Year. [...] We have [...] received clear guidance on certain special scenarios for PRC passport holders to open new accounts with us, for example, allowing PRC passport holders who work or live overseas to open accounts [...]. Recently in mid-July, we submitted the final remediation report [...]. Subsequently in mid-July, the regulatory authorities conducted an onsite acceptance inspection based on our remediation report. (Tianhua Wu, Q2 2023 earnings call)

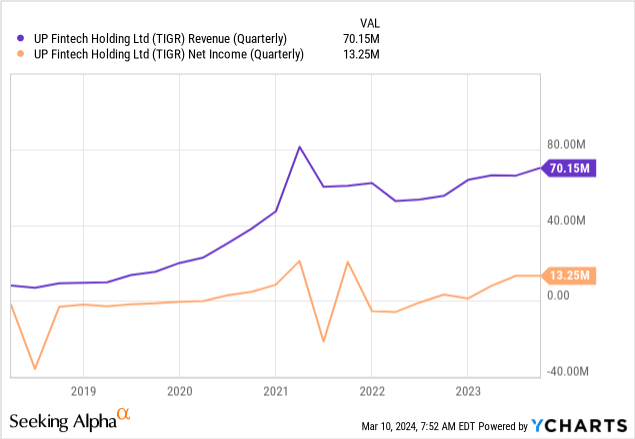

Looking at the bigger picture, it is obvious that TIGR's steep revenue growth until early 2021 suffered meaningfully after this regulatory action and the restrictive interest rate environment. However, the business has stabilized since and revenues seem to be heading in the right direction. The company additionally manages to generate profits again.

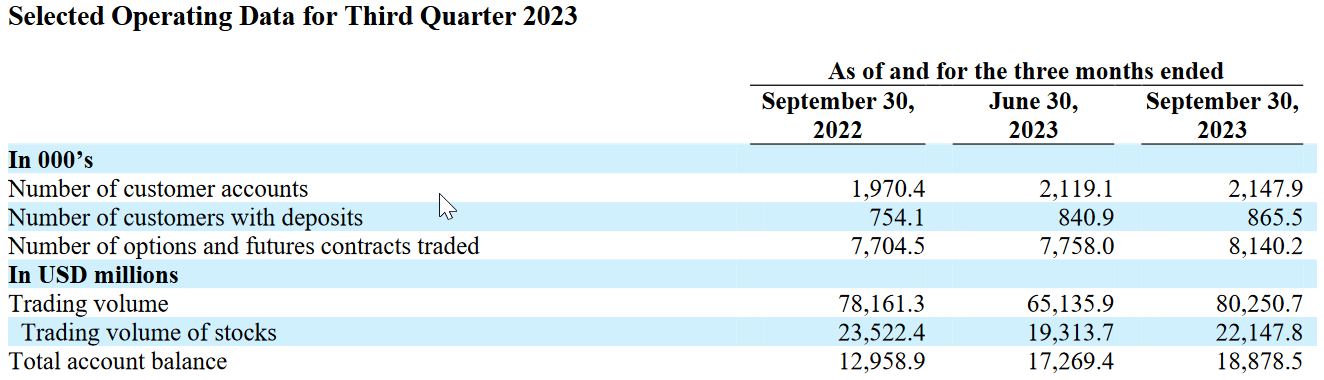

The most recent data on customer accounts (with deposits) growth and trading volume also show that UP Fintech managed to stabilize its business and surpass year-on-year (YoY) comparables. However, it has not yet reached the levels from Q3 2021 when total account balance was $20,551.9 million and trading volume stood at $92,574.1 million (the number of deposited accounts is now higher, though).

Operating development in Q3 2023 (TIGR Q3 2023 Quarterly Result)

UP Fintech is continuously growing at more than 20% since Q1 2023 while generating profits again. At the same time, its international business is showing strong customer adoption, the company keeps adding new features to its platform, and the regular fallout seems to be digested for now. The management is also looking to the future and expects to keep growing and generating operating leverage:

Given most of our costs are relatively fixed and tied to market activity, we believe that if we can better penetrate in Hong Kong, Australia and New Zealand markets, or if there is overall improvement in the market backdrop, we can enjoy more operating leverage, which leads to more stable profit margins. (Tianhua Wu, Q2 2023 earnings call)

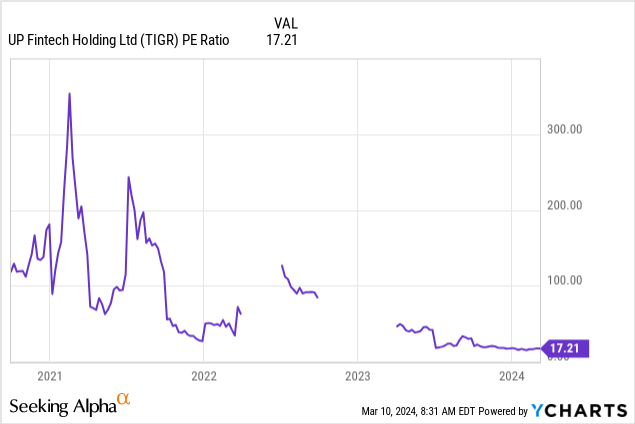

UP Fintech is a more stable, growing and profitable business now. Additionally, it has managed to keep its balance sheet position fairly stable within the last year. Still, the company is trading at a historically low valuation in terms of price-to-earnings. While a lot of this is due to the situation in China, the described issues are less critical today since most restrictions in China have already materialized and the impact of a further deterioration of its domestic economy is meaningfully reduced.

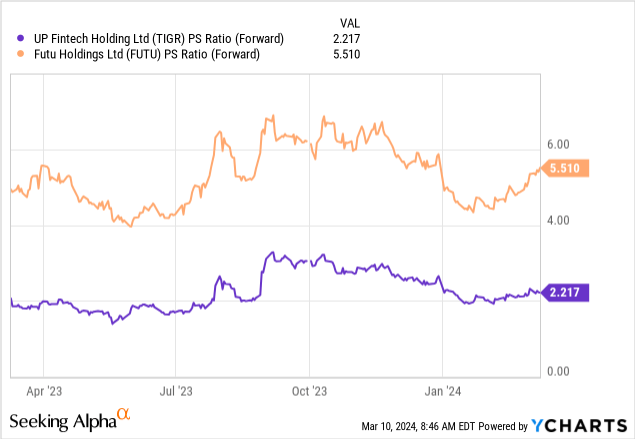

In a relative view, UP Fintech is valued more cheaply than Futu Holdings on a price-to-sales basis. As FUTU however has a better profitability profile, the respective PE ratios are similar at 17 (TIGR) and 14 (FUTU). Still, while the relative valuations of both stocks moved similarly in the past, FUTU seems to be already adapting to returning growth by expanding its valuation recently. TIGR could experience a similar development as soon as investors see more proof that recent growth can actually be sustained and the promises of increasing operating leverage materialize.

Like most small-cap growth companies, TIGR is not covered by many Wall Street analysts, and reliable estimates about future cash flows are lacking. Nevertheless, it does not seem expensive from a relative and historical perspective - particularly if the issues described above fade. Wall Street analysts assign a Buy rating to the stock with an average price target of $6, which is 44% above the current share price. I also believe that TIGR can move higher if the next earnings underline the positive sentiment. Once the share price breaks above $5, it could appreciate further to $6-$7 where the stock exhibits relevant technical markers. In the long run, the stock could then return to double-digit notations.

While not delivering the explosive growth rates it experienced until early 2021 anymore, TIGR keeps announcing stable and profitable revenue growth of more than 20%. The management expects this development to continue and aims to further expand to international markets while delivering over proportionally to the bottom line due to increasing operating leverage. In my view, the worst of the regulatory risk has already materialized, and China recently pledged to be more careful with such interventions in the future. While there is still risk from a possibly developing financial crisis in the country, I believe the communist party would take unseen measures to mitigate these risks (China can enact measures that other countries cannot).

In my view, UP Fintech is a Buy with about 45-70% upside potential in the short to medium term. Due to the company's risk profile, I recommend only attributing a very small share of a portfolio to TIGR. Yet, in my view, it represents an interesting geographical diversification for US and European investors at an attractive valuation.