Galeanu Mihai

Galeanu Mihai

Unfortunately, February couldn't continue the streak that was started in January. After a decent start, the S&P500 was down 2.6% in February, bringing year-to-date returns to 3.4%. My portfolio was also unable to extend its profits as some of my best-performing stocks are back at the price they ended 2022. This does not come as a surprise as the economic outlook is still bleak and I don't see this changing in the coming months. As I am not a market timer but an investor I continue to add money to my portfolio and this month I added €800 to my portfolio. In total, I added capital to 4 stocks, 1 sale, and 1 sale & transfer.

For the people that have not read my previous articles: I am a 25-year-old investor from the Netherlands who is trying to start early so that I will have the option to retire early or at least earlier (the current retirement age is 67 in NL and is trending upwards). If you are interested in previous updates on my portfolio, you can find them here:

My Portfolio November Update: 5 Buys, 1 Sell

My Portfolio December And End Of Year Update: Outperformance Despite FX Headwinds

February wasn't a great month in terms of stock returns but most indices are still up YTD. The decline can be at least partially attributed to the elevated levels of inflation, which was 6.4% in January. As a result of the decline, some stocks have entered my buy territory again and I hope that I will be able to add more money to some of my smaller positions. I am also interested in potentially adding distressed bonds to this portfolio, but I will have to do some more research in that area to fully comprehend what to look for and how it can be added to my portfolio.

In terms of my other portfolios, the results are mixed. The portfolio that I run together with some of my peers for the student competition has been underperforming this year and we are in the middle of the pack. Given the limited timeframe, we have moved from a low beta strategy to a slightly more aggressive strategy and are monitoring our results. For now, I don't expect us to make any major changes, but this might change closer to the end of the competition.

My concentrated portfolio to which I have been transferring some stocks has been performing very well and is up over 12% YTD. I currently hold 6 stocks in that portfolio of which TISG, CoreCard, and NeoGames have been transferred from this portfolio. The other 3 stocks that I own are F-star Therapeutics (FSTX) (M&A), Activision Blizzard (ATVI) (M&A), and Civitanavi (European small cap). I add approximately €300 to this portfolio every month and will mostly add to the holdings I currently have.

Core | Value | Small-cap growth | |

Buy |

|

|

|

Reconsider |

|

|

|

Sell |

|

|

|

Last month I mentioned that I am also running a smaller more concentrated portfolio. In this portfolio, I mainly hold small-cap stocks as well as merger arbitrage. These are stocks that do not necessarily fit the strategy of my dividend portfolio and I wanted to see which one will outperform over a few years. As a result of the concentration, I have decided to sell one of the two stocks. NeoGames is larger than Bragg, has a more diversified offering, and is, in my opinion, better positioned to profit from the ongoing legalization of online gambling. As a result, Bragg was sold and NeoGames was transferred to my other portfolio.

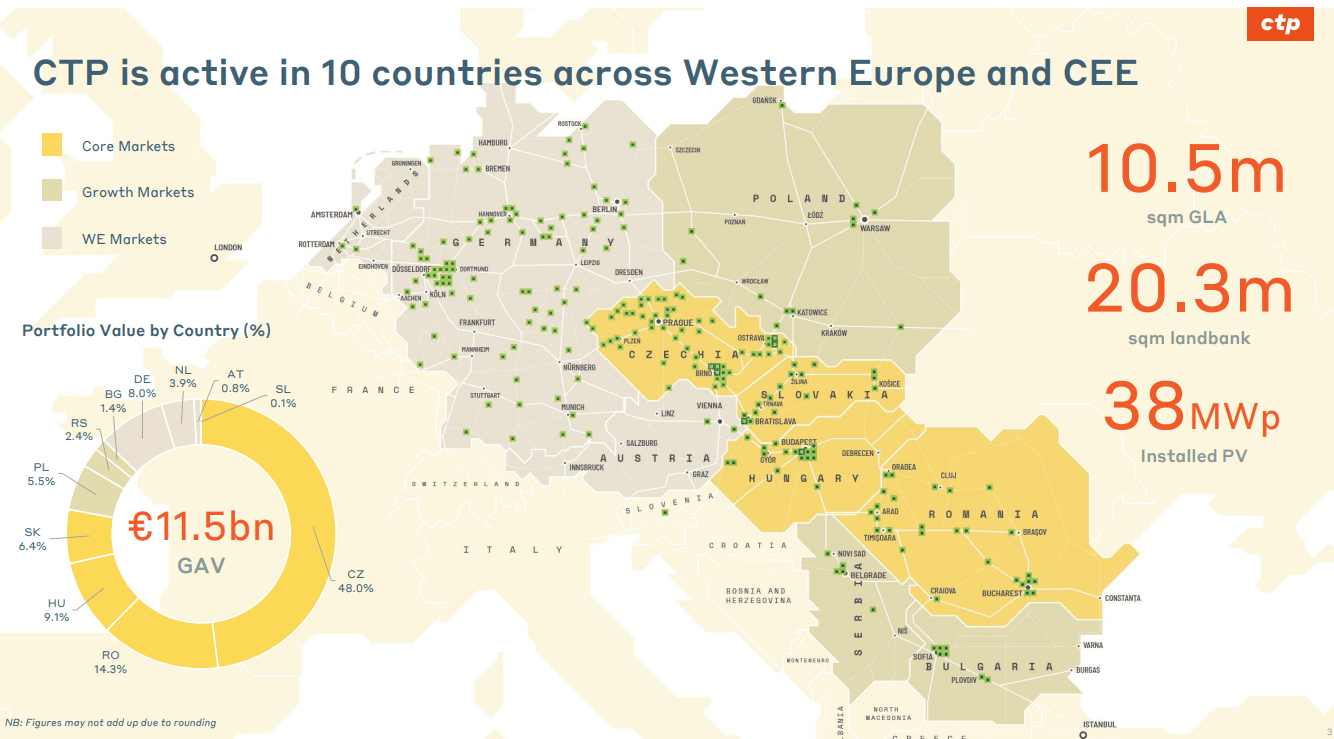

Last month I mentioned that I was interested in adding more capital to my position in CTP N.V (OTCPK:CTPVF). The company is active in the real estate sector and owns and develops industrial warehouses throughout Europe. The thing that sets the company apart is that it owns the majority of its real estate in Eastern Europe and is the largest listed logistics property owner and developer of the region. Management has a lot of experience in the area with CEO Vos being active in the region for over 20 years. Last year the company acquired Deutsche Industrie REIT, and three properties in the Netherlands. This connects the company's warehouses at the Black Sea all the way to the North Sea. This gives it significant economies of scale and improves its bargaining power with tenants. The valuation of the company is decent at a P/FFO of approximately 19.5x. My own estimated price target is €15.96 which makes it undervalued by approximately 20% at the moment of writing.

Asset overview (CTPNV)

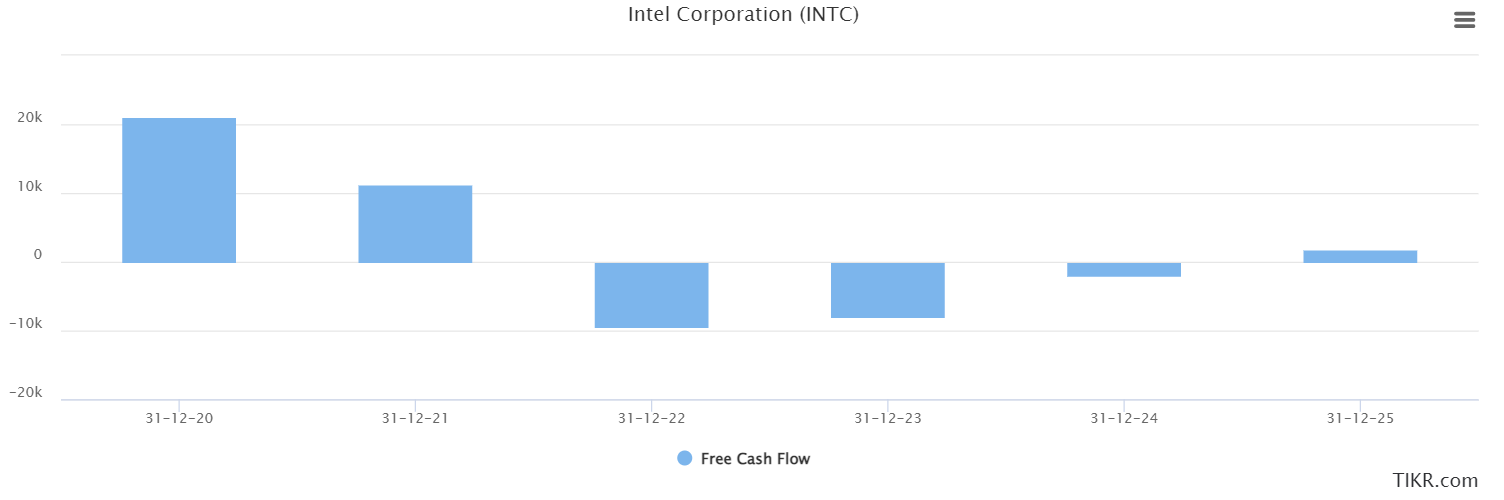

After owning Intel for a couple of years I decided that I had enough of the empty promises. The company has been investing significant amounts but does not expect to catch up with the competition in the coming years. After also cutting the dividend in half, which was an understandable move given the capital constraints, I decided that it was not worth waiting for Intel to finally catch up with the competition. I do think that the company is undervalued at its current valuation but I do not see any catalysts in the coming months that will move it closer to its fair value.

INTC Free cash flow (Tikr.com)

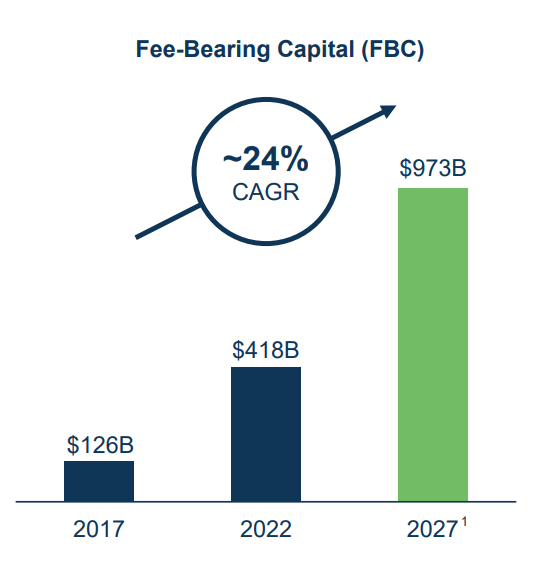

To replace Intel I decided to buy a stock that I already owned shares in, but that has been trading below my estimated fair value. Since the spin-off from Brookfield Corporation (BN), the company's share price has increased substantially. However, given the company's strong outlook, it expects to increase fee-bearing capital by approximately 550 billion by 2027, I was inclined to add more money to the company. What speaks in favor of the company is that it had approximately 400 billion of AUM that wasn't fee-bearing at the end of Q1. If the company is able to generate a fee on that capital it will substantially increase its earnings, which they will use to increase the dividend to its shareholders. For the reasons outlined above, I decided to add to my position in Brookfield Asset Management.

Fee-bearing capital growth (Brookfield)

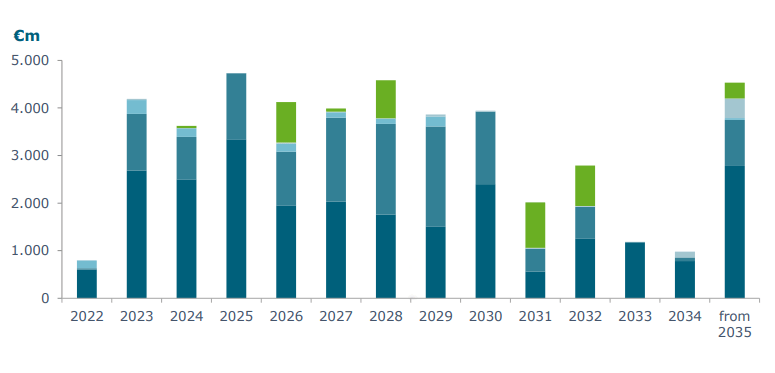

Vonovia is a stock to which I added a significant amount of money in the last year. Out of all my stocks I have put the most in the company. Unfortunately, the company's performance has been abysmal which means that this position is not profitable. My current average cost price per share is €37.96, which I expect to easily break even on in the next two years. Vonovia is the largest listed residential landlord in Germany and Europe. It has significant economies of scale, which they increased even further with the acquisition of Deutsche Wohnen last year. The higher interest rates have depressed the share price, even though the company's rents are adjusted by the Mietspiegel (average rent price in the area for similar properties) or CPI and new construction has declined significantly. The fact that Germany has a shortage of housing, which was strengthened by the influx of immigrants from Ukraine after the start of the war, property prices have remained relatively strong. The company's debt maturity has been spread out over the coming years with the weighted average maturity at 7.5 years at the end of Q3.

Maturity schedule (Vonovia)

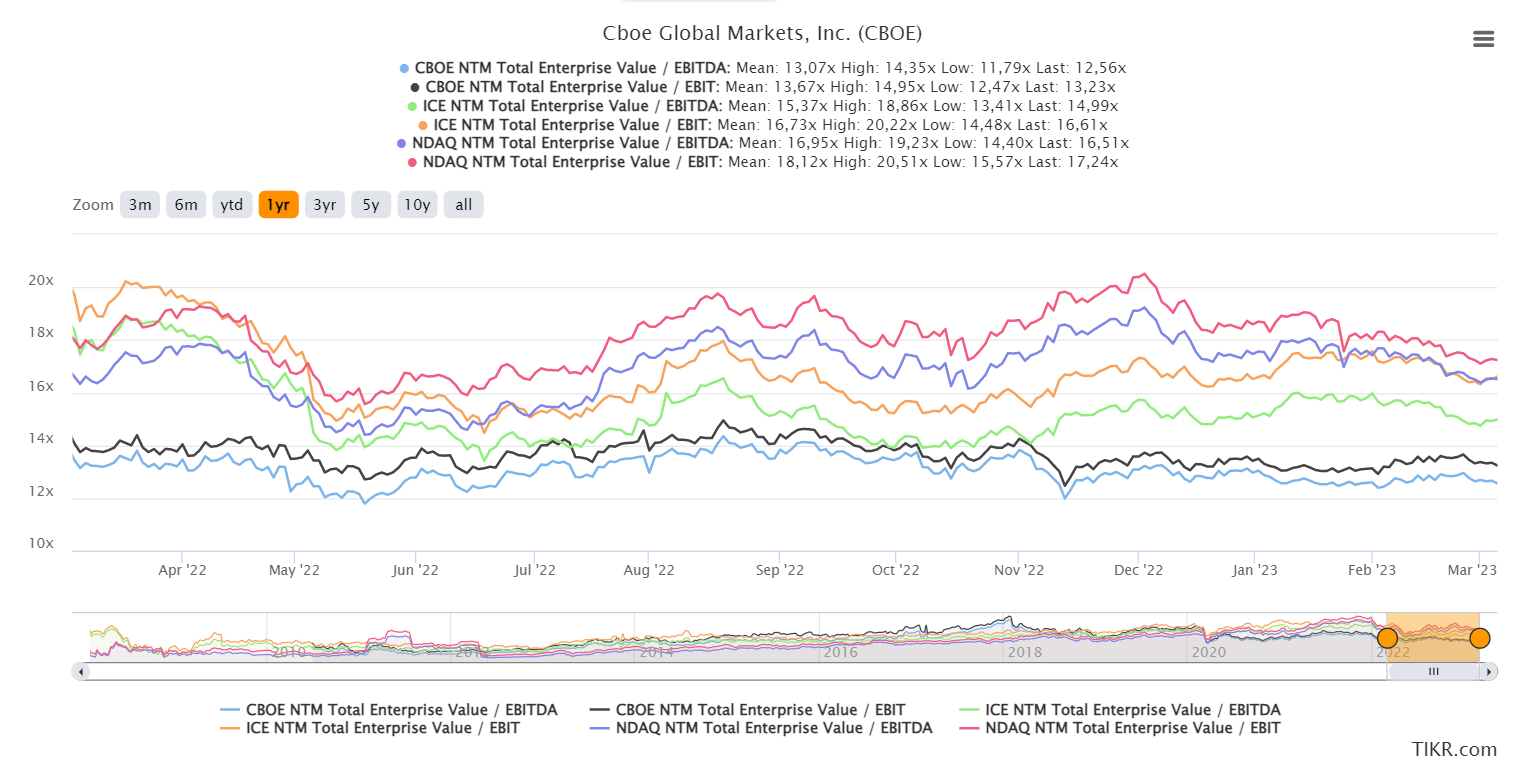

Cboe Global is another company that I mentioned in last month's update. The company runs multiple exchanges which is an industry with high barriers to entry. This protects the company from new entrants and allows the company to invest more into its products without having to fight competition. Additionally, the company is trading at a cheaper valuation than its main competitors Intercontinental Exchange (ICE) and Nasdaq (NDAQ), while its growth outlook is similar, and it has a significantly lower net debt to EBITDA ratio, which gives it the flexibility to acquire other companies in related sectors. This is a strategy that the company has successfully used over the years with the acquisition of the BATS exchange as the most successful one. Based on the reasons outlined above and my fair value estimate of $143.10 I decided to add to this position.

CBOE valuation vs peers (Tikr.com)

Company | Shares | Total price | Effects on dividend pre-tax |

NeoGames | -57 | $820.80 | $0 |

CTPNV | 19 | €258.78 ($275.19) | €8.55 ($9.09) |

Intel | -20.3 | $532.27 | -$9.74 |

Brookfield Asset Management | 17.2 | $584.80 | $22.02 |

Vonovia | 11 | €261.91 ($278.52) | €18.26 ($19.42) |

CBOE Global | 2.1 | $266.89 | $4.20 |

In February dividends were up almost 100% year on year. This was mainly driven by the position in Morgan Stanley (MS), which I did not own last year. My position in AbbVie (ABBV) I have barely touched over the past year, while my position in CVS Health (CVS) I have only recently started to increase again. This means that the majority of the difference is from the hike in dividends last year.

Company | Dividend 2022 | Dividend 2023 | Difference |

CVS Health | $5.14 | $7.05 | $1.91 |

AbbVie | $18.70 | $21.76 | $3.06 |

Morgan Stanley | $0 | $15.81 | $15.81 |

Total | $23.84 | $44.62 | $20.78 |

Author's dividend overview (Author)

This month a few of my companies have decided to increase their dividend. The largest increase was made by TJX Companies (TJX) which increased its dividend by 12.7%. My new forward dividend is now €1,173.34 or $1,251.40.

Company | Increase in dividend quarterly | Dividend per share pre-raise | Dividend per share post-raise |

CTPNV* | €0.05 ($0.05) | €0.40 ($0.43) | €0.45 ($0.48) |

L3Harris (LHX) | $0.02 | $1.12 | $1.14 |

TJX Companies (TJX) | $0.0375 | $0.295 | $0.3325 |

Prudential Financial (PRU) | $0.05 | $1.20 | $1.25 |

Ahold Delhaize (OTCQX:ADRNY)* | €0.10 ($0.11) | €0.95 ($1.01) | €1.05 ($1.12) |

* pay a semiannual dividend with an interim and final payment

sector allocation (author)

Compared to last month there has been a significant shift in portfolio allocation. The additional capital allocated to Brookfield Asset Management in combination with the strong performance of my financial stocks increased their value from approximately $8k to $10k, making it the second largest sector. Secondly, the transfer of NeoGames and Bragg Gaming and the sale of Intel decreased my allocation to IT stocks by approximately $1k. I know that this portfolio is now even more underweighted to IT stocks, but this averages out with my other portfolios. For this reason, I am currently not looking into adding significantly more capital to the IT sector, although this might change in the coming months.

Ticker | Qty Held | Portfolio % | Days Since Latest Buy |

CTPNV | 183 | 5.65% | 22 |

VICI Properties (VICI) | 73 | 5.62% | 386 |

AbbVie | 16 | 5.46% | 466 |

CBOE | 19 | 5.32% | 2 |

L3harris | 11 | 5.21% | 32 |

Ahold | 72 | 5.16% | 192 |

Broadcom (AVGO) | 4 | 4.89% | 151 |

Enbridge (ENB) | 55 | 4.80% | 479 |

Visa (V) | 10 | 4.80% | 177 |

Prudential Financial | 21 | 4.66% | 217 |

Vonovia | 83 | 4.49% | 2 |

Morgan Stanley | 20 | 4.45% | 214 |

TJ Maxx | 25 | 4.39% | 323 |

Inditex (OTCPK:IDEXY)(OTCPK:IDEXF) | 62 | 4.32% | 214 |

Prosus (OTCPK:PROSY) | 23 | 3.86% | 291 |

Aroundtown (OTCPK:AANNF) | 608 | 3.52% | 122 |

Brookfield Corporation (BN) | 45 | 3.39% | 86 |

NETSTREIT (NTST) | 73 | 3.39% | 219 |

Armada Hoffler (AHH) | 111 | 3.24% | 70 |

CVS Health (CVS) | 16 | 3.01% | 32 |

Brookfield Asset Management (BAM) | 39 | 3.01% | 8 |

Fresenius SE & Co. KGaA (OTCPK:FSNUF) | 40 | 2.40% | 336 |

Mips AB (OTC:MPZAF) (OTCPK:MPZAY) | 19 | 1.93% | 70 |

Microsoft (MSFT) | 2 | 1.20% | 122 |

StoneCo (STNE) | 53 | 0.99% | 231 |

Interactive Brokers (IBKR) | 4 | 0.74% | 290 |

Tezos (XTZ-USD) | 50 | 0.13% | 736 |

Hedera Hashgraph (HBAR-USD) | 680 | 0.11% | 708 |

Bitcoin (BTC-USD) | 0 | 0.08% | 708 |

Binance (BNB-USD) | 0 | 0.02% | 736 |

In the coming month, I am aiming to add an additional €800 to my portfolio. I will try to add to companies that I think are good value for money. Currently, I am aiming to add to the following stocks:

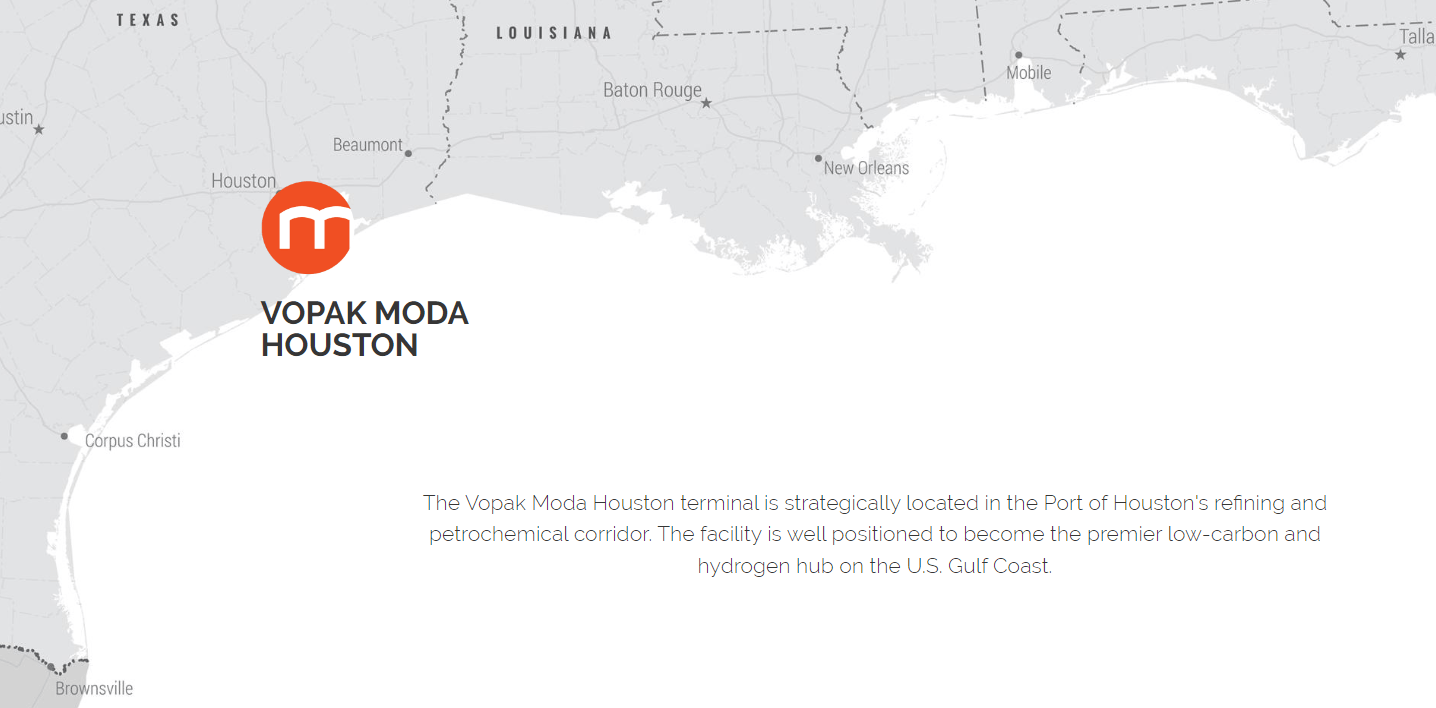

Enbridge is one of the largest pipeline and energy companies in the world. Its pipelines spawn from Canada all the way to the south of the United States. Last year the company acquired Moda Midstream, which gave it access to one of the largest crude oil storage and export terminals in the United States. What I like about pipeline companies is that pipelines can generate a stable revenue stream for a significant amount of time, even after they have been completely written off. Furthermore, the economic environment has been shaky at times over the past few months, making Enbridge's stable cash flows more attractive. There are some risks with Enbridge though as the governor of Michigan has been trying to sue the company for quite some time. Personally, I don't believe that anything will come from it as we will still need oil and gas in the coming years, which are best transported through pipelines. For those reasons, I am interested in adding more capital to Enbridge.

Moda Houston (Moda Midstream)

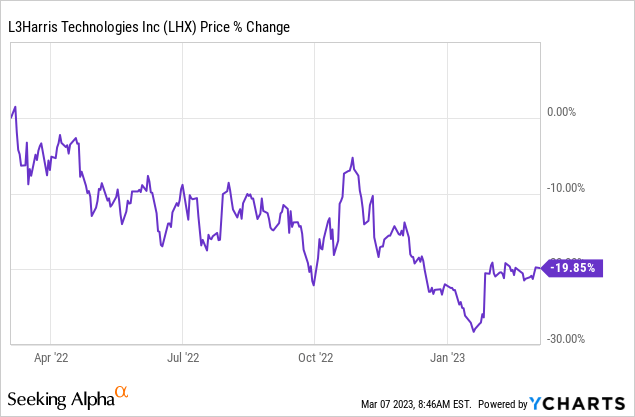

L3Harris is a company that has sold off over recent months. There are a multitude of reasons why it sold off. First of all, the war with Ukraine has slowly but surely lost the attention of people, bringing stock prices in the defense sector back to pre-war levels. Secondly, the high inflation rates have hit margins and impacted the profits of defense companies. Thirdly, more specific to L3Harris is the pending acquisition of Aerojet Rocketdyne (AJRD). The acquisition follows after an acquisition by Lockheed Martin (LMT) was canceled after the FTC decided to block the acquisition. Even though there is a significant chance that this will happen again, L3Harris has a larger chance of pulling it off as it is currently not active in the engine maker. My personal conviction on the stock is not reliant on the acquisition going through and at the current prices, I estimate that the company is undervalued by approximately 10%.

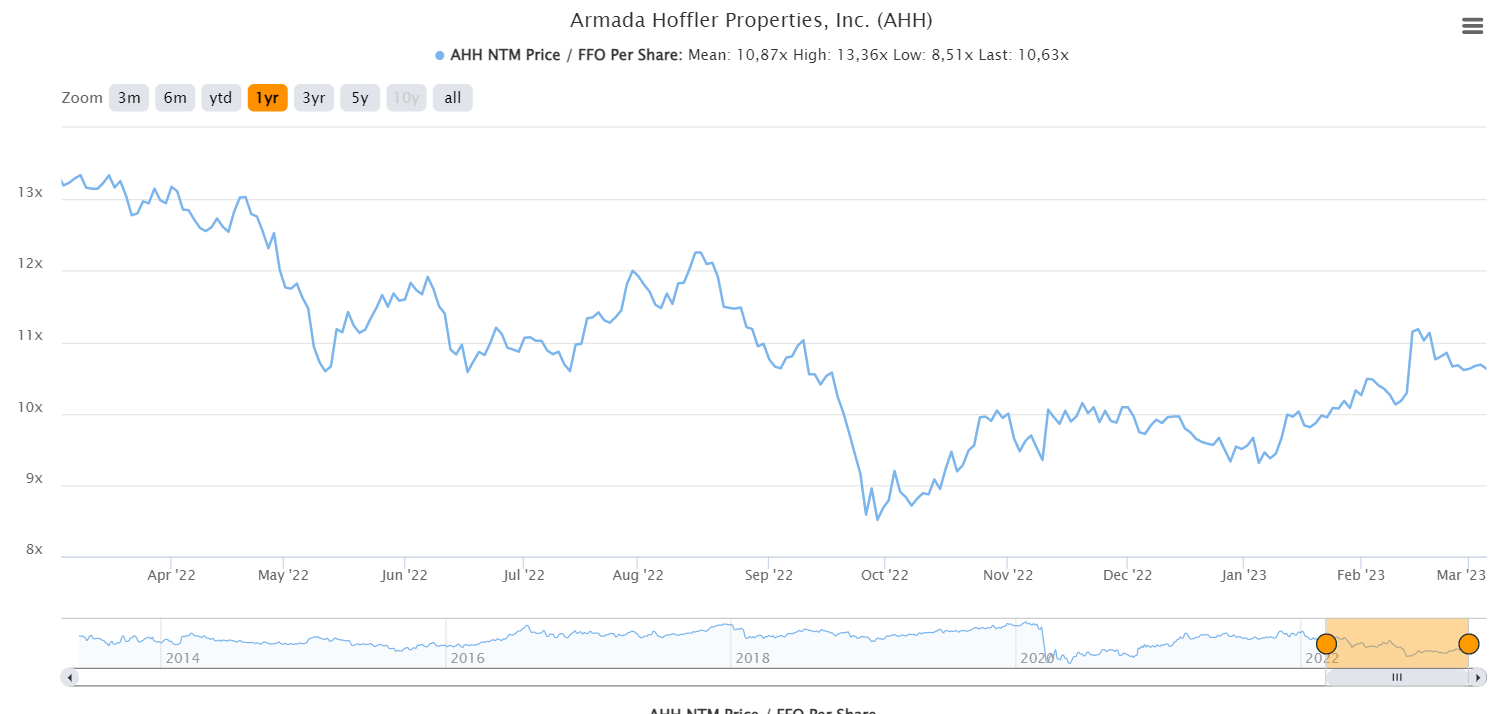

Armada Hoffler is a real estate owner and developer active in the Mid-Atlantic region in the United States. The company owns 3 different classes of real estate: retail, office and residential. The strength of the company is that it develops entire town centers and builds retail and office spaces near the apartments. As a result, the properties of Armada Hoffler have some of the highest occupancy rates in office and retail. At the same time the company is currently a bargain, trading at a forward P/FFO of 10.6x, while the average REIT trades at approximately 15x FFO. Truth be told the company has a relatively high leverage level but was recently upgraded to investment grade. This should lower the cost of capital going forward, even after the rate hikes of the last few months. For those reasons, I would love to add to my position in Armada Hoffler.

AHH P/FFO (Tikr.com)

The final stock is one that I also mentioned last month. Prosus is a venture capitalist that is listed on the Amsterdam Stock Exchange. The company is originally a spin-off from Naspers (OTCPK:NPSNY), but nowadays the structure is a bit more complicated. Both companies own shares in the other and the only difference between the two companies is the stake that Naspers has in some South African companies. The complicated structure, the large exposure to China through its stake in Tencent (OTCPK:TCEHY) and the rate hikes have affected the share price significantly over the past year. As a result the company trades at a significant discount to its holdings, which I currently estimate at 36.5% at the moment of writing, while the discount to its stake in Tencent is around 17%. My valuation is based on sum of the parts which use the market value of its publicly traded holdings and the book value for the other stakes. Some of its most well-known stakes besides Tencent include Delivery Hero (DHERO), Udemy (UDMY), and Remitly (RELY). Thus, by owning Prosus you own these businesses at a fraction of the price.

Overview of some of the holdings of Prosus (Prosus)

The stock market wasn't able to extend its run into February, which was in line with my own expectations. As a result, some stocks moved closer to their buy territory and this month it led to the addition of capital to 4 stocks and the sale of 1 stock.

During this month I received approximately $45 in dividends, which was up approximately $20 compared to last year. My forward dividends at the end of February were $1,251.

I hope you enjoyed the update about my progress, and I would love to hear your thoughts on my portfolio and what you would like to see in future updates.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.