bjdlzx/iStock via Getty Images

bjdlzx/iStock via Getty Images

Key ratios indicate Federal Signal Corporation is currently overvalued, but I have rated it a Buy nonetheless.

It has grown rapidly since getting past the COVID-19 and supply chain issues of a few years ago, and should deliver more growth and capital gains in the long run. I have a one-year target price of $93.50, an increase of roughly 16% above the current price.

The company describes itself, in the 10-K for 2023, this way “The Company designs, manufactures and supplies a suite of products and integrated solutions for municipal, governmental, industrial and commercial customers.” It operates through two segments:

According to the fourth-quarter earnings release, ESG is the biggest breadwinner, with Q4 sales of $373 million, compared to $75 million for SSG.

The company was founded in 1902, and it operates 21 manufacturing plants in five countries.

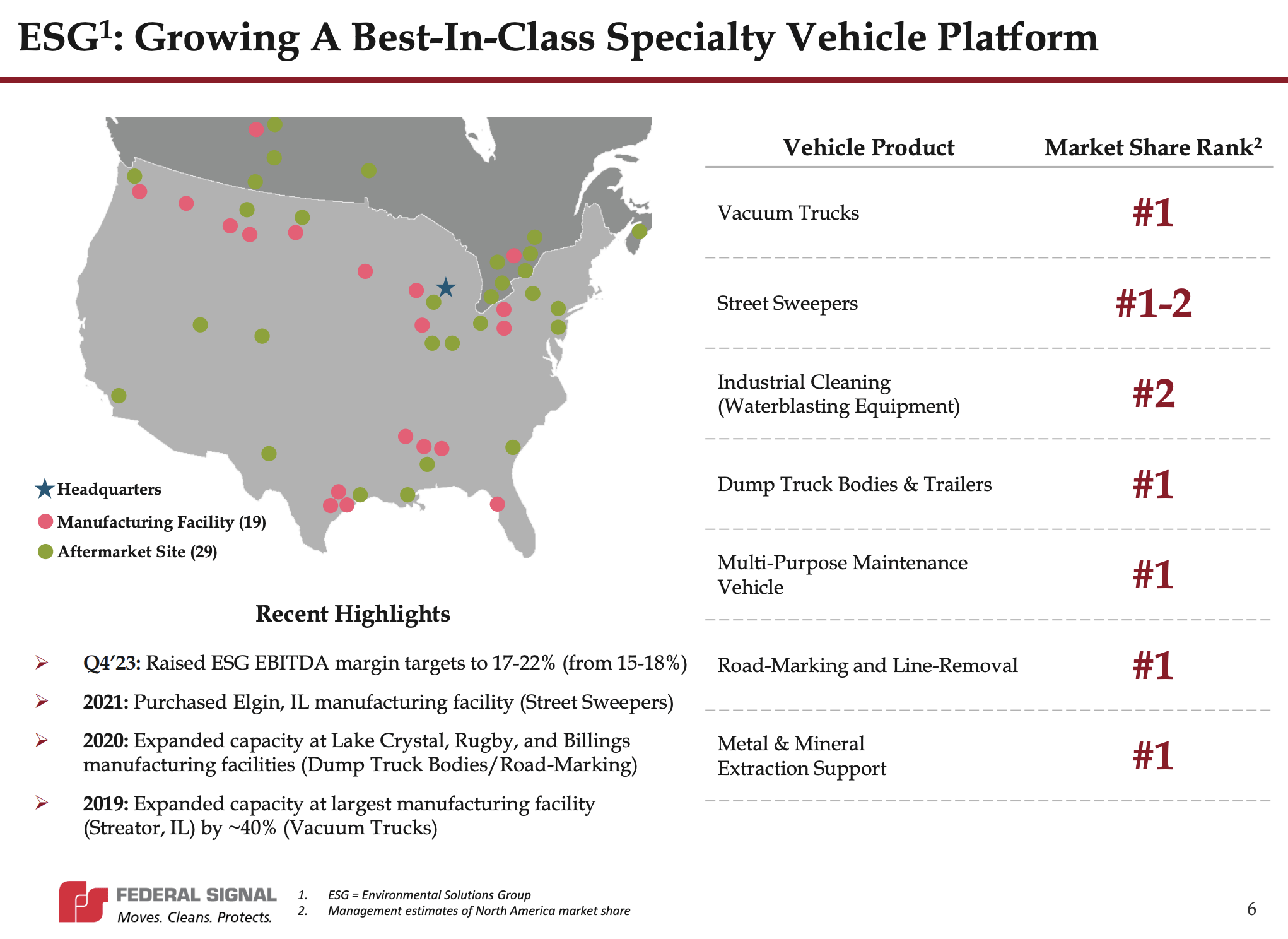

In its December 2023 investor presentation, Federal argued that it holds top market shares in many of the markets it serves:

FSS Market Shares (December 2923 investor presentation)

I checked on two of those claims and found they are backed up for vacuum trucks by Allied Market Research and for street sweepers by Global Market Insights.

According to the latter, major street-sweeping competitors include Alamo Group Inc. (ALG) and Bucher Industries AG (OTCPK:BCHHF). According to Allied, Federal competes with many privately held companies for vacuum truck sales.

Another competitive advantage comes from its long history and brand names.

In the 10-K, it argued that its regional, national, and global dealer network for vehicles is a distinguishing factor from its competitors. Presumably, that means none or few of those competitors have the same brand visibility, economies of scale, and after-sales support.

Do Federal’s profitability margins indicate competitive advantages? Yes, the gross margin is 26.13%, about 15.0% lower than the Industrials sector median of 30.71%. However, it does beat the sector on its EBITDA margin, which is 16.54% and its net margin, which is 9.14%. The latter is 52.0% higher than the sector median. One other measure of profitability is Return on Common Equity, at 16.9%.

The margins, and particularly the gross, are helped by a growing gap between revenue and cost of revenues. These are the differences (revenues minus cost of revenues):

Again, we see the dip associated with the pandemic and then the rebound.

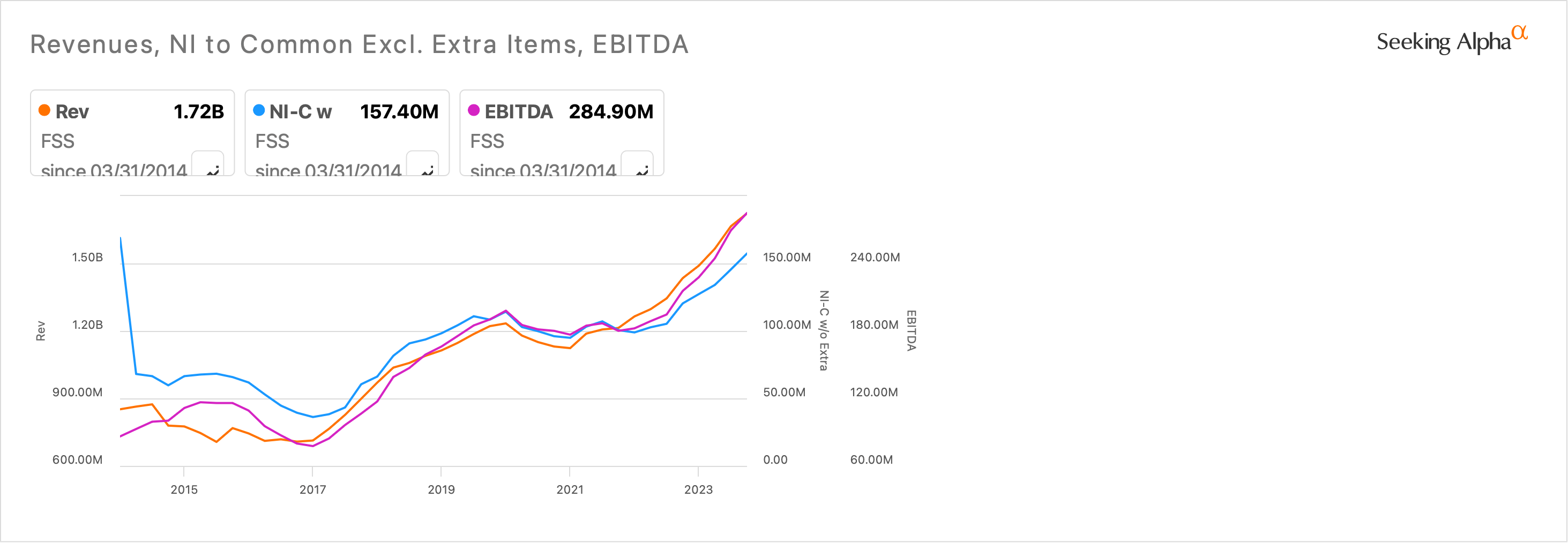

The following chart shows how Federal’s fundamentals began picking up steam in 2017, and rose rapidly with the exception of a COVID-19 and supply chain slowdown:

FSS chart of revenue, EBITDA and EPS (SeekingAlpha)

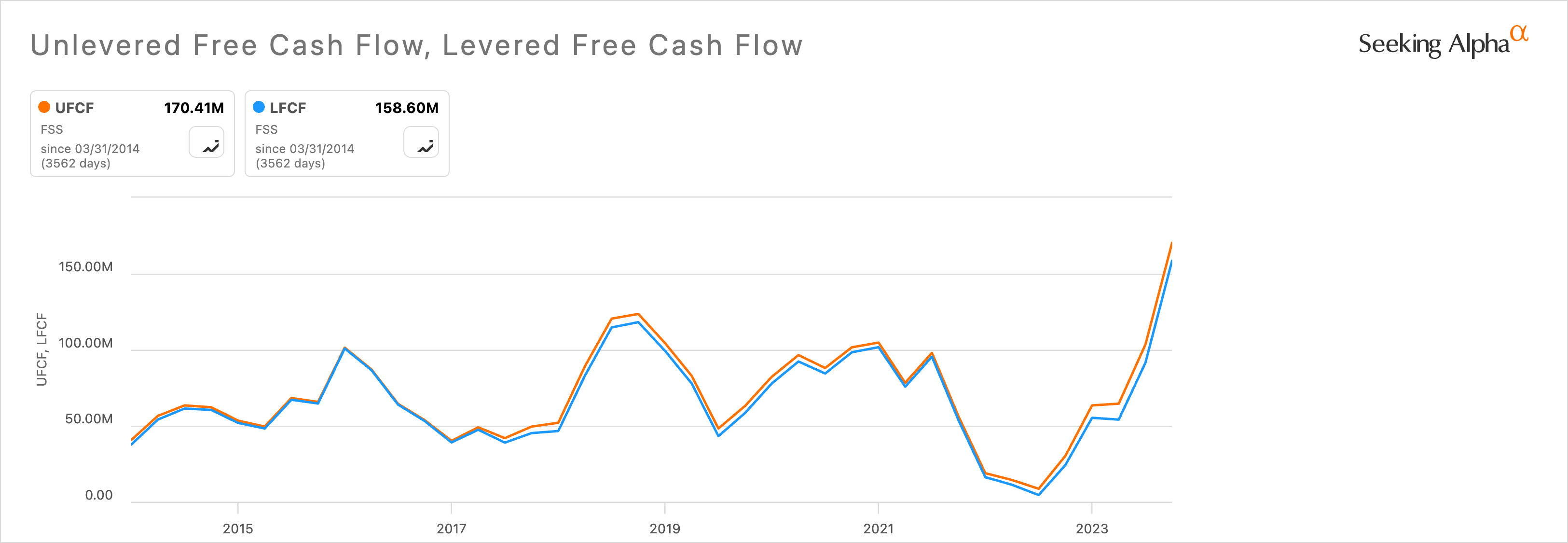

It also has the levered and unlevered free cash flow to continue growing:

FSS Free Cash Flow charts (SeekingAlpha )

It also has the benefit of several macro tailwinds. In her March 2023 letter to shareholders, CEO Jennifer Sherman pointed out that the company was “already seeing some impact” from the U.S. government’s American Rescue Plan Act, an initiative that helps fund state and local municipalities’ essential infrastructure. She also mentioned the infrastructure legislation should provide benefits for most of its products and services.

Feedback from dealers indicated that contractor inquiries were picking up as they develop plans to work on infrastructure projects. At the end of 2023, Federal reported an increased backlog, $1.03 billion, up 17% from the end of 2022.

On the financial side, the firm expects net sales of $1.85 to $1.90 billion, compared to $1.72 billion in 2023. In its outlook, it also projected adjusted EPS of $2.85 to $3.05, up from $2.59 in 2022.

The five Wall Street analysts who have prepared EPS estimates for the end of this year see earnings growing 15.88% to $2.98. The four who projected earnings in 2025 expect another 12.52% increase, to $3.36.

Also growing is the dividend, which is currently $0.48 annually and has grown by an average of 4.70% per year for the past five years. The yield is 0.60%, which puts it below the S&P 500 average but is reasonable for a growth stock.

President and CEO Sherman, a corporate attorney, joined Federal in 1994, and after serving in other leadership positions became CEO in 2016. Her work on new product development earned Federal a 2016 Chicago Innovation award and a CEO Innovator of the Year nomination from the Executives’ Club of Chicago. In addition, Ms. Sherman is a director of Franklin Electric Company, Inc. (FELE).

Ian Hudson is Senior Vice President and Chief Financial Officer, and has held the financial reins since 2017. Before joining the company, he held a senior accounting positions at Groupon, Inc. (GRPN) and was a senior audit manager at Ernst & Young, LLP.

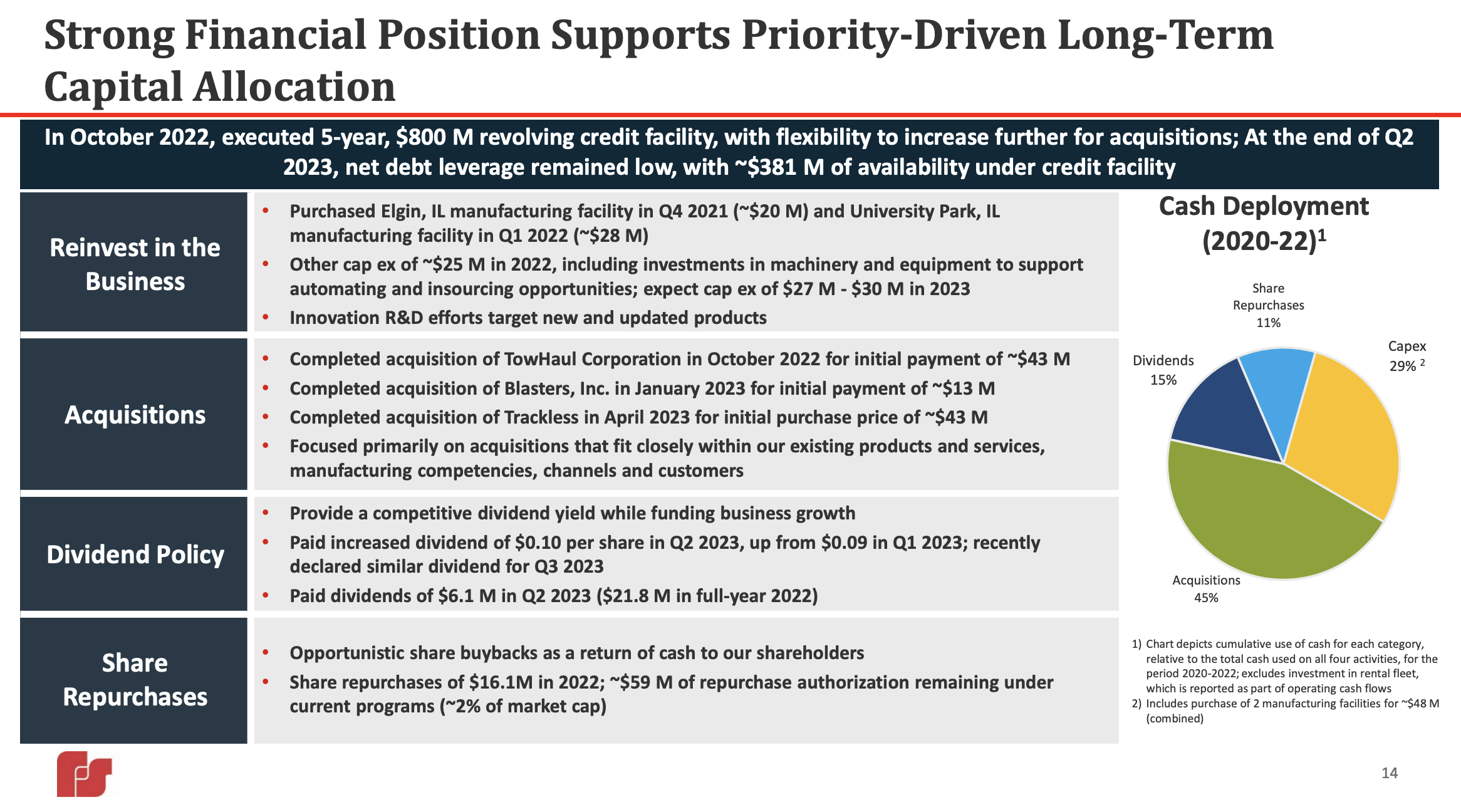

In its December 2023 investor presentation, Federal laid out what it calls its “strategic pillars”:

As this slide from its August 2023 investor presentation shows, merger and acquisition spending gets the largest share--45%--of capital allocation:

FSS Allocation (Investor Presentation)

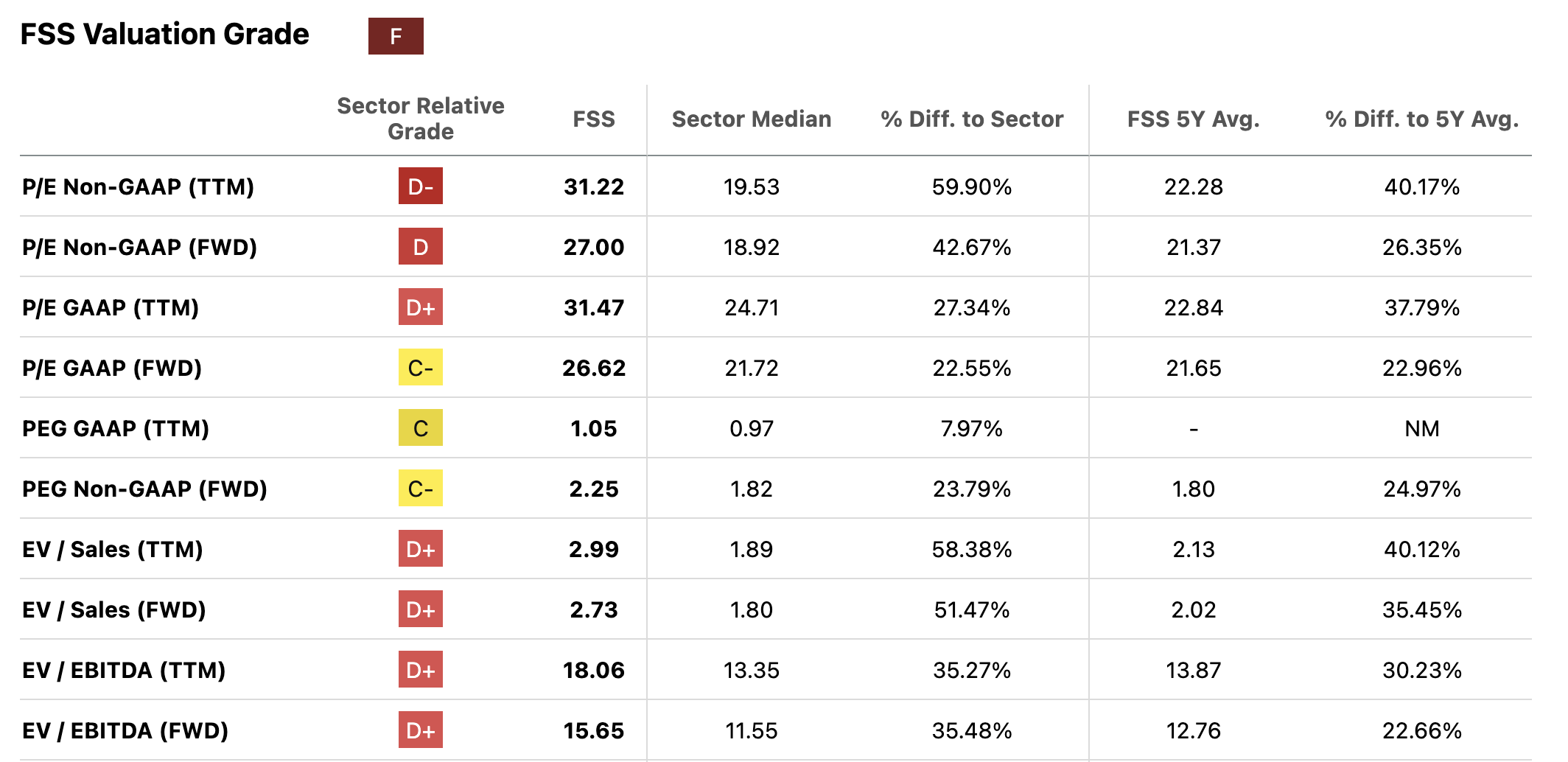

This extract from the Seeking Alpha Valuation page shows how Federal is more expensive than several industrial sector medians.

FSS Valuation Ratios table (SeekingAlpha )

Investors have pushed up the price, apparently expecting further increases. It also means the stock is currently overvalued, even when growth is factored in (with the exception of PEG GAAP (TTM).

As noted, Wall Street analysts expect EPS to grow by 15.88% this year and 12.52% next year. Despite that bullishness, their average price target for the next year is $78.00, which is below the March 5 price of $80.71.

Federal is guiding an adjusted EPS of $2.85 to $3.05. That implies a 10.42% increase on $2.85 and an 18.22% increase on $3.05.

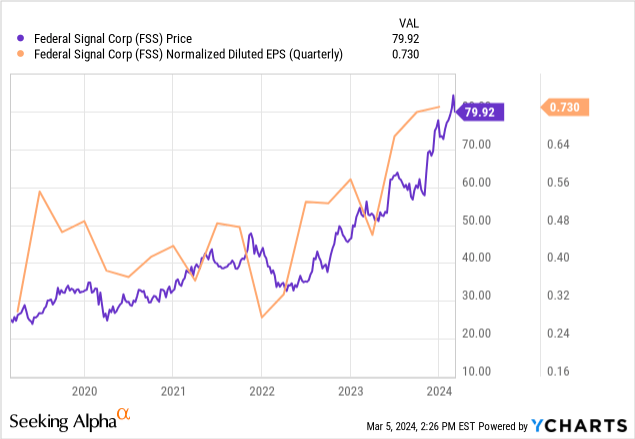

Given macro tailwinds, as well as its own growth efforts, I expect 2024 to be closer to $3.05 than $2.85. And as the following chart shows, earnings and the share price track quite closely:

Therefore, like the Wall Street analysts, I expect earnings and the share price to grow by 15.88% over the next 12 months. Adding 15.88% to the March 5 price of $80.71 would be $93.53.

Growth of nearly 16% is attractive, but we also have to assume the price is currently overvalued. Potential investors will need to weigh three issues: by how much is Federal overvalued; where on the spectrum between $2.85 and $3.05 do they expect it to end up; and are these differences material when looking at an investment of at least three to five years?

I’m in the latter camp and would not buy on a short-term basis. But, over the next three to ten years, it could deliver significant capital gains. There’s also a small sweetener in the form of the dividend that currently yields 0.60%. On that basis, I’m rating Federal as a Buy.

The Quant system has a Hold rating; there have been no other Seeking Alpha ratings in the past 90 days; and Wall Street analysts give it one Strong Buy, one Buy, and three Holds.

A large proportion of Federal’s revenue comes from municipal, state, and federal governments. Should that spending slow, it will pull down the company’s revenue, and perhaps its EBITDA and EPS, as well. In its 10-K for 2023, it noted that it is subject to “considerable cyclicality” and moves in response to the overall economy.

About 20% of its net sales come from international operations, which means greater exposure to geopolitical and currency exchange risks.

As a manufacturer, it is exposed to raw materials issues, including availability, prices, and logistics. In 2022, supply chain problems adversely affected its operations.

While a strong economy is good for the company, low unemployment rates may make it difficult or more costly to hire and retain employees. In addition, about 10% of its workforce is unionized, and any stoppages could adversely affect its operations and financial results.

The company also reports that it is subject to “heavy” government regulations, especially in the areas of the environment and employee health and safety.

Federal Signal Corporation has been on an upward trajectory since coming out of the pandemic and associated supply chain problems. It has solid fundamentals that back that growth, including aggressive innovation and acquisition plans and resources.

I have a one-year price target of $93.50, but regardless of that, this company should continue delivering annual growth and capital gains in the long run.