Khanchit Khirisutchalual

Khanchit Khirisutchalual

Based on my current outlook and analysis of Freshworks (NASDAQ:FRSH), I recommend a buy rating. FRSH meets two key considerations that I have before investing in a company: a large market and strong execution. The markets that FRSH is in have a strong secular tailwind, largely driven by growing digitalization, and management has demonstrated that they can capture this demand through strong execution.

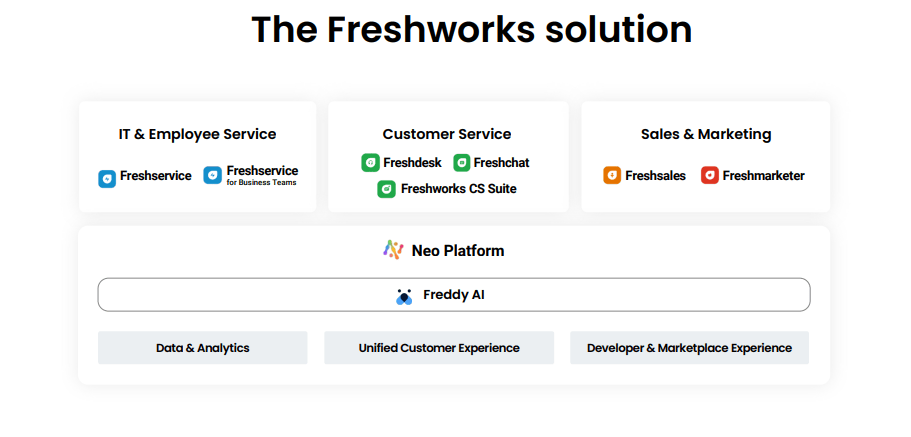

FRSH makes revenue by charging companies to use its software-as-a-service applications. Through the Neo platform, which offers a shared set of services, customers are able to customize the company's solutions to meet their specific needs. Freshworks provides businesses of all sizes with a portfolio of tools that address a wide range of functions, including: IT & Employee Service [IES]; Customer Service [CS]; Sales & Marketing [S&M].

FRSH

FRSH

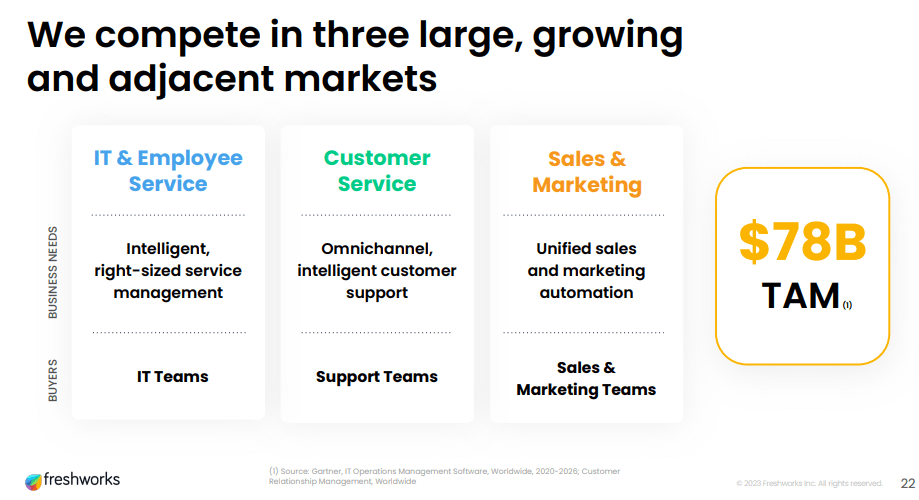

The functions that FRSH is tackling are huge addressable markets that collectively are worth $78 billion. As of LTM, FRSH generates ~$600 million in revenue, implying less than 1% in market share. To be realistic, FRSH will never be able to capture 100% of the market given that there are plenty of competitors out there, such as Salesforce, Inc. (CRM), but the sheer size of the market represents plenty of opportunities for FRSH to grow. Even achieving 2% market share is more than 2x FRSH’s current revenue size.

Aside from size, the speed of adoption should accelerate as the world becomes more digitalized and businesses continuously seek to improve productivity. There are still a lot of businesses that are not adopting digital solutions to facilitate their business. For instance, they could still be recording customer information and tracking sales using pen and paper. This could work on a very small scale, but as the business gets bigger, it is not a feasible option because of human error (cost to the business) and speed (humans cannot calculate faster than computers). More importantly, businesses stand to lose out against competitors as they are running on a higher cost structure. Hence, I believe it is an eventual thing for all businesses to tap on digital solutions. The secondary impact of being more digitalized is the higher need for IT support. The burden on the IT department gets larger as the company adopts digital solutions—from learning how the product works to implementation and troubleshooting. To make the life of the IT department easier, businesses would need to adopt necessary solutions (like what FRSH offers) to help with productivity.

Lastly, consumers today are much more sophisticated than in the past. Take this shopping journey, for example. A consumer could Google the product for reviews, compare prices across multiple sites, take a look at the physical goods in store, and probably contact the seller for questions before purchasing the product. Of all these steps, the one that will trigger a furious customer is likely the customer support step, where consumers are not able to easily contact the seller to address their concerns, or the seller simply doesn’t or takes too long to reply. This does not only apply to B2C businesses but also to B2B as well. Dealing with one customer is alright, but imagine dealing with hundreds of them. Hence, I think businesses need a digital solution to address this.

A large addressable market and a positive long-term growth trend are useless if FRSH cannot execute. Thankfully, execution has been really strong at FRSH, even in the current soft macro environment. One does not need to look too far to understand this. Just yesterday, FRSH reported its 4Q23 earnings, where it reported constant currency revenue growth of 19%, coming in at the high end of its guidance (17% to 19%). This performance is relatively strong when considering companies are scrutinizing their budgets and putting off tech deployments, leading to tech spending seeing pressure. Key operating metrics also point to strong execution and demand trends. For instance, FRSH has been making steady strides in reducing churn by concentrating on bigger and stickier customers. Additionally, FRSH saw a turnaround in declining trends from earlier in the year and stronger sequential expansion. As a result, the net retention rate [NRR] improved by 1 point sequentially to 107%. Apart from the improved fundamentals, the more important point to note is that trends have seen a recovery, painting a positive growth outlook for FY24 if the momentum follows through from 4Q23. While management 1Q24 guidance implies NRR to drop by 100 basis points (to 106%), I believe management is simply being conservative due to the macro still being uncertain (fed pushing back on rate cuts is not a good sign) despite new business remaining strong, particularly with larger customers where the company had a record number of new deals >$100K in both IES and CS segments.

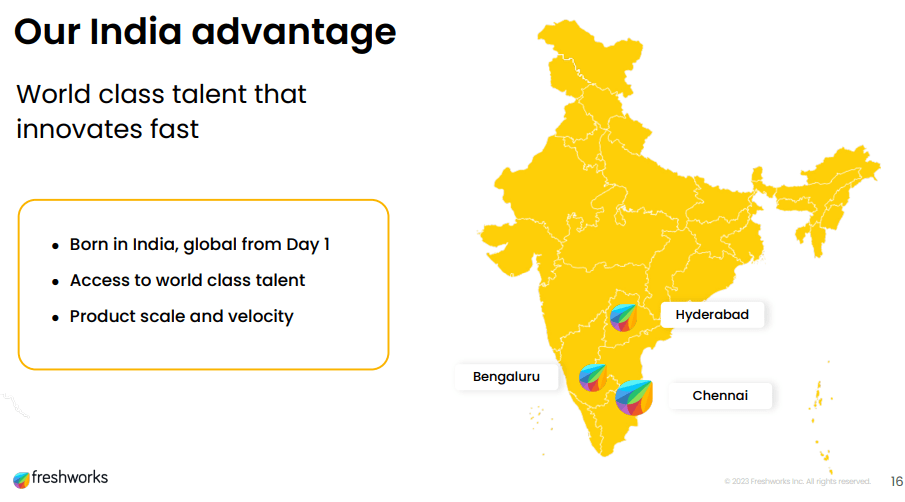

I would also note that FRSH has a structural cost advantage because a large portion of its workforce is located in India. This is a major cost advantage against its peers, which have most of their R&D employees in the US. This has massive implications as, for the same dollar, FRSH is able to achieve more R&D productivity (it can hire more in India), which means it is able to iterate and roll out more product features than peers. Also, in turbulent times (like today), even if FRSH were to downsize its R&D employee base, it could still achieve similar R&D efficiency at a cheaper cost.

FRSH

Author's work

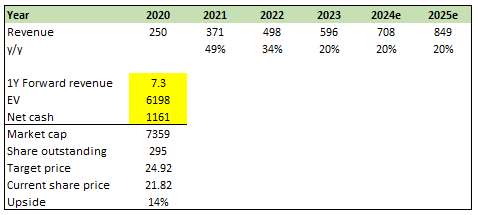

I believe FRSH will have no issues growing at least 20% for the next few years, given that it is already growing 20% in the current macro backdrop. If the macro recovers, growth can only get better from here. Management's 20% growth guidance for FY24 also supports my view. Another upside catalyst is a higher valuation being applied to the stock, and this should crystallize when FRSH improves its profitability. When compared to peers, FRSH trades at a discount because of its weaker margin profile, despite having similar growth strength. FRSH has been improving its profitability (non-GAAP EBIT margin improved from -4.5% in FY22 to 7.5% in FY23), and if this trend continues, it deserves a higher multiple, in line with peers. As of today, I am taking a safer approach by assuming FRSH valuation stays at where it is today (7.3x) at the low end of where peers are trading.

Author's work

A near-term risk to execution is the change in go-to-market leadership. While management doesn’t expect these changes to be disruptive, there is no guarantee that this will be the case. If the new leader and existing team cannot work well together, for whatever reasons, it will be very negative for FRSH stock sentiment as growth might be heavily disrupted. Note that the equity story is largely pinned on FRSH's ability to continue growing at 20%. If it shows a sign of weakness, the stock will feel a lot of pressure.

In conclusion, I recommend a buy rating for FRSH based on its significant growth potential within a large addressable market and robust execution. The increasing digitalization trend, coupled with businesses' continuous need for productivity improvement, enhances FRSH's growth prospects. Despite a challenging macro environment, FRSH reported strong 4Q23 earnings, demonstrating effective execution and demand trends. The company's strategic cost advantage, with a significant workforce in India, contributes to its cost advantage.