Chadchai Ra-ngubpai/Moment via Getty Images

Chadchai Ra-ngubpai/Moment via Getty Images

JFrog won the enterprise in FY23. That will be my key takeaway from their stellar Q4 FY23 results, which will be discussed in further detail below. What further encouraged me in my review of JFrog’s Q4 report was that its management went into great detail to explain initiatives that they had undertaken through the year to focus on acquiring larger, enterprise customers.

Moving forward, I see the developments in JFrog’s Q4 earnings report as bullish as well as providing tailwinds to position the software company for growth throughout the year. As of market close on February 14th, JFrog (NASDAQ:FROG) was up 3.3% YTD, underperforming SP 500 (SP500) which was up 4.8% YTD. I see strong upside here and will rate this stock as a BUY.

JFrog offers software management tools that help developers simplify & automate their software packages or artifacts in the software development process. The end result is that JFrog’s artifact management and automation tools help its clients continuously update their software without diluting the client’s end-user experience. JFrog is credited with launching the world’s first universal software package repository, called JFrog Artifactory. Over time, the company also began offering tools that help its clients spot and mitigate security issues early on in the software development lifecycle.

The company operates a freemium model and then converts customers using their land-and-expand model into upgraded tiers. JFrog officially uses a tiered-subscription-based model, as listed on their website. But their menu pricing also includes consumption-based pricing, similar to other players in the DevOps and DevSecOps software markets. The consumption pricing is very important to remember when assessing this company because the company stands to strategically benefit when consumption trends on their platform trend higher, as I observed in JFrog’s Q4 earnings, which I will talk about below.

Additionally, the company has ~7400 customers, mostly skewed towards smaller customers such as SMBs. But in the last few years, JFrog is also focusing more on large enterprise customers with >$1M contributions in ARR and success is showing as this segment is growing rapidly with the company scoring large deals.

As I mentioned at the start of this research note, JFrog is seeing massive tailwinds from enterprise acquisition and adoption of its tools. Management mentioned on the call how they were early in making changes not only to their sales processes but also to their product & feature development plans, which centered around acquiring and engaging enterprise customers. When summarizing their success in scoring large enterprise deals, here is what management had to say:

Finally, I would like to add a few words about the enterprise go-to-market changes we have successfully applied. AT&T, Vimeo, IVU Technologies, and Clalit, are all demonstrating what we have shared as our go-to-market strategy over the past few years. JFrog not only built and expanded our technology offerings, but also moved from inbound bottom-up sales processes to enterprise top-down motion. We best serve the enterprise, and we strive to build value around enterprise pains. Therefore, our team was focused in 2023 on expanding our customer portfolio with companies that meet this profile and land with a higher ASP and a higher propensity to expand faster.

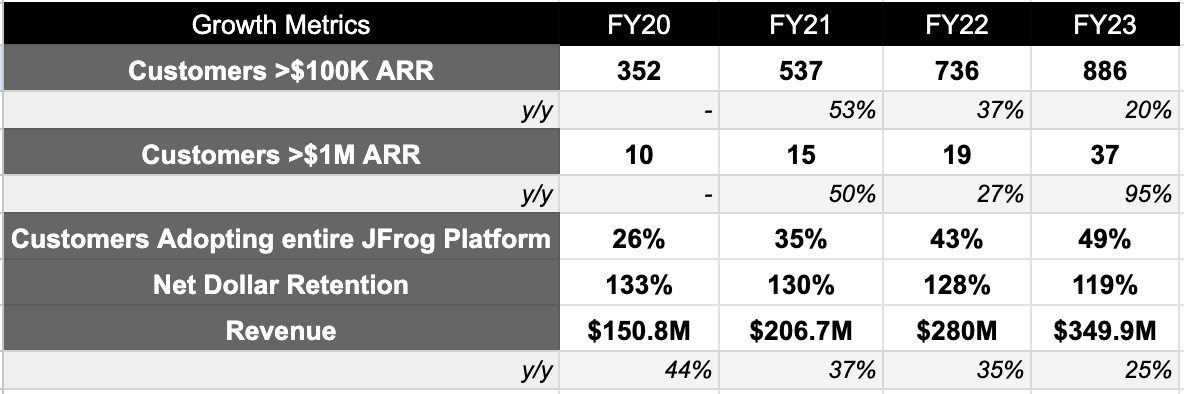

On the Q4 earnings calls, management also revealed that some of the features released last year were focused on MLOps & MLSecOps in the AI and ML DevOps space. These AI/ML products suddenly became relevant to large enterprises, especially since JFrog’s large customers and large target customers “are planning to have AI/ML software assets in production during 2024," according to management commentary. This has resulted in JFrog surprising me with its penetration into enterprise customers who contribute more than $1M in ARR, as can be seen below. Its closest competitor, Gitlab (GTLB) do not report on customers with >$1M ARR since their focus till now is still on SMBs as can be seen in Gitlab's Q3 FY23 report.

JFrog’s Customer & Revenue Metrics, Q4-FY23 investor presentation

In the most recent Q4 FY23 quarter, JFrog reported revenue of $97.3 million, topping analysts’ expectations of $93 million by 4.6%. Revenue in the fourth quarter not only improved y/y by 27%, but it also improved sequentially by almost 10%. For the full year FY23, revenue equaled $349.9 million, up 25% y/y and beating consensus forecasts by 1.2%. Management mentioned that they were seeing customers in the target market were moving to consolidate their DevOps and DevSecOps solutions into single vendors, suggesting JFrog was benefiting from these vendor consolidation trends. Here is some commentary that I found interesting:

Everything we bet on (in FY23) turned out to be what CIOs and CISOs want. They want consolidated suppliers rather than point solutions, they want security as part of the software supply chain, and they want to be able to track the full delivery flow of their software. We’re positioned in a very good place to answer market demand.

These vendor consolidation trends are quite similar to what I had observed in another segment of the AIOps market last week, where I mentioned how Datadog was winning over its competitor, Dynatrace. In addition, JFrog's management also mentioned that while cloud migration workloads were stabilizing, it was really the higher consumption of their platform that drove up consumption fees for JFrog, which was accretive to JFrog’s revenue growth. With management continuing to see higher consumption trends persist into this year, I believe this could also lead to a potential renegotiation of contracts by existing JFrog’s customers towards higher consumption limits, leading to higher contract values, which bode well for JFrog.

On an adjusted basis, the company earned 19 cents per share in Q4 FY23, beating consensus estimates of 13 cents a share. For the full year, JFrog earned 51 cents a share, ahead of market expectations of 44 cents a share. Most of the gains in its income were driven by a significant expansion in its adjusted operating income, which ballooned to $39 million, delivering adjusted margins of 11.1%. In FY22, JFrog was just about to break even on an adjusted basis, with operating margins at 0.5%.

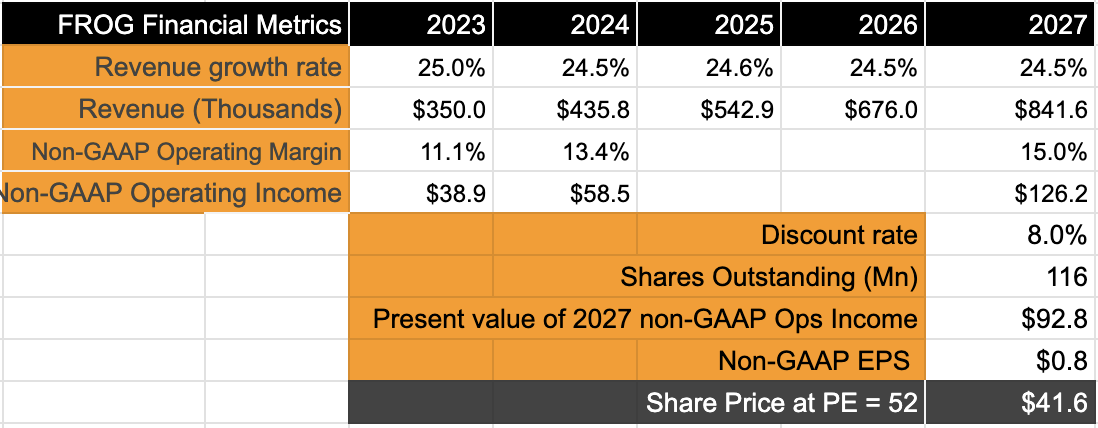

JFrog’s Financial Metrics, Q4-FY23 investor presentation

The company carries very little debt, which is only in the form of operating lease liabilities totaling ~$22.2 million, down about -8% y/y. Cash and cash equivalents grew 86% y/y to ~$85 million.

For the first quarter, JFrog mentioned they expect revenue to grow by 23.4% to $98.5 million at the midpoint, ahead of consensus estimates of $97.5 million, with adjusted earnings of 14 cents per share at the midpoint, above the consensus estimate of 11 cents.

For the full year, the company sees revenue growing by ~22% to 426 million at the midpoint, ahead of ~$421 million that analysts were expecting. Management also mentioned that it expects to earn ~59 cents a share on an adjusted basis, 13% higher than what consensus estimates were for JFrog’s earnings in FY24. I will use these updated numbers in my forecasts, in addition to the previous long-term model that was laid out in the Q1 call last year.

Driven by the strength in adoption of the JFrog Platform and our expectations for future contributions from the platform security core, we believe our operating model can achieve a 5-year revenue CAGR of 22% to 24% through fiscal year 2027, which would imply a potential revenue range of $775 million to $825 million, while delivering free cash flow in the range of $200 million to $240 million, implying an estimated margin of 26% to 29%.

Author

With the improved FY24 forecast and the long-term operating model I noted earlier, I see JFrog’s non-GAAP operating income now growing at a CAGR of 34% faster than their compounded revenue growth rates of ~25%. With earnings growing four times faster than the S&P 500’s long term 8% growth rates, I see a forward PE of at least 50x here since its earnings are expected to grow four times faster than the long-term EPS growth of the S&P 500 at 8%.

In terms of headwinds, the company may not be immune to any sudden slowdowns in the larger macroeconomy. If there are sudden slowdowns or a recession, clients may again lower their consumption patterns on JFrog’s platform, impacting revenue. In severe cases, clients would also optimize their usage of JFrog’s products, similar to behavioral patterns that were noted by management in the Q1 FY23 call last year. Additionally, if the company slows down its pace of innovation, it may become a victim of its own potential complacency. So far, JFrog has proven to be correctly developing tools in anticipation of their target customers' enterprise needs, especially in the AI/ML space. This has allowed them to penetrate the enterprise market faster than expected. This is something I will be keenly monitoring through this quarter, as well as in management’s commentary during their Q1 review next quarter. I expect management to have more visibility into how sustainable their market penetration can further be into the enterprise segment.

Finally, by operating in the DevOps or DevSecOps space, the company may be competing with other players that offer software artifact management tools such as GitLab, which offers pure cloud-based solutions. However, with JFrog now breaking further into the enterprise market, the company may be differentiating its offerings from GitLab, which still appears to have its focus on SMBs. However, if GitLab and other competitors were to also attempt to move upmarket, it could threaten the progress seen by JFrog so far.

A quick note about the impact of Israel's geopolitical conflict that I would also like to call out as a risk here. So far, the impact seems contained for JFrog. Management mentioned that the number of employees who were called up to the army reserves was reduced to 40 in Q4. The company explained that they have taken further steps to mitigate geopolitical risks by duplicating resources outside of Israel, while also adding that 99% of the company’s technology and intellectual property are outside the country.

The all round progress by JFrog has turned me bullish on the company’s software package management tools business. The company has prioritized enterprise clients who can help it weather economic storms better, and allows JFrog to have a well grounded margin profile. For now, I rate JFrog as a BUY.