muhammet sager

muhammet sager

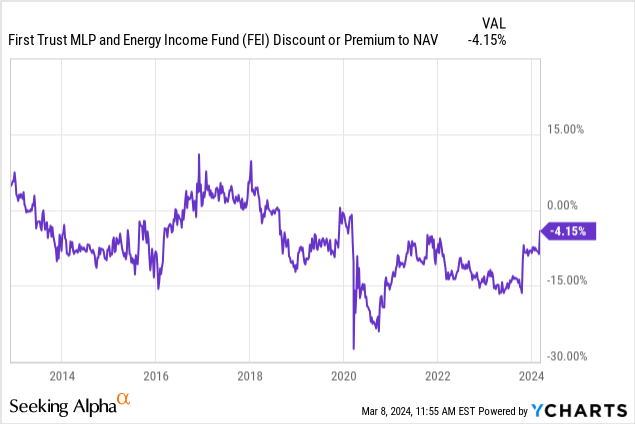

First Trust MLP and Energy Income Fund (NYSE:FEI) is a closed-end fund in the midstream space. Mostly investing in pipeline operators. The primary reason I'm interested here is that it is about to convert from a closed-end structure to an ETF structure. Its discount to net asset value is only 4.13% (which is very low for a pipeline CEF) but that's because the conversion is scheduled for Q2 2024. My guess is that it will happen early May (based on management disclosures) but if it happens a bit later in the 2nd quarter, that's not a disaster.

A 4.15% discount means there is 4.3% upside if the assets trade around net asset value after the conversion. In absolute terms it is not a huge return, but given the conversion should be done early May it is amazing in an annualized sense. There are ~2 months to go. At a glance, anyone will understand it is great if you could capture 4.3% 6x per year serially. Compounded, it gets a bit ridiculous because you end up with a 32%+ annualized rate. I don't like to count on that kind of returns with these kinds of deals, but I do think it illustrates that it is likely a beneficial bet to take.

It is uncertain whether the associated beta will cooperate. The pipelines look attractive enough to me on a fundamental basis. More importantly, Bill Gross really likes them. But over the next two months, fundamentals can only explain a small part of market gyrations. But at the end of the day, this is an AI and crypto market. Anything can happen.

The transformation isn't a 1:1 transformation, but actually a number of closed-end pipeline funds are being merged into an ETF in one go. I've also publicly covered First Trust Energy Infrastructure Fund (FIF) which is part of this transaction.

The First Trust Energy income and Growth Fund (FEN) and First Trust New Opportunities MLP & Energy Fund (FPL) are also involved. The merger of the MLP C Corp Funds (FEN, FEI, and FPL) should be tax-free to shareholders according to First Trust. However, the merger of the MLP C Corp Funds has a tax impact at the fund level. This could potentially impair the net asset value at the fund level. However, the latest disclosure about the required adjustment came in quite favorable:

...Subject to the satisfaction of certain customary closing conditions, the mergers of the Target Funds into EIPI are expected to close by the end of April 2024, or as soon thereafter as practicable. No assurance can be given as to the exact timing of the closing of the mergers...

...In connection with its merger into EIPI, each of FEN, FEI and FPL will likely be required to recognize an adjustment to its NAV as of February 29, 2024. Based on information available on February 28, 2024, FTA estimates that such adjustments will not result in any change to the NAV of FEN and could result in an increase in NAV of approximately $1,357,800 (or $0.030 per share) for FEI and a decrease in NAV of approximately $1,943,747 (or $0.083 per share) for FPL...

A $0.03 net asset value adjustment is more or less negligible. It decreases the upside from 4.3% to 4%. Annualized, this still ends up above 30% before factoring in the return of the underlying.

It seems like a reasonable option to hedge the underlying. This captures the return from the discount disappearing in a very clean way. The downside is that it is complicated and there are a lot of additional costs related to short-selling that eat into the returns. However, it is a return that isn't driven by market returns, and that's rare. Just holding the underlying comes with a lot more volatility, and the beta return (either positive or negative) could easily dwarf any returns made through the conversion.

Top 10 Holdings (as of 1/31/2024)

| Holding | Percent |

| Enterprise Products Partners L.P. (EPD) | 9.43% |

| Energy Transfer LP (ET) | 7.84% |

| MPLX LP (MPLX) | 5.49% |

| Cheniere Energy (LNG) | 5.41% |

| ONEOK, Inc. (OKE) | 5.09% |

| Plains All American Pipeline, L.P. (PAA) | 4.85% |

| The Williams Companies (WMB) | 4.27% |

| DT Midstream, Inc. (DTM) | 3.21% |

| Kinder Morgan, Inc. (KMI) | 3.19% |

| Sempra (SRE) | 2.84% |

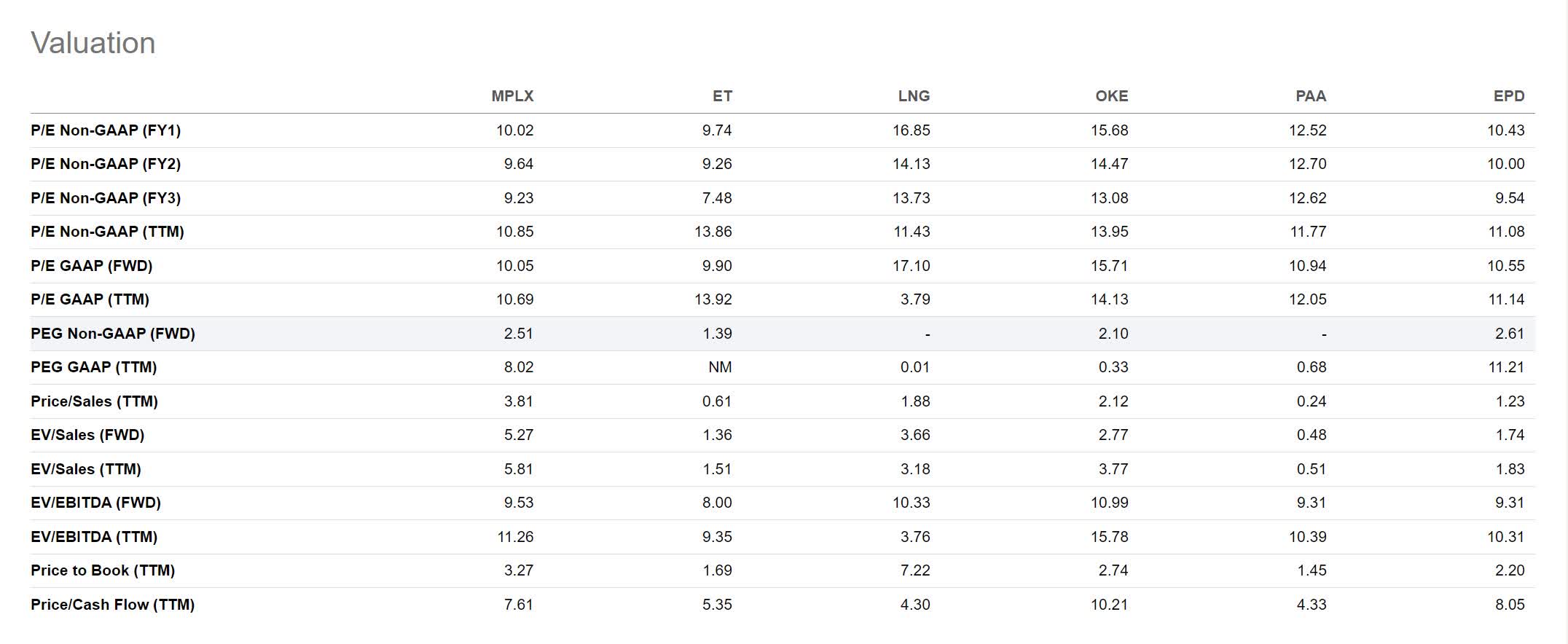

I looked up the fundamentals of the top 6 holdings out of the above through Seeking Alpha:

valuations pipeline holdings (Seekingalpha.com)

Earnings and EBITDA multiples look fine. Well below market rates for what are arguably relatively stable earnings. The price/cash flow metrics are great. It appears to me that these companies are in a harvesting phase after arguably overbuilding for quite some time.

Pipeline CEFs tend to trade at much deeper discounts, FEI's conversion makes the ~4% return potentially achievable through conversion very attractive. That's outside of any beta returns expected of the pipeline industry. I'm not sure if management skill matters much, as the two-month timeframe leaves very little room for a manager's skill to really shine through. This is even more truth when operating with a very narrow mandate.

Hedging the underlying delivers the cleanest and least correlated returns. However, this comes with increased complexity and costs. Hedged, I think of this as a relatively safe and uncorrelated ~4% return captured within 2 months.

Unhedged, there is at least $0.10 in announced dividends coming. Yet, it is hard to predict how pipelines will trade over the next two months. If I were holding this fund, I would think twice selling before the conversion went through. I would need high conviction that getting out of pipelines is the right idea, and even in that case I would be inclined to simply hedge the underlying and hold on to capture the conversion.