keeperofthezoo/iStock via Getty Images

keeperofthezoo/iStock via Getty Images

On our last coverage of Farmland Partners Inc. (NYSE:FPI) we weighed the bull and the bear arguments and found both to be wanting. We could not rate it a Sell and we were only ready to buy a bit lower.

But for FPI to actually deliver this value, will require a firm commitment to sell the whole company. This can happen right away or even over two years. But that is the only way we can see some significant upside. Exploiting the differences between public and private market values often turns out to simply be an educational exercise in realizing that public values were right to begin with. At present we rate FPI as a hold and would stick to our $8.50-$9.50 range for a tactical buy.

Source: Why The Strategy Is Not Working

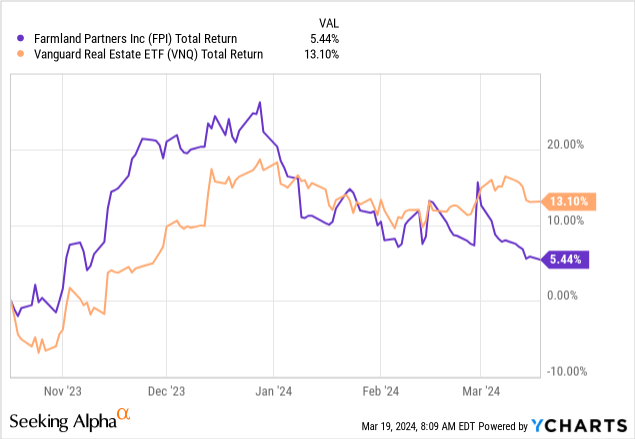

While FPI has moved higher since then, it has not remotely impressed compared to the rally in the Vanguard Real Estate Index Fund ETF (VNQ).

We look at the recently released Q4-2023 results, the 2024 outlook and update our views.

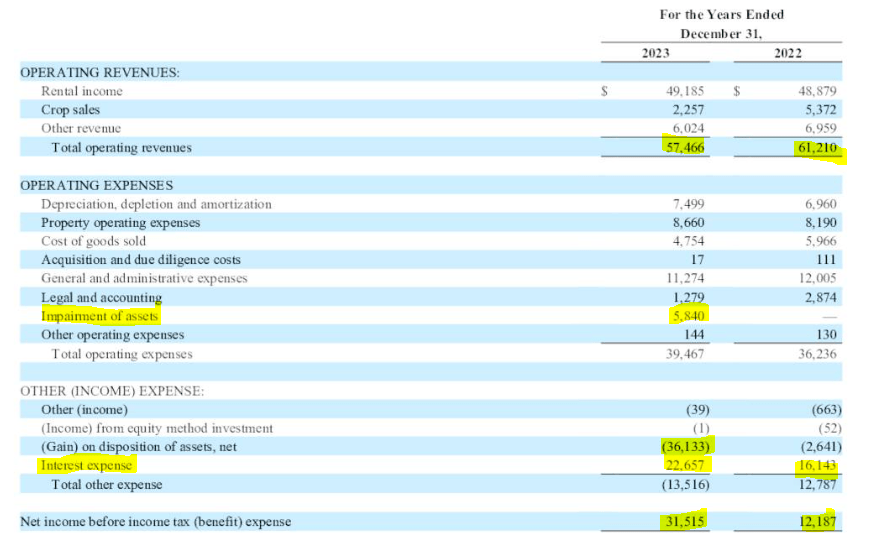

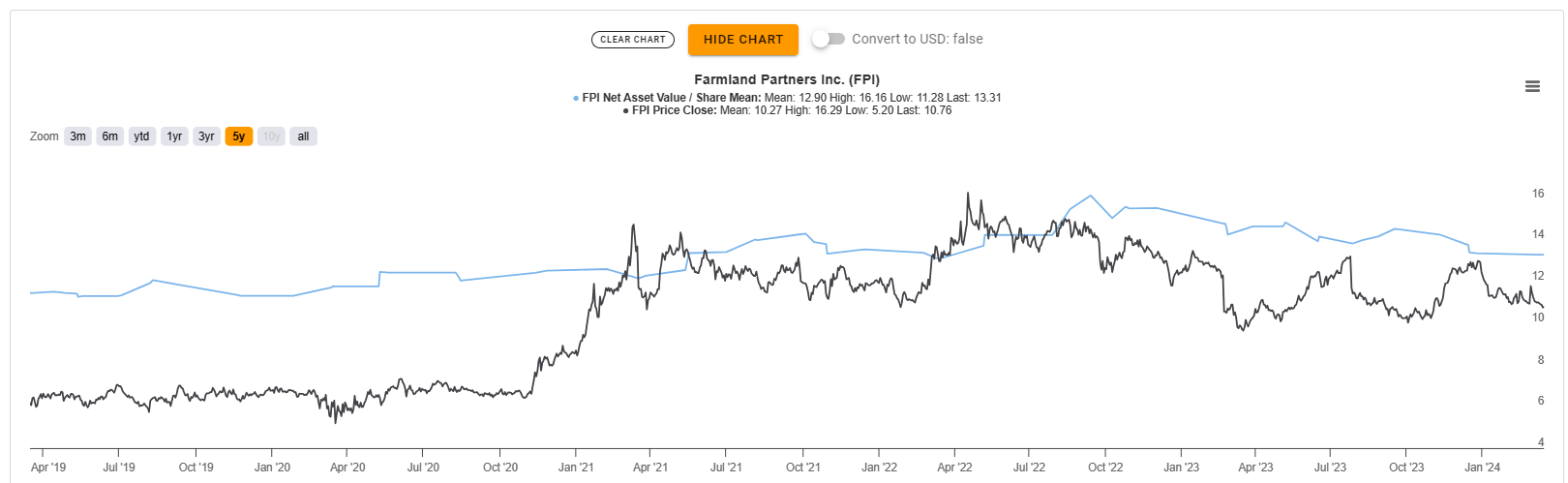

FPI had an active 2023 with a lot of asset sales. These were done in general at premiums to book value and resulted in $31 million worth of gains during the year. But the obvious side effect of that was that total operating revenues dropped year over year. This was despite the company reporting that the farm leases that expired during the year (14% of total), were renewed at rent increases of about 20%.

FPI Presentation

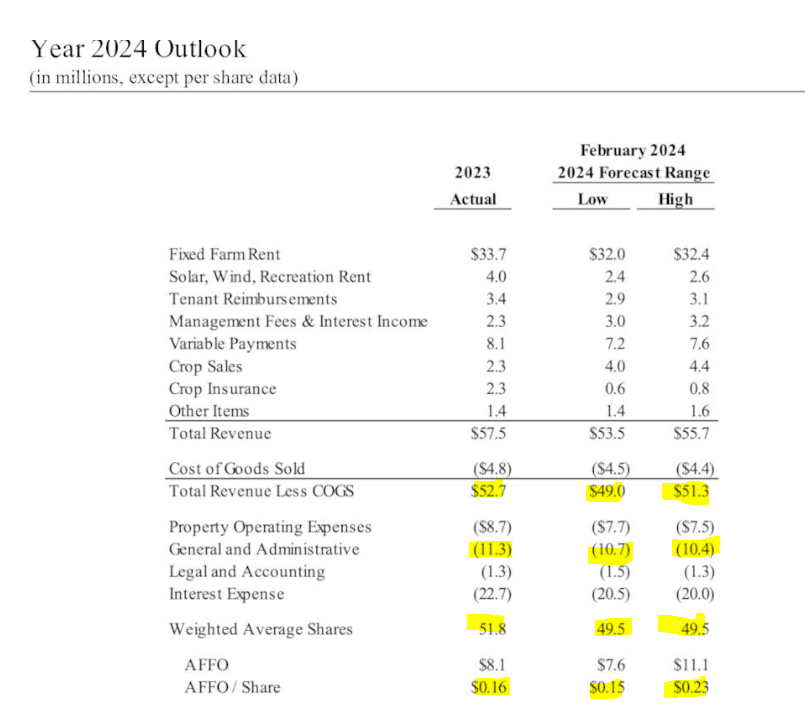

This just goes to show how much FPI has been selling during the past couple of years. Other notable items there were the $5.84 million impairment, which the company attributed simply to assets being worth less than their carrying value. Also notable was the increase in interest expense which went from 27% of revenues in 2022 to 39% in 2023. The overall net income looked impressive but that is a volatile series, thanks to asset sales. If you strip out the asset sale gains and the impairment, you can see that FPI did not do so well. The company's outlook for 2024 was even more interesting. Despite some more hefty increases in the renewing leases, the total revenues will be lower for certain. Interestingly though, the company's general and administrative expenses will be moving lower.

FPI Presentation

This is something we have discussed previously with the thinking being that expense category was a bit large for the revenues FPI generates. Combined with a lower a share count, FPI should manage to do a slightly better adjusted funds from operations (AFFO), at least at the midpoint of guidance.

Before we get to our outlook, there were a few things said on the company's conference call that really rang true. The first one was the gap with NAV, which we have acknowledged as well.

So the first point is we continue to be significantly undervalued comparing ourselves to the underlying asset value of the portfolio. Land values across the country have continued to go up in the green producing regions of the country, the growth rate slowed some in 2023. And we think that rate will slow yet again in 2024. But that needs to be taken in the context of the prior years. So in 2021 and 2022, we saw as rapid appreciation in farmland values as we've probably ever seen in history in the grain-growing regions of the country. That can't go on forever. So we will see sort of a flattening or a plateauing in my opinion as we move into 2024.

But what that has led us to and this is an overwhelmingly row crop oriented portfolio is there is a huge disconnect between the market value of our land in the private markets and the public company trading value of our common stock. As many of you know, I bought a significant amount of stock personally last year. The company bought back a lot of stock. We're likely to continue that effort as long as that gap continues.

Source: Q4-2023 Conference Call Transcript

So more asset sales and more buybacks for 2024. That is not a surprise. The second point was FPI acknowledging that the NAV discount and $2.00 buys you a coffee at Tim Hortons. The cash flow is more relevant for them. The company is now laser focused to try and raise this.

Despite what I said about the gap between our underlying asset value and the stock price, we are valued in many ways on AFFO. I frankly think that's incorrect as it relates to our company, but that is how REITs are valued. So, we must drive AFFO higher and we're working quite hard to do that.

So, we have embarked over the last 12 months or so on an aggressive cost-cutting effort and we're going to continue that effort into 2024. That cost cutting is coming from selective staff reductions, cutting our travel costs, [indiscernible] the size of our Board which is always a challenging thing to do but we have done it. I am going to take a $500,000 compensation cut in the 2024 year. That's 25% of the compensation I received for 2023 and Luca is going to stay flat in his compensation.

These steps really are required to try to drive AFFO higher. As a major shareholder I think like an owner not an employee and we are going to get this stock price higher and that requires increasing of AFFO.

Source: Q4-2023 Conference Call Transcript

So we are not going to sit back and say that the company does not get what it needs to do. But at a broader level, this is likely to be ineffective. Farmland is not an asset class that generates a lot of income. It works as a store of value and unfortunately for FPI shareholders, even this part has not really worked out.

The company is in a better position for 2024 than they were for 2023. They have made enough asset sales to deleverage, despite using a substantial sum to buy back shares.

10-K

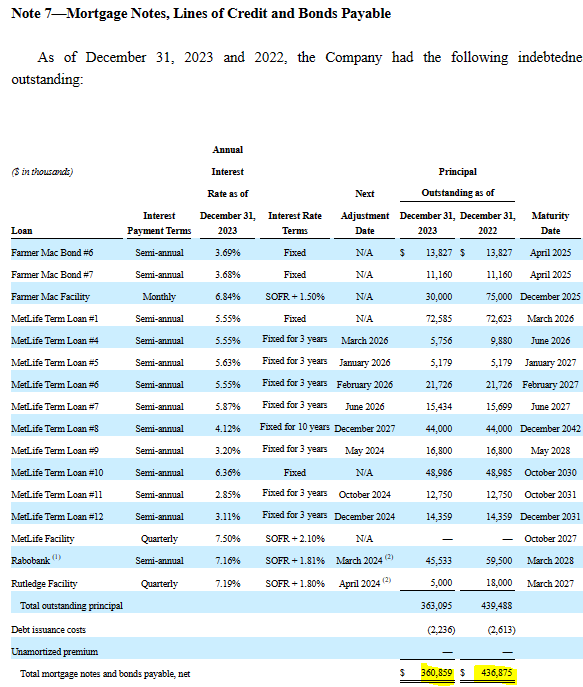

The two near term maturities are minuscule and won't make a dent if they are paid off with the credit line. But the question remains as to how we are going to catch up to NAV. It is also interesting here to note that the perpetually optimistic Wall Street Analyst community does not see NAV as significantly higher than the current stock price.

TIKR

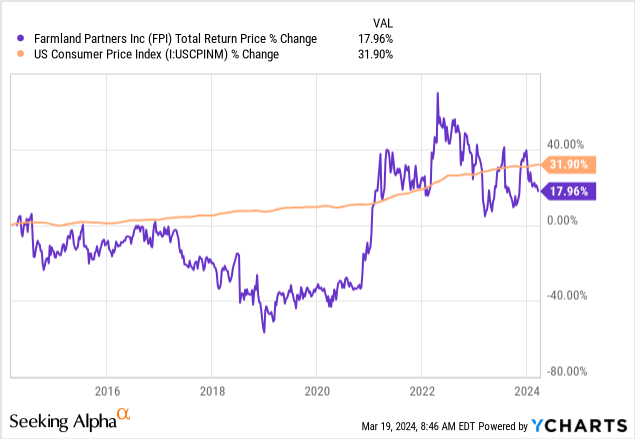

We will note here that it is hardly unusual to get this level of NAV discounts in REIT land today. You also have shorter term interest rates above 5% and it is relatively easy to reach 6% in yields without taking more than a modicum of risk. So FPI has to compete with that. The counter is that 5% and 6% interest rates cannot give you the appreciation that Farmland gives you. Well, that might be true but have a look at the NAV movement over the past decade.

TIKR

If that starting NAV compounded at 6% a year, it would be well over $30. Today the mean estimate is $13.31 and even the company likely does not believe that the NAV is more than $17.00. So the compounding never really happened and investors are rightly preferring a guaranteed 6% rate versus the lure of higher NAV.

You have T-bills offering you a decent return and you can get up to 6% or even more without taking excessive risks. For those looking for an inflation hedge Treasury Inflation Protection Securities are actually offering a solid risk-reward. FPI stands as an oddball here. If it was at a massive discount to our NAV estimates, we would take a punt. We know that value equities are at one of their cheapest levels relative to growth equities. But here, we don't think the risk-reward is well balanced, especially relative to alternatives. We are maintaining our original buy under-price with the caveat that the company could likely liquidate today for at least a 20% premium to the current market price.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.