Olivier Le Moal

Olivier Le Moal

Shares of Amicus Therapeutics (NASDAQ:FOLD) are up modestly since my September 2023 update where I argued that the limited label of Pombiliti+Opfolda may not matter for the product combination's uptake because it would have been used like the label says anyway. And while there are no real pipeline updates to look forward to, the company may attract a different kind of investor base going forward - investors predominantly focused on revenue and earnings momentum. Amicus should start delivering better revenue growth rates in the following quarters with improving operating leverage and increasing cash flows.

Global net sales of Galafold increased 17% in 2023 to $388 million and Amicus expects 2024 net sales to grow between 11% and 17% based on a constant exchange rate to $430-450 million. Galafold has been unusual from the start with the majority of global net sales coming outside the United States, initially due to it being available in Europe first and a few years later in the U.S., but U.S. sales did not really catch up.

The addressable population for Galafold is rather small and I believe Amicus has done an excellent job, capturing what it estimates is 60-65% of the Fabry population that is amenable to Galafold. As a reminder, estimates vary, but Amicus believes that 35% to 50% of the total population has mutations that make them amenable to Galafold.

The growth rates have decreased as there are fewer patients to switch from enzyme replacement therapy and growth in the future will be predominantly driven by improved diagnosis rates through screening, testing, and education, and also by geographic expansion.

Amicus still sees Galafold as a $1 billion-a-year drug by the end of the decade. While I am acknowledging this as a possibility through a combination of better-than-expected growth in the number of treated patients, faster addressable market expansion, and price increases, I expect the company to fall short of its goal as it would take very high market penetration and we would also need to assume there will not be any disruptive competition by the early or mid-2030s. Based on Amicus' market share estimates for Galafold of 60-65%, the total market today is worth between $600 million and $650 million, meaning the market would need to grow by more than 60% and Galafold's market share would need to be north of 90%.

Amicus said in early January and this week that approximately 120 Pompe disease patients were either treated with commercial product or scheduled to be treated. This does not sound like much, but it is if we consider the annual price tag over $600,000 per patient which translates to an annualized net sales run rate of approximately $70 million. However, we should be mindful of the fact that 105 patients transitioned to commercial therapy from Amicus' clinical trials and that only 15 patients are coming from competing enzyme replacement therapies, Sanofi's (SNY) Myozyme and Nexviazyme.

This is a good start, but the next few quarters should show how successful Amicus will be in switching patients from Myozyme and Nexviazyme. Interestingly, management said today that the majority of the switches in the United States are coming from Nexviazyme, Sanofi's next-generation product, which I thought was less likely to happen and I believe this is a good sign.

So far, so good for Amicus' combo and I believe it is on track to capture 20% of the global Pompe disease market by 2027 or $300-350 million in annual sales assuming the market grows from $1.3 billion in 2023 to $1.5-1.7 billion in 2027. Longer-term, Pombiliti+Opfolda could generate more than $500 million in annual net sales and bring Amicus closer to its long-term total combined annual sales projections of Galafold and Pombiliti+Opfolda of between $1.5 billion and $2 billion.

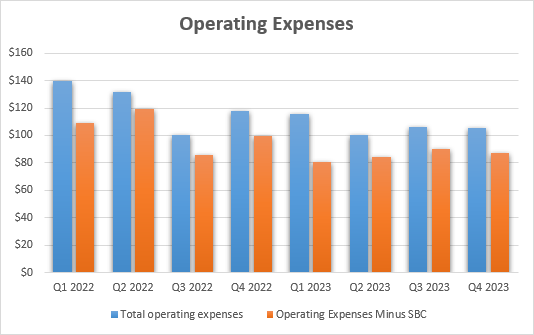

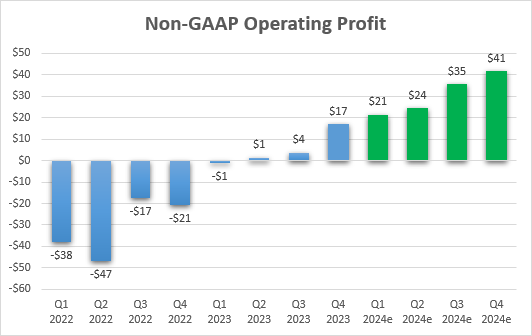

Amicus managed to reach non-GAAP profitability in Q4 2023. This was achieved through a combination of significant R&D spending cuts as the gene therapy pipeline was deprioritized and through the continued solid topline growth of Galafold, and more recently, the launch of Pombiliti+Opfolda.

Amicus Therapeutics earnings reports

Below is my estimate of what the potential non-GAAP operating profit progress could look like in 2024. Assumptions are total net sales of approximately $530 million (current analyst consensus is $535 million) and total non-GAAP expenses being $355 million which is the mid-point of the company's $345-365 million guidance range.

Amicus Therapeutics earnings reports, author's estimates and calculations

In the absence of pipeline catalysts, strong topline growth driven by the recent launch of Pombiliti+Opfolda and expanding margins are the key ingredients for potential value creation in the following quarters and years.

The key risks in the near- and medium-term are total net sales falling short of Street expectations and the company not being able to deliver on the goal of improving operating leverage. This could come as a result of Galafold's growth slowing down more than anticipated in 2024 and beyond, or Pombiliti+Opfolda not being able to capture market share in the Pompe disease market. The latter seems like a greater risk to me as Galafold is a mature product with a predictable trajectory and the outlook for Pombiliti+Opfolda is still far from certain.

The potentially increased competition is the key factor that could cause future sales to come short of expectations toward the end of the decade and in the 2030s. However, as of today, I do not see competing candidates in development that could threaten Galafold or Pombiliti+Opfolda. Gene therapy and/or gene editing candidates are a long-term threat, but it will take years before any of the candidates in development reach the market or start taking market share.

Amicus is in good financial shape with $286 million in cash and $400 million in long-term debt. If the company meets this year's growth expectations, it will become profitable and could generate more than $100 million in cash and significantly more in the following years. The debt was refinanced in October 2023 and matures in October 2029 and I do not anticipate Amicus having trouble paying back the loan in cash at the time or sooner considering the expected profit and cash flow growth in the following years.

Amicus entered 2024 with a strong revenue growth outlook and with prospects for achieving non-GAAP profitability this year. Galafold should continue to contribute with mid-teens net sales growth but the main growth driver is the Pombiliti+Opfolda combination in Pompe disease. The combination of improving margins and strong topline growth put the company in a good position to deliver shareholder value in the following quarters and years.