kasezo

kasezo

Fabrinet (NYSE:FN), is a 23-year-old business that benefits from outsourced low-volume production of highly complex products such as optical communication devices, modules, sub-systems, lasers, and sensors. These products are primarily relied on by companies based in industries such as optics, automotive, industrial, and medical.

Q2 Presentation

FN may only have a relatively small pool of customers (for instance, around ~55% of the company's business comes from just 4 customers), but don't disregard how pivotal its services are, particularly in the field of optics (80% of group revenue) where other third-party manufacturers with the requisite optical or electromechanical process capabilities are few and far between. This is exemplified by the fact that in most cases, Fabrinet serves as the only outsourced manufacturing partner for its clients.

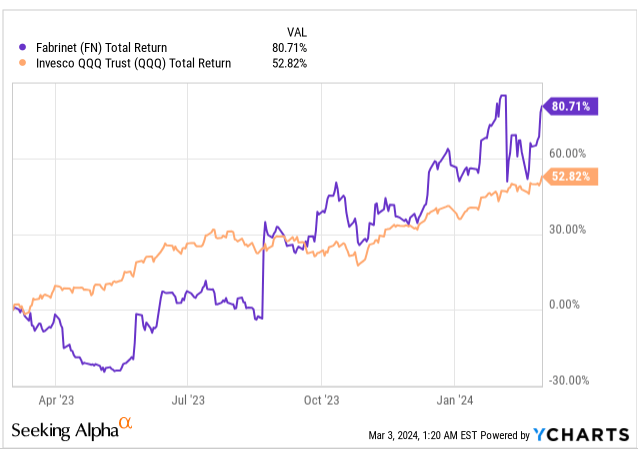

YCharts

Over the last year, the FN stock has proven to be a strong source of alpha, delivering around 80% returns, and consequently outperforming the Nasdaq (which in itself has been quite resilient) by 1.5x.

The euphoria around Fabrinet has mainly been driven by the enormous spurt in AI and what that's doing for the company's datacom revenue. In Q2-22, this only contributed $82m of sales, or just 14% of group sales. Now it is the largest contributor to group sales at over 40% or nearly $288m. The company is well-poised to ride the tailwinds here, as quite a few of the traditional products in the industry lack the necessary speed and bandwidth to support AI use cases.

Q2 Presentation

Note how FN's products with speeds of over 400-GIG have been growing at robust levels of 17-27% on a sequential basis since Q2-23 (within the +400-GIG bracket, 800-GIG programs linked to AI have witnessed a great deal of impetus off late).

Q2 Presentation

Over the last three quarters, datacom revenue has grown at a pace of well over 100% YoY (in Q2 the growth came in at 155%), but this is not sustainable, and soon the segment will have to contend with the high base effect (for Q3, the segment will have to contend with a base period where growth came in at 50% YoY). Solid positive growth will still come through, but if this segment has to keep up the same pace of triple-digit annual growth over the next few quarters, we suspect FN will need to close and announce a few follow-on program wins, something which is yet to meaningfully take place.

On the telecom side of the business, industry conditions still remain largely weak (note that FN's telecom revenues have been sliding for 5 straight quarters), but one part of the portfolio that is showing signs of life is the growing demand for 400ZR pluggable modules, which can be instrumental in reducing the cost of data center interconnects. A few quarters ago, management suggested business here would move in "stops and starts" but now they're a little more confident, describing the pipeline here as "good".

What FN does, it does rather well, but we would like to see management demonstrate better utilization of its hefty cash resources? The company no doubt deserves a great deal of credit for maintaining a solid net cash position over many years, but currently with a record amount of cash at over $0.7bn, we think there's a lot of sitting on that balance sheet. For a manufacturing company, one would expect the PPE or working capital to take up the largest chunk of assets, but in FN's case, it is the cash and liquid investments that account for 35% of the asset base.

Also note that on an FCF yield basis, the position is already quite healthy, with the stock now yielding a figure that is over its 5-year average of 3.41%. There's potential for the figure to continue to trade above its average in the short-term, as channel inventory adjustments in the telecom industry continue to take place. This has meant that inventory investments which have largely sucked out FN's cash over the years have been a useful source of cash over the past 3 quarters as the company continues to draw down its existing resources.

YCharts

All in all, considering the status quo with FN's cash position, we think a dividend ought to be considered, or strategic M&A that can maybe add an edge to their manufacturing process (since FN's comfort zone is with low-vol manufacturing, it doesn't look like they will resort to M&A that will boost its scale). The company can well deploy cash to execute buybacks to the tune of $93.6m (the current pending war chest), but given where valuations are (more on that later), one does wonder if that would be a great use of cash.

The FN stock has enjoyed its time in the sun, but at this juncture, one does wonder if things look a bit overextended.

Investing

The relative exuberance towards FN off late is well-captured in the monthly price imprints over the last seven years or so. Until July last year, FN had been trending up at a rather healthy pace, within a certain ascending channel, but in August, we saw a strong breakout candle, which was the start of a rather steep uptrend.

We're typically rather uncomfortable with commencing fresh long positions when a stock is trading close to lifetime highs after witnessing a steep uptrend, and that's what you have with FN now.

It's also worth considering that the 14-period default RSI indicator (which recently pivoted) still suggests that the stock still remains overbought.

Stockcharts

Then the chart above suggests that investors who are on the lookout for cheap rotational candidates within the growth component of the Russell 2000 index are unlikely to favor FN. As things stand, the relative strength (RS) ratio of the FN stock versus its peers from this segment is over 50% more than the mid-point of its long-term range.

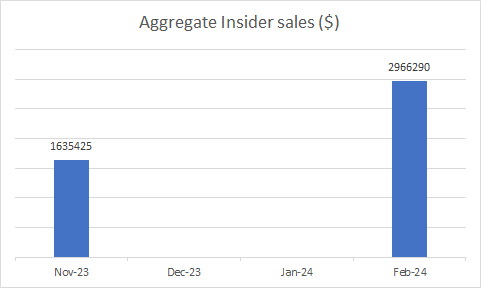

Investors may also want to take a cue from the recent shift in insider positioning. After a couple of months of dormant insider activity, we've recently seen a few insiders reduce their stake in the stock this month to the tune of $3m.

Barchart

Finally, investors should also consider that FN is not a particularly cheap stock to own. We accept that the growing importance of AI interconnects in facilitating higher data throughput and reduced latency means the FN stock may never quite trade at a discount to its 5-year P/E average, at least in the foreseeable future.

However, at 21.3x forward P/E (based on FY consensus estimates for June 2025), the current premium represents a mammoth premium of 53%, and with potentially slower implied annual earnings growth of 13% in FY25, we don't think it would be a great idea to pay that premium.

YCharts