Juanmonino/E+ via Getty Images

Juanmonino/E+ via Getty Images

1-800-FLOWERS.COM, Inc. (NASDAQ:FLWS) expects Adjusted EBITDA and FCF to be a bit better in 2024 than that in 2023. Besides, I believe that reduced labor costs, better inventory management, and new products could serve as gross profit catalysts in the coming years. In addition, FLWS does seem like a buy given that acquisitions are mainly done in cash, and debt investors also seem interested in the business model. Clearly, there are some risks out there coming from supply chain issues or goodwill impairments, however FLWS stock appears cheap at 4x cash flow.

Primarily based on an e-commerce platform for the distribution of its products, 1-800-FLOWERS operates predominantly within the United States. The products are made with flowers as part of the traditional business, to which are added customized gifts, shopping cards, or specialty cuisine among others. Among its brands, some of the best known are 1-800-Baskets, Cheryl’s Cookies, Harry & David, PersonalizationMall, and y Shari's Berries among others. Through its loyalty program, the company offers free shipping to its customers, based on its platform that allows it to take orders and fulfill shipping on the same day.

Currently, 1-800-Flowers functions via its three business segments according to the type of product it sells: flowers and floral arrangements, gourmet foods and gift baskets, and the BloomNet segment.

The first of these segments involves the core of the company's business, which includes direct-to-consumer retail stores for flowers and fruit arrangements, e-commerce platforms, and the Alice's Table brand, which provides indoor lifestyle offerings and culinary experiences throughout the country.

Within the gourmet food segment, we find specialty grocery retail distribution channels, associated e-commerce platforms, and some brands aimed at specific products such as Simply Chocolate or Shari's Berries.

Finally, in the BloomNet segment, the operations are carried out on wholesale vegetables and the distribution of products for third parties within the gift and floral arrangements market.

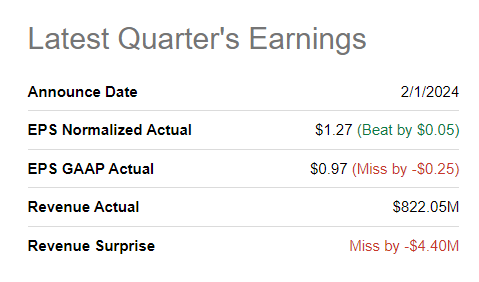

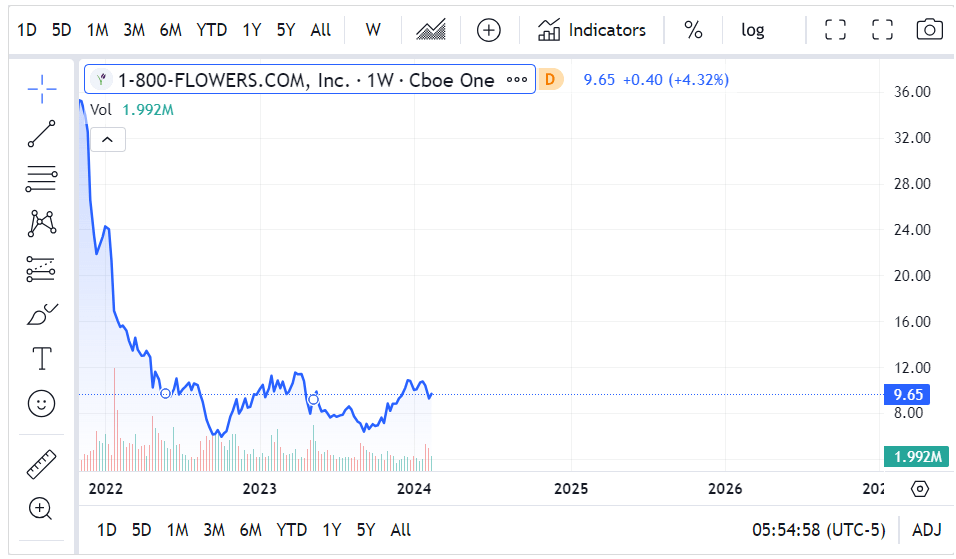

The most recent quarterly report delivered in February was lower than expected, with EPS GAAP of $0.97 and quarterly revenue of $822 million. With that, I became interested in the stock because it is trading at the lowest level seen in the last three years. The company traded at more than $30 per share in 2020, and it is now trading at less than $10 per share.

Source: Seeking Alpha

Source: Seeking Alpha

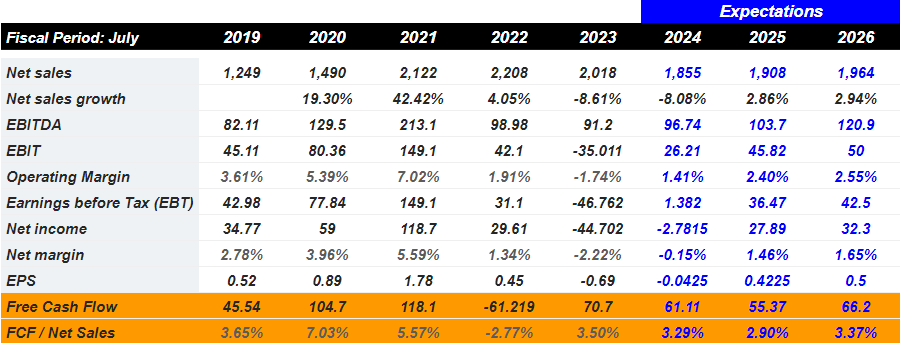

The new 2024 guidance given was, in my view, beneficial. 2024 revenue is expected to be a bit lower than that in the past. However, Adjusted EBITDA, Free Cash Flow expectations, and the gross profit margin could increase as a result of expense optimization efforts. Total revenues may decline close to 7%-9%, adjusted EBITDA may be close to $95-$100 million, and FCF is expected to be about $60-$65 million.

Expectations from other analysts are also in line with the guidance given by management. 2025 net sales are expected to be close to $1.964 billion, with 2025 EBITDA of $120 million, EBIT of $50 million, and 2025 free cash flow of about $66 million.

Source: Market Screener

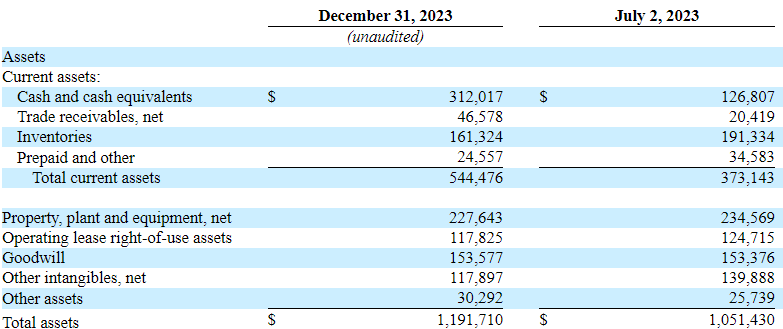

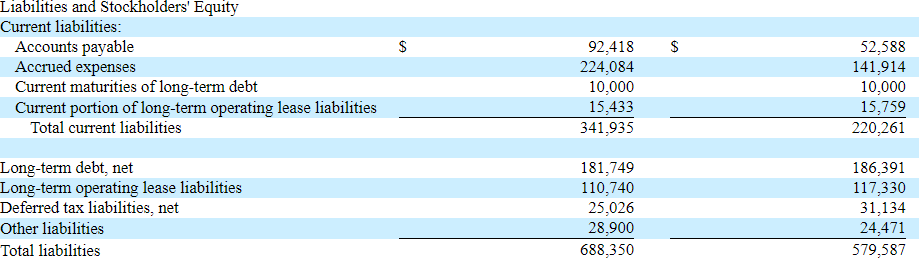

I believe that the company’s financial situation appears quite healthy. With a significant amount of cash, some inventory, and properties, the assets are financed thanks to accrued expenses, some accounts payable, and long-term debt. More in particular, cash and cash equivalents stand at close to $312 million, with trade receivables worth $46 million, inventories of about $161 million, and total current assets worth $544 million.

Also, with property, plant, and equipment of about $227 million, operating lease right-of-use assets stand at close to $117 million, goodwill is close to $153 million, and total assets stand at $1.191 billion. The asset/liability ratio is about 2x, so I do believe that the balance sheet appears in good shape.

Source: 10-Q

Accounts payable stood at about $92 million, with accrued expenses of $224 million, current maturities of long-term debt worth $10 million, and total current liabilities of about $341 million. The ratio of current assets/current liabilities is larger than 2x, so I do not really see a liquidity issue here. Long-term debt stands at about $181 million, and total liabilities are equal to $688 million.

Source: 10-Q

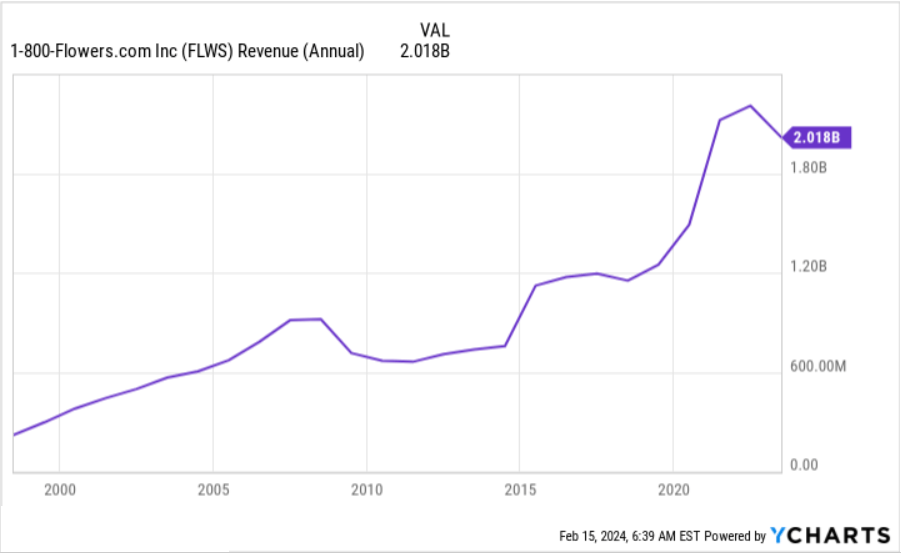

1-800-Flowers has had extraordinary results in recent times, practically doubling the size of its business and reaching 2 billion in revenue, within a market that is estimated at 130 billion by 2023. I believe that the business model works pretty well. Further internationalization, expansion into new markets, and economies of scale could accelerate FCF growth in the coming years.

Source: Ycharts

In my view, the recognition of the brand within the floral arrangements market and new successful decisions with respect to acquisitions of other businesses and investment in its electronic platforms for distribution to customers will most likely lead to net sales growth. In addition, I believe that further creation of an extensive database from the collection of user preferences and data science could be net revenue catalysts.

Besides, further expansion of the company’s online offering and improvement of logistics that allows it to deliver products the same day could bring economies of scale and FCF margin growth. Moreover, I believe that the improvement of the online platform along with the launch of new high-end brands and the improvement of its marketing and customer loyalty strategies could also represent net sales catalysts.

Net sales growth in the last part of 2023 was not positive. However, in the last quarter, the company made a reference about several efforts and events that could bring back profitability in 2024 and 2025. In particular, lower freight costs, reduced labor costs, and inventory management efforts could serve as gross profit catalysts.

Gross profit percentage increased 230 and 280 basis points during the three and six months ended December 31, 2023, respectively, compared to the same periods of the prior year, driven by lower freight costs, a decline in certain commodity costs, reduced labor costs, and better inventory management. Source: 10-Q

Given the current balance sheet and cash in hand, I believe that we could expect new acquisitions in the coming years. As a result, total net sales growth may be a bit better than expected. In addition, it is worth noting that acquisitions that were completed in 2023 were made in cash. The company did not use its own shares to buy companies. With this in mind, in my view, management may be thinking that its shares are cheap. The companies that trade at expensive valuation tend to use their own shares to buy competitors.

The Company completed its acquisition of certain assets of the Things Remembered brand, a provider of personalized gifts, whose operations have been integrated within the PersonalizationMall brand, in the Consumer Floral & Gifts segment. The Company used cash on hand to fund the $5.0 million purchase, which included intellectual property, customer list, certain inventory, and equipment. Source: 10-Q

In 2023, the company successfully signed a debt agreement with JPMorgan (JPM), which I believe may be celebrated by market participants. The agreements included a maturity date of around June 27, 2028. In my opinion, equity market participants may be a bit more interested in the company as soon as they see that debt holders are offering financing to the company. As a result, I believe that we could see an increase in the stock demand.

On June 27, 2023, the Company, certain of its U.S. subsidiaries, the lenders party thereto and JPMorgan Chase Bank, N.A., as Administrative Agent entered into a Third Amended and Restated Credit Agreement. The Third Amended Credit Agreement amends and restates the Company’s Second Amended and Restated Credit Agreement, dated as of May 31, 2019. The Third Amended Credit Agreement, among other modifications: increases the amount of the outstanding term loan from approximately $150 million to $200 million, decreases the amount of the commitments in respect of the revolving credit facility from $250 million to $225 million subject to a seasonal reduction to an aggregate amount of $125 million for the period from January 1 to August 1, extends the maturity date of the outstanding term loan and the revolving credit facilities by approximately 48 months to June 27, 2028, and increases the applicable interest rate margins for SOFR and base rate loans by 25 basis points. Source: 10-Q

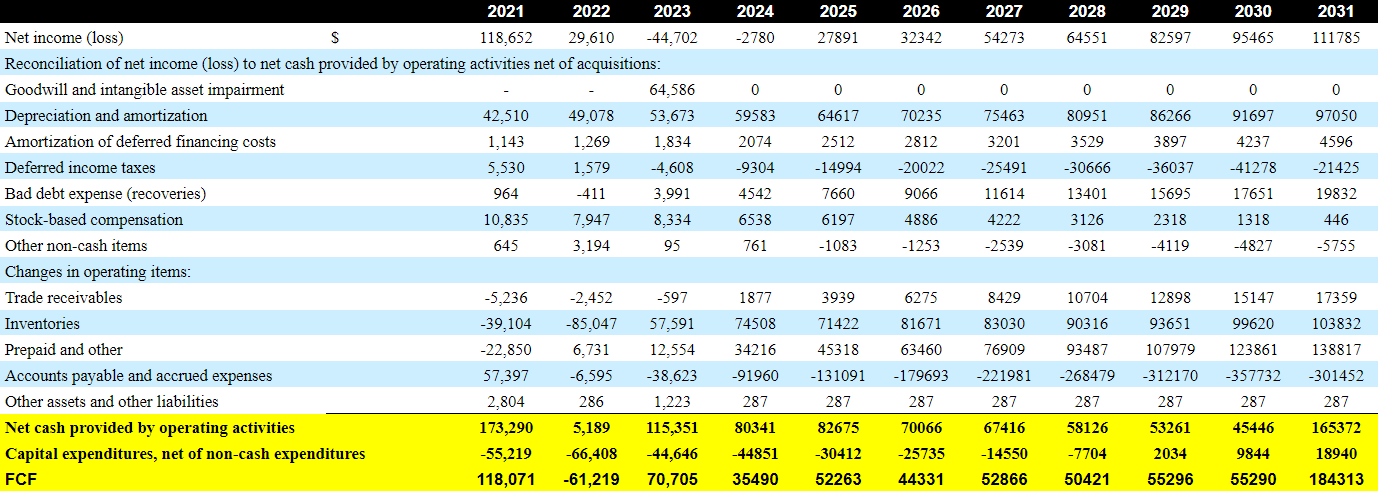

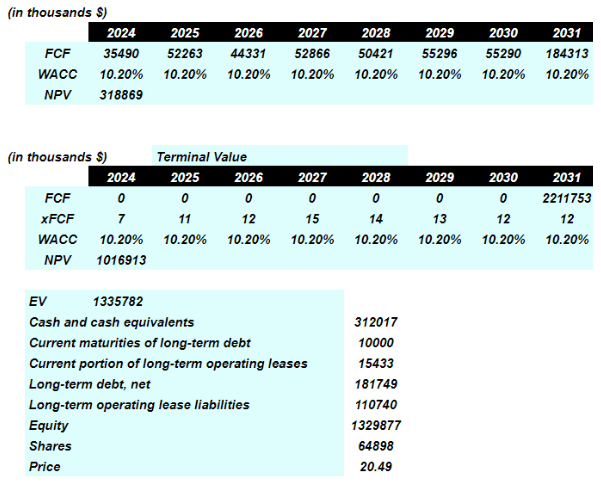

My cash flow expectations include 2031 net income of about $111 million, with the following reconciliation of net income to net cash provided by operating activities net of acquisitions. First, I assumed depreciation and amortization of about $97 million, with amortization of deferred financing costs worth $4 million, deferred income taxes close to -$22 million, bad debt expense of about $19 million, and changes in trade receivables of $17 million.

Additionally, with changes in inventories of close to $103 million and changes in accounts payable and accrued expenses of -$302 million, I obtained net cash provided by operating activities worth $165 million. Finally, if we also include capital expenditures of $18 million, 2031 FCF would be $184 million.

Source: Author's Work

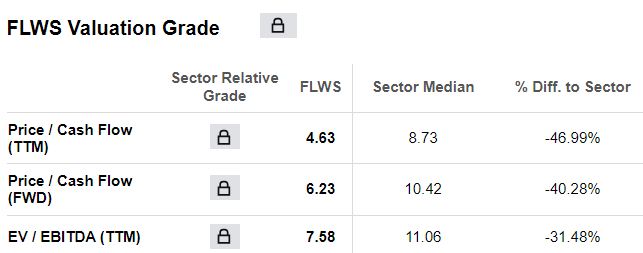

With the previous assumptions, I also included a WACC of 10.2%, which is in line with the cost of capital included by other investors. Besides, I assumed an EV/FCF of 12x, which, I believe, is a conservative exit multiple, and is in line with the valuation of other competitors. Note that FLWS appears a bit undervalued as compared to the peer group depicted by Seeking Alpha.

Source: Seeking Alpha

My results include a potential valuation of $1.3 billion, including debt, equity valuation of $1.3 billion, and an implied fair price of about $19-$20 per share.

Source: Author's Work

Despite being one of the most recognized brands in its field, the company receives competition from other businesses in the flower and gift market, as well as product offerings on electronic platforms. In this sense, many companies allocate larger amounts to the development of the offer or adopt more aggressive pricing strategies than the company.

On the other hand, within the floral market, there are a large number of independent retail stores, flower stores within supermarkets or general retail chains, and lifestyle brands within which the most products are found in some cases. The specific e-commerce platforms for these products can also be added to this list.

In a general framework, there are collection risks from the point of view of a reduction in sales due to an economic crisis that prevents consumers from accessing the company's products. For this reason, in the last year, 1-800-Flowers developed a cost reduction strategy, which may not be effective, and may not be able to prevent the company from amortizing the entirety of this reduction if it continues through 2024.

In particular, regarding its logistics, any disruption in the supply chain could generate complications in the delivery of its products, especially if we consider that a large part of these supplies comes from imports and it is still uncertain if there will be changes in the regulations of these movements due to part of the United States government in the short term.

In the future, the company's expectations are to continue with the accelerated growth it achieved in recent years, and of course, this depends on outside actors and the ability to integrate acquisitions or develop successful outreach strategies to expand its operations. In the last quarter, the company included impairment as the discount rate assumed for one of the acquisitions. I believe that we could see new goodwill impairments in the near future, which may lower the book value per share and future net sales expectations.

During the quarter ended December 31, 2023, as a result of a decline in the actual and projected revenue for the Company’s PersonalizationMall tradename, as well as a higher discount rate resulting from the higher interest rate environment, the Company determined that an impairment assessment was required for this tradename. Source: 10-Q

1-800-FLOWERS provided a beneficial 2024 guidance in terms of Adjusted EBITDA and FCF. Besides, I believe that reduced labor costs, better inventory management, and new products could serve as gross profit catalysts in the coming years as they were at the end of 2023. Putting everything together with the recent debt agreements and the fact that acquisitions are being made in cash, I believe that 1-800-FLOWERS does show significant upside potential in the stock price. Yes, there are risks out there coming from goodwill impairments, supply chain issues, or failed M&A efforts, however 1-800-FLOWERS does trade cheap.