carlosgaw

carlosgaw

My investment thesis for Flowers Foods (NYSE:FLO) relies on two core principles: firstly, the company's performance within its industry, particularly regarding gross margins; and secondly, the discrepancy between its current stock price and its intrinsic value. To verify the dissonance between the current price and the intrinsic value, I used two different growth rates that I believe are conservative.

Therefore, when I look at Flowers' margins, especially in terms of its gross margin, a possible resilience is evident in a scenario of abrupt cost increases, and this seems to be an intrinsic characteristic of Flowers that distinguishes it from the other companies I analyzed.

My thesis is based on the premise that if Flowers' operational efficiency has historically been driven by optimal cost management, then I anticipate corresponding management of SG&A expenses along similar lines in the coming years, thus expecting an improvement in this aspect in the future.

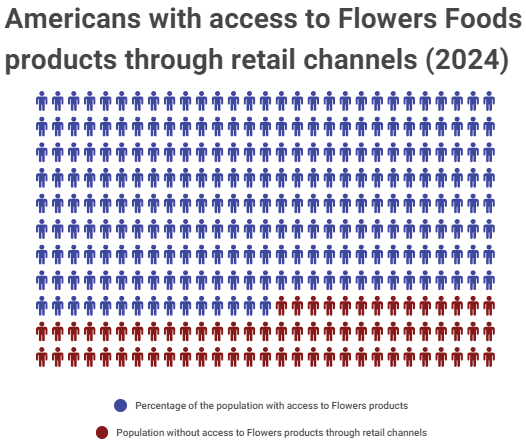

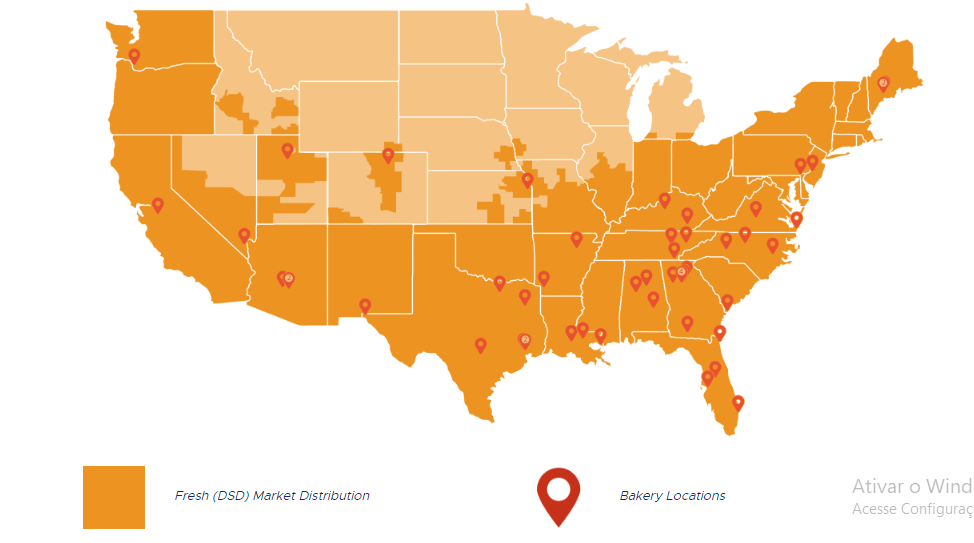

Flowers Foods is a bakery company that has been operating and is considered one of the largest companies in the industry. Flowers has 46 bakeries spread across much of the country, especially on the East Coast. Flowers distributes its products through direct retail channels to approximately 85% of the United States population.

Americans with access to Flowers products through retail channels (Author) Geographic distribution of Flowers factories and their geographic reach (Flowers Foods)

Still on distribution, it is worth highlighting that since 1984 direct-store-delivery - a business model that has been developed in the bakery sector since the 1950s in which the company supplies Independent Distributors (IDs) the exclusive right to sell and distribute Flowers brand products to companies requesting the DsD service located within a defined geographic area or areas. Flowers offers ID's its products at reduced prices so that they can be sold to customers in its geographic area of operation. The company is exempt from any sales expenses that may occur with the operation of the IDs, which are the responsibility of its executor.

The model operates successfully nationwide, but Flowers recently encountered issues in California, necessitating the repurchase of previously granted rights to independent distributors (IDs). In the third quarter, Flowers incurred a loss of $46.73 million, primarily due to $137 million allocated for legal settlements and litigation expenses linked to resolving class action lawsuits involving California distributors.

Due to these issues, Flowers will need to implement an exceptional distribution system in the state of California for the year 2024 in which the company will own distribution system and will no longer use DsD. National distribution will continue in the same way as before, but investors must be aware of the precedents that this decision could set.

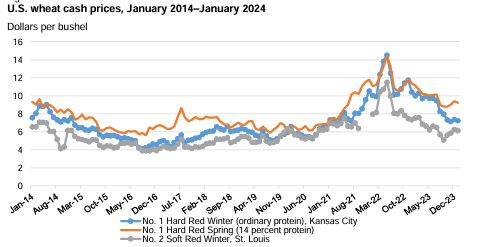

Flowers Foods uses a variety of raw materials to create its product line. Mainly, expenses linked to its operations (in addition to expenses with capital goods and the like) revolve around the acquisition of agricultural products of national origin, whenever viable and beneficial. These commodities include staple foods such as eggs, wheat, sugar and a range of other essential ingredients. Therefore, variations in the prices of agricultural commodities directly impact Flowers Foods' production costs.

Wheat price over the years (USDA)

Many market analysts don't anticipate a sudden surge in wheat prices unless there's a geopolitical conflict causing disruptions in the supply chain. Stocks are predicted to remain near their lowest point in a decade, partly due to decreasing domestic demand influenced by shifting consumer preferences and dietary trends. However, wheat consumption typically shows consistent long-term patterns.

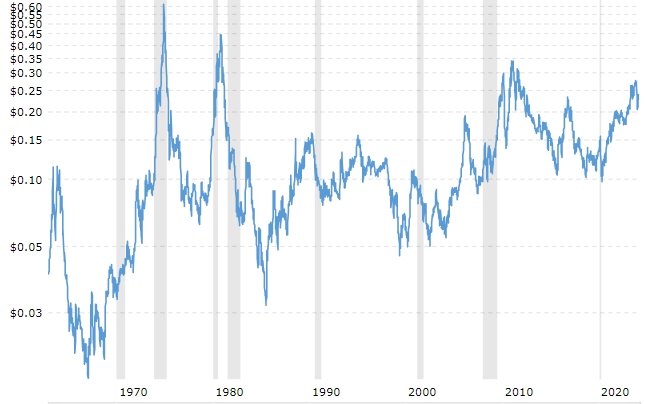

The price of sugar is at less favorable levels, rising almost 70% since the beginning of 2019. With an anticipated decrease in supply this year, combined with factors affecting sugar production in India and Brazil, we may expect some price increases for sugar. However, Flowers Foods has demonstrated its ability to manage such challenges effectively, as seen during previous peak periods in 2016 and 2020.

Sugar price over the years (Macrotrends)

Flowers has several brands, including some that it operates independently and others where it has the right to sell through franchises. Examples of brands that Flowers has the rights to trade include well-known names such as Little Miss Sunbeam, Sunbeam's own brand and Bunny Bread.

Flowers' own brands include Nature's Own (fresh breads, buns, and rolls), Dave's Killer Bread (organic bread), Canyon Bakehouse (gluten-free breads, bagels, buns, and English muffins), Wonder (loaf bread, buns, rolls and muffins), Tastycake (snack cakes, pies, and donuts), Mrs. Freshey's (sweet treats), Merita (breads and buns), Captain John Derst's (Captain John Derst's Old Fashioned Bread and other baked goods), Evangeline Maid (buns, rolls and loafs), European Bakers (breads, buns, and rolls), Butternut (Butternut breads), Mi Casa (quesadillas, fajitas, burritos and enchiladas) and Homepride (breads).

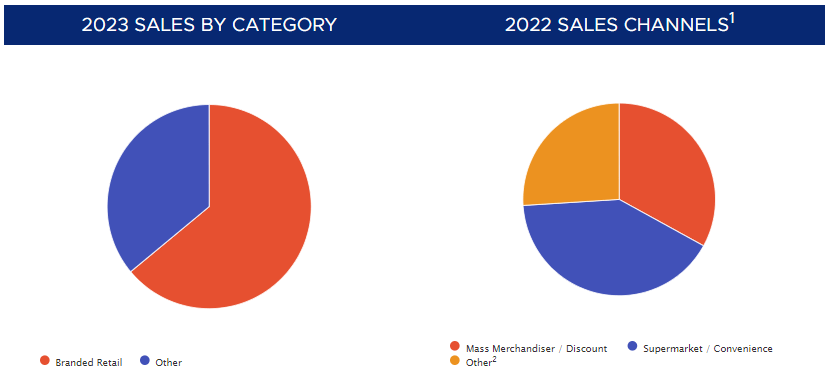

Some brands that belong to or that Flowers has the right to market (Flowers Foods) Compiled sales data and their respective transmission channels (Flowers Foods)

Sales are evenly distributed across multiple sales channels, indicating that Flowers does not rely heavily on any single channel for its customer base and maintains a healthy mix for achieving sales in a potentially congested sales environment.

I will begin my analysis by investigating the proportion of own resources and third-party resources in the composition of Flowers Foods' capital, as well as evaluating the degree of immobilization of these two types of capital.

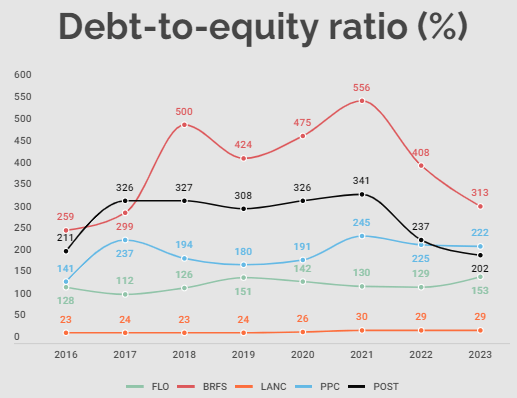

Debt-to-equity ratio of the companies analyzed (Author)

Flowers Foods' debt-to-equity ratio has fluctuated between 128% and 153% since 2016, indicating changes in its leverage over time. Notably, in 2023, there seems to be an upward trend in the composition of debt within the company's capital structure.

Hence, it can be inferred that as the debt-to-equity ratio increased, the company's reliance on third-party capital also grew, consequently amplifying its dependence on allocation decisions, particularly with respect to working capital. Although significant, Flowers Foods' reliance on external capital is not among the highest in its sector, as illustrated in the preceding graph.

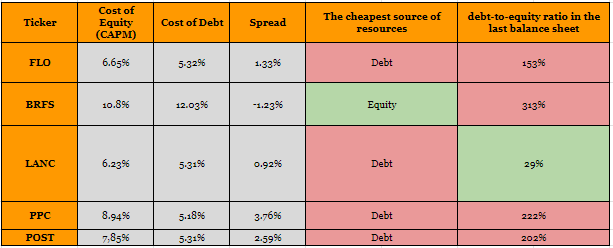

Table that summarizes the cost of capital of the companies analyzed (Author)

Critical factors in fundamental analysis that need to be analyzed at Flowers Foods are:

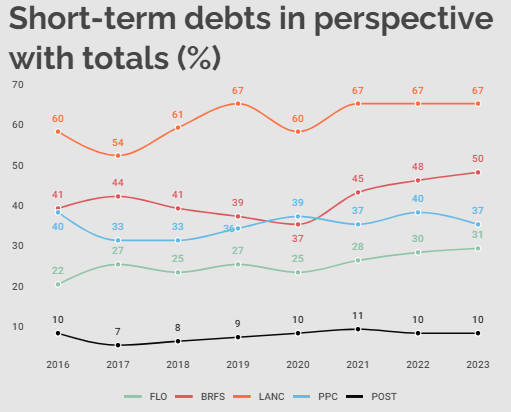

That said, let's analyze the debt profile by looking at the debt composition of Flowers and its peers:

Amount of short-term debt in perspective with the total (Author)

Flowers Foods' debt profile remains healthy, though its long-term debt is growing faster than short-term debt, indicating increased reliance on third-party capital for long-term asset immobilization.

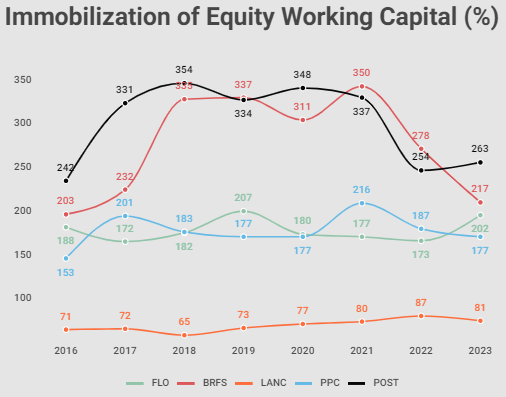

Regarding asset immobilization, which represents Flowers' investment in fixed assets, let's assess the financial "slack" using the equity working capital, which is the portion of equity invested in current assets. This analysis will determine if Flowers Foods requires loans for working capital by measuring asset immobilization.

Immobilization of Equity in perspective with the other companies analyzed (Author)

Lancaster (LANC) stands out as the sole company maintaining its own working capital. In contrast, all other analyzed companies have fully immobilized their internal resources and continue to depend significantly on third-party capital for their working capital needs. Hence, it's imperative to acknowledge Flowers Foods' reliance on acquiring debt to manage its working capital, particularly amidst a scenario of consumer spending constraints resulting from contractionary monetary policies.

The structural levels of Flowers' immobilization are not healthy, and this is where I begin to highlight the structural problems that Flowers suffers from. To spin one's wheels, Flowers will need a continuous restructuring of its loans for cash management and the amortization of permanent asset debts.

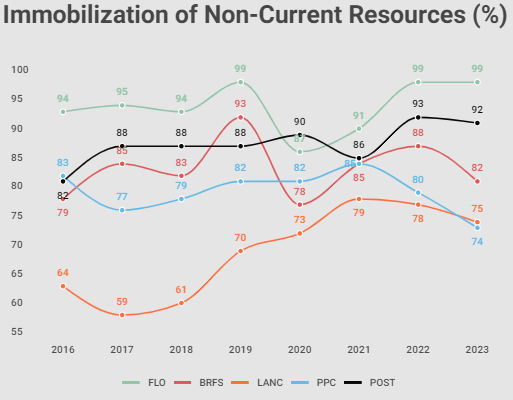

Immobilization of non-current resources in perspective with other companies analyzed (Author)

Among the companies analyzed, Flowers Foods exhibits the poorest index. The position of having 99% of its non-current resources allocated to fixed assets leads the company to maintain only 1% of these same resources for current assets.

This means that the company has already tied up resources greater than its equity (202% bigger), with this excess being financed by long-term liabilities, which alone had to cover its net working capital. Flowers finds itself with just $28 million in net working capital. It is a dependency that is not healthy in the long term, since the equity will not need to be paid (I say paid, not remunerated), but the liabilities will.

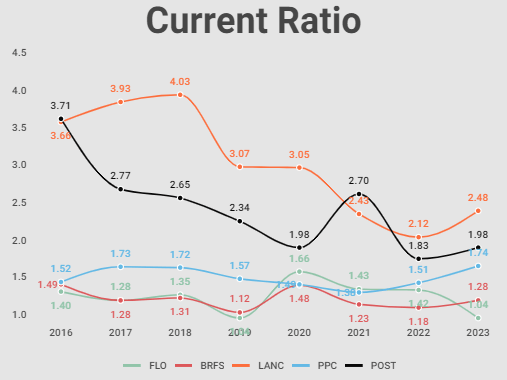

Now, let's take a look at Flowers Foods' liquidity ratios.

Current Ratio of the companies analyzed (Author)

Flowers has enough current assets to cover its current liabilities (and is consequently solvent with its short-term obligations) and still maintains a margin of just 4%. Let's look at the deterioration of Flowers' short-term solvency, which in 2023 is at alarming levels. Given that current liquidity essentially reflects the margin of maneuverability for balancing the inflow and outflow of an entity's resources, it can be inferred that Flowers Foods is currently experiencing a period of rigidity in managing these flows.

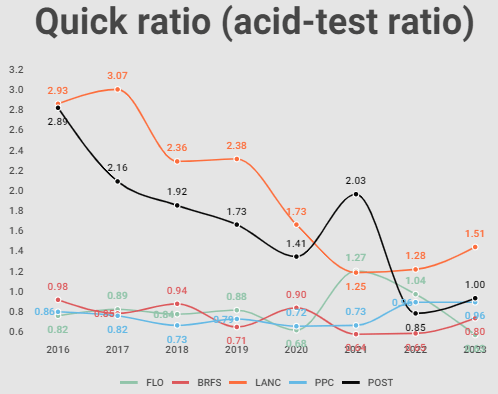

Quick ratio in perspective with other companies (Author) Table condensing and evaluating liquidity data (Author)

Based on the empirical analysis of liquidity indicators, it is evident that Flowers Foods is facing challenges in liquidity management, as its liquidity metrics consistently underperform those of its peers in the sector. And this is mainly due to the lack of net working capital, since the company has already immobilized all of its own capital and a large part of its non-current resources. As fixed assets are very little liquid and still suffer variations in realizable value due to selling expenses and other problems, Flowers has a small portion of net working capital, which it raised from non-current resources acquired from long-term debts.

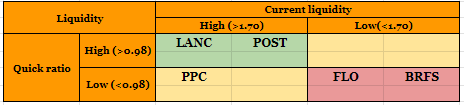

Asset turnover in perspective with the sector (Author)

From what the asset turnover indicates, Flowers Foods is at accommodative levels in the transfiguration of the invested capital materialized in the assets for improvements in its revenue.

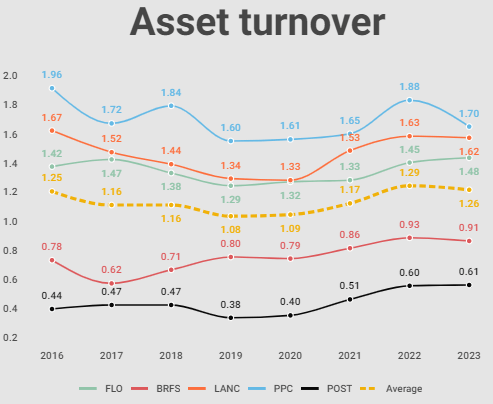

gross margin in perspective: this is where Flowers stands out most (Author)

Despite the weakness of liquidity indices and vulnerable capital structure, highly dependent on third-party capital and with little margin to finance its commercial operations (see net working capital, practically all fixed assets and own capital, all fixed assets), the company maintains a parameterization excellent COGS, far above the sector.

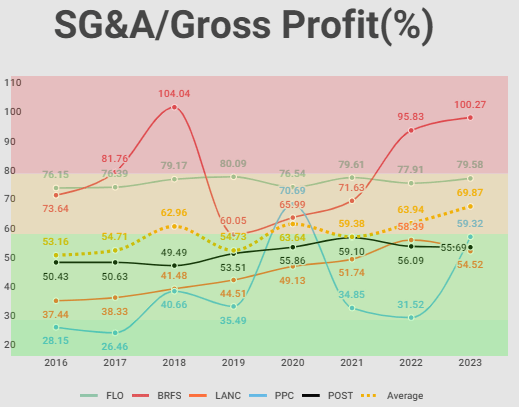

Percentage of gross profit that each company allocates to SG&A (Author)

Flowers Foods' SG&A expenses, in comparison to its gross profit, consistently exceed the industry average by roughly 15% annually. When employing our benchmark to gauge optimal levels for stock selection, Flowers Foods exhibits SG&A expense multiples that hover around the least favorable end, reaching up to 80%.

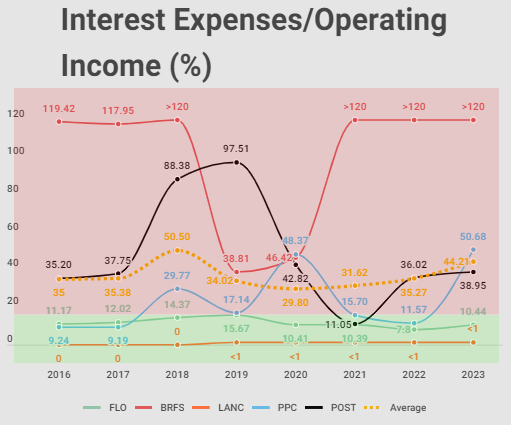

Percentage of Operating Profit/Loss that each company spends on Interest Expenses (Author)

The debt service performance of Flowers Foods suggests that the company effectively manages its interest payments relative to its operating income, maintaining levels that are notably more favorable compared to industry norms.

Flowers Foods' average net margin sits at approximately 3.90%, which is roughly 0.5% higher than the sector average. However, when compared to significantly healthier companies like Lancaster, which boasts an average net margin of 8.80%, Flowers Foods does not stand out. It's crucial to note that none of the analyzed companies exhibit net margins that I would consider robust, which would typically be multiples above 20%.

Net Margin in perspective with other companies in the sector (Author)

In 2023, Flowers Foods achieved a return on assets of 3.6%, slightly surpassing the sector average. However, recent quarters have shown a deterioration, attributed to the increase in fixed assets and a decline in net profit since 2022.

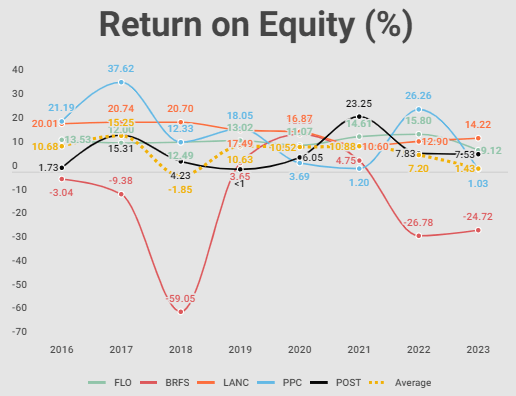

Return on Equity compared to other companies in the sector (Author)

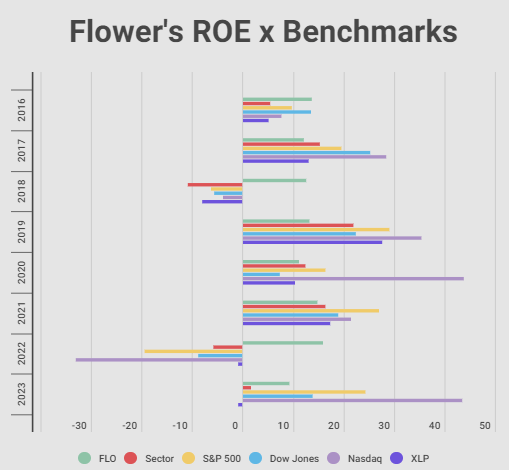

Flowers Foods' equity return rate averages 12.95%. Generally in the Consumer Staples sector, a return on equity of 8% on average is observed. Some other returns can be used as benchmarks to make a comparison between the return on invested capital for comparison purposes.

Was the return on equity worth it? The graph compares profitability with important benchmarks (Author)

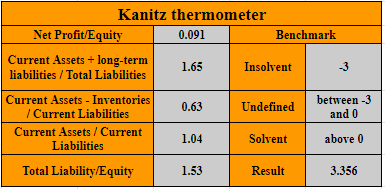

When analyzing the financial situation of Flowers Foods and assessing the risk of bankruptcy, the Kanitz model will be applied. This model is recognized for its effectiveness in predicting bankruptcies and has approximately 80% accuracy in detecting solvent companies and 68% of insolvent companies.

Kanitz model for bankruptcy prediction (Author) Result of the Kanitz model for each company analyzed: all out of danger (Author)

According to our quantitative model for bankruptcy prediction, Flowers Foods does not appear to be at risk of bankruptcy, as well as all the companies in the sector analyzed.

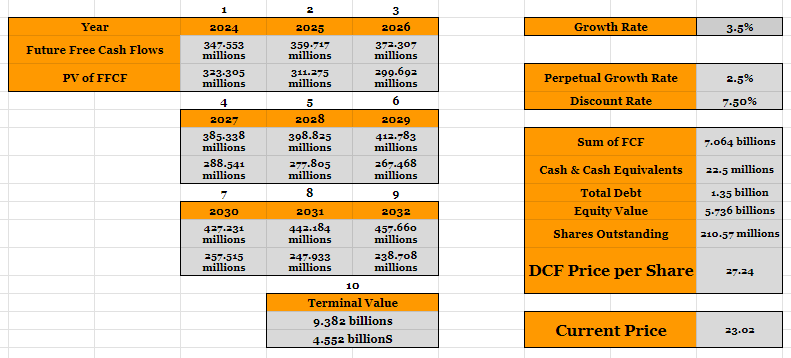

First, I will use our discounted cash flow model to assess the intrinsic value of Flowers Foods.

Flowers' Cost of Equity, determined by the formula Risk-Free Rate plus Beta multiplied by ERP, is currently at 7.5%. With a Beta of 0.69, reflecting the stock's volatility compared to the market, and the current Risk-Free Rate standing at 4.35% based on government bond yields, along with an ERP of 4.57% representing the additional return investors demand over the risk-free rate, the Cost of Equity for Flowers Foods is 7.5%.

DCF Model to find the intrinsic value of Flowers Foods (Author)

Using a growth rate (g) of 3.50%, which is in line with the projected EBITDA growth for the future, an intrinsic value of $27.24 per share is obtained, this means that at current levels, Flowers Foods' shares are being sold at almost 20% discount in relation to its intrinsic value.

Based on the insights from analysts covering Flowers Foods, it appears that they are projecting a growth rate for the stock at approximately 4.5%, which is slightly more optimistic compared to my own projections. Out of curiosity, using the projected growth of 4.5%, an intrinsic value of $29.76 is obtained. That's a discount of almost 30% from its current value.

Also, out of curiosity, the implicit (or embedded) growth rate for Flowers Foods is approximately 1.65%, that is, the market is pricing Flowers to have this growth in the coming years according to pricing movements.

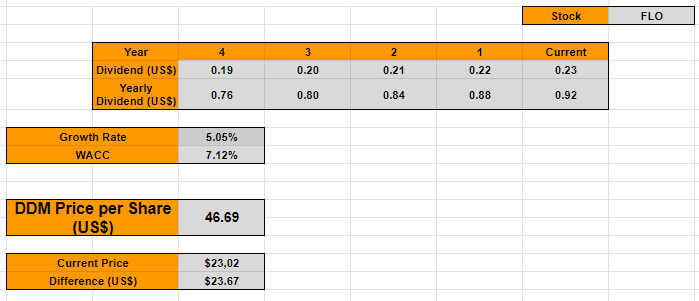

Discounted Dividend Model to find the intrinsic value of Flowers (Author)

When I use the Discounted Dividend Model, I find an intrinsic value of $46.69, which is $23.67 above the current share price. To realize this result, I rely on dividend growth in line with the last five years (approximately 5.05%) and with the WACC of 7.12%.

So, according to the valuation methods used, I came to the conclusion that Flowers Foods is undervalued and that given the price levels and growth prospects, the moment opens up a very pleasant buying window for the value investor.

I will list below some critical points in our thesis, which, despite my Buy recommendation, are still factors to take into consideration before buying the stock in question.

1. Operational rigidity resulting from low net working capital: As previously discussed, one of the main risks regarding my Buy thesis for Flowers Foods is the operational rigidity resulting from the immobilization of non-current resources. As the company has immobilized all of its own capital and most of its net working capital, Flowers has approximately 28 million to manage its current assets. Flowers Foods' operational rigidities may limit its ability to quickly adapt to market changes, reducing its operational efficiency and negatively affecting its future growth.

2. Recent deterioration in liquidity ratios: In the last year, due to weaker results and, mainly, the deterioration of current assets due to acquisition operations paid with money, and the constant immobilization of resources, there was a more evident dissonance between liabilities and assets. Additionally, the company is constantly refinancing its debt. In 2023, Flowers issued 892.2 million dollars to settle long-term obligations of 744.8 million. With the remaining 147 million, the company focused on repurchasing approximately 32.36% more common shares than in 2022. All of these operations drained Flowers' cash. Therefore, the risk here is related to the company's liquidity status in the face of a possible economic contraction.

3. SG&A exceeds the mark I consider acceptable: As seen previously, despite Flowers maintaining an excellent parameterization of COGS in relation to Revenue, and maintaining an exceptional gross profit margin (both for its sector and companies in general) of 48%-50% for approximately ten uninterrupted years. The company has SG&A expenses compared to its gross profit at perilous levels. Here our concern is Flowers' ability to maintain market share without using this gigantic capital allocation, this may indicate that Flowers is "buying" some type of competitive advantage through high SG&A expenses. I would like to see a reduction in these expenses to increase the net margin. It would be a risk to our thesis if the company needed more and more capital allocated to SG&A.

4- The restructuring of the distribution model in California and the legal precedents that this action could cause: There will be pressure on costs due to the restructuring of the distribution model in California and the West Coast as a whole. Any and all changes affect the company's operability and can put upward pressure on margins, but in the long term these costs should decrease. What concerns me most here is the precedent this decision could cause if other distributors file lawsuits against Flowers and the company has to remodel its entire distribution system.

Flowers is a company that has several brands, a strong position in the market and, according to my quantitative models, is undervalued, presenting a good window for purchase.

Of course, the company has its problems with debt, liquidity, very high SG&A allocations and problems with its distribution model, but in my opinion, most of these problems are temporary and will be resolved in the long term. It has been demonstrated that the company is not at risk of bankruptcy, has excellent operating margins to withstand a change in commodity prices and pays safe and stable dividends.