Ingenious Buddy/iStock via Getty Images

Ingenious Buddy/iStock via Getty Images

First Horizon Corporation (NYSE:FHN), founded in 1864, and headquartered in Memphis, Tennessee, provides banking solutions to consumers, businesses, financial institutions, and governments.

This conservatively capitalized company has a well-diversified portfolio and its business has performed well in both the short and long term. Not only are its common shares trading at a very modest premium to book and low price level against its EPS, but the dividend profile seems attractive.

However, investors may also want to consider its Non-Cumulative Perpetual Preferred Stock, Series F (NYSE:FHN.PR.F) which offers a higher yield and is being offered at a significant discount right now.

10-K

At the close of 2023, First Horizon's subsidiaries had a network exceeding 450 business locations spread across 24 states. Specifically, the company concluded the year with 415 retail banking centers operating in 12 states. Furthermore, First Horizon has over 50 client-service offices that are focused on providing fixed-income, home mortgage, wealth management, and commercial loan services.

Lending is the most important revenue stream for the company. Primarily concentrated in commercial lending, First Horizon categorizes its loans into two main types: commercial and consumer, each further segmented into distinct portfolios.

The three primary portfolios include unsecured commercial, financial, and industrial ("C&I") loans; secured commercial real estate ("CRE") loans; and secured consumer real estate loans. Additionally, a fourth portfolio consists of consumer credit card and other consumer debt. As you can see below, commercial loans constitute the majority of the portfolio, and they are more exposed to C&I sectors than CRE:

10-K

Notably, a significant proportion of loans originate from five key states: Florida, Tennessee, Texas, North Carolina, and Louisiana:

10-K

It's also well-diversified based on the industries its commercial customers come from:

10-K

In 2023, First Horizon achieved significant growth with some expected deterioration in the credit quality of its portfolio. Let's take things from the start.

Deposits reached $65.78 billion, marking a solid 3.61% YoY growth. The loan portfolio reached $61.29 billion, showcasing a 5.49% YoY increase. At the same time, its loans with a Special Mention rating increased by 39.63% and those with a Substandard rating rose by 49.15%. Moreover, non-performing loans increased by 46.08% and credit loss provisions were 173.68% higher than they were at the year-end of 2022. Meanwhile, net charge-offs grew by 188.14%. While these are important changes to note when reviewing the performance, keep in mind they don't pose a solvency concern as we'll see in a bit.

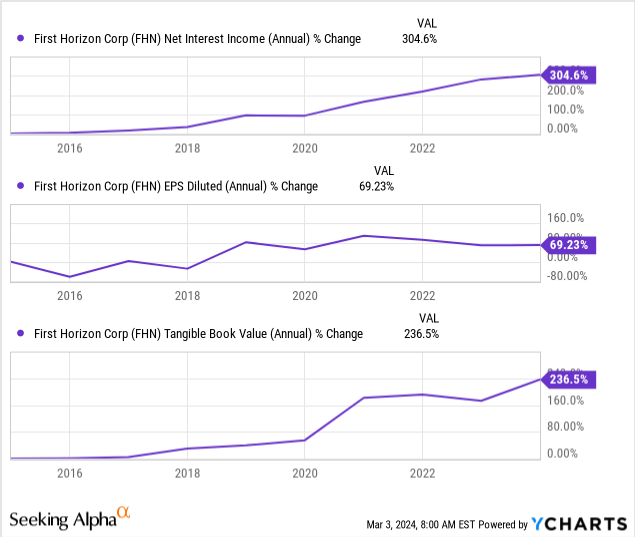

Turning to profitability, revenue surged by 52.81% YoY, reaching $4.1 billion. Additionally, net interest income experienced a YoY growth of 6.19%, reaching $2.54 billion and non-interest income grew by 13.74% on a YoY basis.

However, net income remained steady with a marginal increase of 0.44%; the same applied to diluted EPS which increased by 0.65%. Net interest margin expanded by 33 bps to 3.42%.

Regarding 2024, now, management has provided some guidance that reflects even more growth regarding net interest income based on assumptions related to balance sheet growth and some rate cuts, but higher noninterest expenses and net charge-offs:

Investor Presentation

Last, I always want to see how the performance looks using a long-term period when I first cover a company and it seems that First Horizon has experienced substantial and steady growth in its profitability and equity over the last 10 years:

In 2023, the company marked YoY improvements in all its capital adequacy ratios, surpassing the highest capital requirements for being considered "well capitalized" under Basel III regulatory standards.

The Common Equity Tier 1 (CET 1) ratio increased to 11.4%, up by 123 bps from the previous year, well-exceeding the minimum regulatory requirement of 6.5%.

The Tier 1 Capital ratio rose to 12.42%, a YoY increase of 50 bps and much higher than the regulatory threshold of 8%.

The Total Capital ratio reached 13.96%, up by 63 bps, surpassing the regulatory requirement of 10%.

The Tier 1 Leverage ratio climbed to 10.69%, marking a 33 bps increase from the previous year, also well above the regulatory minimum of 5%.

We could say that the company is more than well-capitalized. However, there are some things that investors should monitor. First, the LDR increased by 100 basis points to 93%. While this is a relatively attractive level right now, the portfolio's potential deterioration may narrow the margin of safety if deposit growth doesn't manage to offset it. Here are some changes that I believe to be important in regard to that:

The percentage of loans with a Special Mention and Substandard rating rose by 33 bps to 1.07%, and 21 bps to 0.76%, respectively.

The non-performing loans ratio increased by 25 basis points to 0.4%.

Credit loss provisions as a percentage of the loan portfolio reached 0.26%, an increase of 17 bps.

The net charge-off ratio increased by 201 basis points to 6.23%.

So, while the solvency profile looks good, because of the uncertainty of the times we're in, investors should keep a close eye on things that could significantly impact the credit quality over time. One of them is the net charge-off ratio which reflects a substantial increase in a relatively short period and which as we saw above is expected to keep increasing in 2024.

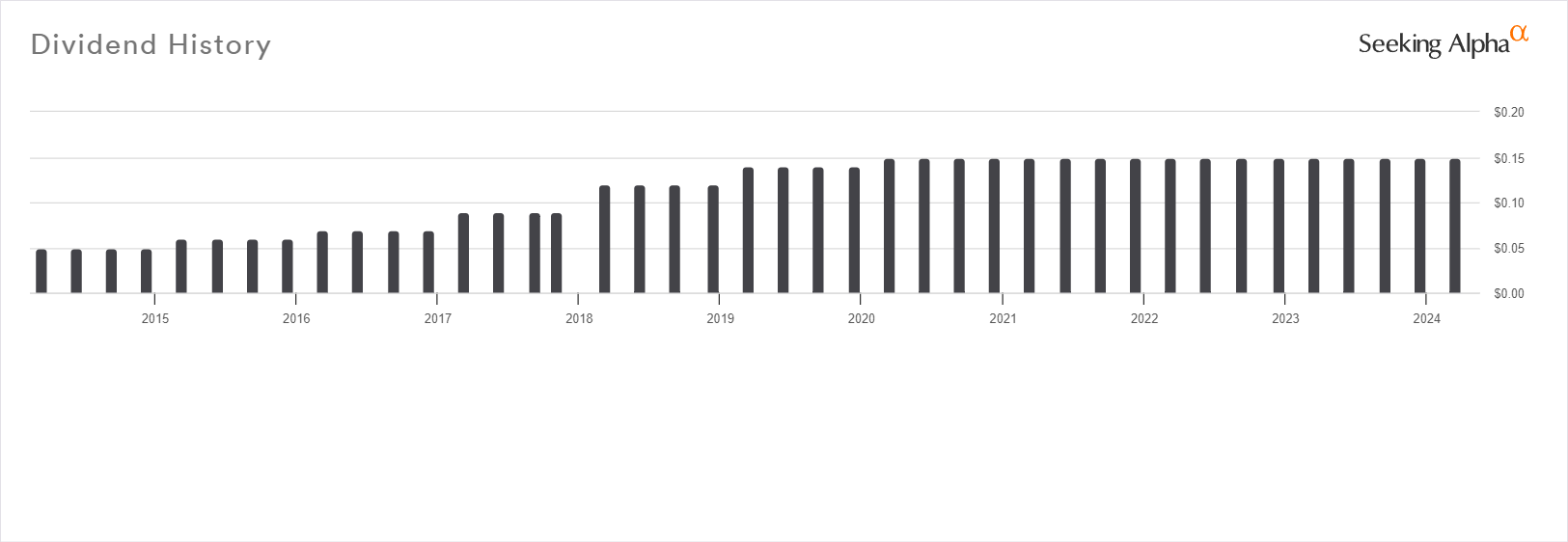

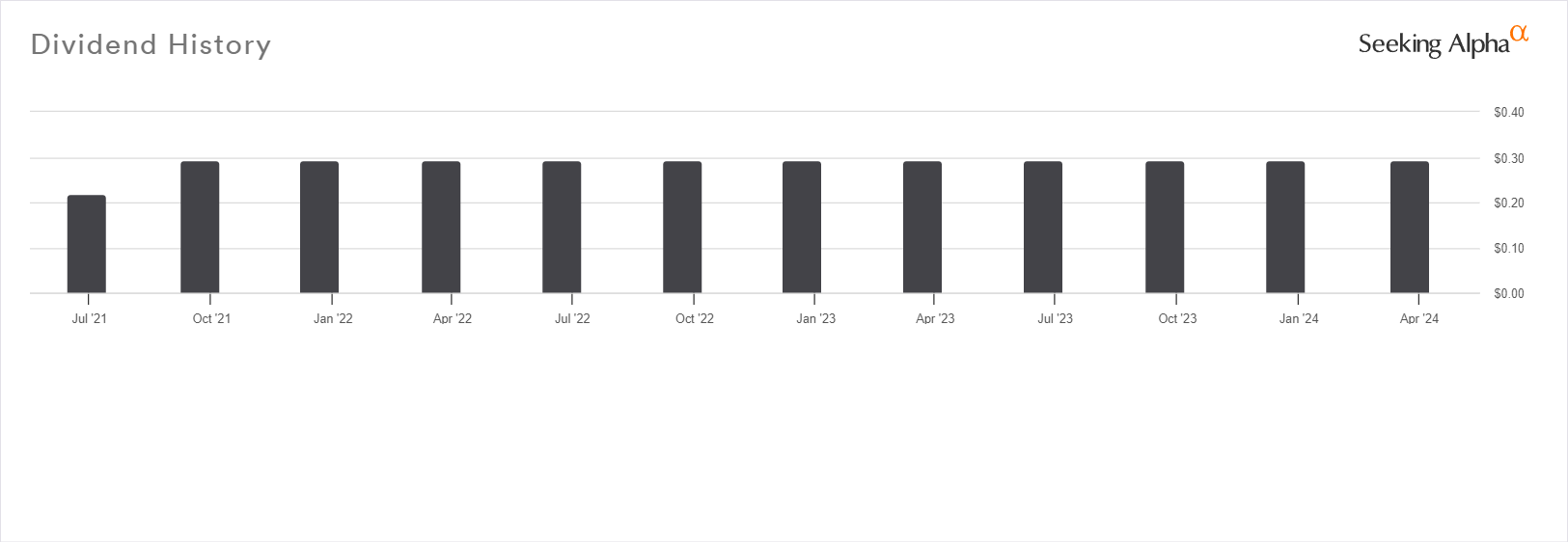

The company distributes dividends on a quarterly basis, with each dividend amounting to $0.15 per share, resulting in a forward yield of 4.27%. Both the payout ratio of 41.96% and the payment record suggest the dividend is safe.

Seeking Alpha

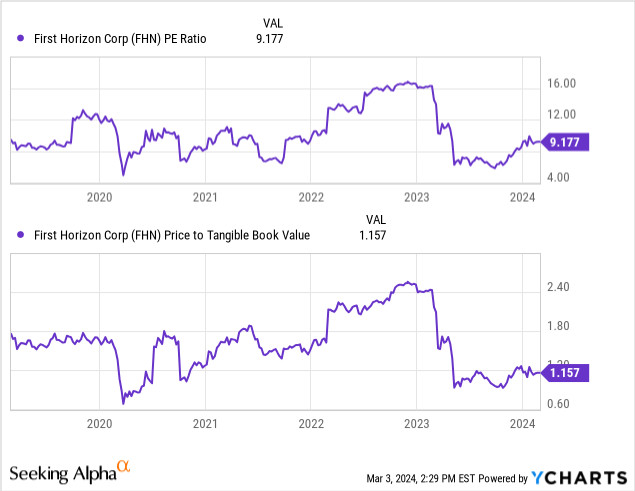

Further, I believe that income investors can enjoy the distribution with the added reassurance that the current stock price level has resulted in a relatively low earnings multiple and a modest premium to the bank's tangible equity:

Regardless, I believe that the Series F preferred shares are an even better pick because of their large discount to their liquidation preference, potentially a result of their much lower coupon yield; however, because of the discount, they now offer an equally attractive yield as the other series.

| Name | Ticker | Dividend yield | Discount to Liquidation Preference |

| Non-Cumulative Perpetual Preferred Stock, Series B | FHN.PR.B | 6.80% | 2.52% |

| Non-Cumulative Perpetual Preferred Stock, Series C | FHN.PR.C | 6.88% | 4.08% |

| Non-Cumulative Perpetual Preferred Stock, Series D | FHN.PR.D | 6.07% | -0.48% |

| Non-Cumulative Perpetual Preferred Stock, Series E | FHN.PR.E | 6.71% | 3.20% |

| Non-Cumulative Perpetual Preferred Stock, Series F | FHN.PR.F | 6.70% | 29.84% |

The company will be able to redeem them after July 10, 2026, which leaves plenty of time to capture gains if the dividends keep coming and the market continues its repricing that began at the end of 2023.

Seeking Alpha Seeking Alpha

Before we wrap it up, I'll have to go over the most relevant risks that come with investing in First Horizon:

Interest Rate Risk: A further increase in interest rates has the potential to negatively impact a bank's net interest margin which can shake investor confidence and result in a lower price.

Credit Risk: A sudden surge in default rates can significantly affect the company's profitability and its stock value.

Regulatory Risk: The industry faces potential shifts in regulatory frameworks, including alterations in capital requirements and lending standards, which could also affect a bank's bottom line.

Macroeconomic Risk: Changes in macroeconomic indicators such as inflation, GDP growth, unemployment, and consumer sentiment can affect the bank more directly than other industries. Economic downturns can result in less loan demand and elevated default rates.

All in all, I find the performance of this company more than decent in the current environment. Further, its business is adequately capitalized and reflects strong liquidity. Though I don't think that FHN is ideal for a value portfolio because of the premium to book value, its price level is low enough to make it a good dividend pick considering that a dividend cut is unlikely. For this reason, I am rating it a buy.

The Series F preferreds, however, deserve a strong buy because the unusually low coupon yield coupled with the increasing interest rates in the past appear to have motivated the market to make them both a dividend and value pick.

What do you think? Do you own either? Let me know in the comments and I'll get back to you soon. Thank you for reading!