Brandon Bell

Brandon Bell

I expressed my bearish view on FedEx Corporation (NYSE:FDX) in my initiation article in January 2024, indicating the growth headwinds from the business shift from air to ground. FedEx released their Q3 FY24 result on March 21 after market close, delivering -2% revenue growth and 90bps margin expansion. They are reaffirming the midpoint of the full-year guidance. Although I am impressed with the margin improvement driven by their DRIVE initiative, I am still bearish on the company's growth prospects. I reiterate the "Sell" rating with a fair value of $257 per share.

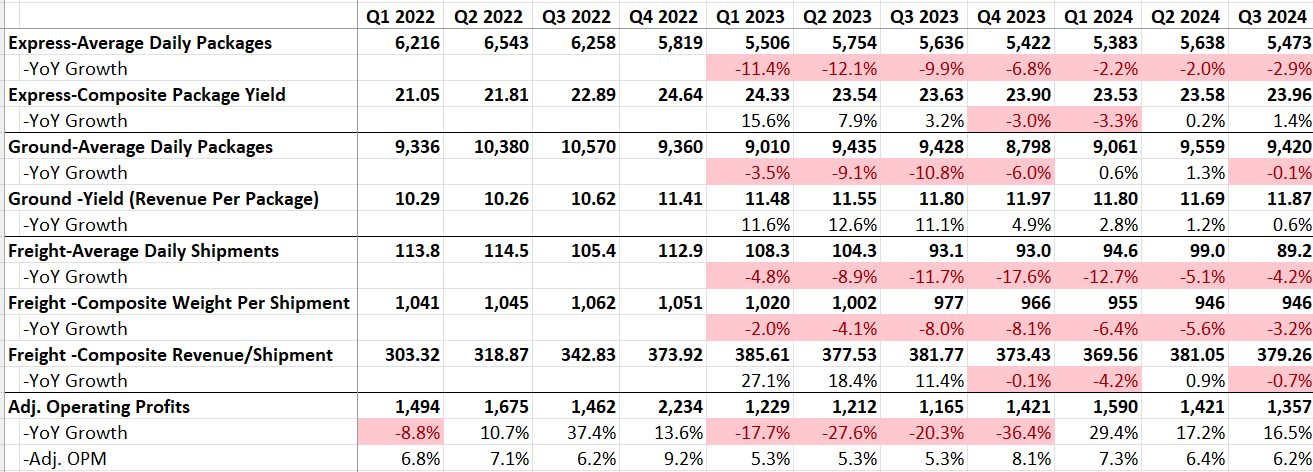

In fiscal Q3 FY24, their revenue declined by 2% year-over-year, while the adjusted operating profits increased by 16.5%, thanks to their cost-reduction initiatives, particularly in the Express and Ground business segments. The volume declined across the board, with Express dropping by 2.9%, Group declining by 0.1% and Freight decreasing by 4.2%.

FedEx Quarterly Results

There are several reasons for the weakness in volume growth:

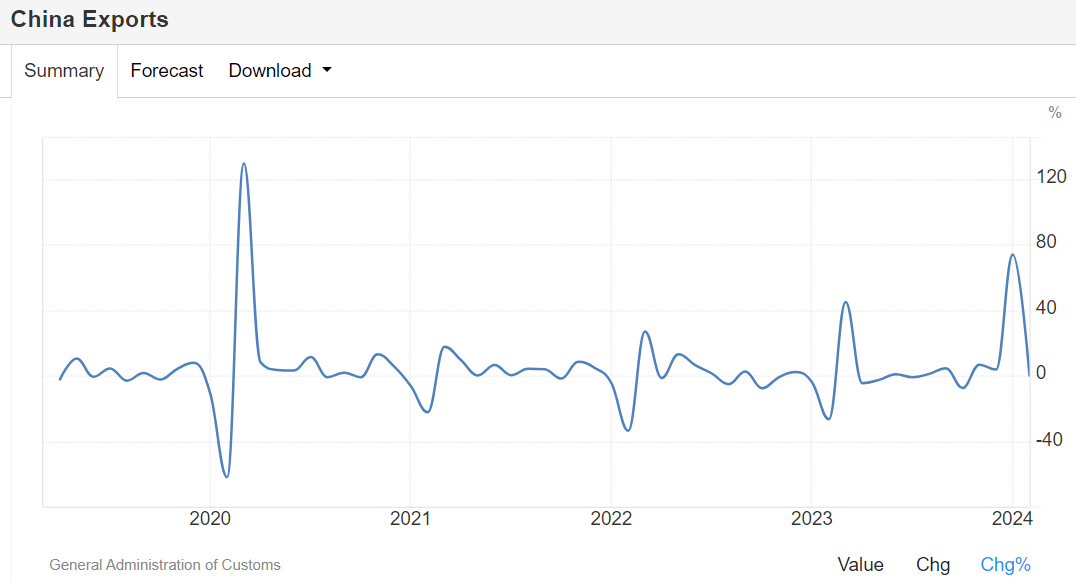

According to the Bureau of Industry and Security, 47.7% of total U.S. imports are coming from China, especially in textiles, consumer goods and industrial raw materials. Due to the high inflation globally, China's export volume has not shown any growth over the past few years, as depicted in the chart below. Please be aware that the chart presents currency in USD; therefore, the export volume growth should be negative after excluding the pricing factor.

Trading Economics

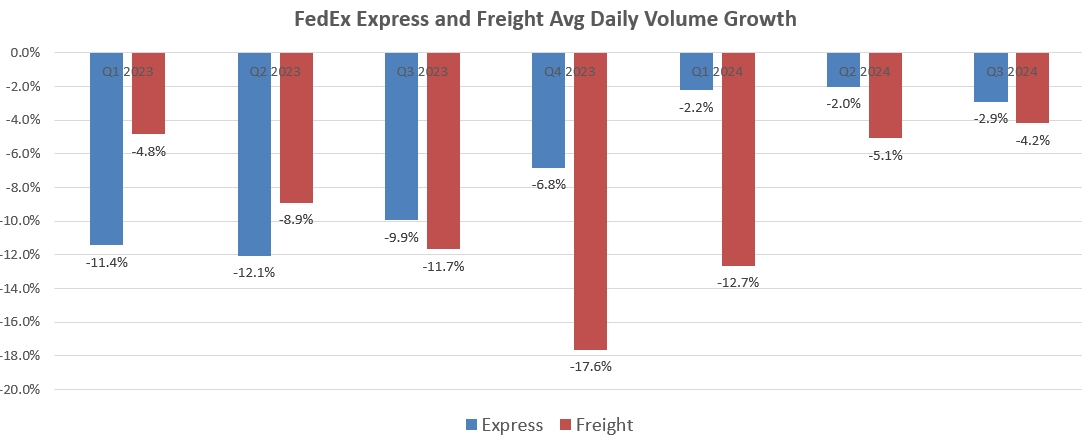

The weakening global trade has significantly impacted volume growth for the Freight and Express businesses. FedEx's Express and Freight businesses have experienced declining average daily volumes over the past few quarters, although the rate of decline is moderating.

FedEx Quarterly Results

Additionally, FedEx's Ground business has been impacted by the weak U.S. Industrial production growth. As illustrated in the table below, the Industrial Production Index has been presenting weak growth since 2023. Weak industrial production could potentially reduce demands for ground transportation. According to various industrial companies such as 3M Company (MMM), the general industrial market is undergoing an inventory correction process, and the timing of general industrial recovery is uncertain at this moment.

Federal Reserve

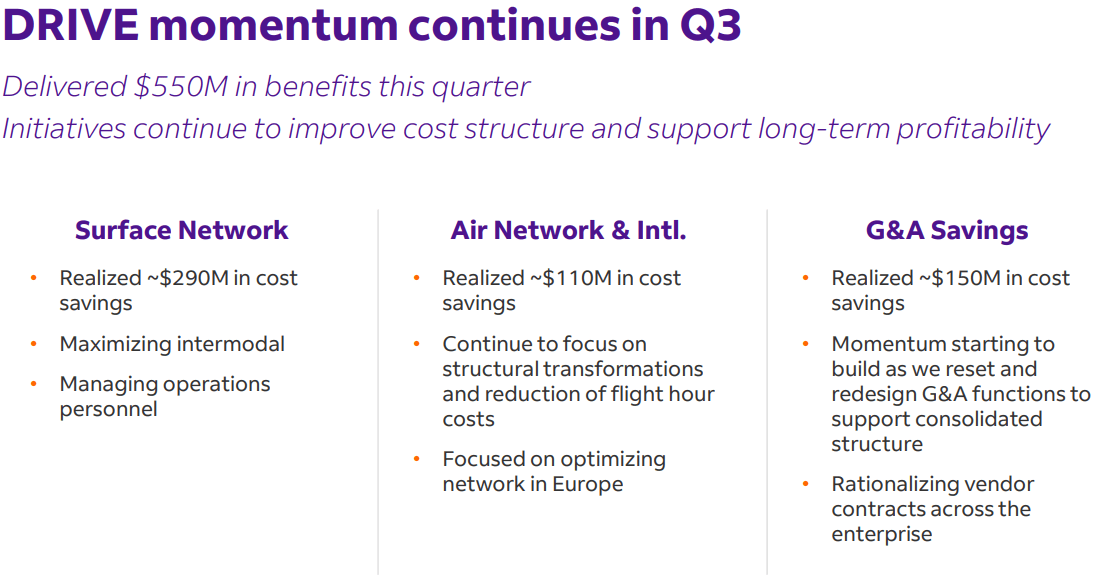

To offset the weak volume growth, FedEx has been actively managing their costs and improving yield. As illustrated in the slide below, their DRIVE initiative delivered $550 million in benefits this quarter, and the cost savings are across their surface network, Air, and G&A spending.

FedEx Investor Presentation

Over the earnings call, their management indicated that they were making progress on DRIVE to generate $600 million of savings in FY25. Based on their actual operating expenses in FY23, the total savings would represent a 70bps margin improvement, which is quite remarkable. The cost-cutting initiatives also include the continuing headcount management, as indicated during the earnings call. I am encouraged by their initiatives to manage their costs amid a weak volume growth environment.

They announced a $5 billion shares repurchase program, which would represent more than 7% of total market capitalization according to today's stock price. Their management anticipates completing a $2.5 billion share repurchase in FY24. It is worth noting that they only repurchased $1.5 billion in FY23 and $2.2 billion in FY22; as such, the company has accelerated its share repurchase activities.

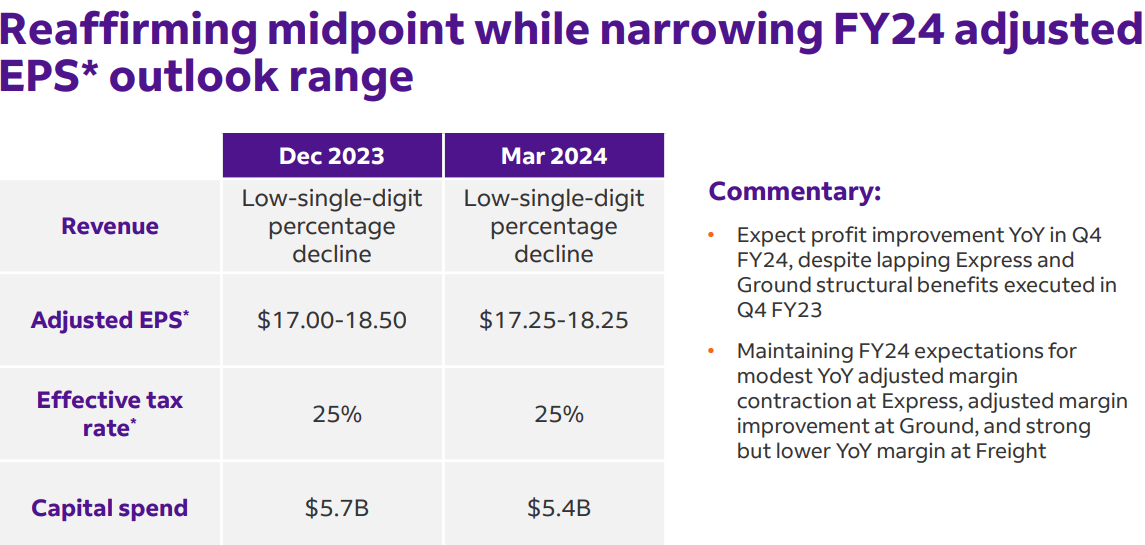

They reaffirmed the midpoint of FY24's guidance while narrowing the EPS range, as shown in the slide below.

FedEx Investor Presentation

For the full year, I anticipate the pressure on volume growth remains, albeit with easing trends. However, I expect their cost-saving initiatives to continue improving their operating margin in the near future.

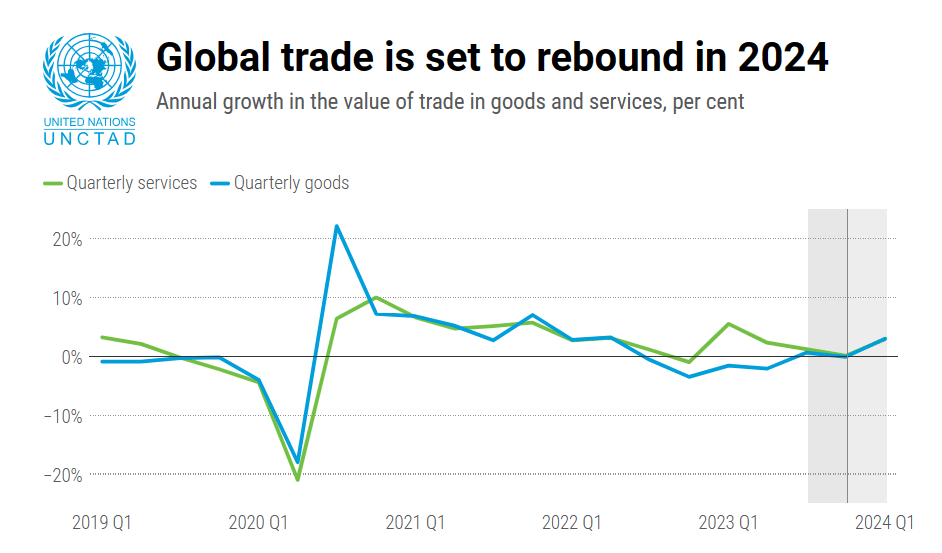

As discussed previously, FedEx's volume growth is closely tied to global trade activities and industrial production growth. According to UNCTAD's March forecast, global trade is poised to rebound in 2024 after a 5% drop in goods in 2023, as illustrated in the chart below.

UNCTAD

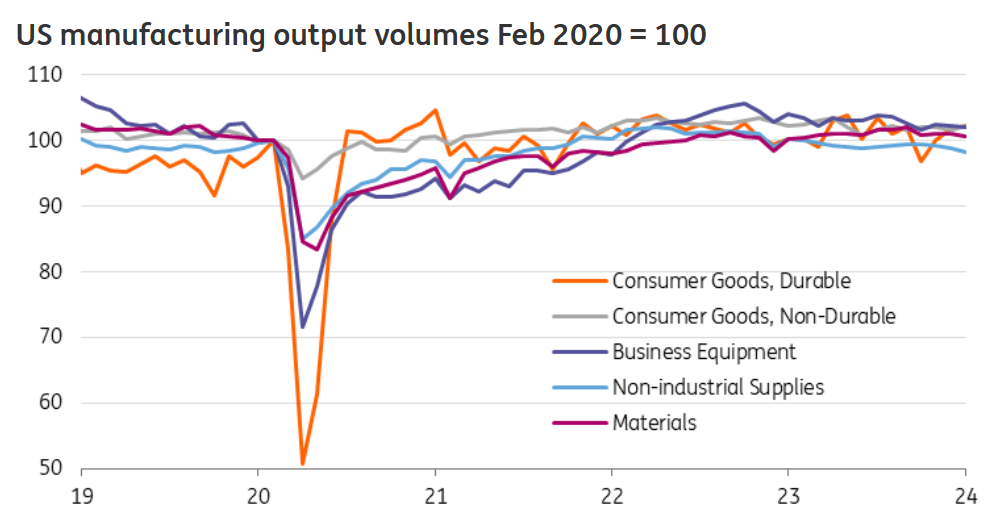

I am quite pessimistic about the U.S. industrial production activities for the year 2024. ING forecasts muted growth in the U.S. manufacturing output volumes. The current high interest rate would not support a meaningful recovery in the general industrial market, in my opinion.

ING Report

Assuming FedEx will repurchase $2.5 billion own shares in FY24, and another $2.5 billion in FY25, the total count of shares outstanding will be reduced by 3.5% year-over-year.

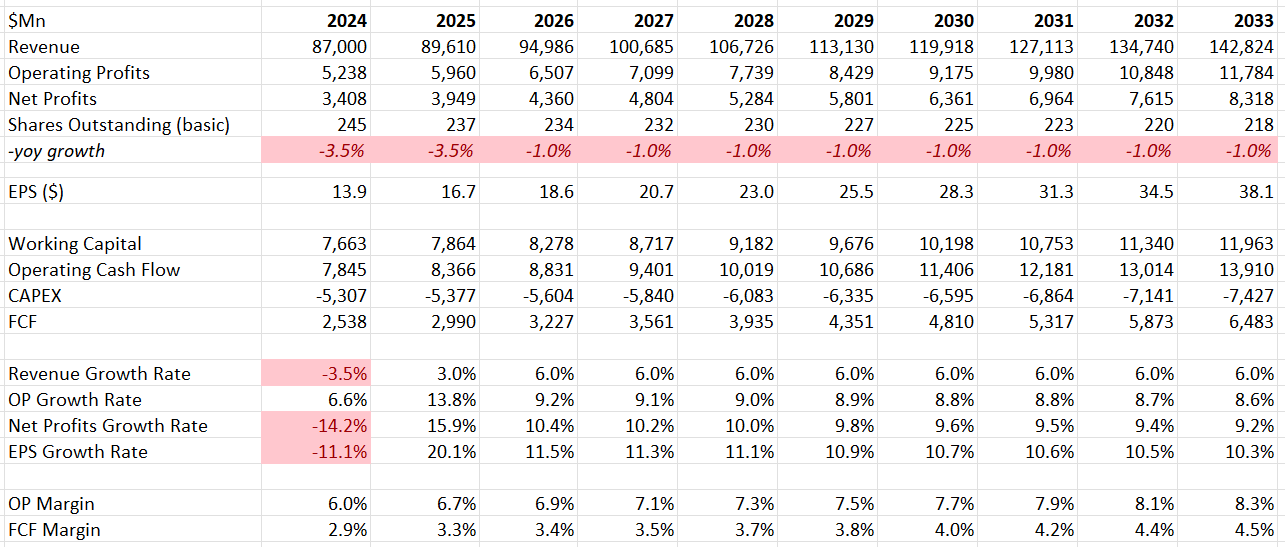

As discussed above, I anticipate FedEx's volume growth pressure from weak global trade and industrial production. The revenue growth is projected to decline LSD in FY24 and start a moderate recovery in FY25 with LSD growth. For the normalized growth, I continue to project 6% revenue growth, reflecting both yield and volume growth, and the normalized growth rate is consistent with their historical average growth rate.

Over the earnings call, their management disclosed that they will generate $1.8 billion in cost savings in FY24, offset by additional restructuring costs of $300 million. In FY25, they expect to generate an additional $600 million in cost savings. Based on these figures, I anticipate a 70bps margin improvement in FY25.

FedEx DCF - Author's Calculations

The WACC is calculated to be 10% with the following assumptions:

-Risk-Free Rate: 4.26%. The U.S. 10-Year Treasure Yield.

-Beta: 1.03. SA's 24-m Data.

-Cost of Debt: 7%; Equity Market Risk Premium: 7%.

-Tax Rate: 25%.

With a discount rate of 10%, the enterprise value is calculated to be $76.3 billion in the model. Adjusting the balances of cash and total debts, the fair value is estimated to be $257 per share.

United States Postal Service (USPS): I highlighted that USPS's strategy shift from air to ground will continue to pose growth challenges for FedEx in my initiation report. Over the earnings call, the management indicated that they were experiencing a continued headwind from USPS with reduced volumes. FedEx is still in the process of negotiating with USPS at this point, and the current contract ends on September 29th, 2024. I suggest investors pay attention to any news regarding the contract negotiation in the coming months, as the news could potentially fluctuate FedEx's stock price.

Despite some moderation in Q3, FedEx Corporation's volume growth continues to be under pressure due to weak global trade and weak industrial output growth. I acknowledge their efforts to save costs and improve yield, and I don't think it is a good entry point for FedEx. I reiterate with a "Sell" rating with a fair value of $257 per share.