NoDerog/iStock Unreleased via Getty Images

NoDerog/iStock Unreleased via Getty Images

Fresh Del Monte Produce Inc. (NYSE:FDP) is a massive food giant. The company is involved in the production, marketing, and distribution of fresh, and fresh-cut fruits and vegetables. You may be most familiar with seeing their canned goods at your local grocery store, but the company does have other business lines as well, including being a player in the prepared food market within Europe, Africa, and the Middle East. Over the years, the company has worked to vertically integrate its operations. This means that Fresh Del Monte manages pretty much its whole supply chain. This means they grow their food, package it, and deliver it to consumers and businesses.

For those who fancy sustainability initiatives in the companies you may invest in, Fresh Del Monte has a significant focus on environmental responsibility. The company has employed water-saving practices and works to ensure sustainable agricultural practices. The company also has its own ocean freight for shipping goods, and even has some restaurants that serve its foods directly to consumers.

The stock has been beaten down badly, but we think this is a level you can consider buying for value, growth, and the company just raised its dividend so it offers a nice forward yield here. In this column, we discuss the just-reported earnings and why we see shares as a buy.

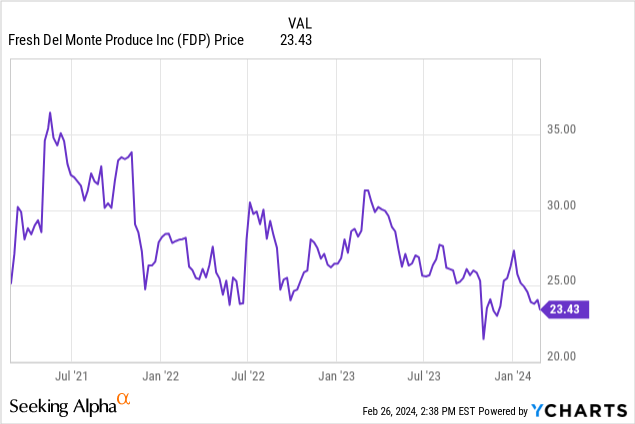

The stock is bumping along near 3-year lows and offering a 4.2% yield for those who start buying here. Inflation costs have hit the company hard, but people need to eat, and much of the costs have been passed on. We think the valuation here is compelling, and there is solid growth here too overall. It is a compelling level for investment. Let's talk about performance.

First the company is coming out of a big strategic review in the fall. The company reassessed priorities in the North America operations. This led to a non-cash impairment of $131.2 million in Q4, mostly as a result of Mann Packing operations. Moving forward, the company is still considering strategic alternatives for Mann Packing but also has a strong focus on improving profitability by controlling costs in the coming year. We like the setup.

Net sales for Fresh Del Monte dipped 1% to $1.01 billion compared with $1.04 billion in the prior-year comparable Q4. This slight decrease in sales was driven by lower banana sales, and lower performance in its services segments. However, there were higher per unit selling prices for most products, most notably avocados, fresh-cut fruit and vegetables, and pineapples. We mentioned the company is focused on cutting costs. This comes as gross profit took a hit.

Gross profit in Q4 was $62.5 million down from $81.7 million a year ago thanks to higher per unit production costs. Some of this was driven by unfavorable currency fluctuations. However, there were lower per unit distribution and ocean freight costs this quarter compared to a year ago, which is very positive. Adjusted gross profit was down to $56.2 million compared with $81.7 million in the prior-year period. These adjustments control for insurance recoveries and inventory write-offs.

The company has been impacted to a degree by the Red Sea conflicts where shippers have been targeted. Overall operating loss hit $113.4 million compared with operating income of $31.2 million but this was driven by the charge we mentioned above related to Mann Packing in North America. Adjusted operating income was still down to $12.0 million compared with $34.2 million in Q4 2022. All of this led to a net loss of $106.4 million.

Adjusted net income was $11.8 million compared with $21.5 million last year. On a per share basis, income was $0.25. It is important to note, however, that for all of 2023, profit was up, with adjusted net income hitting $101.7 million, up from $94.3 million.

Cash flow is strong here. Net cash provided by operations was $177.9 million for all of 2023, a strong increase from 2022. The company also chipped away at its long-term debt. Long-term debt to end the year decreased to $400.0 million from $539.8 million as of the prior-year end. This led the company to have a very manageable adjusted leverage ratio of 1.7x. The company moving forward in 2024 will continue to control costs and sell underutilized assets. By starting these cuts and selling some assets, this was actually the best-performing year for margins since 2016. It is also worth noting that during Q4, the company also announced and completed a $500,000 share buyback.

As we move into 2024, we expect cost controls to continue to boost margins. We like the dividend hike. Management did guide for a slight increase in capex to about $70 million, to fund expanding production in certain key global operations, such as the Fresh Pet Production Facility in the United Kingdom. For the year we are looking for low to mid-single digit revenue growth, on comparable margins to 2023, if not slightly better.

We think Fresh Del Monte Produce Inc. EPS, depending on the success of cost-savings, and no significant changes in freight costs, can hit $2.30 to $2.50. This puts the stock at less than 10X FWD earnings. We think for a global food leader, this is attractive, and you can collect a healthy 4.2% yield while you wait.