Elena Bionysheva-Abramova/iStock via Getty Images

Elena Bionysheva-Abramova/iStock via Getty Images

We previously compared Freeport-McMoRan (NYSE:FCX) in December 2023, discussing why we finally rerated the stock as a Buy, attributed to the higher copper spot prices, expanded production volumes, and lower operating costs by 2024, likely to boost the miner's near-term top and bottom lines.

Most importantly, we believed that its dividend payouts might be raised in 2024, thanks to the healthier balance sheet and richer free cash flow generation, offering opportunistic income investors with potentially more than doubled yields.

In this article, we shall discuss why we continue to rate the FCX stock as a Buy, attributed to the long-term electrification trend and near-term tailwinds with the miner likely to report higher top/ bottom lines as the copper spot prices rise.

Combined with the projected climb in the copper spot prices over the next few years, we expect to see the stock deliver both capital appreciation and higher variable dividend payouts moving forward, further sustaining its investment thesis despite the recent rally.

For now, FCX has reported top/ bottom line beats in the FQ4'23 earnings call in January 24, 2024, with revenues of $5.9B (+1.3% QoQ/ +2.6% YoY) and adj EBITDA of $2.29B (+4.5% QoQ/ +1.7% YoY), with FY2023 numbers of $22.85B (+0.3% YoY) and $8.79B (-7.6% YoY), respectively.

With copper comprising the equivalent 75% (-2 points YoY) of FCX's overall sales in FY2023, we believe that these numbers appear to be impressive.

This is given the decline in the realized copper prices of $3.85 per lbs (-1.2% YoY/ -11% from FY2021 levels of $4.33) and the higher unit net cash costs per pound at $1.61 (+7.3% YoY/ +20.1% from FY2021 levels of $1.34), implying the miner's ability to execute consistent operating/ capital cost discipline while delivering improved bottom lines.

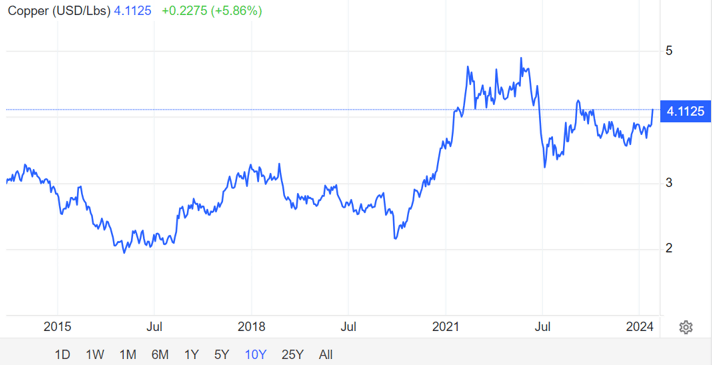

Copper Spot Prices

Trading Economics

With the copper's future now priced at $4.11 per lbs (+5.6% QoQ/ +3.7% YoY/ +47.8% from 2019 averages of $2.78), higher than FCX's FY2023/ FY2022 average realized prices, we believe that the miner may be able to report improved top/ bottom lines over the next few quarters.

This is mostly attributed to multiple macro events, as the global supply tightened with the closure of First Quantum Minerals Ltd.'s (FM:CA) Cobre Panama mine, which accounted for approximately 350.4K metric tons of copper capacity in 2022, or the equivalent to 1% of the global production.

With arbitration still ongoing, it remains to be seen when the Panama mine may reopen, with copper prices likely to remain elevated in the mean time. Even FCX has guided flattish YoY copper production in FY2024.

At the same time, Chinese smelters have also came together in an effort to boost the copper refining prices through "a symbolic cut in loss-making production, (though) without specifying volumes and timing."

It appears that this development is attributed to the new smelter capacities expected through H2'24, including FCX's recently inaugurated smelter expansion in Indonesia, potentially triggering further volatility on copper concentrate supplies and eventually, prices.

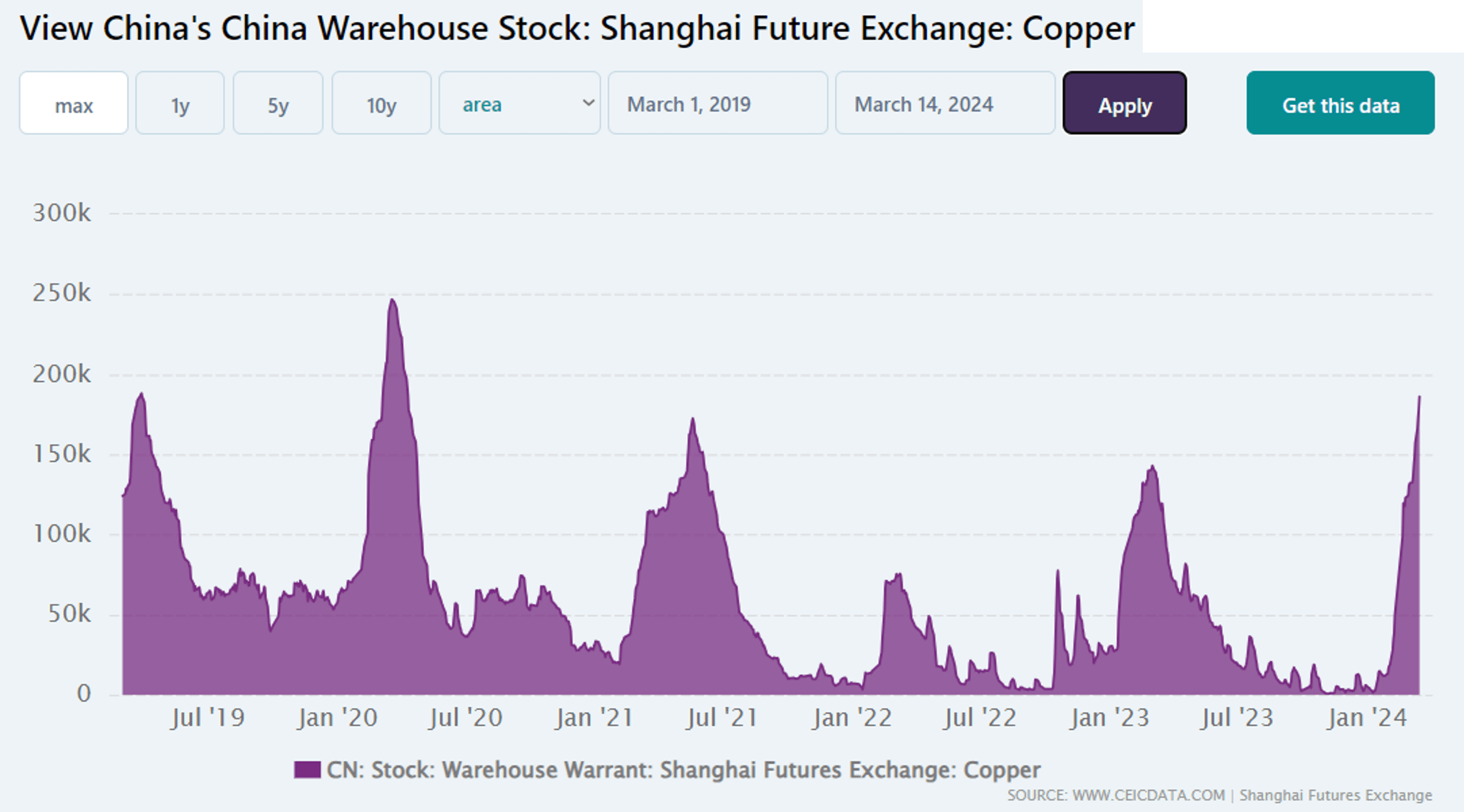

China Warehouse Stock: Shanghai Future Exchange: Copper

China Warehouse Stock: Shanghai Future Exchange: Copper

On the one hand, as the spot prices rose, China's copper warehouse inventory also grew to 186.2K ton by March 14, 2024, compared to the bottom of 753 ton in November 2023 and the peak of 246.87K ton in March 2020, implying that a reversal in spot prices may soon come if inventory continues to grow.

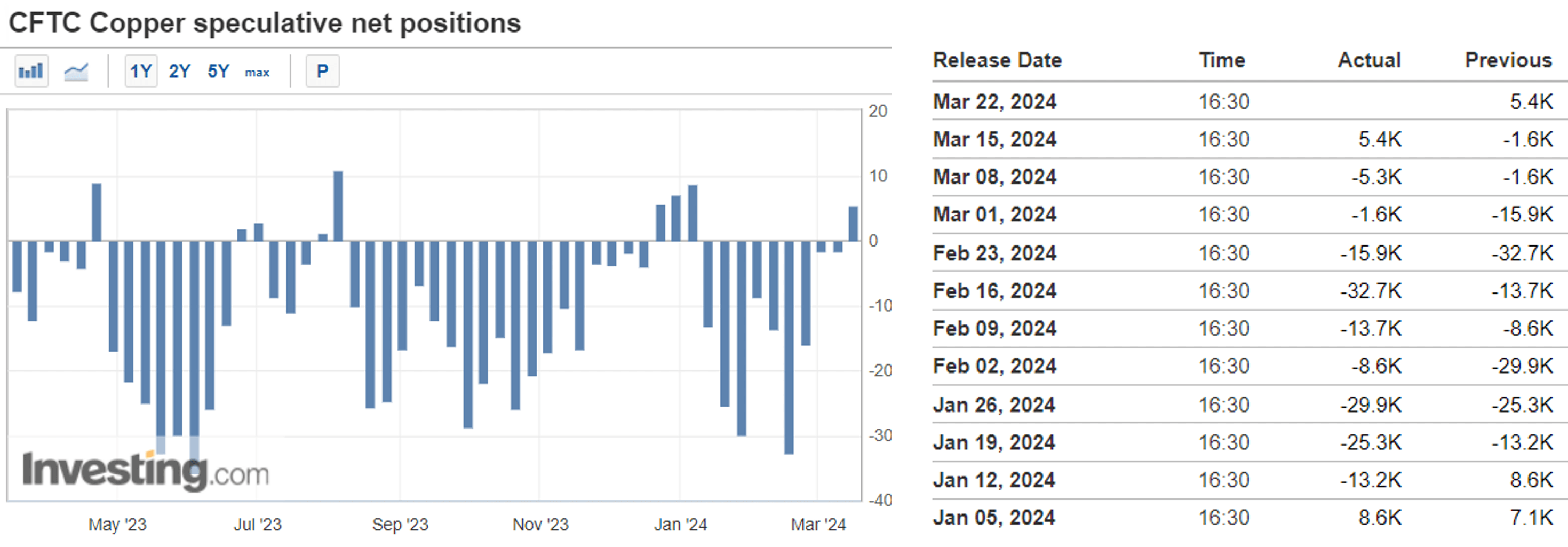

CFTC Copper Speculative Net Positions

Investing.com

On the other hand, it appears that copper futures may further rally, as the total net long position in the Commodity Futures Trading Commission reverses positively to 5.4K by March 15, 2024, the second time it does since the start of the year at 8.6K in January 04, 2024.

This is compared to the -5.3K reported the week before and -32.7K reported in February 16, 2024, implying a potential reversal in market sentiments as analysts anticipate higher prices ahead.

Finally, we believe in the restart of the electrification trend globally, with lithium miners, such as FCX, to benefit from the healthier demand once the macroeconomic outlook normalizes and renewable/ EVs are adopted by the mass market.

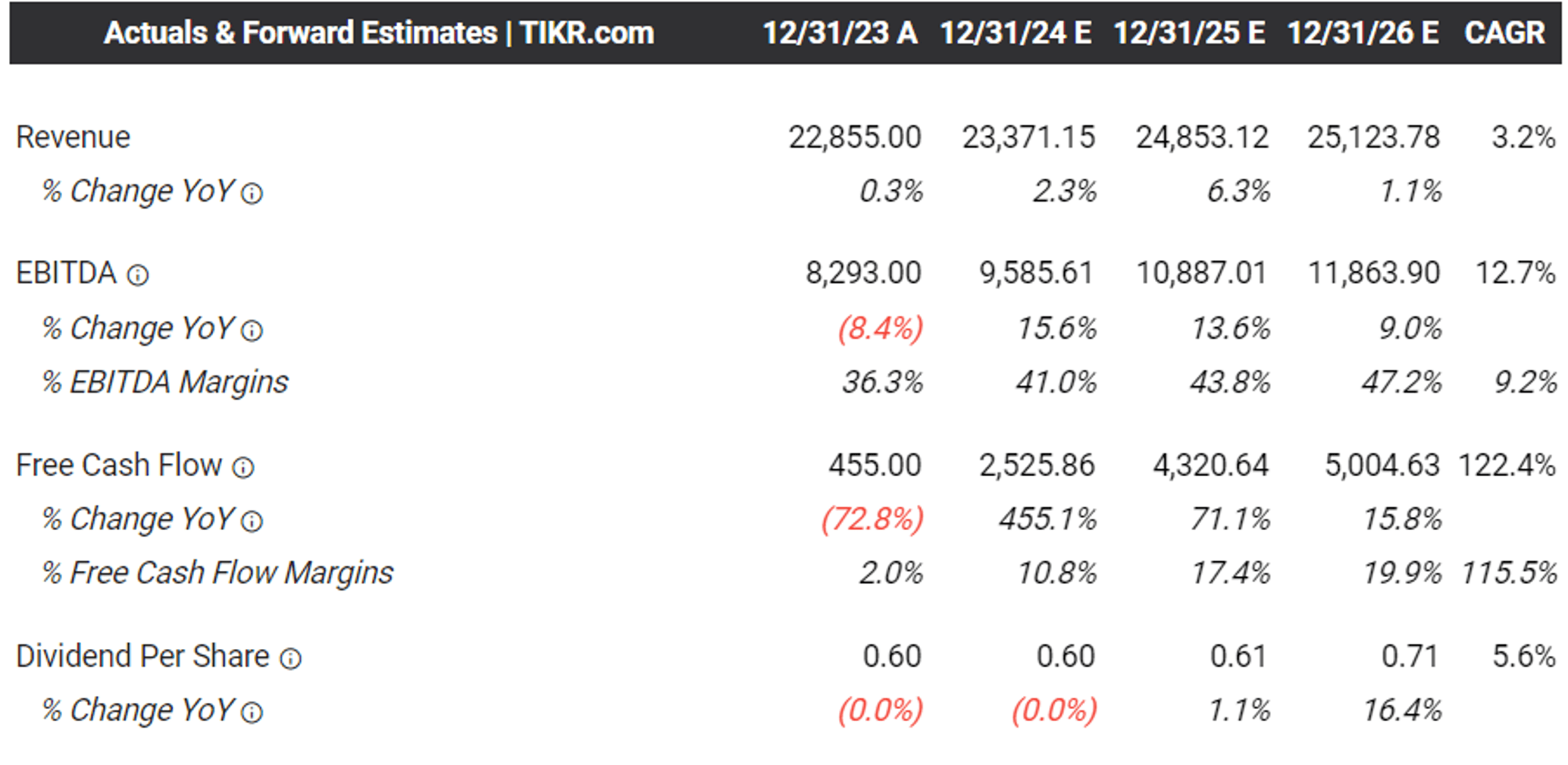

The Consensus Forward Estimates

Tikr Terminal

The same has been estimated by the consensus, with FCX expected to generate an accelerating EBITDA growth at a CAGR of +12.7% with expanding EBITDA margins of over 40% and FCF margins of over 10% through FY2026.

This is compared to the profit margins of 18.8%/ -8.1% reported in FY2019, 45.5%/ 24.5% in FY2021, and 36.3%/ 2% in FY2023, respectively.

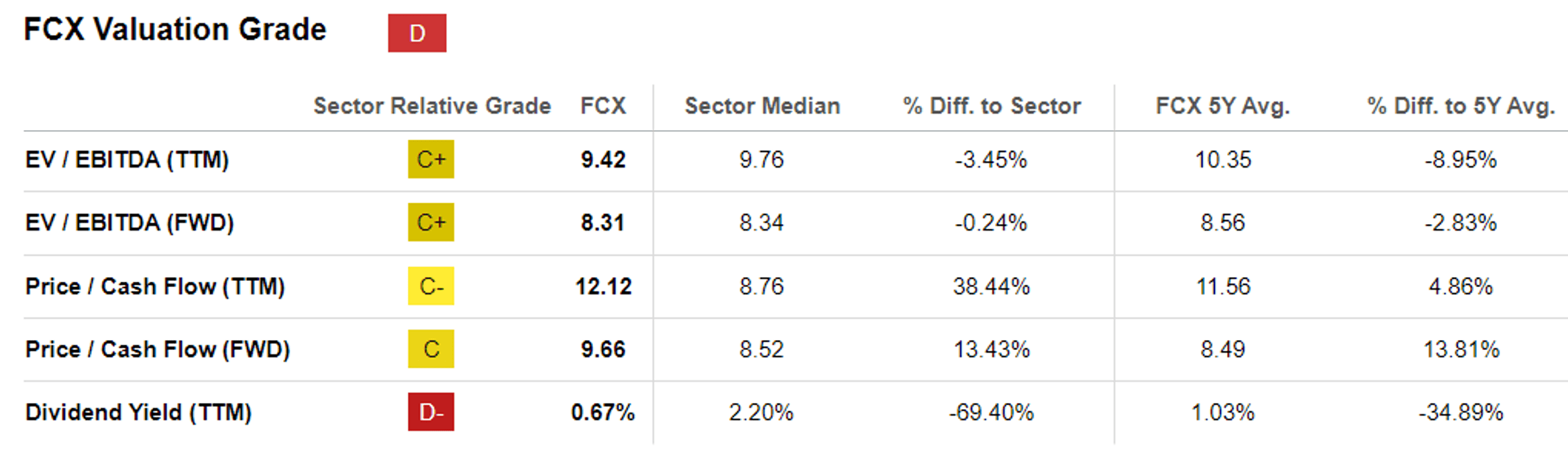

FCX Valuations

Seeking Alpha

This is also why we can understand why the market has moderately upgraded FCX's prospects to FWD EV/ EBITDA of 8.31x and FWD Price/ Cash Flow of 9.66x, compared to our previous article at 7.80x/ 10.09x and the mining sector median of 8.34x/ 8.52x, respectively.

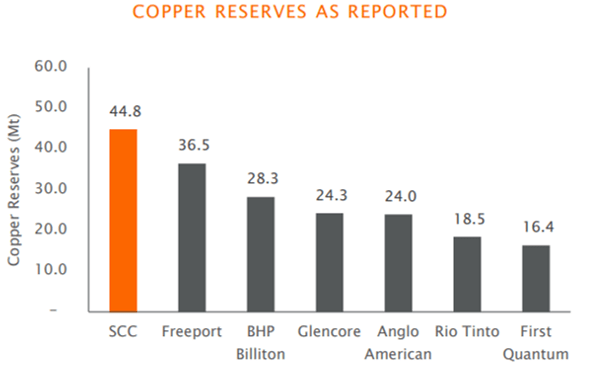

FCX's Copper Reserves

SCCO

It is apparent that FCX's focused copper portfolio is paying off extremely well now, especially due to the next-decade electrification trend, naturally exemplifying why the stock deserves its premium FWD valuations as copper prices continue to climb.

It also cannot be ignored that FCX boasts the second largest global copper reserves, while being the second largest producer by volume in 2022 and Q3'23.

As a result of its long-term growth prospects, we believe that FCX is fair valued now, especially since the same premium is also observed in its pure-play copper mining peer, Southern Copper (SCCO) at 14.29x/ 21.80x.

If anything, with iron ore spot prices falling now, we can also understand why there is a widening gap in the FWD valuations to its diversified mining peers, such as BHP (BHP) at 5.27x/ 10.56x, Rio Tinto (RIO) at 4.26x/ 5.41x, and Vale (VALE) at 4.62x/ 4.27x, respectively.

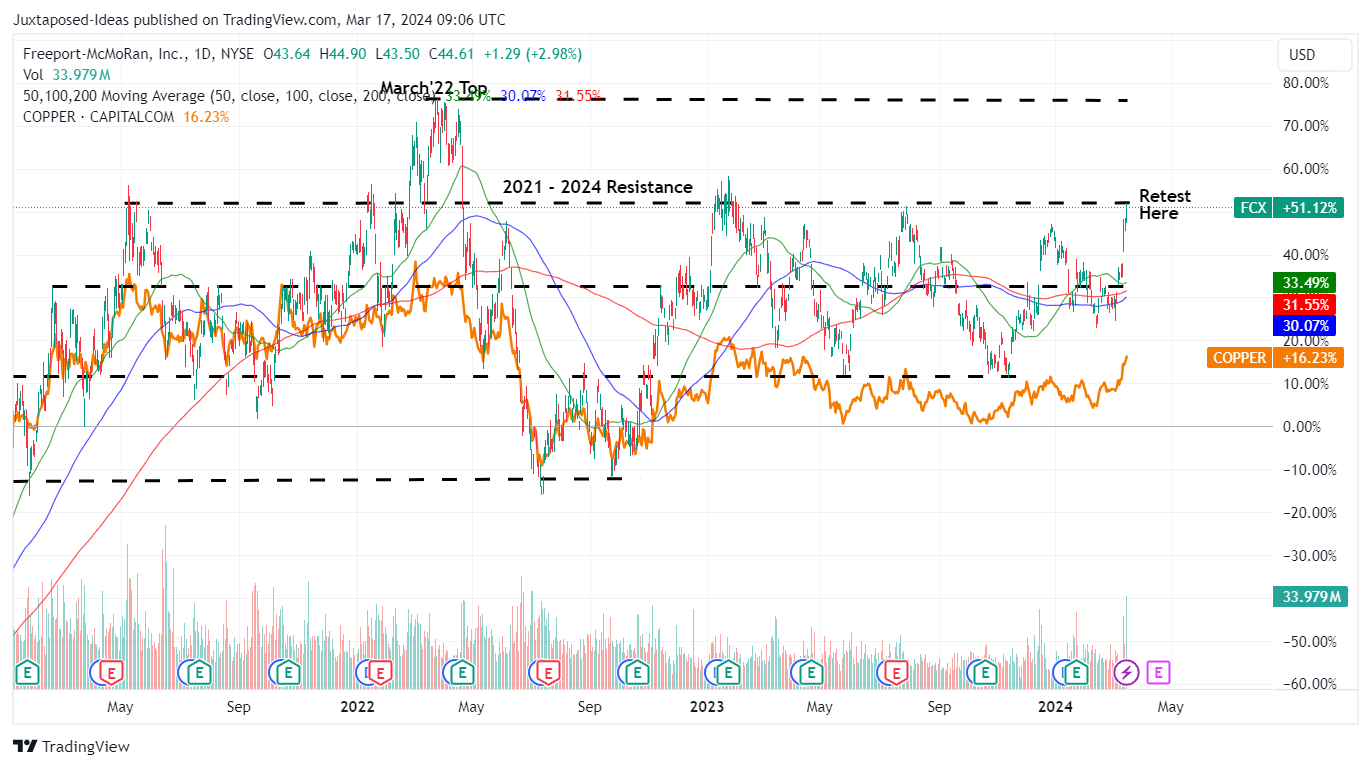

FCX 3Y Stock Price

Trading View

As a result, we can also understand why FCX has risen as it has, with the current copper spot prices potentially triggering FY2024 adj EBITDA of over $10B (+13.6% YoY), if not more, as the management guides flattish unit net cash cost of copper at $1.60 per lbs (-0.6% YoY).

With analysts still expecting copper prices to "soar more than +75% over the next two years amid mining supply disruptions and higher demand for the metal, fueled by the push for renewable energy," we believe that FCX stock prices may similarly rally ahead.

This is on top of the possibility of higher variable payouts, due to FCX's healthier balance sheet with lower long-term debts of $8.65B (-9.7% YoY/ -11.9% from FY2019 levels of $9.82B) and moderating debt-to-EBITDA-ratio of 1.02x in FY2023 (compared to 1.02x in FY2022 and 4.36x in FY2019).

As a result of the relatively attractive risk/ reward ratio, we are maintaining our Buy rating for the FCX stock.

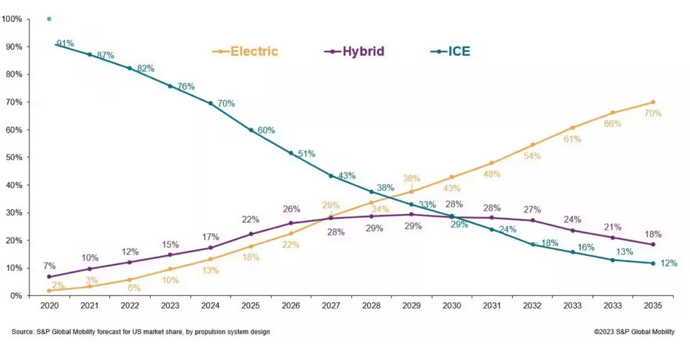

Global Mobility Projections

S&P Global Mobility, Car Scoops

Naturally, it goes without saying that copper prices will remain volatile until the second wave of electrification starts by speculatively 2026, once the macroeconomic outlook normalizes, borrowing costs moderate, renewable energies are embraced, and EV mass adoption starts, with a "crossover point with hybrid and ICE sales expected by 2029."

As a result, we expect FCX to similarly fluctuate moving forward, as the world slowly electrifies through the next decade, implying that the stock is only suitable for those with moderate risk appetite and long-term investing trajectory.