peshkov

peshkov

Written by Nick Ackerman, co-produced by Stanford Chemist.

Eaton Vance Tax-Managed Global Diversified Equity Income Fund (NYSE:EXG) invests in a fairly diversified portfolio, including providing global exposure. The fund is quite similar to its sister fund, Eaton Vance Tax-Managed Global Buy-Write Opportunities Fund (ETW). If the name alone doesn't tell you what the difference between these closed-end funds, or CEFs, is, then you're probably not alone.

Both funds incorporate global exposure, but the benchmark for EXG is, more specifically, the MSCI World Index. For ETW, they incorporate both the S&P 500 and MSCI Europe Indexes as its benchmark. Both of these funds then also incorporate a call-writing overlay strategy, writing against indexes. This is also where they slightly diverge in terms of their approach. ETW overwrites up to nearly 100% of its value, and EXG is at around 50%.

What makes EXG (and ETW) attractive at this time is the large discounts these funds are carrying. A large discount on its own doesn't tell us the whole story, but this fund isn't just trading at a wide discount on an absolute basis but also on a relative basis.

EXG will:

"invest in a diversified portfolio of domestic and foreign common stocks with an emphasis on dividend-paying stocks and writes call options on one or more U.S. and foreign indices with respect to a portion of the value of its common stock portfolio to generate current cash flow from the options premium received."

They last reported being overwritten by 48%, which regularly is the case, as it was the exact same in our prior update.

They have a "tax-managed" focus, as the name would suggest. They do this by:

"evaluating returns on an after-tax basis and seeks to minimize and defer federal income taxes incurred by shareholders in connection with their investment in the fund."

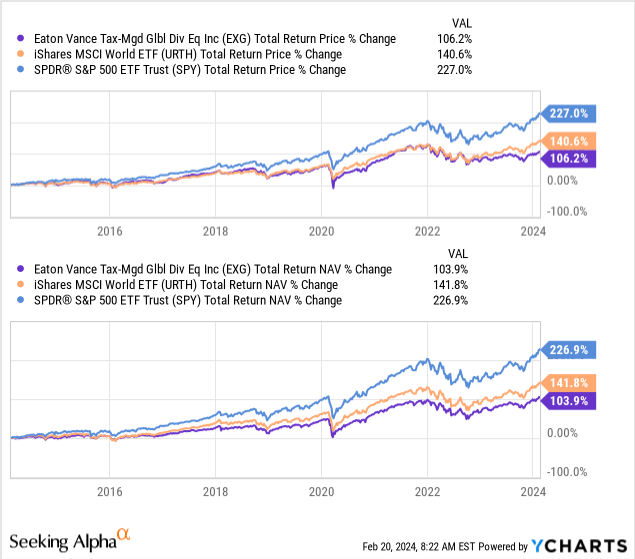

Since our last update, the fund has provided positive total returns and slightly positive price returns. However, it was exceeded easily by the S&P 500. Some of this was due to the discount widening, leading to somewhat reduced results.

EXG Performance Since Prior Update (Seeking Alpha)

However, a larger factor here is global exposure and a call-writing strategy. Global investments have been relatively weaker performers for most of the last decade. However, that isn't always the case, as historically, there have been periods where international investments did outperform. That said, for most of EXG's life, it has been relatively weaker.

The call-writing strategy also plays a role in some underperformance when the market is broadly performing well. That's why, over the last decade, it also isn't too surprising to see the fund outperformed by something like the iShares MSCI World ETF (URTH).

Ycharts

Writing calls can sometimes cap upside potential, and by writing index calls, the fund can experience losses when the index it writes against keeps rising.

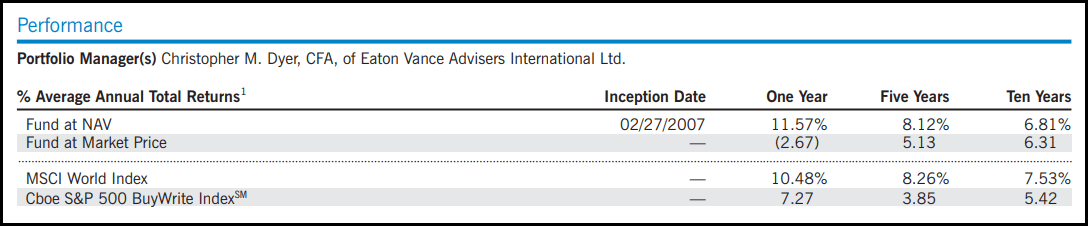

That's why when the fund lays out its performance, it also includes the CBOE S&P 500 BuyWrite Index for comparison to help provide some context of the performance relative to the options strategy it employs. On that basis, EXG's results are much more comparable and even exceed the index's results quite substantially. Though it should be noted that these results are from the fund's last annual report, that is, for the period ending October 31, 2023.

EXG Annualized Performance Compared to Benchmarks (Eaton Vance)

One thing that investing in an index can't provide - besides not being directly investible in the first place without a proxy ETF that tracks an index - is a discount to its net asset value per share.

The discount for EXG, similar to the other Eaton Vance equity-based funds, came primarily as the result of distribution cuts the sponsor took in late 2022. A distribution cut is often one of the main catalysts for a discount to open up on closed-end funds because, unlike their exchange-traded fund ("ETF") counterparts that often pay variable dividends based on cash flows received, CEFs aren't allowed to cut their distributions based on conditions. They must pay a managed or level distribution for their entire life. Well, not really by any real law or anything, but by the unwritten laws of most CEF investors.

Personally, I find distribution cuts often present some of the best investing opportunities. Of course, I wouldn't say I like it when it's done in a fund I already own, but if it's one I'm looking to add, it often provides an opportunity.

With that being said, before that, the fund was trading at a premium. So clearly, this was one of the main catalysts to push the discount wider.

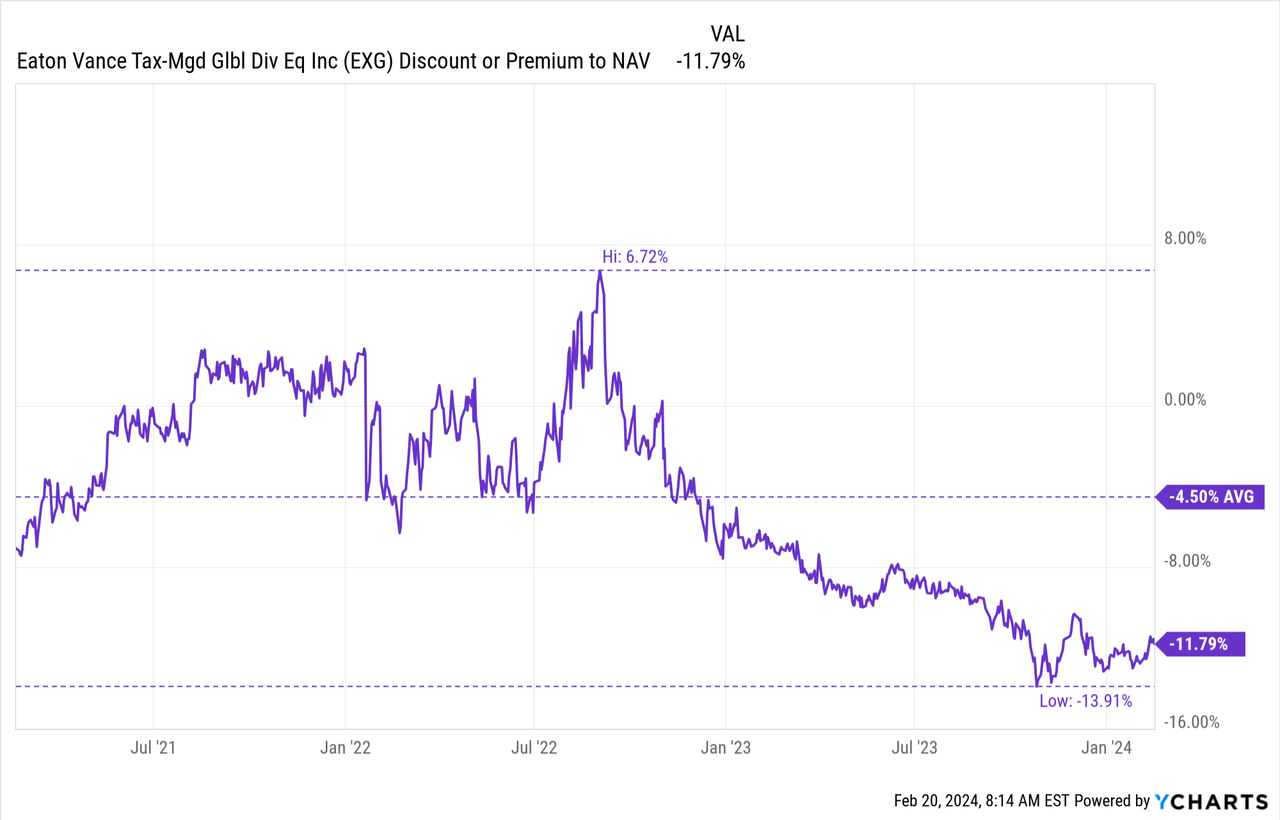

Further, CEFs have been trading at some of the widest discounts historically. This has narrowed somewhat more recently. However, since we came from 2021 when discounts were historically narrow, the drop has certainly felt much more dramatic over the last couple of years.

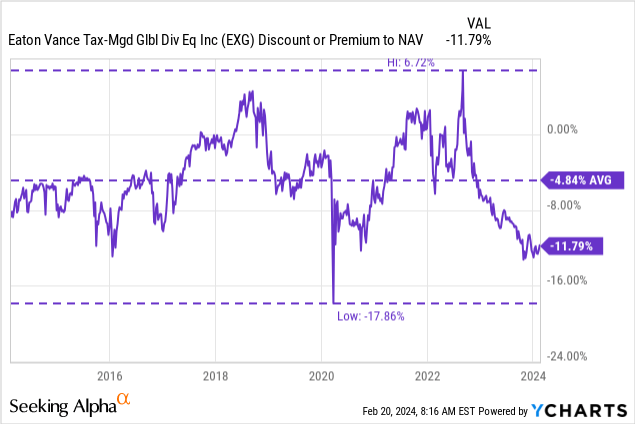

EXG was pretty much a perfect example to highlight what was happening more broadly and what a distribution cut can do to a CEF's valuation as well. Going from a premium of nearly 7% and then dropping all the way to a low discount point of nearly -14% is something shareholders are going to feel.

Ycharts

We've come off the lows, but on a relative basis, we can see that the discount is quite appealing at this time. Though the above is for the last three years, if we look at the last 5 years, the fund's average discount was somewhat similar at around -5.2%. Looking back even longer, over the last decade, we also see a similar picture.

Ycharts

The fund could go to an even wider discount, but at least if history is any indication, further discount widening could be limited from here.

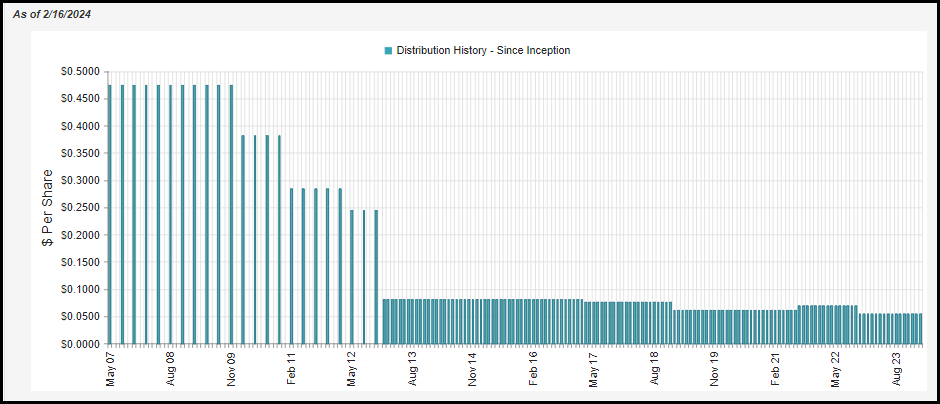

The fund's distribution comes to a relatively attractive 8.37% distribution yield, and that works out to an NAV rate of 7.38%. The difference here is that thanks to the fund's substantial discount, investors can receive more than the underlying fund has to earn.

EXG Distribution History (CEFConnect)

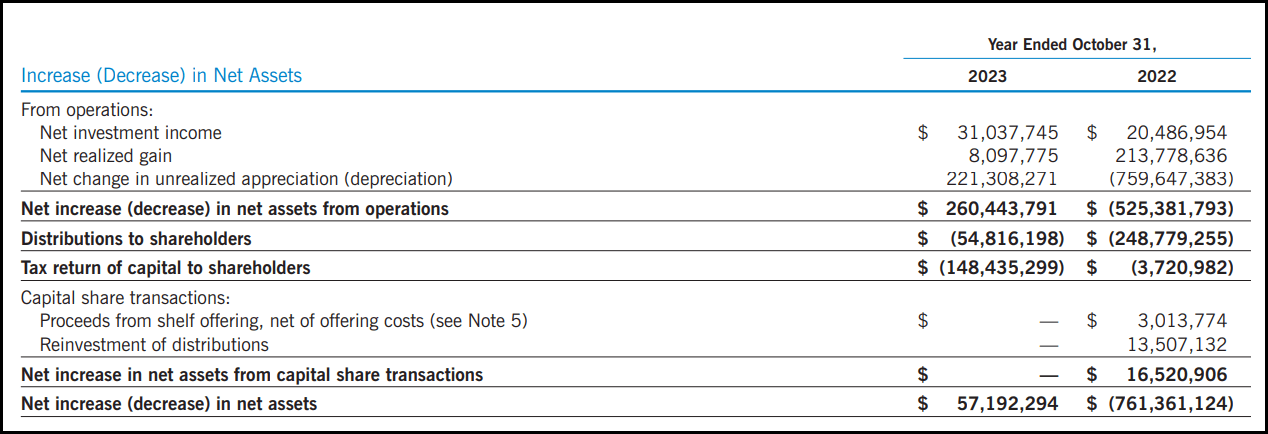

At this rate, we could almost be in a position for the fund to raise its payout to investors, assuming the market continues to remain relatively calm and perform well. The market performing well is a real concern for the distribution because, like many equity CEFs, it will rely significantly on capital gains to fund its payout to investors.

EXG Annual Report (Eaton Vance)

Some of these capital gains can come from the options writing strategy. However, it sometimes isn't as straightforward as that. This is because the strategy can also produce losses; as we mentioned above, if the index continues to rise, they'll have to close out the contracts at a loss.

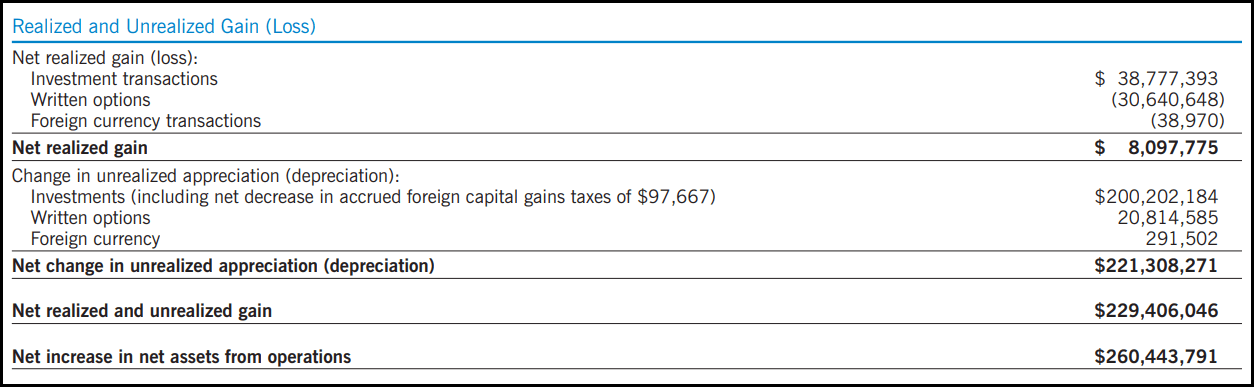

That's what ended up happening in the last fiscal year, as the options strategy generated unrealized losses of over $30.5 million - partially offset by the unrealized gains of nearly $21 million from the strategy. These losses were also more than offset by realized appreciation from the fund's underlying portfolio.

EXG Realized/Unrealized Gains/Losses (Eaton Vance)

This is really where the strategy centers around: an index can't be owned directly, but they can own underlying positions that make up the indexes. So that takes the risk off the table of theoretically unlimited losses that could happen from naked index writing. If the options writing strategy is generating losses, it's because equities are appreciating. This can work in reverse, too; if the underlying portfolio is falling and producing losses, the options premium received can offset some of those declines.

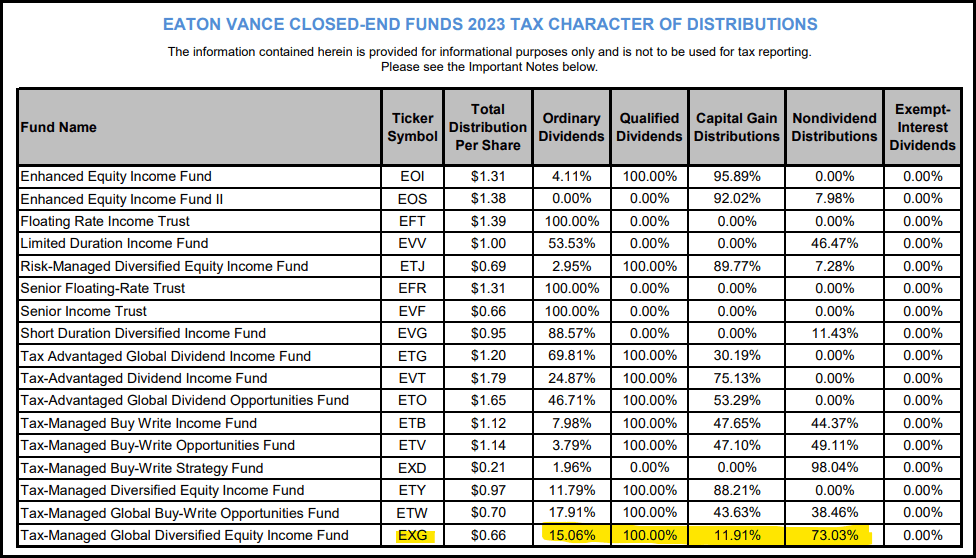

Finally, the options writing strategy can also play a role in the fund's distribution tax classifications. If you realize losses from one side of the strategy that are offsetting realized gains from the other side, you then will end up generating a return of capital distributions. In this case, Eaton Vance labels them "non-dividend distributions."

These breakdowns can fluctuate from year to year, but seeing ROC distributions from Eaton Vance funds isn't anything too surprising. That is, in fact, where they get the "tax-managed" part of their names.

For EXG, 2023 listed that a majority of the distribution was ROC. What portion that wasn't ROC was either qualified dividends or long-term capital gains - which are further tax-friendly classifications for distributions.

Eaton Vance Distribution Tax Character (Eaton Vance (highlights from author))

Turning toward the fund's portfolio, they were a little bit quiet in the latest fiscal 2023. Their portfolio turnover rate came to 19%, which was down from 27% and 44% in each of the prior fiscal years. That's not necessarily a bad thing, either, as it once again can go back to its portfolio strategy of avoiding too much in taxable distributions. If investments are performing well across the board, too much turnover could lead to realizing too many gains.

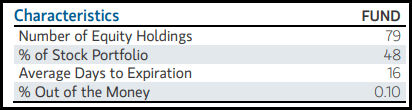

The fund's latest fact sheet showed they were holding just 79 holdings total. We also see that the overwriting of the portfolio came in just shy of 50%, which is consistent with their target level.

EXG Portfolio Characteristics (Eaton Vance)

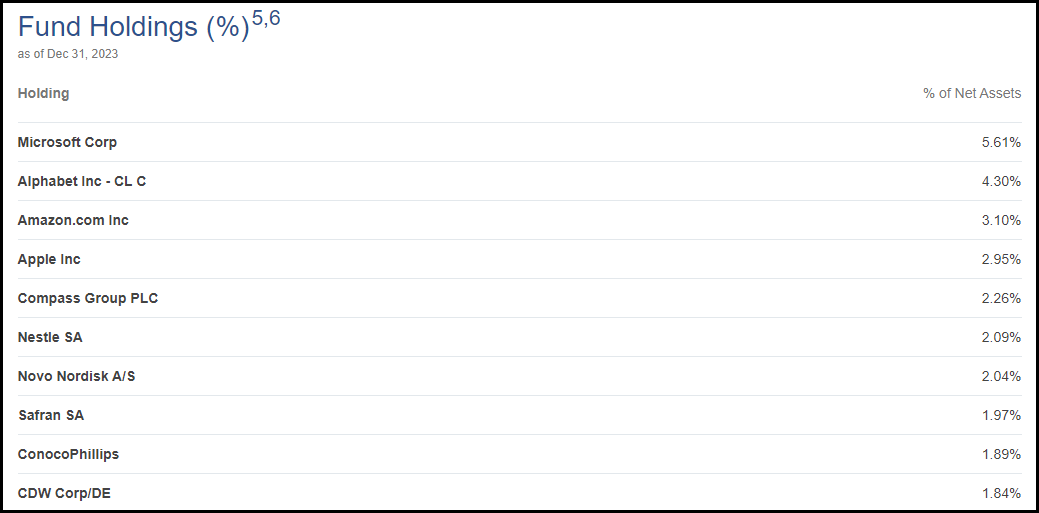

When looking at the top ten holdings, we see quite a few Mag 7 names. In total, these mega-cap tech names represent just shy of 16% between Microsoft (MSFT), Alphabet (GOOG), Amazon (AMZN) and Apple (AAPL). These were also holdings listed as top ten names in the last update we had for this fund.

EXG Top Ten Holdings (Eaton Vance)

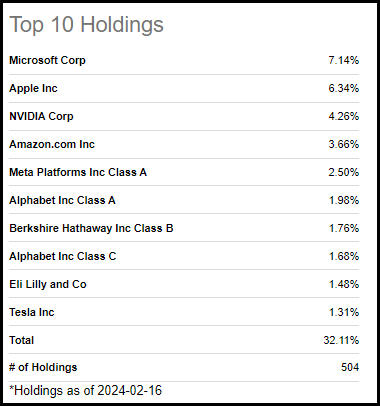

That weighting in the Mag 7 names is actually significantly less than the S&P 500 itself right now, as represented by the SPDR S&P 500 ETF (SPY), which listed its Mag 7 exposure as just over 27.5%. When you consider that SPY lists 504 holdings, that's a big relative overweight to these few selected names. In some ways, it could be argued that EXG is actually more diversified despite only carrying less than 80 total holdings.

SPY Top Ten (Seeking Alpha)

Again, SPY or the S&P 500 aren't actually benchmarks for the fund, but the discussion is helpful for providing some relative context and why performance is going the way it is. If the fund had just overweighted the Mag 7 names historically, it would have actually performed better. That's always easy to see in hindsight, though.

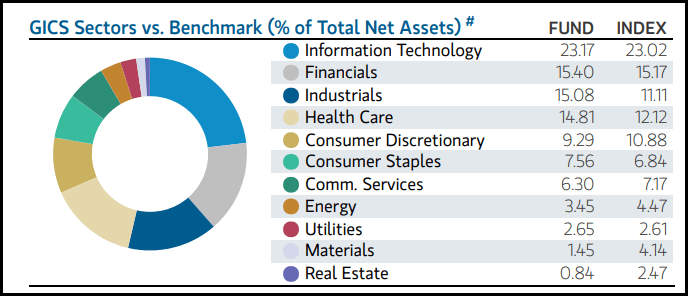

When looking at the fund's actual benchmark, the MSCI World Index, we can see that the sector weightings are much more in line.

EXG Sector Allocation (Eaton Vance)

Eaton Vance Tax-Managed Global Diversified Equity Income Fund is trading at a meaningful discount on an absolute and relative basis. The distribution cut from well over a year ago was at least partially responsible for getting the fund to trade at a substantial discount. However, the widening of CEF discounts over the last couple of years more broadly clearly played a role as well. Whether the discount will narrow in the future is yet to be determined; though, if history is any guide, we could at least be seeing a level where the discount widening even further could be limited. That makes it a fairly attractive time to consider investing in Eaton Vance Tax-Managed Global Diversified Equity Income Fund.