guvendemir

guvendemir

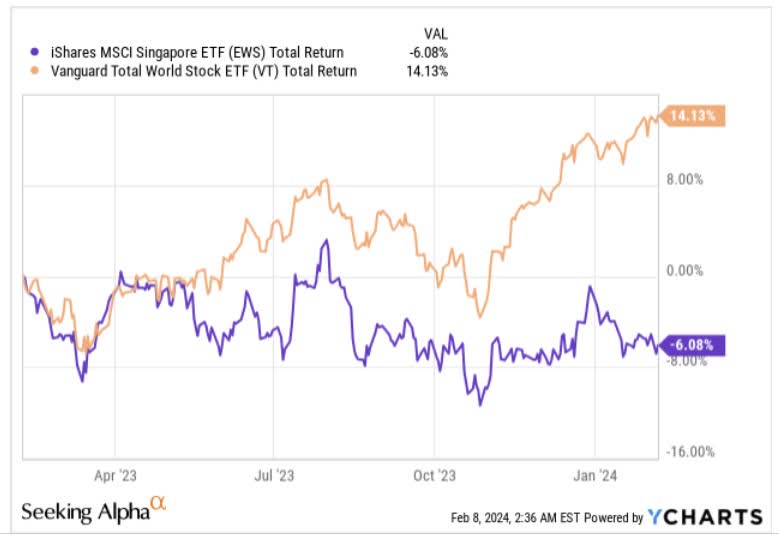

The iShares MSCI Singapore ETF (NYSEARCA:EWS), with 28 years of trading history, is an investment vehicle that offers exposure to 22 large-and-mid-cap stocks in the Singaporean equity market. Over the past year, EWS hasn’t fared too well, witnessing a contraction of mid-single-digits, whilst other global stocks have delivered returns of 14%.

YCharts

Could EWS bounce back in 2024? Well, here's a discussion of some notable themes that could weigh on the ETF's prospects.

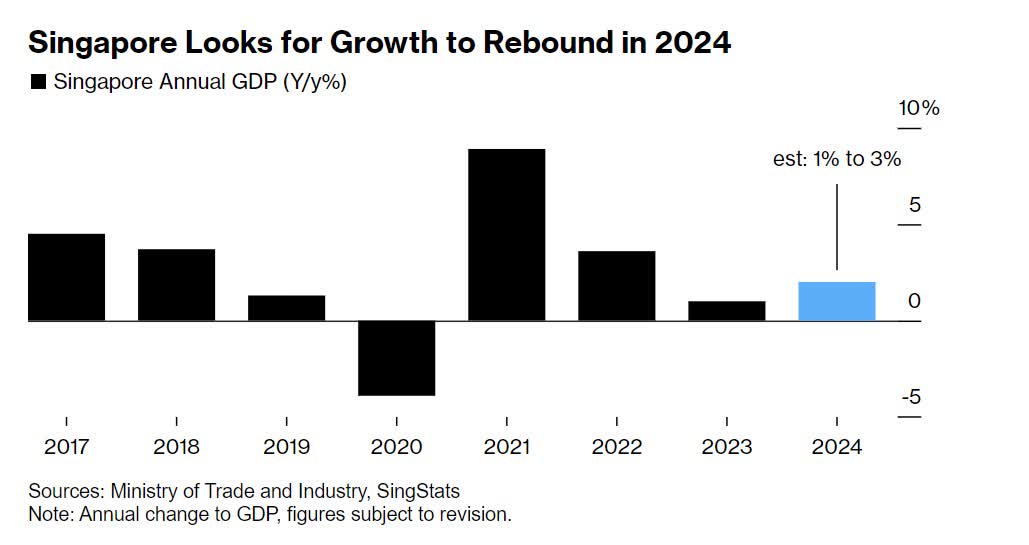

Compared to FY22 where the Singaporean economy grew by 3.6%, real GDP growth in FY23 only came in at 1.2%, and the expectation for the next year is an underwhelming range of 1-3%.

Bloomberg

In contrast, the ASEAN region as a whole (which also includes the likes of Indonesia, Malaysia, Philippines, and Thailand, besides Singapore) is expected to witness superior real GDP growth of 4.7%.

The Singaporean real estate sector, an important cog of the economy, has been impacted by draconian house purchase taxes for foreigners, and a higher interest rate regime, where rates were lifted five times between October 2021 and 2022, and have been left unchanged for the last three MAS (Monetary Authority of Singapore) meetings. For context, last year, less than 6700 housing units were sold, the lowest in 15 years. There are suggestions that the supply side could still remain bloated, as there appears to be a pipeline of 44 projects on the docket.

Interest rates could continue to stay elevated for the foreseeable future, as core inflation trends don’t show any signs of declining. The most recent release highlighted how this grew from 3.2% to 3.3%, and the expectation is that it could remain in a range of 2.5-3.5% in 2024. What could well compound the issue is the fact that GST rates in Singapore have been lifted to 9% (from previous levels of 8%) since the turn of this year.

Singaporean banks may have benefitted from strong interest income trends in light of a higher interest rate environment, but higher funding costs are expected to play a more pronounced role going forward, and loan growth too will remain stunted (expected rate of just 3%), dampening growth of the book value. The underlying prospects of this sector are pivotal to EWS’s fortunes, as they account for nearly half of all of EWS’s holdings. EWS's top three stocks are all banks (DBS Group, OCBC, and United Overseas Bank), and their earnings growth outlook for next year does not look particularly great. The top holding- DBS is staring at a 2% decline, whilst OCBC and UOB will likely only deliver earnings growth of 1.6%-3%.

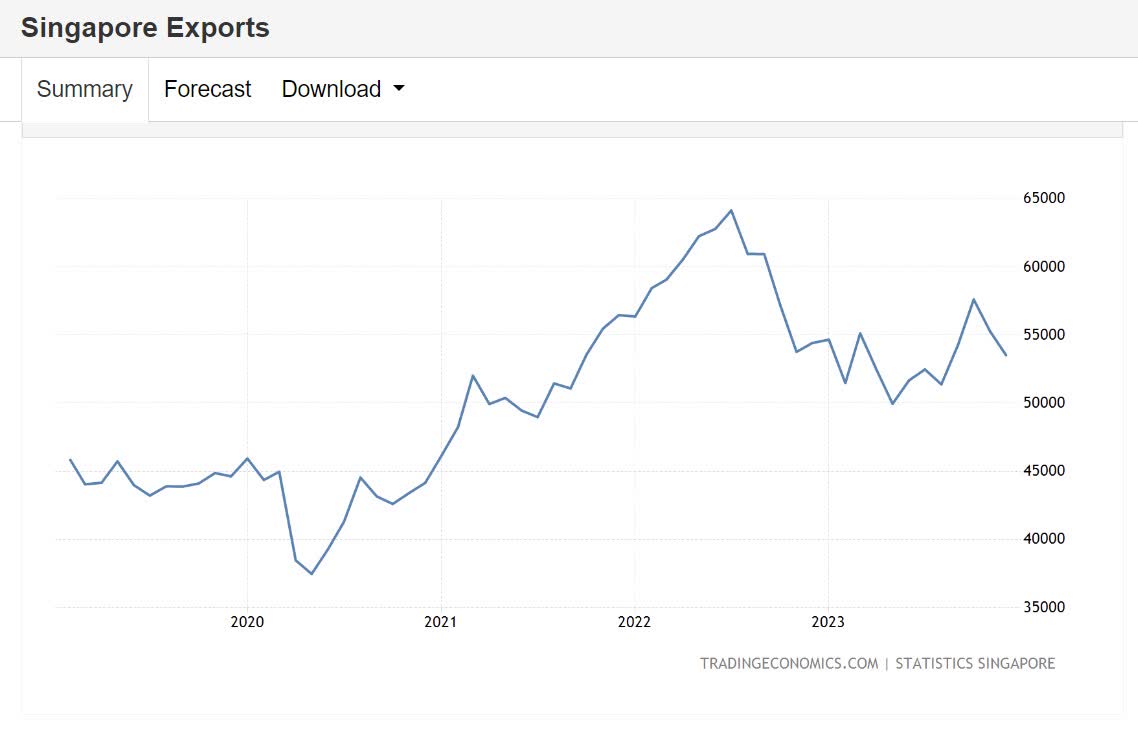

Singaporean exports are another key terrain to watch as they account for 150% of the nation’s GDP. There were signs of an improvement until Q4, but the last three months of the year, have been a disappointment with sequential slides seen through those months.

Trading Economics

On the plus side, the Singapore economy should get some uplift from air traffic and what this means for tourism there. Monthly passenger traffic in December had already recovered to 90% of the pre-pandemic range, and after benefitting from around SGD24.5bn of tourism receipts last year, it looks like this could hit SGD26-27.5bn this year.

Investing

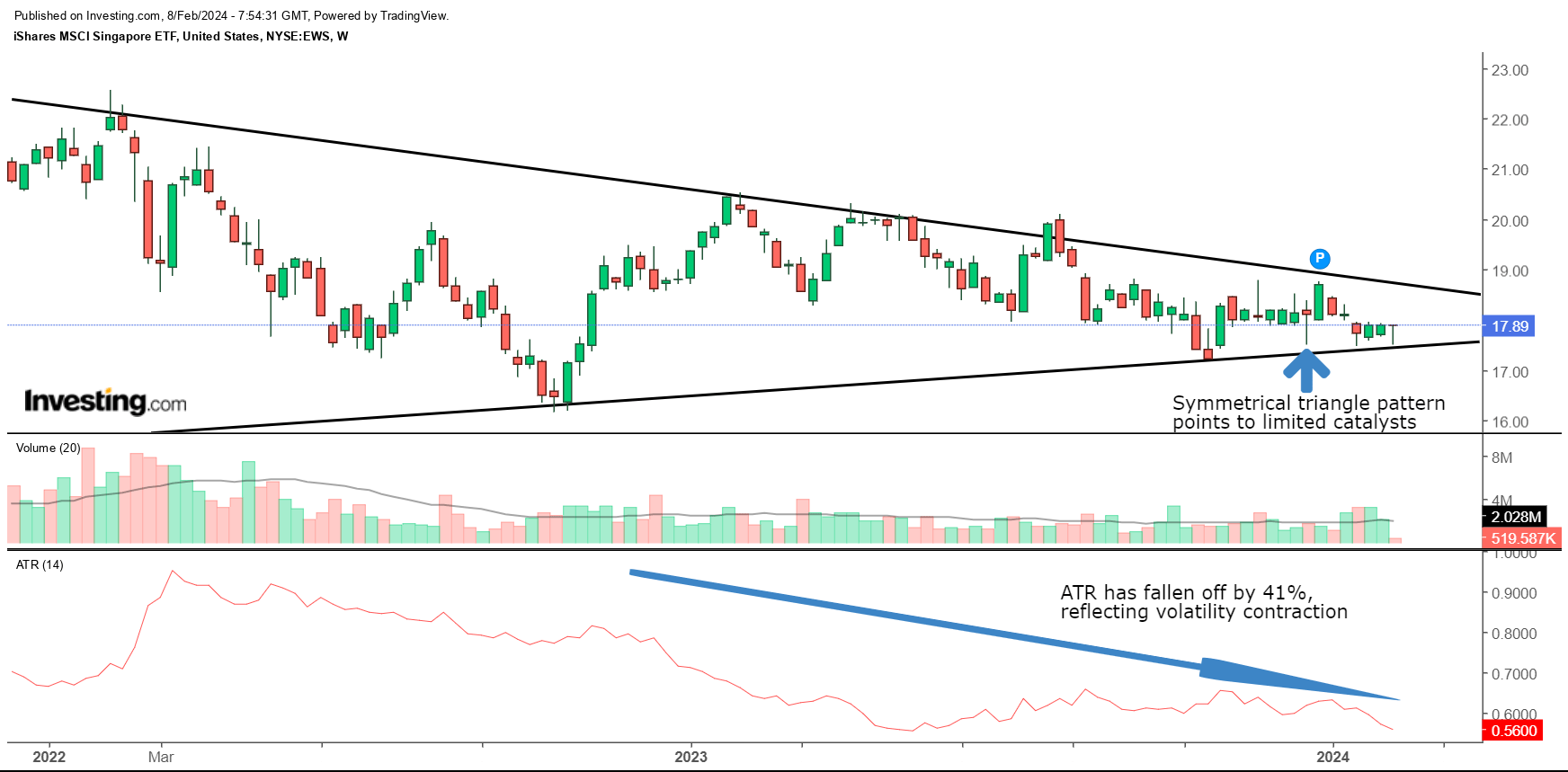

If one takes a look at EWS’s weekly price imprints, what we have is something akin to a symmetrical triangle pattern. Since 2022, we’ve seen a very obvious range contraction, and that is further validated by how the 14-period ATR (Average True Range) indicator has dropped off by 41% from levels seen around two years ago. Put another way, this scenario is broadly indicative of a stock/ETF lacking adequate catalysts to trigger another leg higher or lower. In fact, one can see that from August last year, the ETF hasn’t really gone anywhere.

Now, one could've been tempted to open up a position in EWS if the valuation-to-earnings trade-off was compelling enough, but that does not appear to be the case.

EWS’s valuations are certainly not prohibitive (10.6x P/E), but there’s a good reason behind that. Amongst all the ASEAN regions, Singapore is expected to have the weakest GDP outlook for this year. That coupled with the fact that its dominant financial holdings will likely witness earnings contraction this year doesn’t reflect well on the overall earnings profile. All in all, Morningstar forecasts suggest that EWS's holdings may likely only deliver bland earnings growth of just 3.8%. Contrast that with a diversified product covering South East Asian equities (ASEA), that offers an earnings profile that is more than 3x better (12.4%). ASEA of course is priced at a slightly 8% premium to EWS on a P/E basis (11.55x), but given the superior cadence of long-term earnings on offer, that is justifiable.

Finally, also note that Singaporean stocks aren’t likely to benefit from ample rotation interest within Asia, as its relative strength ratio versus a non-Japanese Asian sample of stocks is already quite close to the mid-point of its long-term range.

StockCharts