pawel.gaul/E+ via Getty Images

pawel.gaul/E+ via Getty Images

Switzerland has proven to be notably resilient throughout the twin crises of COVID-19 and the following surge of inflation that have challenged much of the globe. The country's ability to contain rising inflation and move toward a lower interest rate environment is encouraging. The iShares MSCI Switzerland ETF (NYSEARCA:EWL) provides exposure to a basket of stocks representing this small, but mighty European country. EWL has provided considerable down-side protection and ample return since its inception. However, it isn't cheap and I don't think its opportunity set currently justifies the costs. I rate this as a hold for now.

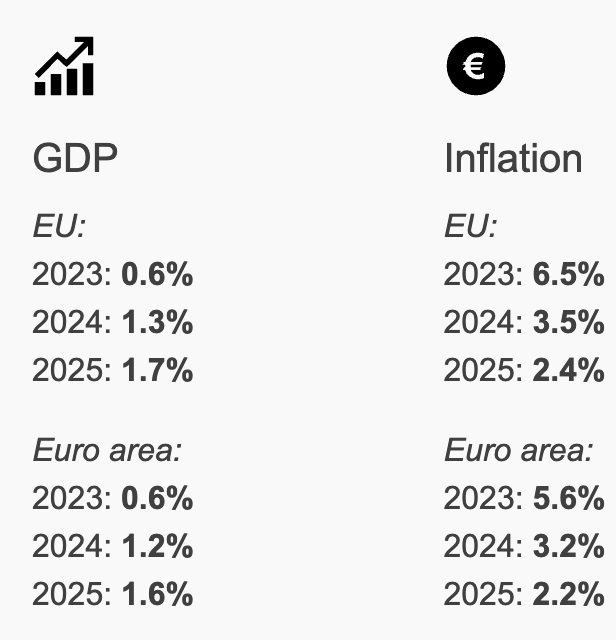

According to the OECD, Switzerland is slated for marginally higher growth in 2024, 0.9% vs. 0.8% in 2023. Growth is then projected to jump still higher in 2025 to 1.4%. While trending positive, these figures come in below both designated EU countries, as well as the broad Euro area, according to the European Central Bank (see figure below).

Switzerland was spared from the more excessive inflation figures found in the Eurozone in 2022 and 2023. Inflation reached 2.28% in 2022, exceeding the Swiss National Bank's target upper limit of 2.0%. Interest rates jumped from negative (-0.75%) in June 2022, to 1.75% in June 2023. Inflation has moderated for the time being and the Swiss Central Bank announced a surprise rate cut in late March, slashing rates backdown to 1.5%. This is the first rate cut in the industrialized West.

ECB

One impetus for the downward revision of interest rates was an appreciating Swiss Franc over the course of 2023, which could prove harmful for manufacturing exports that become more costly to international buyers.

Google Finance

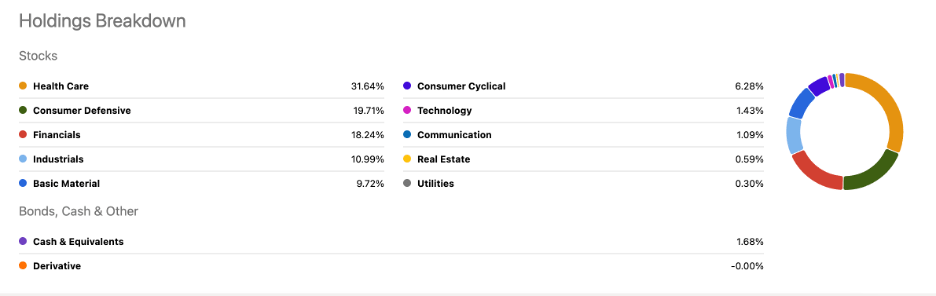

The iShares MSCI Switzerland ETF (EWL) tracks the MSCI Switzerland 25/50 Index which focuses on 53 large and mid-cap stocks in the Swiss Market.

Around a third of the fund is allocated to the Health Care sector (31.64%), while other large sector allocations include Consumer Defensives (19.71%) and Financials (18.24%).

Seeking Alpha

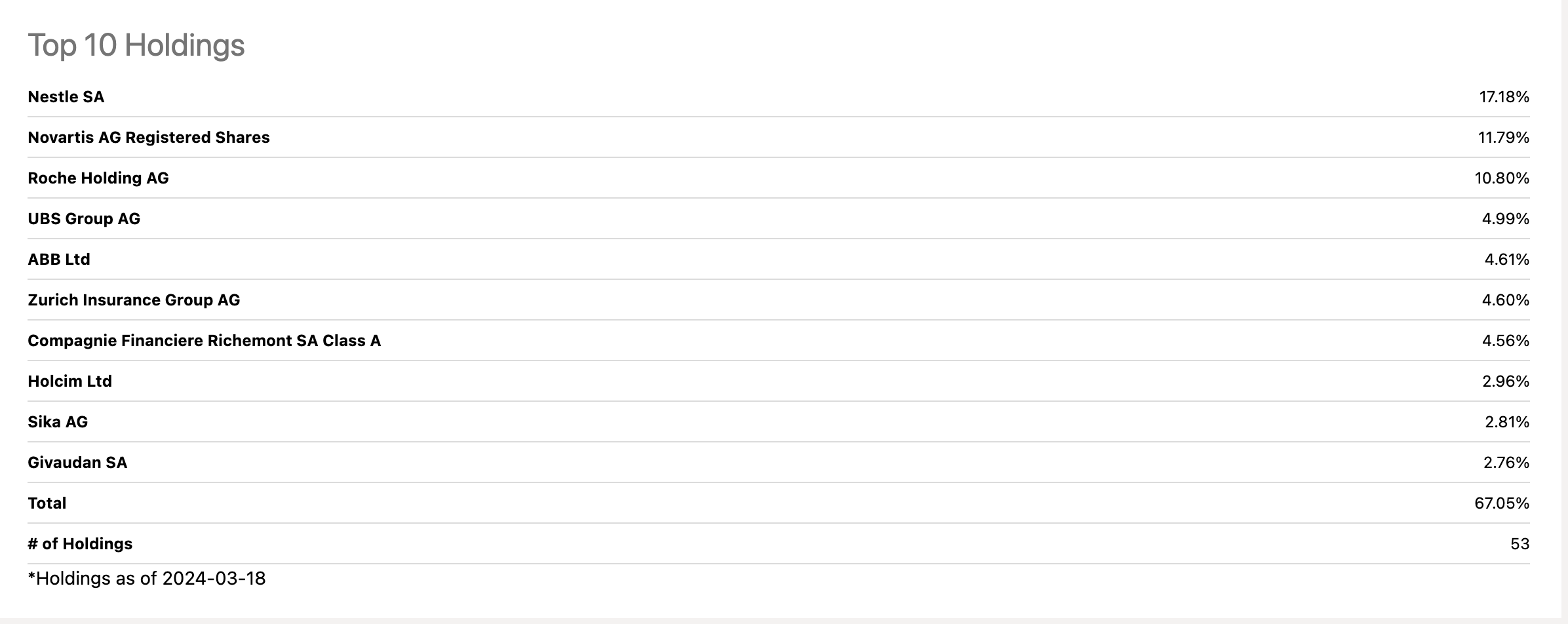

Despite the sector tilts described above, the largest single stock holding to the fund is Consumer Staples giant Nestle SA (OTCPK:NSRGY), which totals 17.18% of all assets in the fund. The next largest holdings, belongs to Novartis AG (NVS) +11.79 and Roche Holdings (OTCQX:RHHBY) +10.80%. These are both large pharma companies headquartered in Basel, with notable accomplishments. Novartis is known for its oncologic products, but it is also reputable for its diverse product set. Total sales are less concentrated in the top 3 products relative to other Pharma companies, which fortifies the company's financials when patens expire. Roche has is a player in the semi-glutide inhibitor space, the weight loss drugs that have exploded in popularity in 2023.

The top 10 holdings total around 67%. This level of concentration is to be expected given the number of holdings and something that I don't see has a deterrent in single country investing.

Seeking Alpha

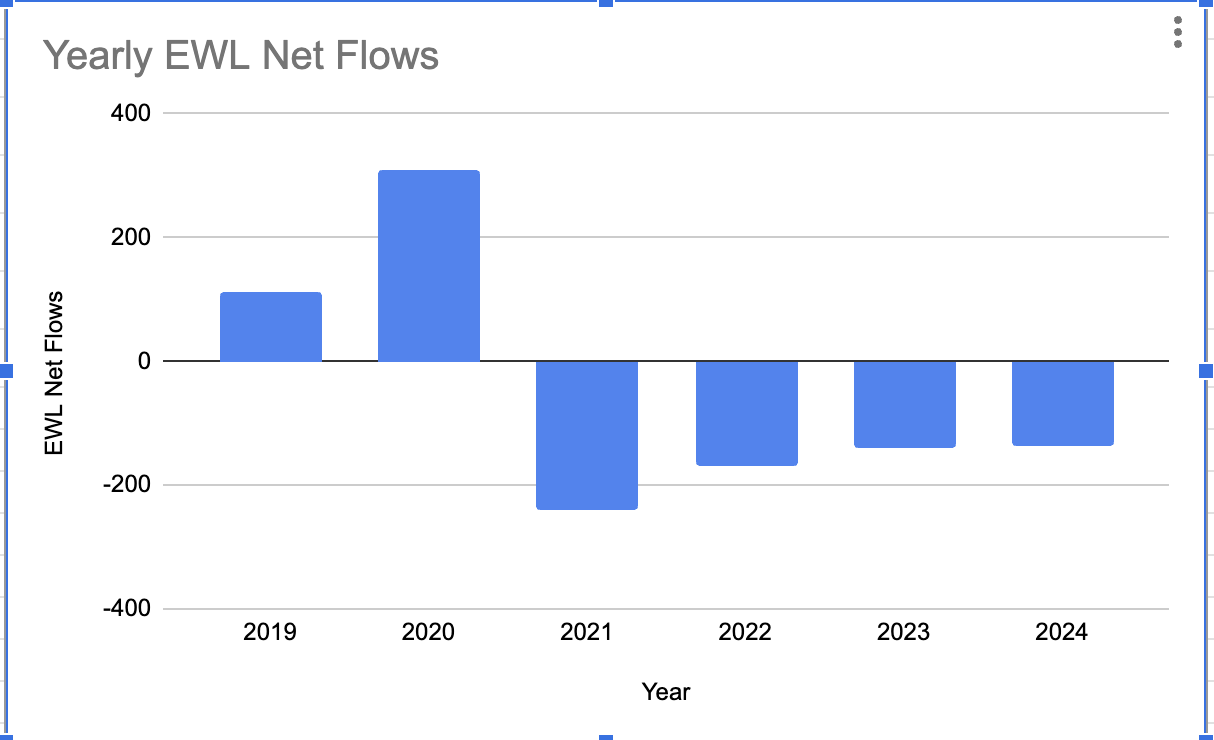

The fund was incepted in 1996 and as of writing currently holds ~ $1.1B in assets. The fund has struggled in recent years, seeing consistent outflows since 2021. Despite outflows, $1.1B is large for a single country ETF and I like that other investors have noticed it is a quality offering.

ETF.COM

EWL is not cheap and it offers a modest yield. It is neither a value nor income play. Currently, EWL is trading 3.64x its book value, while its ratio P/E is 17.71x. It's 12 month trailing yield is 2.18%. For comparison, EWL is more quite a expensive in terms of P/B ratio relative to its European counterparts, and it's P/E ratio is only marginally smaller than the iShares MSCI France ETF (EWQ).

| P/B | P/E | |

| iShares MSCI Switzerland ETF (EWL) | 3.64 | 17.71 |

| iShares MSCI Germany ETF (EWG) | 1.55 | 12.94 |

| iShares MSCI France ETF (EWQ) | 2.08 | 17.87 |

| iShares MSCI United Kingdom ETF (EWU) | 1.72 | 12.65 |

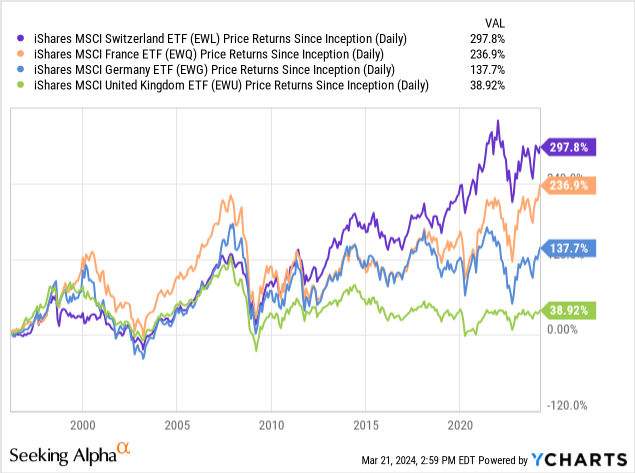

EWL's return profile is impressive. It has managed to outperform other single country European ETFs since 2013 while delivering +297% in daily price returns since its inception in 1996.

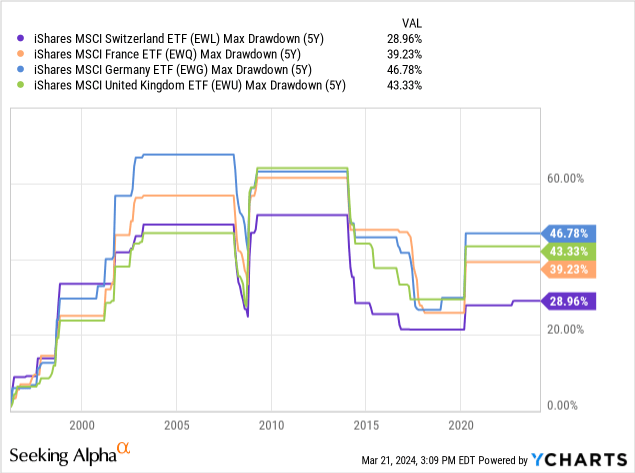

If we compare these European ETFs, taking into consideration the COVID-19 period, we see that EWL has provided better downside protection in periods of market turmoil. Maximum drawdown was between 10% -20% lower than other representative ETFs in the region.

Switzerland has a reputation for being a safe haven, and its representative ETF largely follows in suit. Glaring inflation has not come to pass, and as such its been able to slash rates earlier than expected, which I find promising. EWL's risk-adjusted characteristics are also appealing. However, the fund's current valuation makes me less excited about what it has to offer in the near to medium-term. I rate this as a hold for the time being.