Tim Rue/Corbis Historical via Getty Images

Tim Rue/Corbis Historical via Getty Images

Edwards Lifesciences (NYSE:EW) disclosed their Q4 FY23 results on February 6th. In my previous article, I underscored their recent robust trial data releases. I am particularly encouraged by the recent FDA approval for their EVOQUE tricuspid valve replacement system. Consequently, I reaffirm my 'Strong Buy' rating for EW with a fair value estimate of $98 per share.

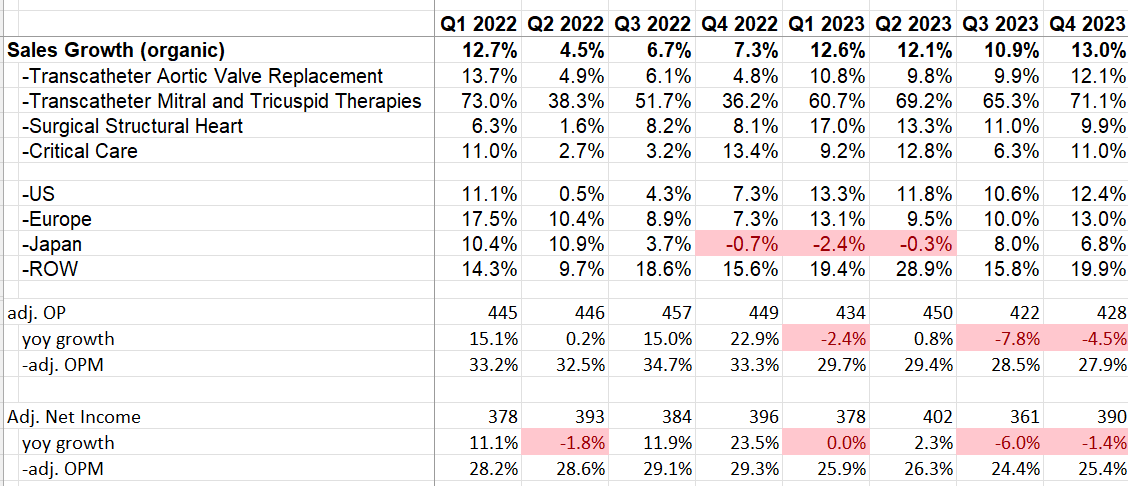

In Q4 FY23, Edwards Lifesciences achieved 13% organic revenue growth and -4.5% adjusted operating profit growth, as illustrated in the table below. Prior to the quarterly earnings announcement, the company received FDA approval for their EVOQUE tricuspid valve replacement system, marking a significant milestone as the first transcatheter therapy for the treatment of tricuspid regurgitation (TR). As highlighted in my previous article, Edwards Lifesciences has consistently demonstrated strength in releasing robust trial data. I am encouraged to see the company's commitment to developing and bringing new products to market for future growth.

Edwards Lifesciences Quarterly Earnings

My key takeaway from the earnings call is Edwards Lifesciences's continued dedication to the structural heart market through the introduction of new product offerings. In December 2023, the company announced its intention to spin off the Critical Care business by the end of 2024. As emphasized during the earnings call, the divestiture of the low-growth Critical Care business is expected to bolster FY25 organic revenue growth by allowing the company to concentrate all resources on the rapidly expanding structural heart market.

Edwards Lifesciences is further expanding its SAPIEN 3 Ultra RESILIA platform, having recently obtained CE Mark approval for the product. The company plans to undertake a disciplined launch in Europe. Given their track record of success in other markets such as the U.S. and Japan, I am confident that SAPIEN 3 Ultra RESILIA will thrive in the European market.

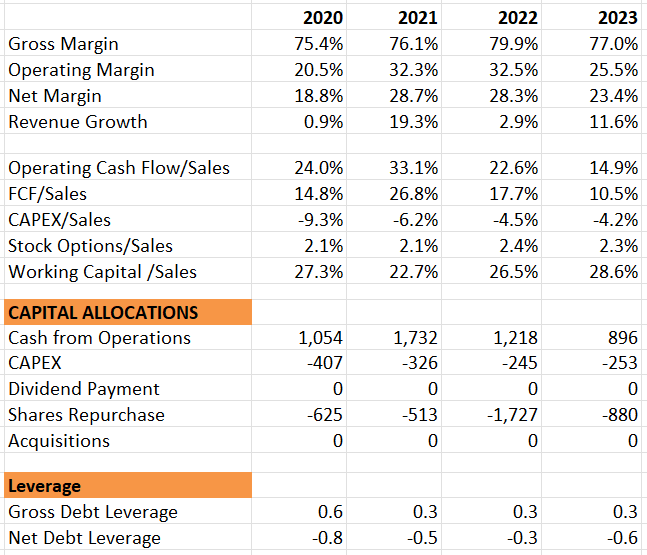

In terms of the balance sheet, Edwards Lifesciences maintains approximately $1.6 billion in cash and cash equivalents, underscoring its robust financial position, as demonstrated in the table below. The company allocated $880 million towards share repurchases and still retains $1 billion in authorization for further share repurchases. Their capital allocation policy remains consistent: prioritizing internal growth while also engaging in selective share repurchases.

Edwards Lifesciences 10ks

For FY24, Edwards Lifesciences anticipates revenue growth of 8 to 10 percent, reaching $6.3 to $6.6 billion, with adjusted earnings per share projected to be $2.70 to $2.80. Several factors contribute to these expectations for revenue growth and margins.

With the FDA approval of their EVOQUE tricuspid valve replacement system, the company is commencing the introduction of this new therapy and providing extensive training to physicians. Their management has indicated the deployment of a dedicated team of clinical case support personnel who have already trained on over 1,000 EVOQUE cases. Tricuspid regurgitation, affecting 1.6 million individuals in the United States and 3.0 million people in Europe according to the National Library of Medicine, represents a substantial market. As the first therapy available in the U.S. to treat this condition, Edwards Lifesciences is expected to gain significant momentum with EVOQUE. The company anticipates full-year sales of Transcatheter Mitral and Tricuspid Therapies to be at the higher end of the previous guidance range of $280 million to $320 million, representing around 4.5% of group revenue in FY24. Additionally, efforts are underway to secure national coverage determination for Medicare patients.

Regarding costs, R&D expenses accounted for 17.8% of total revenue in FY23, with expectations for R&D spending to remain at 17% to 18% in FY24 to support ongoing investment in Transcatheter Aortic Valve Replacement and TMTT technologies. Given the need to maintain technological advantages over competitors such as Boston Scientific (BSX), Medtronic (MDT), and Abbott (ABT), reductions in R&D spending are not anticipated.

SG&A expenses are expected to represent 29% to 30% of total revenue in FY24. This expenditure is deemed reasonable, considering the company's portfolio of products in clinical trials or early stages of launch, including EVOQUE in the U.S. market. The launch of new products entails higher costs for physician training and marketing activities to raise awareness of the new therapy.

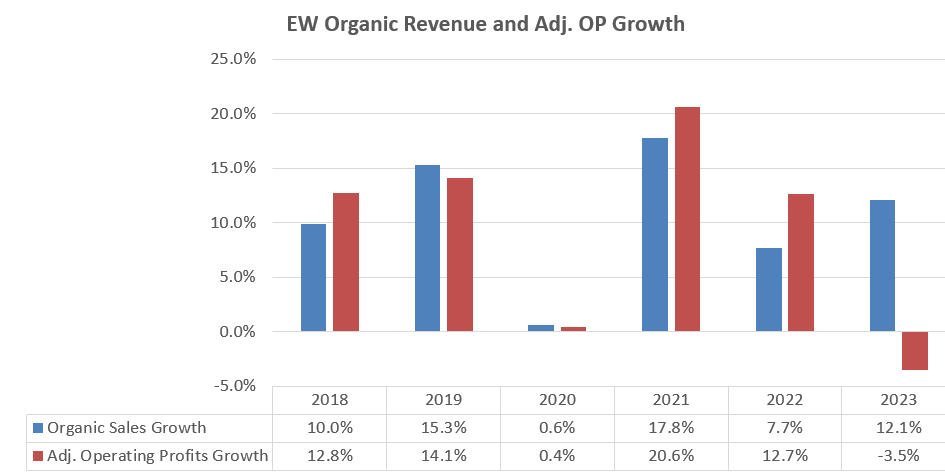

With organic revenue growth of 12.1% in FY23, as illustrated in the chart below, and the anticipated launch of EVOQUE in the U.S. and European markets in FY24, expectations are high for Edwards Lifesciences to achieve even higher growth in FY24.

Edwards Lifesciences 10ks

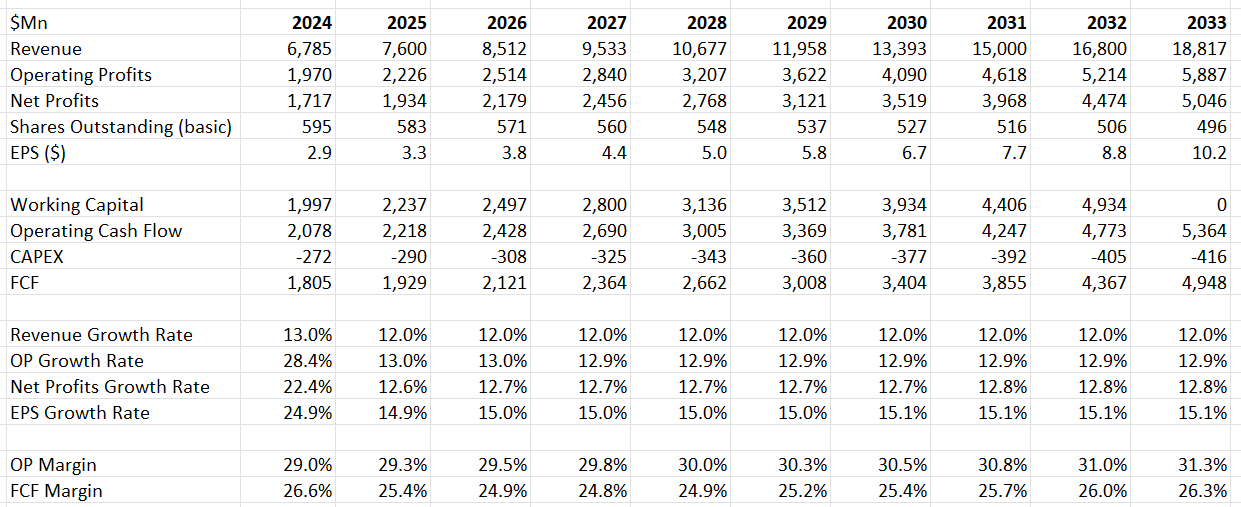

As previously discussed, I anticipate Edwards Lifesciences' FY24 revenue growth to slightly exceed FY23 levels, driven by the EVOQUE launch in the U.S. and Europe. Additionally, the model incorporates a normalized revenue growth rate of 12%, consistent with historical averages. The company's guidance suggests organic revenue growth of 10% or more from FY25 onwards, following the spinoff of the Critical Care business.

Regarding margins, the model assumes that operating leverage will be the primary driver. R&D expenses are estimated to represent around 17.8% of total revenue, in line with guidance. Based on my calculations, operating expenses growth is expected to be 1% lower than topline growth, resulting in margin expansion of 20-30 basis points per year.

With the remaining assumptions unchanged, the fair value of the stock is estimated to be $98 per share. Currently, the stock price is trading at 29 times forward free cash flow.

Edwards Lifesciences DCF - Author's Calculations

The primary risk facing Edwards Lifesciences is the competitive landscape within the structural heart market. Several major medical device companies are seeking to enter this market, posing potential challenges for Edwards Lifesciences. As highlighted in my introductory article, both Abbott and Medtronic are active players in the Transcatheter Aortic Valve Replacement market.

In Q4 FY23, Abbott demonstrated double-digit revenue growth in their structural heart business, driven by the success of MitraClip and other newly launched products. This indicates strong momentum for Abbott in the structural heart market. Similarly, Medtronic achieved mid-single-digit growth in their structural heart business in the recent quarter, albeit lower than their peers.

However, it's worth noting that Edwards Lifesciences enjoys first-mover advantages in the TAVR market. Additionally, the company's exclusive focus on the structural heart market provides another key advantage over its competitors. These factors may help mitigate some of the competitive pressures faced by Edwards Lifesciences in the structural heart segment.

I commend Edwards Lifesciences for their strategic focus on the lucrative Transcatheter Aortic Valve Replacement market, and the recent regulatory approval of EVOQUE represents a significant growth opportunity for the company in the coming years. Therefore, I reiterate my "Strong Buy" rating for Edwards Lifesciences, with a fair value estimate of $98 per share.