3alexd

3alexd

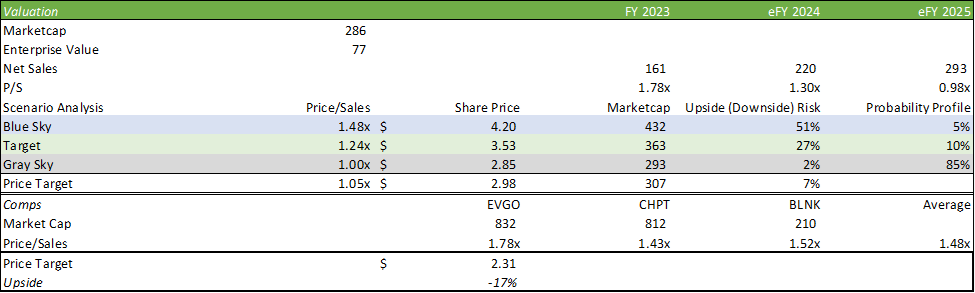

EVgo (NASDAQ:EVGO) reported a significantly strong Q4'23 at the top line with revenue growing by 42% sequentially, a strong continuation of their upward trend. Management appeared very optimistic on the scaling effect of the firm's business model, in which installed charging stations are said to cover the cost to operate net of corporate costs. Despite the optimism, I believe that the macro headwinds in place may be working against EVgo, at least in the near-term, as consumers continue to grapple with high inflation, new waves of corporate layoffs, and shifting consumer preferences in favor of plug-in hybrid vehicles. I maintain my SELL recommendation for EVGO shares, with a price target of $2.31/share at the average TTM price/sales multiple of 1.48x.

Looking at the economy from a big picture standpoint, the underlying figures do not appear as strong as what is showing up in the headlines. One factor that investor Mike Green of Simplify Asset Management referenced on the podcast, Macrovoices, was that the unemployment rate may be artificially lower due as a result of the tradeoff between taking unemployment and driving for rideshare services such as Uber (UBER) and Lyft (LYFT). He suggests that in the near term, this is beneficial to the firms as more drivers are available. He goes on to suggest that in the long term, as more layoffs occur and more drivers become available, the parity shifts to being a negative factor to where there can be more drivers than riders. Looking to the recent February 2024 ISM Services PMI reading:

Employers remain cautious about hiring direct employees and are considering utilizing contract labor to cover project and interim work demands as concerns about the economy continue to be front of mind.

Another comment made by Jim Bianco on the same podcast referenced that the high rate of inflation may not be over and that the Fed cuts may not be in the position of cutting rates as a result.

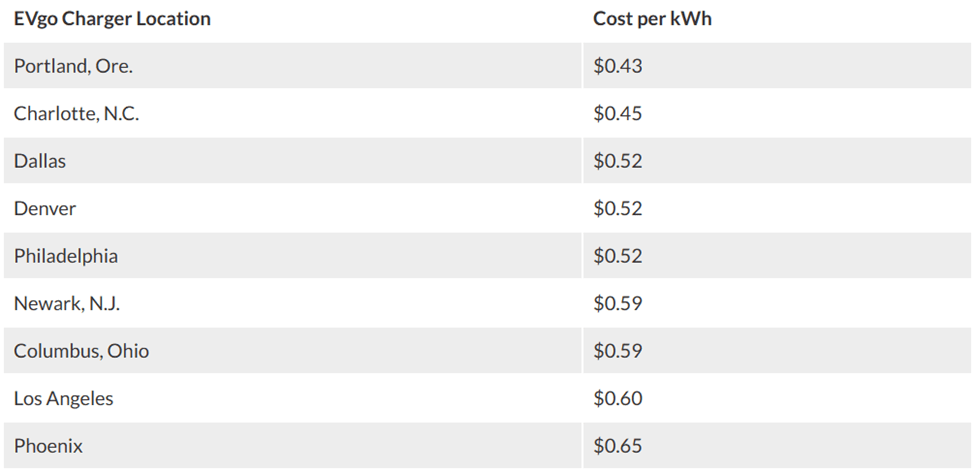

Other implications to EV adoption include insurance premiums for EV owners. According to MarketWatch, insuring an EV can cost between 10-135% more than insuring a traditional ICE vehicle. In addition to this, EVs may have a significantly higher cost to fuel when compared to ICE vehicles. Using data from the same MarketWatch report, EV charging can range from $0.43-0.65/kWh. With EV battery capacity ranging from 28.9kWh to 200kWh for a Mini Cooper SE and a 2022 GMC Hummer EV pickup, respectively, a fill up can really add up in cost. Using the Hummer as an example, filling up to capacity from empty can cost the longer-ranged vehicle between $86-136 when using this charging fee range. Also, in regards to the Hummer, Edmunds reported that the 2023 model has a range of 390 miles with fuel efficiency of 57.8kWh/100miles.

Accordingly, the average daily commute for a US citizen is 40 miles per person, according to the Bureau of Transportation Statistics. Though this data is aged and the work from home vs. in office stats as well as urban vs. suburban are likely to have changed since this report was released, I believe it can continue to stand as a baseline for an example. Tying in the cost to charge, distance, and average commute, a Hummer EV owner may be paying upwards of $23.12/day just to get to and from work! Though this example is at the more extreme end of fuel economy and charging rates, I believe that it offers an eye-opening example regarding the associated costs of owning an EV that may be overlooked by first-time EV buyers and I believe this cohort will take these factors into consideration when it comes time to purchase their next vehicle.

MarketWatch

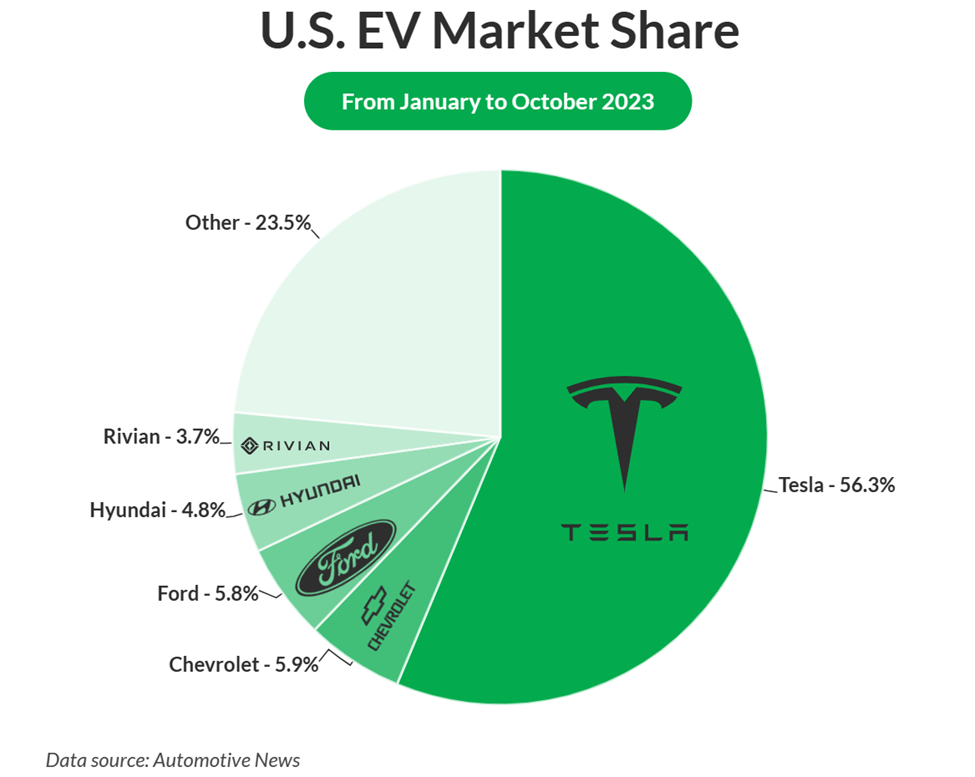

Another factor that may challenge EVgo's growth is the US market share for electric vehicles. Tesla (TSLA) remains as the top EV on the road.

MarketWatch

I believe these last two points relating to cost of fuel and market share will play an important role to EVgo's growth trajectory as the firm heavily depends on non-Tesla EV adoption. I have no doubt that other vehicle adoption will persist. What I'm concerned about is the rate of adoption and whether vehicle owners will cater to EVgo's public charging stations or if consumers will charge their vehicles at work or home.

My takeaway from the q4'23 earnings call was that a large portion of EVgo's demand will derive from rideshare drivers. I believe this will be a driving force for revenue, as I believe drivers would prefer to remain on the road during the day as opposed to being forced to return home to charge their vehicle between rides. I believe this may also improve the demand for fast-charging stations with the presumption that EV drivers choose to remain on the road between riders. My biggest concern, and I referenced this in my previous report covering EVgo, was that fast charging reduces the life of the battery, which is said to be one of the most expensive components of an electric vehicle. Unlike ICE vehicles that can interchange a battery for a few hundred dollars, EV batteries can cost anywhere between $5,000-15,000, according to Edmunds. In tandem with the higher cost to fuel as well as the hour+ charging time, I do not believe there is as strong of a case for ridesharing drivers to purposefully utilize EVs. What I mean by this is that someone that intends to be a driver may not elect to purchase an EV for the sake of taxiing commuters, as opposed to someone who owns an EV that drives on the side or between jobs.

Breaking this out, according to Ride Share Guy, Uber drivers will on average earn $15-20/hr. Making a barebones, baseline assumption that a driver is fully utilized for the hour at a 35mph rate, the Hummer would cost roughly $20.23 for that hour. Again, this is an extreme case at the higher cost of vehicles, but the point remains that the average cost to fuel a vehicle without any consideration for wear and tear significantly eats into the margins for a driver. Given this factor, I believe the case for mass adoption for rideshare EV drivers is broadly overstated, with the exception of some corporate or governmental intervention.

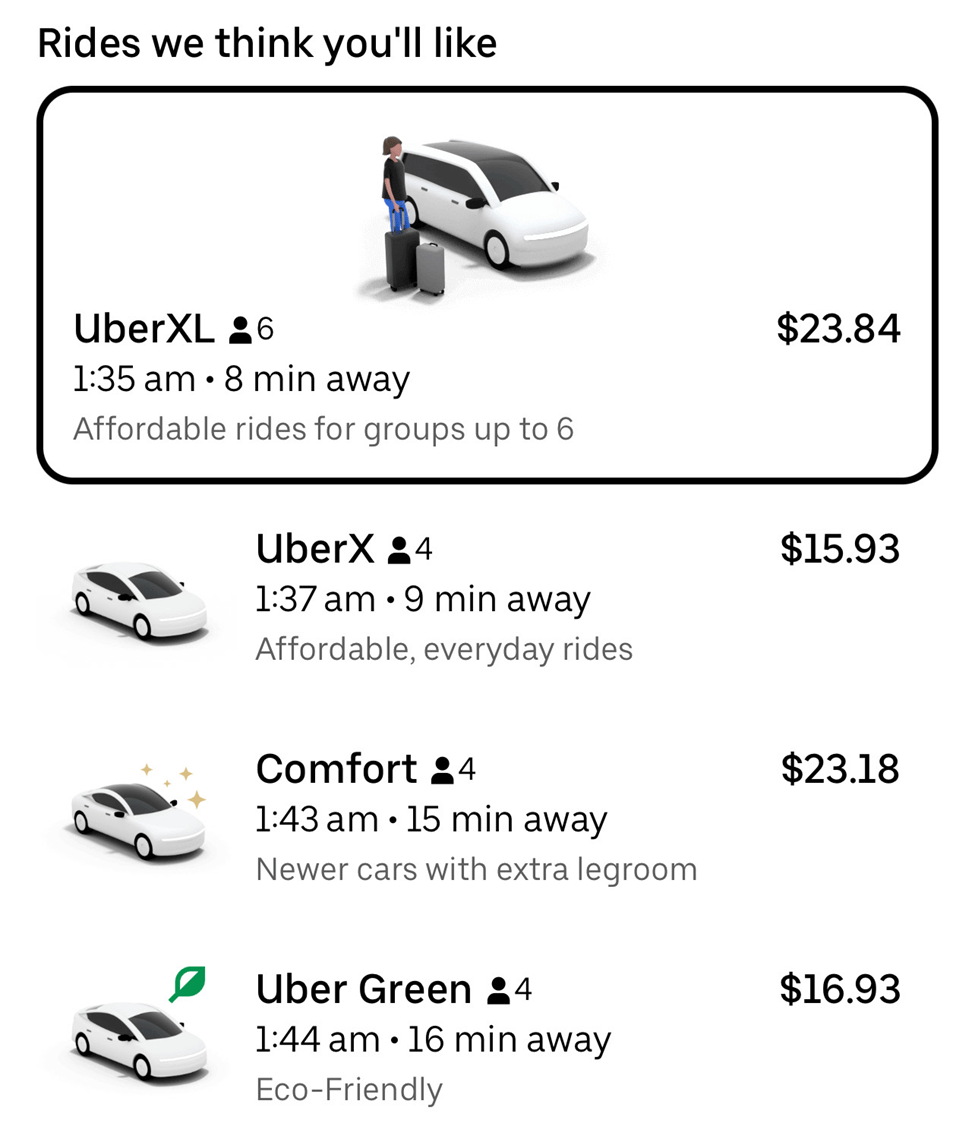

Management did discern that on average, EV drivers using the ridesharing apps command a 5x premium; however, opening my app and searching for a common destination, fees appear relatively flat regardless of whether I take an eco-friendly ride. Tacking on additional costs to the driver, net of surge pricing, demand for eco-friendly rides may further eat into the costs of the EV rideshare driver. Though this is advantageous to EVgo as the firm acts as an EV power utility, this can be a major deterrent to a driver.

Uber

For these reasons, I am modeling EVgo to come in at the lower end of their revenue guidance at $220mm for eFY24. Even with this figure, I believe it is very optimistic as it relates to the adoption of electric vehicles and the case for public charging.

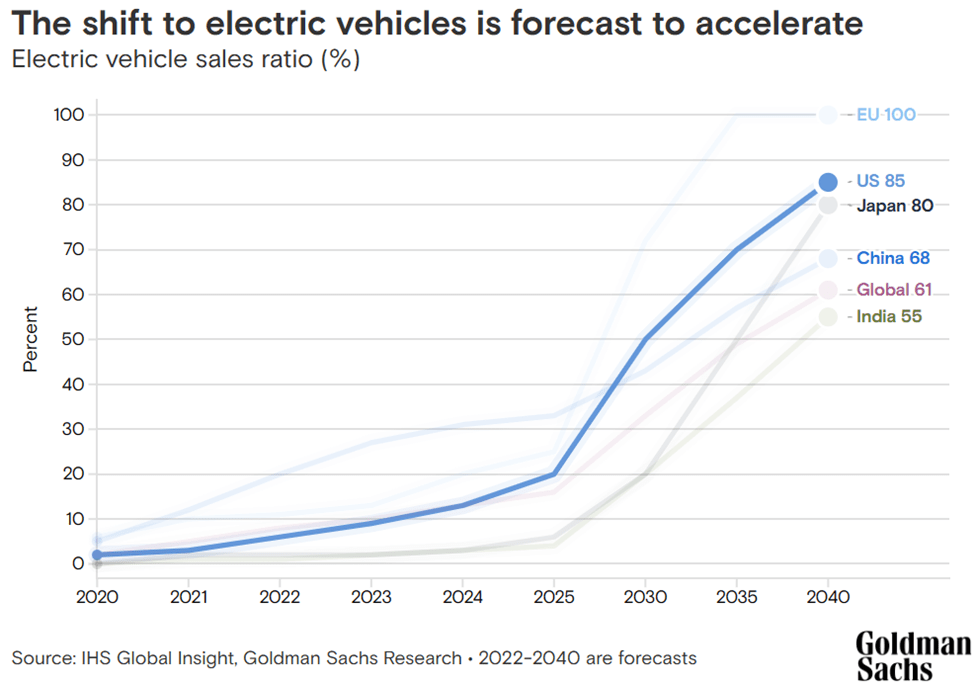

One factor that I do find value in is that the firm has the potential to reach some profitable figure as charging stations scale with the assumption of an average 19% utilization rate as seen in FY23. Management discerned that on the ground charging stations operate profitably, which is a promising factor. Overall, I do not anticipate EVgo to be profitable in the near-term and may not be profitable until as late as 2030 or beyond, as Goldman Sachs analysts anticipate EV adoption to really begin to take off in the US in the 2025-2026 timeframe.

Goldman Sachs

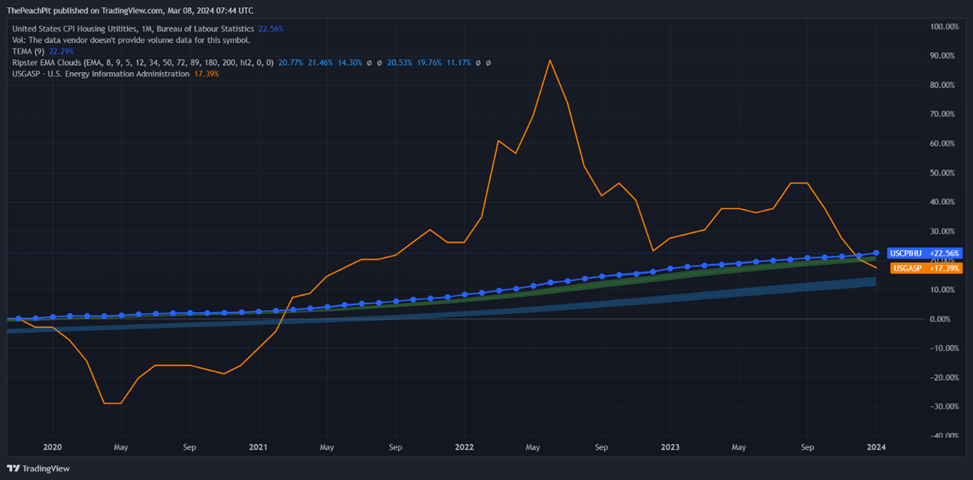

Considering that gasoline prices and utility costs have grown at a relatively similar rate since 2020 may make weighing the differences in vehicle adoption a muted argument, assuming a one-for-one fuel economy between mph and kWh equivalencies.

TradingView

In terms of other associated costs that may be factored into the rate of adoption, I believe financing costs may play a major role in EV adoption, as domestic EVs tend to be sold at an average $10k premium over ICE vehicles. In terms of loan rates, Bankrate is currently reporting rates in the range of 6.84-15% for an auto loan.

Corporate Reports

EVgo experienced revenue growth across all segments, with their commercial segment, growing 56% sequentially. EVgo should be able to maintain this level of revenue growth as more consumer and commercial vehicles are placed on the road. According to CarEdge, EV sales captured 8.1% of total vehicle sales in q4'23 with total CY23 EV sales reaching 1.19mm.

Management anticipates a EBITDA to break even in eFY25 through EV VIO growth and stronger adoption and utilization of the network. Management discerned that they are targeting new regions on a very strategic basis to maximize utilization rates and anticipates to install between 800-900 new stalls in eFY24. Customer adoption has significantly grown across the network, with FY23 ending with 884k customer accounts. The average daily throughput per stall for December 2023 was 200kWh, equivalent to one 2023 Hummer EV per day.

Corporate Reports

On top of this, EVgo has a diminishing cash position with a significantly dilutive share count. I do anticipate cash burn to slow down as the firm nears profitability, and I do not believe solvency to be of concern.

Corporate Reports

Corporate Reports

EVGO shares currently trade at 1.78x FY23 sales. Valuing EVGO shares will pose a challenge as their forward valuation appears appealing; however, on a comparable basis, EVGO shares are priced at a premium. Using the macro narrative laid out above as a guide, I will recommend the more bearish case for EVGO shares, as I anticipate the firm to undershoot on profitability and reach the low end of revenue guidance.

Corporate Reports

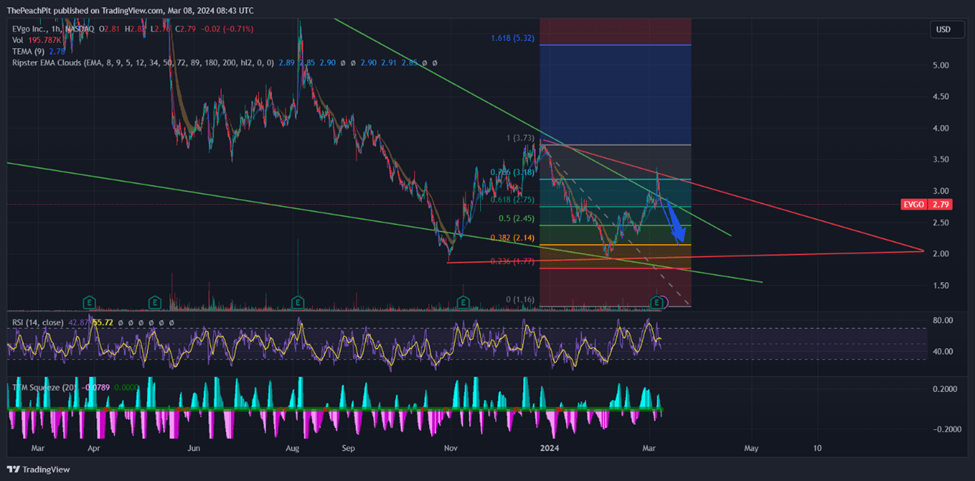

The technical chart shows the share going through an inflection point. I can see shares having three pricing floors, one at ~$2.16, one at ~$1.95, and the bottom floor at ~$1.71. Given the downward trend in the pricing data when using the Ripster EMA Cloud and RSI, I believe that EVGO shares may continue this downward trajectory in the short term. I believe that any signs of headline economic strength that may lead to a continuation of high-interest rates and an easing consumer market may pose as a challenge to EVgo's story. Upside risk is very much a potential, as EVgo may come to bat and report stronger revenue growth and margins than anticipated. I believe that given the current valuation, any good news for EVgo will act as releasing a tightly wound-up spring and will result in significant upside risk in share value. I believe analysts and traders will be most focused on signs of profitability before rewarding shareholders. I maintain my SELL recommendation with a price target of $2.31/share.

TradingView