Bet_Noire

Bet_Noire

The Eaton Vance Tax-Managed Diversified Equity Income Fund (NYSE:ETY) is a closed-end fund that can be employed by investors who are seeking to earn a high level of income from the assets in their portfolios but do not want to give up all of the potential capital gains that accompany an investment in common equities. Unfortunately, the fact that this is an equity closed-end fund means that its yield is going to be a bit lower than some other funds that are available in the market, as its current 7.38% yield cannot really compete with the better fixed-income funds. In fact, some other equity funds that employ options strategies such as the BlackRock Enhanced Equity Dividend Trust (BDJ) also boast higher yields. With that said, the Eaton Vance Tax-Managed Diversified Equity Income Fund still has a substantially higher yield than the 1.31% currently paid out by the S&P 500 Index ETF (SPY). The fund's current yield is also quite a bit higher than safe fixed-income options such as Treasury securities and money market funds. As such, income investors may be reasonably satisfied here, even if the fund is not the highest-yielding option in the market right now.

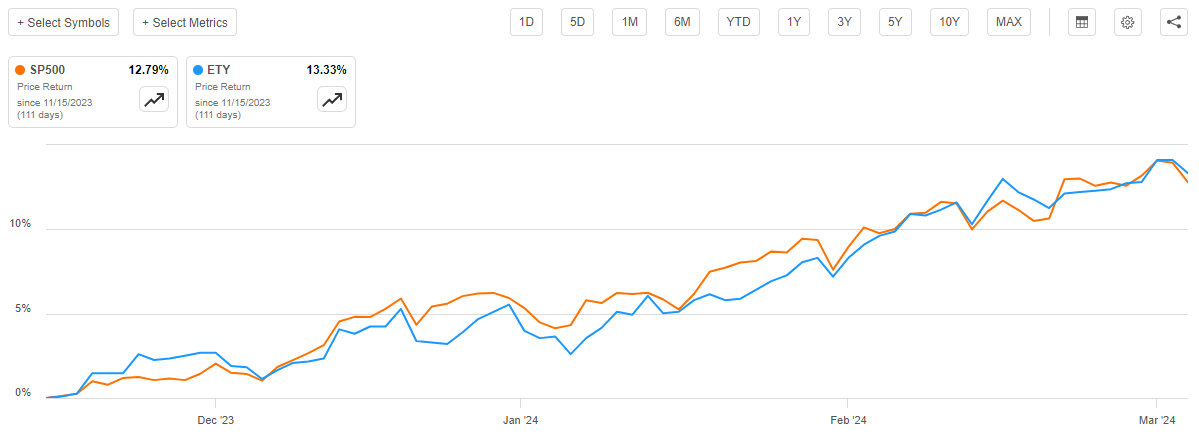

As regular readers can likely remember, we previously discussed the Eaton Vance Tax-Managed Diversified Equity Income Fund in mid-November 2023. The equity market has generally been pretty strong since that time, as the S&P 500 Index (SP500) is up a whopping 12.79% since November 15, 2023. That is better than the historical average annual return of this index. As such, we might expect that the Eaton Vance Tax-Managed Diversified Equity Income Fund has also had a fairly strong run, although the fund's option-writing strategy component will ordinarily reduce its performance somewhat. Curiously though, this has not been the case this time as the fund's share price has actually outperformed the index. As we can see here, shares of the fund are up 13.33% since my previous article on it was published:

Seeking Alpha

It is certain that just about any income-focused investor will find this recent performance attractive. After all, it is somewhat unusual for shares of a closed-end fund to outperform any market index due to the simple fact that closed-end funds typically pay out all of their investment profits to the shareholders. They do not rely on share price appreciation to provide investors with a return, as an index fund does. This is the reason why closed-end funds such as this one typically have much higher yields than most other things in the market.

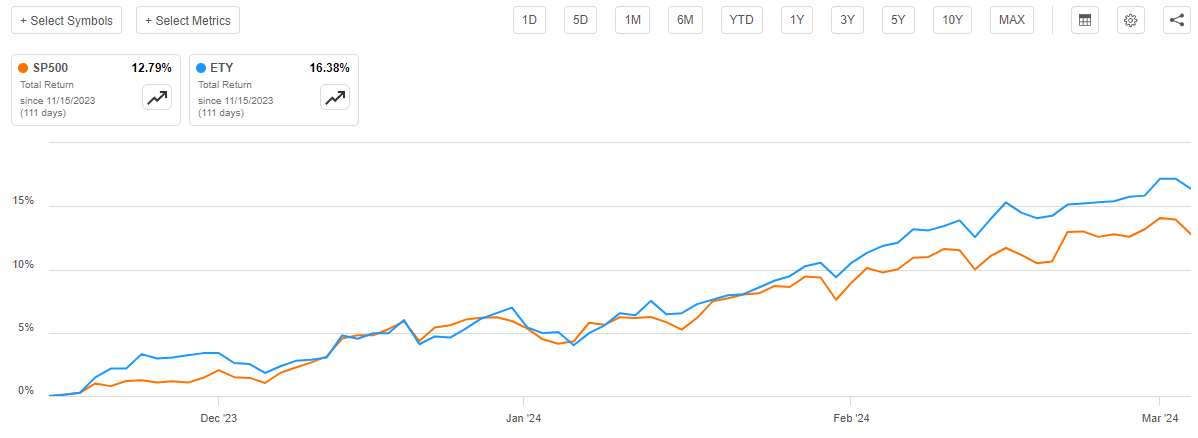

We can see that the fund's performance compared to the index is even more impressive when we consider the impact that the fund's distributions have had on its returns. After all, the direct payments that the fund provides to its investors represent real profits to the investors that increase their wealth regardless of the fund's share price movements. This will always result in the investors receiving a better return than the share price movement alone will indicate. As we can see here, the fund's investors actually received a 16.38% total return since mid-November compared to only 12.79% for the S&P 500 Index:

Seeking Alpha

Obviously, this represents a substantial amount of outperformance, and everybody likes outperformance relative to a benchmark index. A 16.38% return in less than four months is obviously something that anyone can appreciate, including income-focused investors who may sometimes be willing to accept a smaller return in exchange for a high yield.

However, the fund's strong performance may be misleading, as the underlying portfolio did not outperform the S&P 500 Index over the period (although it did once we consider the distribution). This suggests that the share price may have gotten ahead of itself, which is something that we want to investigate. After all, we never want to overpay for any funds. The fund also released its annual report since the time of our previous discussion, so we want to have a look at that as well and determine how well it is actually covering its distribution.

According to the fund's website, the Eaton Vance Tax-Managed Diversified Equity Income Fund has the primary objective of providing its investors with a high level of current income and current gains. However, as is frequently the case with Eaton Vance funds, the website does not provide any information about how exactly the fund is aiming to achieve this objective. Fortunately, the fund's fact sheet provides more information:

The Fund invests in a diversified portfolio of domestic and foreign common stocks with an emphasis on dividend paying stocks and writes (sells) S&P 500 Index call options with respect to a portion of the value of its common stock portfolio to generate cash flow from the options premium received. The Fund evaluates returns on an after tax basis and seeks to minimize and defer federal income taxes incurred by shareholders in connection with their investment in the fund.

This is another one of Eaton Vance's option-income funds, which is actually a little confusing considering the fund's name. Indeed, the fund's name would very easily lead one to believe that this is a fund that is using a dividend-investing strategy, perhaps with the addition of a bit of leverage to boost the effective yield of the portfolio. There are a number of other closed-end funds that do follow such a strategy, including Eaton Vance's own Eaton Vance Tax-Advantaged Dividend Income Fund (EVT). The Eaton Vance Tax-Managed Diversified Equity Income Fund is very different, as the fund employs no leverage and relies on the options strategy to provide it with income.

As the description above states, the fund writes options against the S&P 500 Index in order to receive a premium that essentially provides it with income, although not without risk. However, the description does not state what options it is actually writing on the index with respect to term length or the degree to which the options will be in-the-money or out-of-the-money at the time of writing. These two factors are quite important because they determine the profitability of this strategy. According to the Corporate Finance Institute:

The majority of index options are serial, i.e. they mature in March, June, September, and December. However, there are notable exceptions, such as KOSPI options, which mature every month for the first three consecutive months and then serial afterward.

Despite this claim though, I can actually pull up S&P 500 Index call options with expiration dates on every single trading day in the entire month of March on Bloomberg and most of them do exhibit some volume. Thus, the fund could conceivably be selling options with just about any expiration date that it wants.

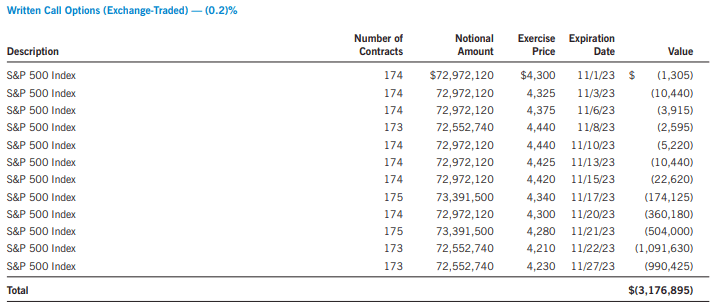

Unlike the fund's common equity portfolio, the fund does not publish regular releases detailing its option positions. We can, of course, find these in the fund's annual report, which will tell us what options the fund was short as of October 31, 2023. Here is what the fund had on that date:

Fund Annual Report

As we can see, as of the end of October, the fund had short option positions expiring on various days in November. It had no other options positions on that date, which suggests that the fund is only writing short-term index call options.

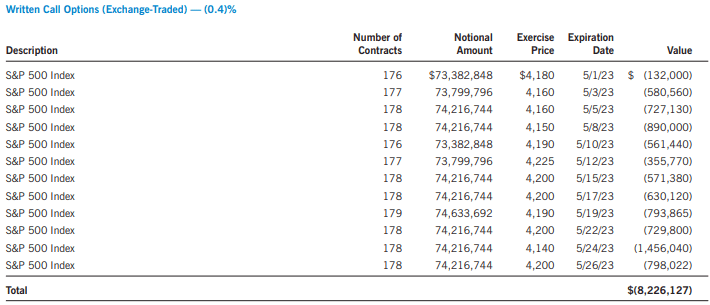

The fund's semi-annual report provides a list of the fund's option holdings on April 30, 2023:

Fund Semi-Annual Report

As of April 30, 2023, the fund only had short options positions with strike prices expiring in May. They did represent a larger position of the portfolio at that time, but still represented a very small proportion of the portfolio.

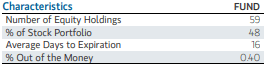

This appears to suggest that the fund is only writing very short-term index call options, such as those that expire in less than a month from the date of writing. The fund's fact sheet says that the fund's option positions had an average of sixteen days until maturity as of December 31, 2023, so that appears to confirm this assumption. However, the fact sheet also says that 48% of the portfolio was overwritten at that time, which at first glance appears to conflict with the much lower percentages provided in the annual and semi-annual reports. However, the annual and semi-annual reports both specify "exchange-traded options," which suggests that the fund is simply doing most of its options trading in the over-the-counter markets.

It is probably a good thing that the fund is mostly writing index options with short maturity dates. As everyone reading this is no doubt aware, the market has been on something of a tear over the past few months as various participants became very excited about the prospects of a pivot in monetary policy. While it seems highly likely that this pivot will not occur to anywhere near the degree that the market is anticipating, the market rally has continued and as we saw in the introduction, the S&P 500 Index has risen at a rate substantially above its historical average over the past few months. As such, there would be a very real risk that long-dated options could go deep in the money if this rally continues. A short-term option has less of a risk of handing the fund significant losses in such an environment. With that said, the fund's fact sheet does state that most of the short options that the fund was liable for as of the start of this year were in the money:

Fund Fact Sheet

As we can see, the fund's fact sheet says that 0.40% of the fund's options positions were out-of-the-money. This implies that just about all of its options were losing positions and the fund will need to pay out cash to settle them once they expire. After all, index options are always cash-settled because it is not possible to own an index. Thus, the fund suffers an actual outflow of cash when an option expires in the money (although it will try and buy it back at a loss in such cases) so the more that can be limited, the better.

In the quote from the fact sheet describing the fund's strategy (shown above), it is explicitly stated that this fund emphasizes investing in dividend-paying common stock for the non-options portion of its strategy. However, as I pointed out in previous articles on this fund, that is not exactly true. We can see this by looking at the largest positions in the fund's portfolio:

Eaton Vance

Here are the dividend yields of these companies:

Company | Current Yield |

Microsoft (MSFT) | 0.75% |

Apple (AAPL) | 0.56% |

Amazon.com (AMZN) | 0.00% |

NVIDIA Corp. (NVDA) | 0.02% |

Meta Platforms (META) | 0.10% |

Alphabet (GOOG) | 0.00% |

AbbVie (ABBV) | 3.46% |

Eli Lilly (LLY) | 0.67% |

Walmart Inc. (WMT) | 1.38% |

Accenture (ACN) | 1.37% |

Admittedly, this is technically not as bad as the last time that we discussed this fund. Now that Meta Platforms actually pays a dividend, only two of the fund's top ten holdings have none at all. However, we can see that the overwhelming majority of the companies shown here have yields that are so low that they may as well not pay a dividend. The only stock with a yield that is likely to be attractive to most dividend investors here is AbbVie. The rest of the others are pretty much just capital gains plays. While this is probably okay as the fund can always sell off stock and realize capital gains to get money to distribute to the shareholders, it does result in the fund's claims about preferring to invest in dividend-paying securities being slightly misleading for some potential investors.

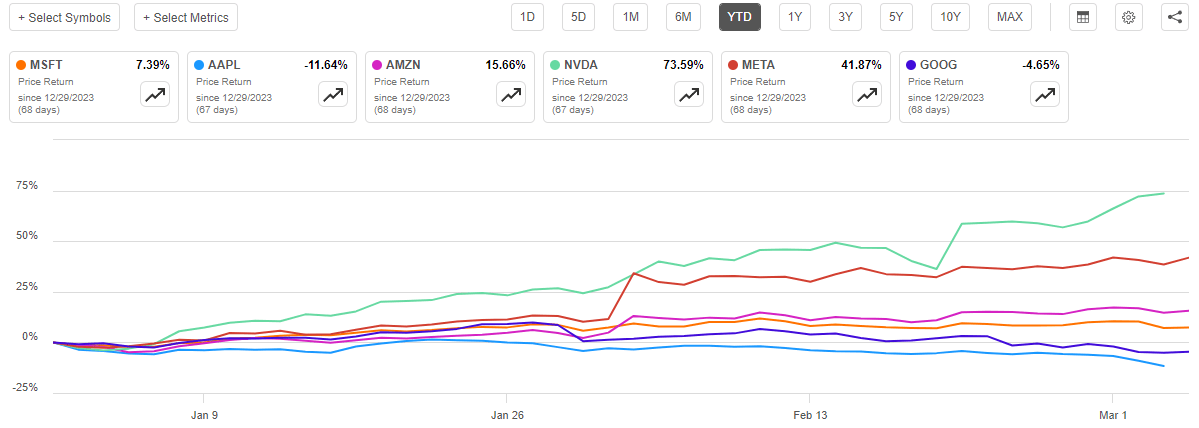

The largest positions in the fund are largely the same as the last time that we discussed it, although some of the weightings have changed significantly. The only change of note is that Mastercard (MA) was removed from the fund's largest positions and replaced with Accenture. The remainder of the changes that we see here are related to the weightings of the various securities in the fund's portfolio and this could be explained by one asset simply outperforming another in the market. Indeed, most of the large technology companies whose shares are included in the fund's largest positions list have delivered a very strong performance year-to-date:

Seeking Alpha

We can see that only Apple and Alphabet have been disappointing, and much of Alphabet's poor performance was driven by the negative criticism that certain vocal individuals and institutions levied against its Gemini AI product. It is uncertain how much of an impact that will have on the stock price going forward. Apple's problems run deeper, as I pointed out in a recent article. In short, Apple's growth has been negligible over the past few years as all of its earnings per share gains were driven by a stock buyback program. Apple is also generally perceived as a laggard in artificial intelligence technology, which has been the driver of recent share price gains at the other companies shown above. It is possible that these two stocks will weigh on the fund going forward. Apple's performance in particular is somewhat concerning as it accounts for such a large portion of the fund's overall portfolio. However, all of these companies are also very highly represented in the S&P 500 Index (as well as in many other equity open-ended and closed-end funds) so any underperformance by one of them would almost certainly spread across the broader market.

As mentioned earlier in this article, the primary objective of the Eaton Vance Tax-Managed Diversified Equity Income Fund is to provide its investors with current income and current gains. In pursuance of this objective, the fund invests its assets in a portfolio of common stocks. Some of these common stocks pay dividends, which provides the fund with a source of income, but as we saw earlier, the yields on many of the largest-weighted stocks in the fund are so low that its income from dividends is not going to be a major source of income for the fund. Rather, the majority of this fund's income comes from the options strategy, which involves the fund receiving an upfront premium from the sale of S&P 500 Index options. The fund also can realize gains from trading the common stocks in its portfolio, which also represent an inflow of new cash. The fund pools together all of the money that it receives from these various activities and pays it out to its own shareholders, net of its expenses. When we consider how high the potential effective yield from an options-writing strategy and capital gains in a given year can be, we can see how this would probably allow the fund's shares to boast a fairly high yield.

This is indeed the case, as the Eaton Vance Tax-Managed Diversified Equity Income Fund currently pays a monthly distribution of $0.0805 per share ($0.9660 per share annually), which gives it a 7.38% yield at the current share price. As mentioned in the introduction, this is not an especially impressive yield for a closed-end fund, but it is still quite reasonable for an equity closed-end fund in today's market environment. For the most part, this fund has been pretty reliable with respect to its distribution over the years, although it did have to cut the payout in response to the monetary policy changes in 2022:

CEF Connect

Unfortunately, the fund's current monthly distribution is slightly worse than the $0.0843 per share that it paid out prior to the pandemic. That previous distribution had been pretty stable throughout most of the 2010s so the increase and then a larger cut could be a bit of a turn-off for those who are seeking a very consistent level of income. However, the fund's current distribution is not really that much lower than what it had prior to the pandemic, and overall, this fund has been much more consistent than most closed-end funds over the past decade.

As I have pointed out in various previous articles though, the fund's distribution history is not necessarily the most important thing for anyone who is considering purchasing shares of the fund today. This is because today's buyer will receive the current distribution at the current yield and will not be adversely affected by changes in the fund's distribution that occurred in the past. The most important thing for any buyer today is that the fund is able to maintain its distribution going forward. Let us investigate this.

Fortunately, we do have a very recent document that we can consult for the purposes of our analysis. As of the time of writing, the most recent financial report for the Eaton Vance Tax-Managed Diversified Equity Income Fund is its annual report that corresponds to the full-year period that ended on October 31, 2023. A link to this document was provided earlier in this article. This is a much newer report than the one that we had available to us the last time that we discussed this fund, which is rather nice to see. After all, this report will give us a better understanding of how well the fund performed during the summer of 2023, which was characterized by pessimism as investors began to realize that their expectations of a pivot by the Federal Reserve in the second half of 2023 were unlikely to come to fruition. This caused many common equities to decline in price, which could have had an adverse effect on the fund and resulted in some losses across its portfolio. This financial report should give us a good idea of how well the fund managed to handle this situation.

During the full-year period, the Eaton Vance Tax-Managed Diversified Equity Income Fund received $27,071,286 in dividends from the investments in its portfolio. When we combine this with what the fund calls "Other Income," we see that it had a total investment income of $28,988,677 over the full-year period. The fund paid its expenses out of this amount, which left it with $8,993,079 available for shareholders. As might be expected, this was nowhere close enough to cover the distributions that this fund paid out to its investors. Over the full-year period, the fund distributed $151,924,121 to its shareholders. At first glance, this might be concerning, as the fund clearly did not have sufficient net investment income to fully cover its payouts.

However, there are other methods through which the fund can obtain the money that it requires to cover its distributions. For example, it might be able to sell some appreciated common stock and realize capital gains. It also receives some money from the sale of index options. Realized capital gains and received option premiums are not considered to be investment income for accounting for tax purposes, but they obviously do result in money coming into the fund that can be paid out to the shareholders.

The fund, fortunately, had a great deal of success at earning money through these alternative methods during the period. Over the course of the year, the fund achieved net realized capital gains of $136,768,968 and had another $53,565,511 net unrealized gains. Overall, the fund's net assets increased by $51,370,803 after accounting for all inflows and outflows during the period. Thus, the fund easily managed to cover its distributions with quite a bit of money left over. It does not appear that we need to worry about its distribution sustainability at this time.

As of March 5, 2024 (the most recent date for which data is available as of the time of writing), the Eaton Vance Tax-Managed Diversified Equity Income Fund has a net asset value of $13.77, but its shares currently trade at $13.20 each. This gives the fund's shares a 4.16% discount on net asset value at the current price. This is not quite as attractive as the 5.72% discount that the shares have averaged over the past month, but it is still a discount.

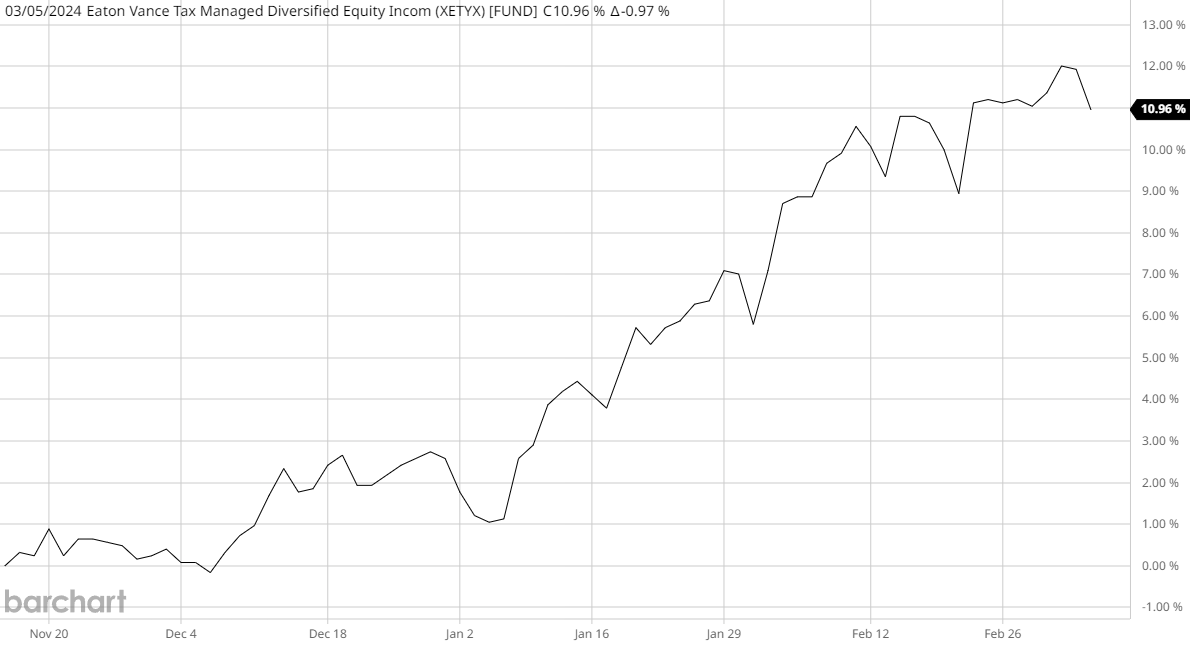

In the introduction, I pointed out that the fund's share price has delivered higher gains than the fund's underlying portfolio since mid-November. This chart shows the fund's net asset value since November 15, 2023 (the date that my previous article on this fund was published):

Barchart

As we can see, the fund's portfolio has only grown by 10.96% but the share price is up 13.33% over the same period. Clearly, then, the fund's shares are outperforming the actual portfolio. As a result, this fund does not have as attractive a valuation as it did previously. We can see this in the simple fact that the fund had a 6.68% discount on net asset value the last time that we discussed it.

It might be possible to get a better price than today's by waiting for a short while. However, the current entry point is certainly not horrible, and purchasing the shares today will still result in obtaining the fund's assets for less than they are actually worth.

In conclusion, the Eaton Vance Tax-Managed Diversified Equity Income Fund is a generally well-regarded option-income closed-end fund that has delivered a pretty decent performance in recent months. However, the fund is not nearly as diversified as might be desired considering that the top six holdings are all mega-cap technology companies, and they account for 34.1% of the fund's assets. All things considered though; the fund does appear to be a reasonable choice for an income investor to use to achieve their goals as long as they ensure that the rest of their portfolio has proper diversification. The fund's price is not as attractive right now as it was a few months ago, but it is still trading at a discount to its assets, so it might be a reasonable purchase right now.