shih-wei

shih-wei

Written by Nick Ackerman, co-produced by Stanford Chemist.

Eaton Vance Tax-Managed Buy-Write Opportunities Fund (NYSE:ETV) delivered some solid returns in 2023 and is starting off with a strong 2024 as well. Of course, this is thanks to the fund's heavy allocation to the mega-cap tech names. 2024 doesn't look like it is so much the Magnificent 7 anymore; it is more just NVIDIA (NVDA) and Meta Platforms (META) really doing all the heavy lifting with strong returns YTD. Both of these names are in the top ten of ETV.

The fund also utilizes a call-writing strategy; it targets nearly 100% of its portfolio with the overwrite strategy. That actually limits the upside potential of the fund and creates a drag on relative performance. With the latest annual report, we saw that the losses from that strategy were quite significant. At the same time, the gains from the underlying portfolio were more than enough to offset those losses created.

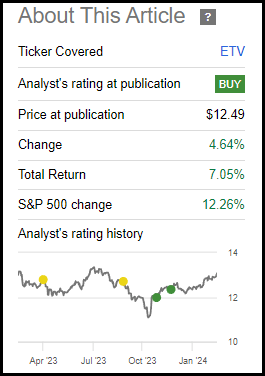

Since our last update, the fund has provided some solid total returns. It also continues to trade at an attractive discount that could provide some more potential upside in the future should we go to more historical levels.

ETV Performance Since Prior Update (Seeking Alpha)

ETV's investment objective is to "provide current income and gains, with a secondary objective of capital appreciation." To achieve this, the fund will invest "in a diversified portfolio of common stocks and writes call options on one or more U.S. indices on a substantial portion of the value of its common stock portfolio to seek to generate current earnings from the option premium."

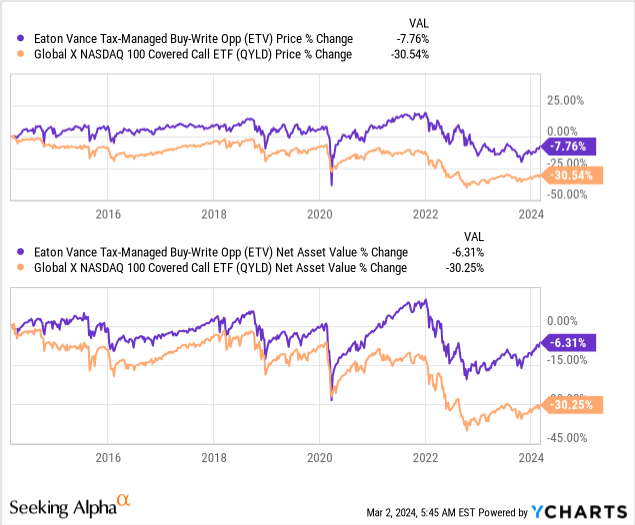

During our last update, we were also giving the Global X NASDAQ 100 Covered Call ETF (QYLD) a look as that's another option writing fund focused on generating high monthly distributions to investors. Both of these funds have been solid on that front, though QYLD has seen quite a bit of price erosion compared to ETV. ETV was holding steady throughout most of the last decade before suffering a decline in 2022.

In the chart below, we are simply looking at the price and NAV changes only here, meaning we aren't factoring in the distributions.

YCharts

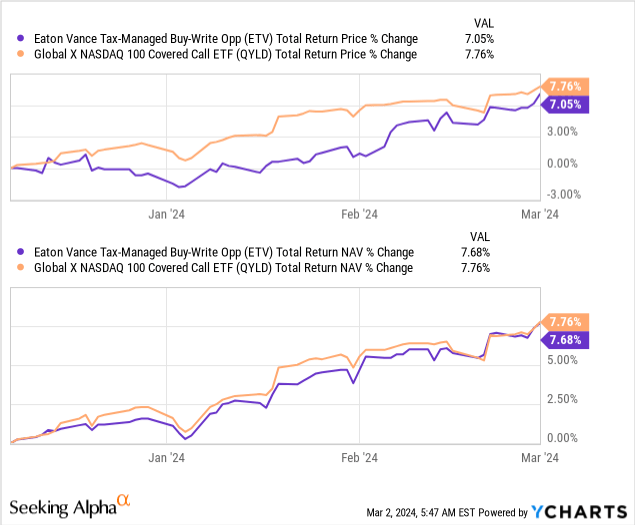

Since our last update, now looking on a total return basis for each share price and NAV results, we can see the funds have performed nearly identically on a total NAV return basis. The total share price returns are quite close as well, though QYLD has been able to edge out ETV a bit more on this front. In some periods throughout, mostly in January and February 2024, this was more noticeable.

YCharts

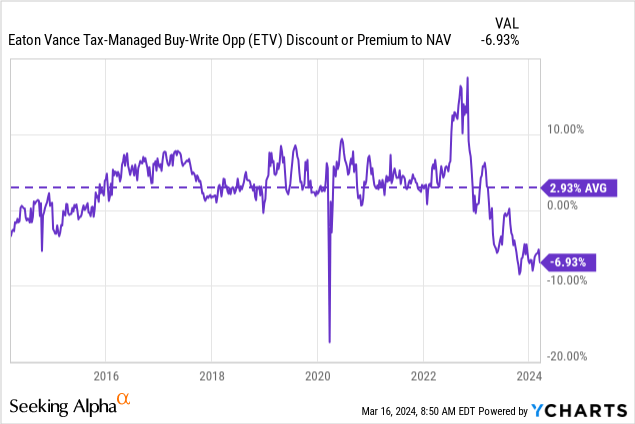

With ETV being able to trade at meaningful discounts/premiums, this is where I believe the closed-end fund structure can provide some opportunities to exploit. Discounts/premiums aren't generally a big consideration for exchange-traded funds as they have a creation/redemption mechanism that will often keep their share price right at par with their NAV price.

For ETV, after 2022's distribution cut, the fund has continued to languish in discount territory. Given that the fund went from an all-time high premium to a level of discount not seen regularly since 2012/2013, the fall was quite dramatic for this fund.

Today, the fund's discount still looks like it is presenting an opportunity. Of course, a risk is that it doesn't mean that this new discount can't become the new "normal" or that the discount can't get wider. That's always a risk when looking for mean reversion plays based on historical valuations.

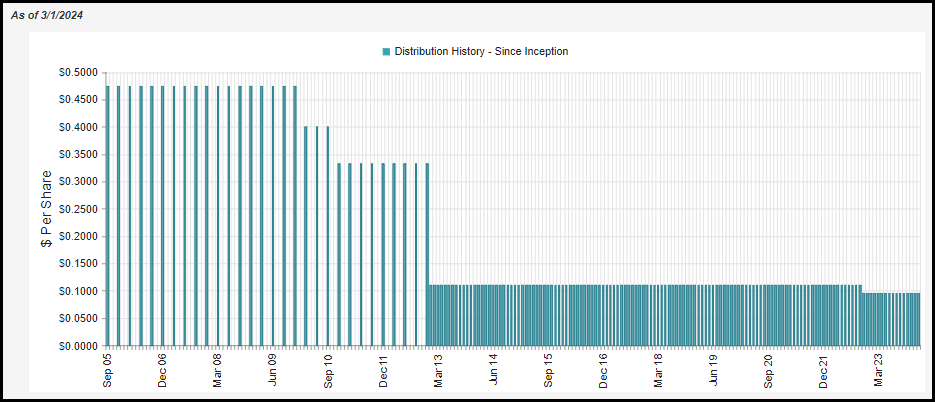

This fund had maintained its distribution for many years before cutting in 2022. The last time the fund had cut its distribution was shortly after the Global Financial Crisis. In 2013, they started to pay a monthly distribution rather than quarterly, but they maintained the same equivalent amount.

ETV Distribution History (CEFConnect)

The annualized rate is $1.1388, with the monthly amount at $0.0949. That works out to a distribution rate of the fund, which comes to 8.83%; on an NAV basis, the rate is 8.22%. The difference here is a reflection of the fund's discount.

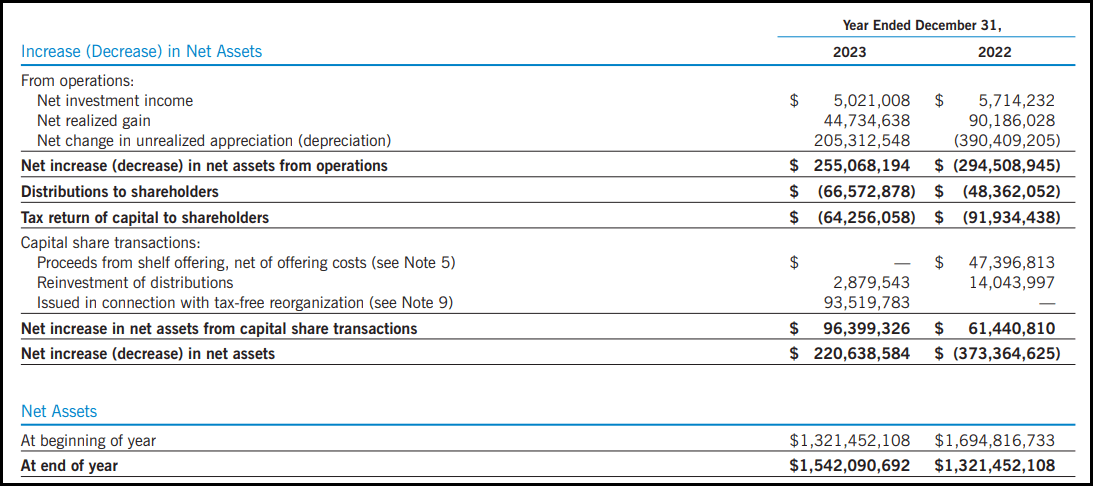

Funding that distribution will require capital gains from the underlying portfolio or its options writing strategy. The mega-cap tech names that this fund holds don't pay out the same level of dividends that this fund looks to pay out in distribution yield to investors. This is quite normal for an equity CEF.

Further, it is quite normal for a tech-heavy CEF such as ETV only to generate a rather small amount of net investment income, too. NII coverage here came to only 3.84% in 2023. When ETV was trading at a premium, the fund was also able to take advantage of selling new shares through its at-the-market offerings or creating new shares through its dividend reinvestment plan. Now, at a discount, that's one perk that they don't have the luxury of any longer.

ETV Annual Report (Eaton Vance)

META is now paying a dividend, but of course, that is unlikely even remotely to bridge the gap. With that, that's where the capital gains would come in to fund the payout of the monthly distribution to investors.

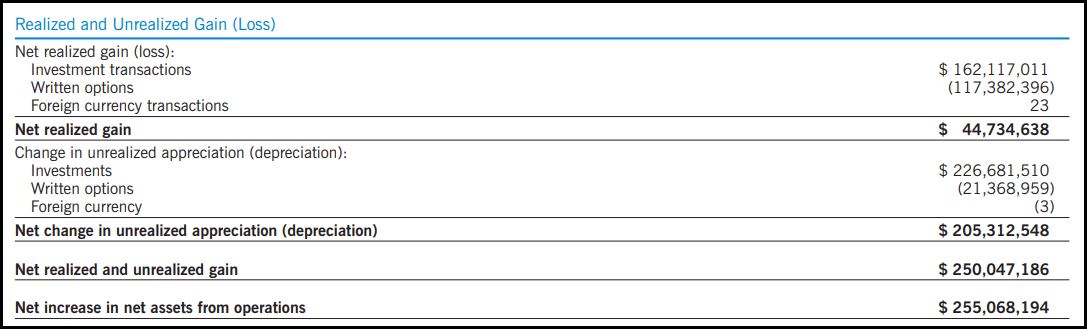

Given that the fund writes call options against indexes, they can't own the fund directly. That creates a situation where the options are cash-settled, and that can mean losses as they roll their options every month. It would mean gains if the premium they received is less than it costs to roll the option in the following month. Throughout 2023, we know that the market was performing quite spectacularly, which meant the options writing strategy for ETV was generating realized losses throughout the year.

ETV Realized/Unrealized Gains/Losses (Eaton Vance)

While the fund can't own an index directly, it can indirectly. That's where the underlying portfolio comes in. For all the losses generated from writing calls, the fund's underlying portfolio was performing incredibly well. Well, enough that all the losses realized from the options strategy were more than offset by gains realized in the portfolio. The unrealized appreciation of the portfolio was also massive as well through the last year.

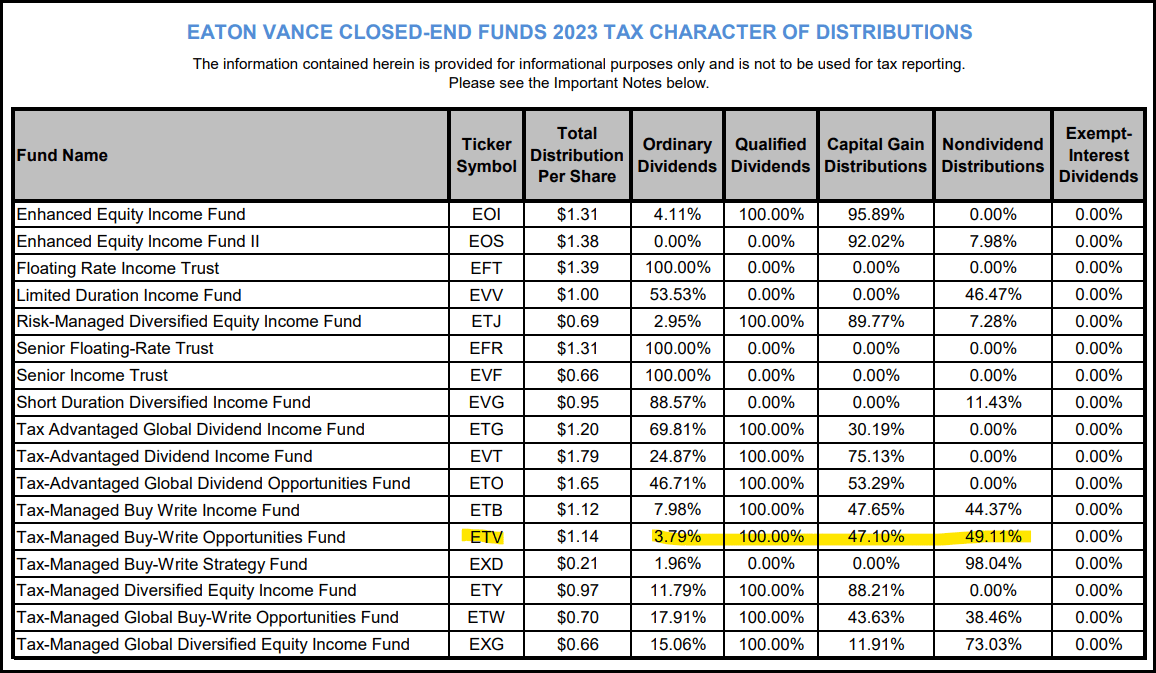

This strategy that the fund employs also goes back to why the fund is tax-advantaged, as its name suggests. This is because the fund can generally generate distributions that are characterized as return of capital. This is a topic we've explored many times in the past.

For 2023, ETV once again delivered a meaningful amount of ROC distributions to its investors. The remaining classifications were either long-term capital gains or qualified dividend income, which are all tax-advantaged on their own. That's what can make ETV a relatively great choice for a taxable account.

ETV Distribution Tax Breakdown (Eaton Vance (highlights from author))

The portfolio turnover for this fund is quite low, coming in at 8% for the last year. Though it was 19% in 2022, that was more of an outlier as in each of the two years prior to that, the turnover was at 9% - similar to 2023.

With that, there isn't generally too much in terms of meaningful shifts in its portfolio between updates.

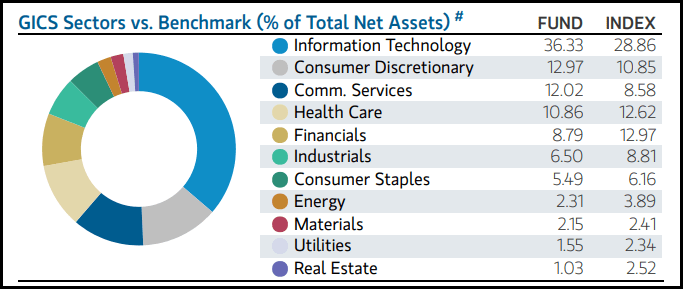

ETV Sector Weighting (Eaton Vance)

The fund continues to favor the information technology sector heavily due to its option strategy of writing calls on the Nasdaq 100 and the S&P 500. Both of these indexes are listed as the fund's equity benchmark.

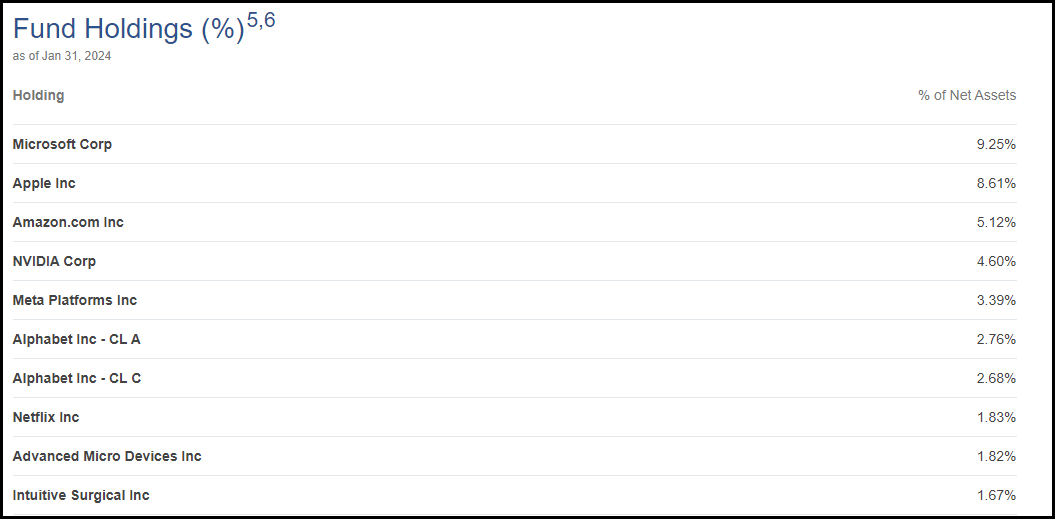

With a weighting to tech like that and writing those calls against indexes, we also see that reflected in the fund's top ten holdings. The mega-cap tech names comprise a massive 38.24% of the portfolio. That's counting 8 of the top 10 names here. Previously, the weighting of these mega-cap names came to 39.41%.

ETV Top Ten Holdings (Eaton Vance)

Advanced Micro Devices (AMD) has also been seeing its share price explode higher as well. It just isn't quite in the same league in terms of market cap as the other names. At the same time, it has pushed itself to be considered a "mega-cap" now as it breaches $327.42 billion, with the definition of a mega-cap at anything over $200 billion. For some context, though, META is at $1.28 trillion, NVDA passed over $2 trillion, and Microsoft (MSFT) went over $3 trillion.

That said, AMD is particularly noteworthy here because it came into ETV's top ten, but that saw Tesla (TSLA) removed from the top ten since our last update. TSLA is still a position for this fund, but it has slipped down to the 11th spot due to weaker price performance. This is one of the reasons why there really doesn't appear to be a Mag 7 club anymore.

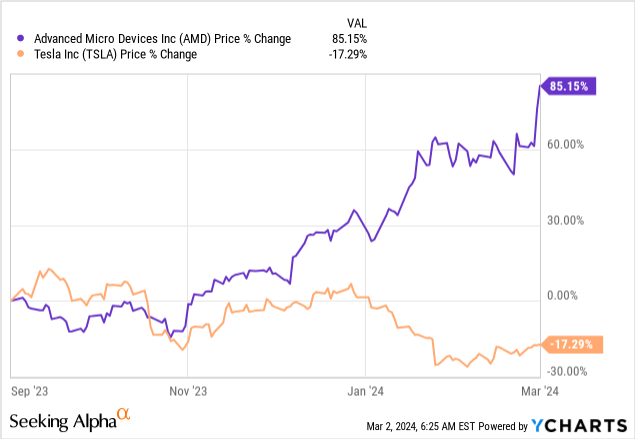

Taking a look over the last six months of performance between AMD and TSLA really helps to illustrate just how dramatic the performance divergence has been. Therefore, it's why ETV's top ten can gyrate quite meaningfully sometimes without the managers even having to do anything at all.

YCharts

ETV provides investors with an attractive monthly distribution. It isn't as deep as some other options out on the market on an absolute basis, but on a relative basis compared to its history, the level is quite attractive. The fund is heavily invested in the mega-cap names that have been dominating the market performance. This makes sense, considering the fund's strategy.

The fund's option writing strategy necessitates the need for the fund to be 'hedged.' An index can't be owned directly, so with writing options against an index, you are essentially writing naked calls. By having an underlying portfolio that largely reflects the indexes being written against, you get that cover indirectly. As these names continue to dominate in terms of performance, they are naturally going to become a larger and larger weighting of the indexes, so ETV's own portfolio needs to reflect that.