blackdovfx/iStock via Getty Images

blackdovfx/iStock via Getty Images

Now well into the Q4 earnings season, the past month so far has proven to be quite a landmine of volatility. Stocks are moving sharply on earnings news, some soaring more than 30% on strong outlooks for the year; and others falling double-digits even without any meaningful bad news to share.

Elastic (NYSE:ESTC), unfortunately, falls into the latter camp. This enterprise search and data observability platform fell more than 10% after reporting a ho-hum earnings quarter, beating quarterly expectations by a hair and offering decent guidance for the upcoming quarter. To be fair, that correction only partially offsets Elastic's sharp rise this year, still up nearly 10% after the post-earnings crunch.

I wrote a neutral opinion on Elastic earlier this year, when the stock was trading at a similar ~$115 level. Now after its most recent earnings release, new considerations have popped up on both the good and bad side of this play, and I remain neutral on Elastic's prospects through the remainder of the year.

On the positive side for this company:

At the same time, however, I am cognizant of a number of meaningful risks:

To me, this is a fairly balanced bull and bear case for this company. From a valuation perspective, Elastic is neither cheap nor overly expensive as well. At current share prices near $117, Elastic trades at a market cap of $11.66 billion, and after we net off the $1.02 billion of cash and $568.3 million of debt on Elastic's most recent balance sheet, the company's resulting enterprise value is $11.21 billion.

Meanwhile, for next fiscal year FY25 (which is the year ending in April 2025 for Elastic), Wall Street analysts are pegging the company's revenue target at $1.48 billion, representing 18% y/y growth. That in itself is a fairly aggressive growth target that doesn't assume any deceleration from current growth rates. Taking consensus estimates at face value, we arrive at a multiple of 7.6x EV/FY25 revenue.

Yes, peer multiples have gotten frothy in the software sector again, but personally, I'm positioning my portfolio for a near-term market correction. As such, I prefer to lean more toward value names at the moment (in particular I like Instacart (CART), Toast (TOST), Sonos (SONO), DocuSign (DOCU), and Asana (ASAN) at the moment) that have more staying power to withstand a broader market downturn.

All in all: outside of generative AI's incremental revenue opportunities, which Elastic management itself has said will take time to accumulate into a meaningful business, I'm not certain there are any meaningful catalysts for Elastic in the near-term horizon to justify a meaningful rally from here on out. I'd prefer to wait on the sidelines until a better price for this stock avails itself.

Elastic's fiscal Q3 (January quarter) results, released in late February, caused broad disappointment in the markets as the company pointed to another quarter of business-as-usual. Take a look at the quarterly results below:

Elastic Q4 results (Elastic Q4 earnings release)

Elastic's revenue grew 19% y/y to $328.0 million, slightly outpacing Wall Street's expectations of $320.9 million (+17% y/y) while accelerating as well from Q3's 17% y/y growth rate - a meaningful positive for the company in a quarter that saw deceleration for most of Elastic's software peers.

Heightened customer interest in generative AI has been a meaningful business driver to date. The company noted that it has signed up several hundred customers onto Elasticsearch Relevance Engine, which is a platform to build and deploy generative AI applications.

Still, per CFO Janesh Moorjani's remarks on the Q3 earnings call, it will take time for AI to become a meaningful driver of revenue for Elastic. In addition, customers are still quite mindful on spending levels, preferring to consolidate their usage to lower their bills:

As in prior quarters, we saw a number of customers consolidate onto the Elastic Platform to lower their total spend without sacrificing innovation. We also saw healthy cloud consumption growth as customers continued to consume against their contractual commitments.

As Ash mentioned, we continue to see strong customer interest around Generative AI use cases. Customers express a strong desire to use ESRE to build Gen.AI applications, since it provides a comprehensive and enterprise ready platform to ground large language models with their private business context. While it will take some time for Gen.AI spend to become a significant driver of our revenue, we continue to expect that Gen.AI will present a meaningful revenue opportunity for us in the longer term."

The company's outlook calls for 18% y/y growth in Q4, representing no deceleration from the current quarter - again, a meaningful distinguisher for Elastic vis-à-vis many software peers.

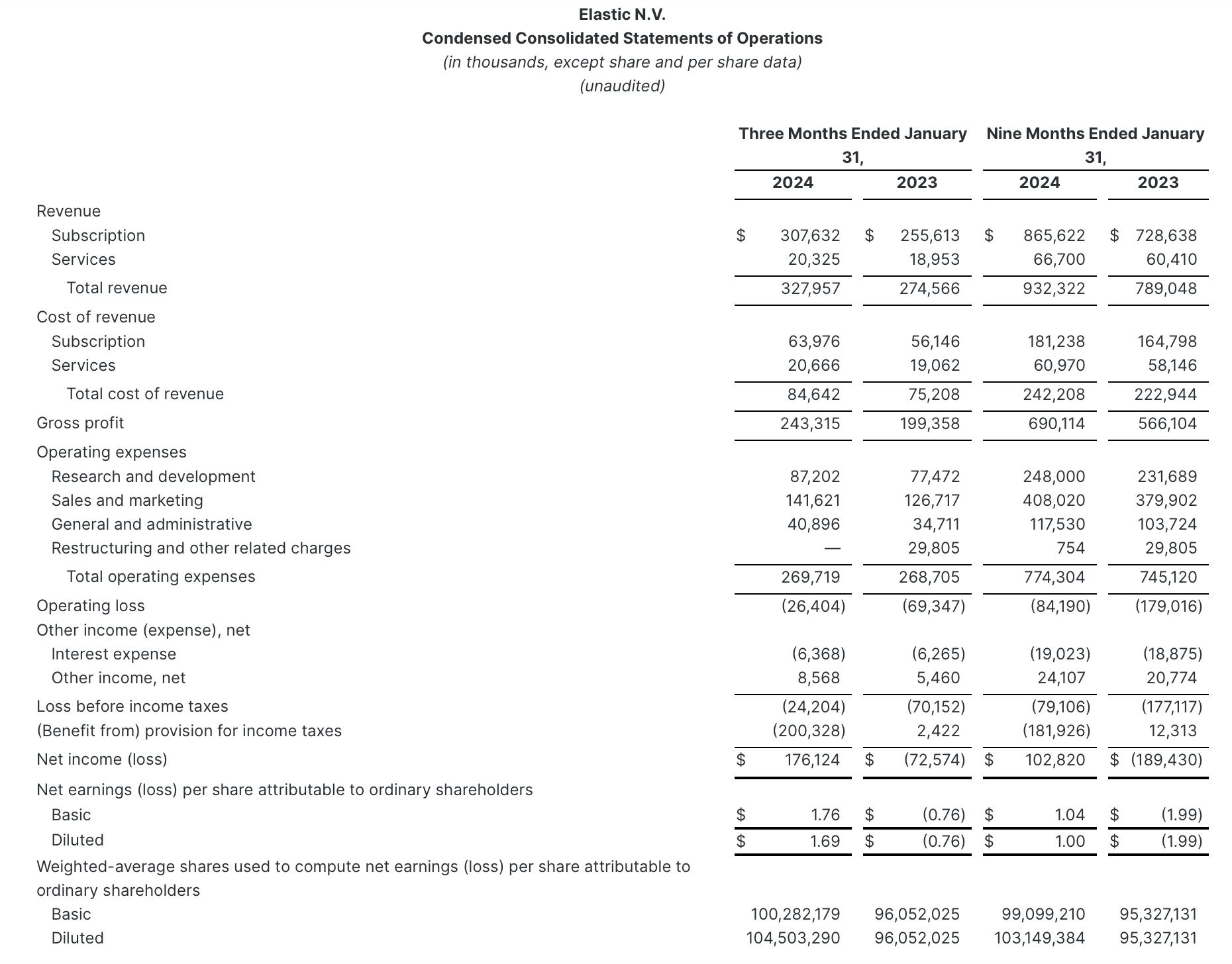

Pro forma operating margins also rose to 13.2% in the quarter, up 530bps y/y from 7.9% in the year-ago Q3, which was driven in part by a better revenue mix into subscriptions. Free cash flow for the year to date, meanwhile, has more than tripled to $108.9 million, representing a 12% FCF margin - up eight points y/y.

Elastic FCF (Elastic Q4 earnings release)

There can be no doubt that Elastic is continuing on a path of stable and strong execution, with longer-term tailwinds in AI workloads expected to benefit its revenue base over the next several years. However, the double-digit drop in Elastic's share price on the back of strong results on paper is a reflection of the company's already-fair valuation multiple, and at a near-8x forward multiple of revenue despite growth expected to sit only in the teens, I'd still maintain caution here.