David Henderson/iStock via Getty Images

David Henderson/iStock via Getty Images

Empire State Realty Trust, Inc. (NYSE:ESRT) is a US-based REIT operating mostly rental office space in Manhattan, New York City. Its most famous asset is the namesake Empire State Building, a landmark of the Big Apple.

The trust owns several more buildings: It owns dozens of locations within the office, retail and residential spaces. Most buildings are situated in Manhattan or adjacent metro areas.

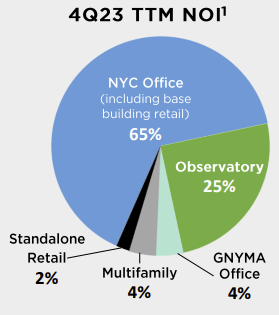

For its most recent quarterly earnings reported, Empire State's net operating income (NOI) was distributed as follows, with the vast majority deriving from office and base retail:

Empire State Realty Trust investor presentation

"Observatory" here refers to NOI from tickets sales of the Empire State Building observatory.

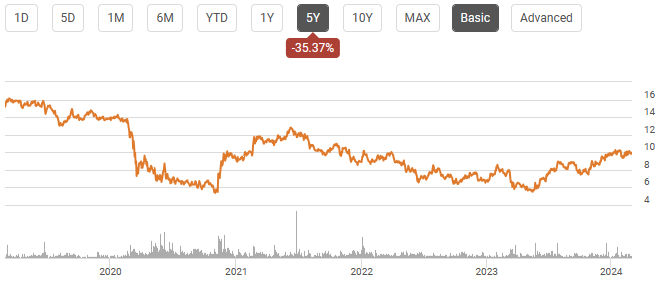

If you had placed your money in Empire State Realty Trust 5 years ago, you would have lost a significant portion of your investment. Empire State is down ~35% over the past 5 years:

Seeking Alpha

Against the backdrop of a market (S&P 500) that has advanced ~80% in the same timeframe, it's clear that the stock has underperformed badly.

But this doesn't come down to any real company-specific issue. In fact, the entire commercial real estate sector has been badly hit first by the COVID pandemic and since the tendency of many businesses to prioritize hybrid or remote work, lowering demand for office space.

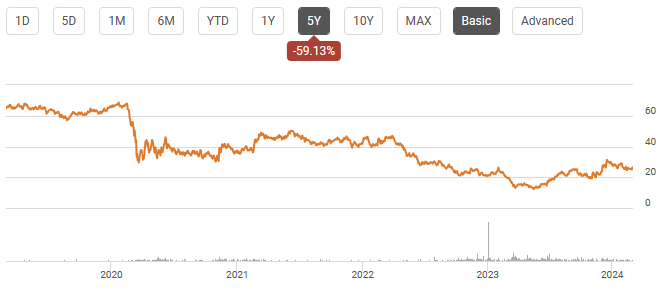

One of Empire State's large competitors, Vornado Realty Trust (VNO), has performed even worse over the past 5 years:

Seeking Alpha

As is seen from both graphs (Empire State and Vornado), troubles started with the onset of COVID, rebounded some as cities reopened, but has since struggled to return to pre-pandemic levels.

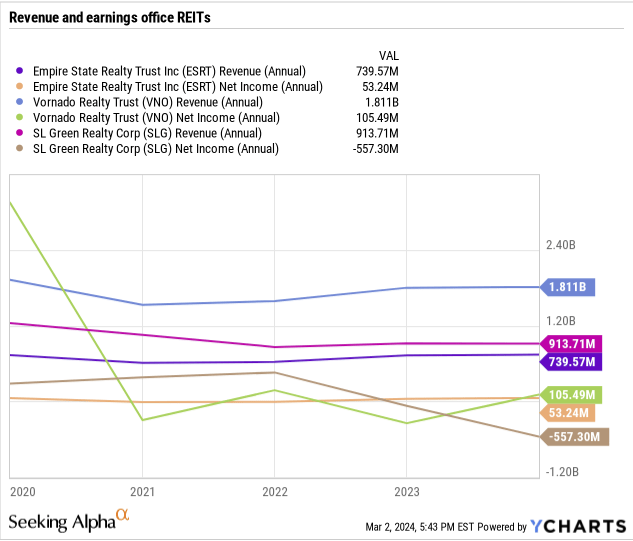

Not surprisingly, we see some of the same development with the fundamentals. For Empire State, revenue and net income were down during COVID, but has actually since rebounded. For its peers, Vornado and SL Green (SLG), troubles seem to have protracted somewhat:

YCharts

To me what the numbers show is that the industry has seen structural changes and challenges in recent years. At the same time, they show that while slow, there is a definite recovery and "reversion to the mean".

That doesn't mean the industry and Empire State don't have more work to do to start delivering shareholder value again. I'll take a look at these efforts below.

While the pandemic was still raging in 2021, Empire State bought 2 apartment buildings in Manhattan to diversify its portfolio.

This initiative joined a general trend of property owners to move towards more residential buildings and less office buildings. A lot of office space in NYC is even being converted to residential space. With too much office space and not enough housing, why not?

In a recent interview with CNBC, Empire State's CEO hinted that Empire State is in a position to buy more properties - and looking to do just that:

We want to make sure we have run way, so we are in a position always to take advantage of opportunity. And by that I mean acquisitions. - Empire State Realty Trust CEO Anthony Malkin

While many office REITs probably are not looking to expand their footprint in the somewhat distressed industry, it appears Empire State wants to double down and use its financial position to expand.

Empire State hasn't just diversified into more residential units. The Empire State observatory adds what management has described as an "inflation hedge". Through dynamic pricing, Empire State should be able to raise prices in a more flexible manner than is the case with rents.

In its focus to recover from the pandemic in its core business, Empire State has managed raise the leased and occupancy percentages on its properties coming out of the pandemic. The occupancy rate on NYC office space is now 86.3%. This compares to 89.8% in Q4 of 2019. This means Empire State is almost back to normal. Empire State has also demonstrated 8 consecutive quarters of positive leased absorption - essentially meaning that when tenants vacate, that space is absorbed (rented) by other tenants.

These developments, according to management, shows what they call a "Flight To Top Quality Space" in its rental price tier. Essentially, management seems to consider Empire State well-positioned within its pricing tier to absorb present and future demand.

As an office REIT, Empire State obviously employs debt to leverage returns and finance properties.

According to its most recent 10-K, Empire State has opted to only use fixed rate debt. While many other property owners have taken advantage of floating rates in recent years due to the historically low cost of capital, Empire State's policy to only use fixed rate debt seems a brilliant strategic move in hindsight: It now secures continued cheap financing even through the inflationary period we've gone through and the hiking of rates by reserve banks.

At December 31, 2023, Empire State's debt carried a weighted average interest rate of 3.9% and a weighted average maturity of 5.4 years. This means Empire State has secured fairly low interest rates for the coming years.

Empire State's conservative approach to financing further includes maintaining a reasonable ratio between debt and equity. It currently has a debt-to-equity ratio of 1.29 (long-term debt to common equity), which is well in line with its NYC office REIT peers:

| Office REIT | Debt-to-equity ratio |

| Vornado | 1.88 |

| Empire State | 1.29 |

| SL Green | 0.95 |

Because of Empire State's strong balance sheet, the company is able to return cash to shareholders not just in the form of its dividend but also through an aggressive buyback program. In December 2023, Empire State announced a buyback program in the amount of $500 million - a substantial portion of its market cap. In their most recent investor presentation, Empire State said returning cash to shareholders through buybacks was one of its core areas of focus to drive shareholder value.

Empire State currently trades at a P/FFO (FW) of 10.80 according to data from Seeking Alpha. This puts it above below Vornado and above SL Green:

| Office REIT | P/FFO (FW) |

| Vornado | 11.33 |

| Empire State | 10.80 |

| SL Green | 7.99 |

With Empire State a little more expensive than its peer SL Green and not as expensive as Vornado, the question is if it's the best buy of the three based on what you get for the price.

In answering that question, I think a key point to the affirmative is that unlike its peers, Empire State has been able to recover from the pandemic in terms of revenue and earnings – and they’ve guided a clear path forward to growth. As outlined above, this path involves meeting demand in its legacy office business, but also reaching for the opportunities in diversifying into residential and attractions. Then there's the balance sheet: Empire State is in a strong financial position, and that's worth paying for.

In many respects, the negative impact of the COVID pandemic seems to be behind the commercial real estate sector. Societies have opened back up, and companies are asking their workers to return to the office. Some companies have even said they may sanction workers who don't.

But this reversion of pandemic corporate policies hasn't gone without pushback: Many workers will prioritize if not fully remote than hybrid work opportunities. During and after the pandemic, a new trend among especially younger workers - quiet quitting - even added to the pressures caused by the pandemic. This trend is essentially about doing the bare minimum at your job to keep it - but never going the extra mile for your employer. While this doesn't necessarily challenge office REITs more than any other line of business, it underscores how the workspace environment is changing: The idea of the typical 9 to 5 is under pressure, and workers are finding out there are different ways to perform jobs that have typically been carried out from a conventional office space. This carries with it the risk that the commercial real estate environment may have changed for good. The appropriate action on the part of office REITs in response to this is probably adjusting to the new norms. The properties owned by these trusts are valuable regardless of their utility: Empire State is demonstrating this by their converting of some office space to residential use and through the opening of the Empire State Building Observatory deck that opened in 2019, also an alternative use of some of the floor space.

Adding to these risks, there's the risk of oversupply. According to some, there was an oversupply of office space even before the pandemic. Developers tend to construct office buildings in good times with cheap financing, effectively betting that conditions won't deteriorate before construction is finished and the property leased. New York City has been no exception with major development projects having sprung up over several years even before the pandemic. For instance, the Hudson Yards development has added millions of square feet of office space to the existing landscape. Groundbreaking took place in December 2012 - and the development isn't expected to be fully completed until 2027. The risk to REITs with such developments is that they can weigh on occupancy and lease rates if they result in oversupply.

Empire State is a well-diversified REIT that, in spite of its name, operates not just the Empire State Building but several other quality office buildings and other purpose buildings.

Like its peers, Empire State experienced hardship from the COVID pandemic and the ensuing "remote work" culture. Empire State seems to have made their way past these troubles, though. They've seen demand recover, and they're diversifying the business. You're paying a price well in line with its peers, but it appears to be the superior pick based on what you get for that price.

Just like investing in real estate outright comes with risks, so does buying it through a REIT: Corporate policies on remote work can affect the future landscape of commercial real estate, and with many developers in NYC, there's always the risk of oversupply.

These risks aside, I consider Empire State a well-run REIT with attractive exposure to the NYC office space with enough diversification to counter the inherent risk.

For the reasons stated above, I rate Empire State a Buy.