hxdyl

hxdyl

Energy Recovery (NASDAQ:ERII) is the leader in pressure exchanger systems used in desalination plants worldwide.

I wrote about ERII in November 2022 with a Hold recommendation. Despite the company's impressive control over the pressure exchanger market, I considered the stock price too high and charged with optimism (part of it fueled by management). This represented a risky entry point.

In this review, I find the stock price much more compelling, albeit I continue to rate the stock a Hold. The reason is that the multiple on the profitable water business is still high, while success in the CO2 market is not guaranteed.

However, I believe if the stock made a further dip (which is possible in FY24, given the company's guidance), then it could become a purchase opportunity.

If I told someone that a company maintained profitability but grew two emerging segments by 100% and 400%, with promising future perspectives, that person would probably not guess that the stock is 50% down. This is the case of ERII from its all-time high.

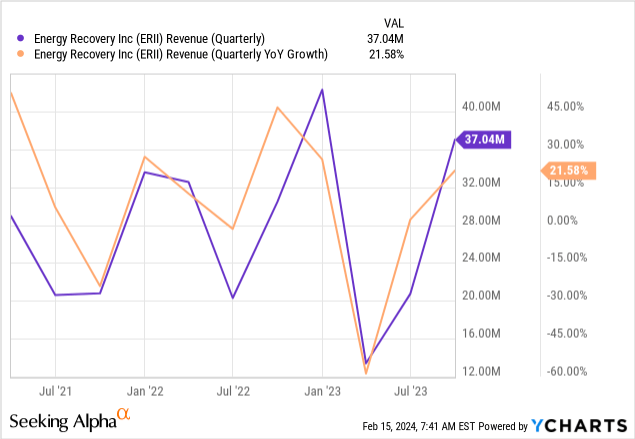

ERII had a rough start to the year after Q1 revenues from desalination megaproject revenues collapsed compared to the previous year. This led to lower gross profits and significant operating losses.

At the time, management said the reason was typical delays in these megaprojects. The guidance was accurate, as ERII returned to YoY in 2Q23, reaching 22% YoY growth by 3Q23. The chart below does not include 4Q23 data released this week, which boasts $57 million in quarterly revenues and 35% YoY growth.

On top of that, the company's wastewater market (embedded in the water segment) is expected to end the year at $7 million in revenues, almost double the FY22 $4 million level, which in turn was four times the FY21 $1 million level. It is expected to grow to $10 to $15 million in FY24.

Finally, the company's refrigeration segment revenues surpassed $600 thousand in FY23 compared to about $100 thousand a year before. The company expects the new system to be installed in 50 locations in FY24, reaching single-digit millions in revenue.

So, the company kept growing in its primary market and blazing in its emerging markets, yet the stock decimated to $16 today from $30 in April 2023. This is the type of risk I warned against in my first article. When the sky is the limit, even good performance can be seen as subpar, leading to people dumping the stock.

The company announced its CEO and President would be stepping down in October 2023, fueling the stock's selloff. Later, management said the decision had been meditated on for long, but many investors read it as a bad sign. After releasing 4Q23 data this week, the CFO (in office since 2018) also resigned.

One of the company's directors, David Moon, was appointed interim CEO and then ratified. Moon comes from refrigeration, specifically from the commercial segment of Carrier. It indicates the company's new focus is the refrigeration market.

I was critical of management's aggressive guidance in my first article, mainly because they guided multiples of revenues and profitability by 2026. I believe this fueled the optimism that turned its other cheek on the company, dumping the stock.

In this review, I find that the company's management is aggressive in its guidance but also sincere in the state of the business.

On the latest company calls, management has issued several warnings, for example, on interest rates affecting CAPEX-intensive projects in desalination, of higher exposure to execution-risky emerging markets like Egypt or Algeria, on a probably more muted FY24 in terms of desalination market growth, and on the fact that refrigeration is still nascent and mostly untested.

I now believe that the aggressive guidance is not a scheme to pump the stock price but rather simply excitement from mostly technical managers who believe in their product. I find that ERII's product leaders are knowledgeable and are promoting the technology. For example, look for Energy Recovery on YouTube. You will not find too many videos about the stock, but rather many hour-long videos in specialized channels on pumps, refrigeration, and desalination.

The desalination segment is the company's star, with impressive growth and profitability, as seen below.

| Water segment | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 |

| Op Inc | 29 | 33 | 39 | 45 | 52 | 65 | 62 |

The company's handle on this market is almost uncontested. I say almost because up to 2022, there was virtually no alternative with the efficiency characteristics of ERII's PX line. However, in October 2022, a competitor in the pump and piping segment, Flowserve, launched a similar product called FLEX.

Although FLEX still has to make inroads in the market, it has a lot of meat to eat. The reason is that ERII has used its market dominance to charge 70% gross margins on its PX products. This means there is much room for FLEX to present price competition.

The FLEX challenge is the main risk to the company's long-term dominance of this critical market. Management has also guided more muted investment in desalination plants (expensive in CAPEX) because of higher interest rates, but I believe this is a cyclical phenomenon. Long-term, desalination is almost the only solution in many areas of the planet, and investments in this infrastructure will continue to expand.

If we consider the water segment alone, ERII does not seem as highly overpriced as it looks when including the refrigeration segment. The company posted $130 million in revenues in FY23 and $60 million in operating profits. Apply 25% taxes to reach $45 million in NOPAT. Compared with an EV of $800 million, it yields a high 18x EV/NOPAT multiple. High, but way lower than the current 50+ multiple when adding the refrigeration segment.

However, ERII's consolidated profits are much lower than $60 million because the company spends/invests a lot of money in its refrigeration segment. For FY21, FY22, and FY23, the 'emerging technologies' segment (refrigeration) consumed $20 million each.

Considering those investments as losses is not correct. If the company invested $20 million in CAPEX (building a new plant), those expenses would be capitalized and depreciated over 20 or 25 years. Because the company is paying R&D and sales personnel, the investments are expensed in one year.

In the end, the question is of capital allocation. That is why I prefer not to incorporate the losses from refrigeration in my valuation. If the refrigeration segment proves a flop in two years, the company can still post good profitability from its desalination business. If we buy the company at a reasonable multiple of its desalination business, we get the rest as optionality.

ERII's investment in the refrigeration segment makes sense. The company's pressure exchanging technology is applicable, and there is a long-term unmet demand trend for solutions that improve CO2 refrigeration systems' efficiency above 20 degrees Celsius, as HFCs are phased out in developed economies. However, it is a nascent technology (currently tried in less than five locations), that cannot be accurately valued.

As a reminder, ERII invested millions in an O&G solution (the VorTeq pressure exchanger) that had the same characteristics: PX technology applied to a pressing market need that could potentially save billions in the industry. However, the solution was a flop, it was never adopted and was sunset by ERII.

Therefore, I considering ERII using the BCG matrix framework. In this framework, there are four types of businesses inside a company: stars that grow and generate cash, cash cows that generate cash but do not grow; these two have to be tendered and their profits used to finance question marks, businesses with low profitability today, but high growth potential.

The desalination business is a star; it grows a lot and generates a lot of profitability. That is the basis on which to value the company today. Part of that profitability is applied to a question mark business, refrigeration. It is a business with a lot of unproved potential that is difficult to value. If the question mark business fails, the company can reduce investments in new projects and return the profitability of the star segment to shareholders.

Of course, if the refrigeration segment got derisked, it could be valued independently. In this route, following the (expected) 50 more locations to come in FY24, tenfold the current applications of the system will be critical.

Still, using this framework, I believe ERII is still overpriced. An 18x multiple on the desalination business is high, especially if the company is now facing a challenger that has the potential to erode significant margins via price competition.

Further, if management's guidance for FY24 is correct, the desalination business may even decrease cyclically. FY23 already decelerated against the growth trajectory during the past five years. With so much optimism in the stock, this could lead to disappointment for short-term investors, further fueling a downward price spiral.

I prefer to wait for lower prices and would consider the stock below a $500 million enterprise value or a share price of $10. This means I assume the risk of the stock going up and never finding a good low-priced entry point. I am ok with that, as part of being a long-term investor is coping with FOMO.