aquatarkus

aquatarkus

Dear readers/followers,

This is not my first article on Equinor (NYSE:EQNR). It's a follow-up on a piece I in fact wrote almost two years ago.

You can find that article here, but you'll notice that I at the time went "HOLD" on a company that was thought to then outperform (which it also did, momentarily), only to then move more or less in accordance with my expectations for the next few years. The RoR for Equinor since that article now looks like this.

Because of this, I view this as a fairly successful rating and article, and I currently only own a very small stake in Norwegian Equinor.

However, the time has come to revisit my rating and potentially change it, and maybe even start building that Equinor stake again.

The reasons for doing this are something that I will visit in this article, and by the end of it I will update my thesis and rating for Equinor along with a justification. I believe this company is one of the better ones in its field, and in case we do see a cheap enough level, this becomes what I believe to be a must-buy.

I still know Equinor as Statoil - that's the name it held for many years. The simple fact for the business is that this is the largest Norwegian energy business in existence. The company is a company of many "firsts". I would say that before renewables were all the rage, Equinor was already part of the renewables sector, and not for the sake of greenwashing.

Beyond that, it's in the top 10 of oil/gas companies on the planet. It used to be smaller until it merged with the energy division (sans generation) of what is now known as Norsk Hydro (OTCQX:NHYDY), another company which I frequently cover. The name of the company actually has an interesting story, coming from "equi" (meaning 'roots') and "Nor-way" - an homage to the company's Norwegian roots.(Source: Equinor IR)

It was privatized in 2001, and since then has moved to become a major, albeit volatile player in the energy market. When I last wrote about it, the yield wasn't that great - today it's better. The fundamental safety was superb, and it still is. Equinor is one of the very few energy companies with an AA rating. (Source: Equinor IR)

This is owed in no small part to its sub-31% long-term debt to capital rating.

What makes the company such a good business?

It's market-outperforming.

On the basis of sector comparisons in the energy/oil sector, the company manages sector-outperforming gross and operating margin levels, combining this with superb financial fundamentals. The company has a debt/EBITDA of below 0.7x, a net margin of 11.1% and an operating margin of 33.4%. It's not rare to see this business, at least not in the last few years, produce or manage close to that double-digit net margin, and that is an attractive thing in itself (Source: GuruFocus).

The company has transitioned to a new strategy for the coming few years, with high value in the company's renewables, an optimized and conservative oil/gas portfolio while capturing opportunities in low Co2 as a sector.

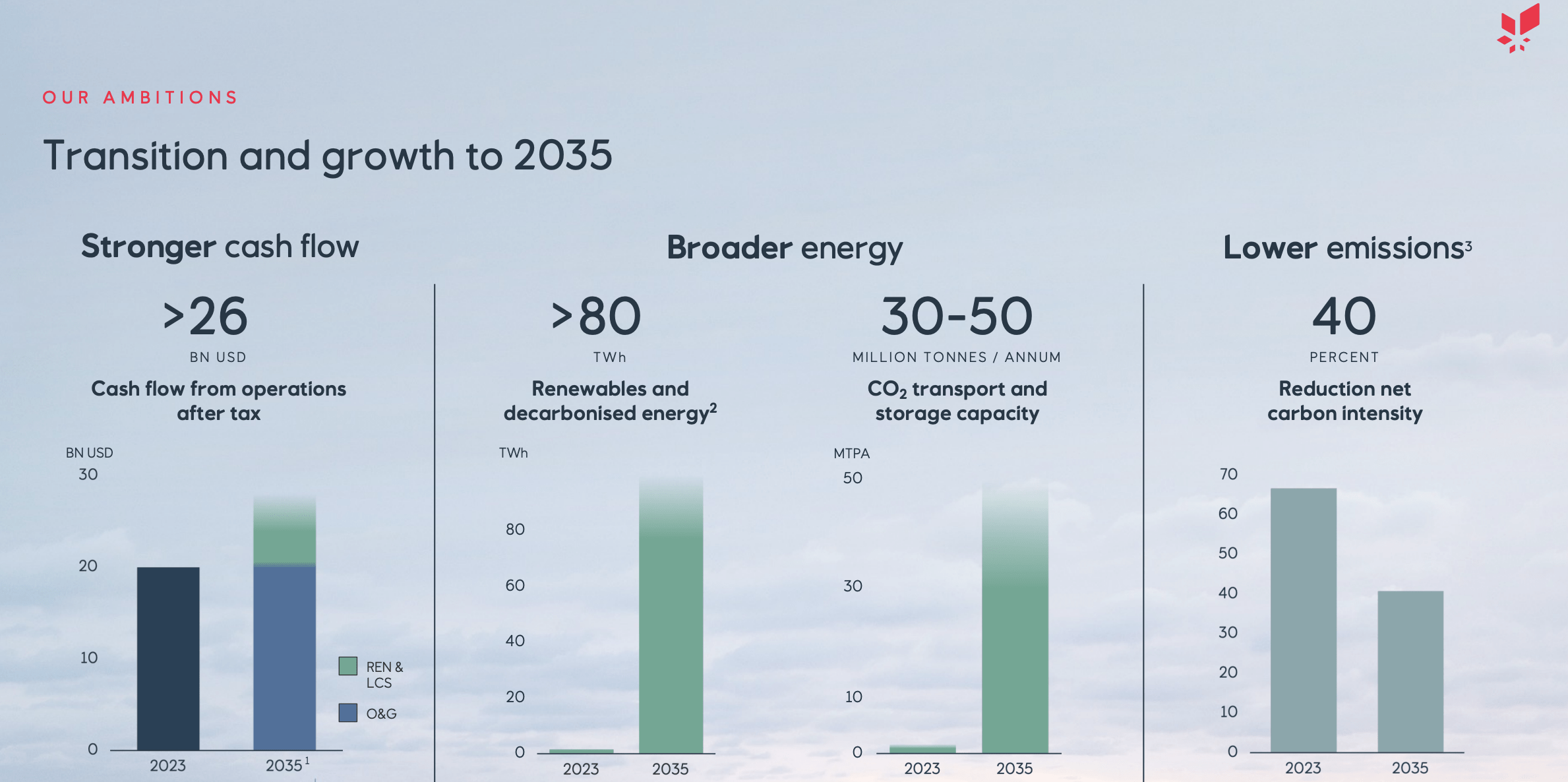

The company wants better cash flows, broader energy, and lower emissions.

2023 was a so-so year, as evidenced by the company's drop in share price. But the company managed $36B in adjusted earnings, $20B in operational ROCE and very good margins, like I mentioned.

Here are the company's 2035 targets. (Source: Equinor IR)

Equinor IR (Equinor IR)

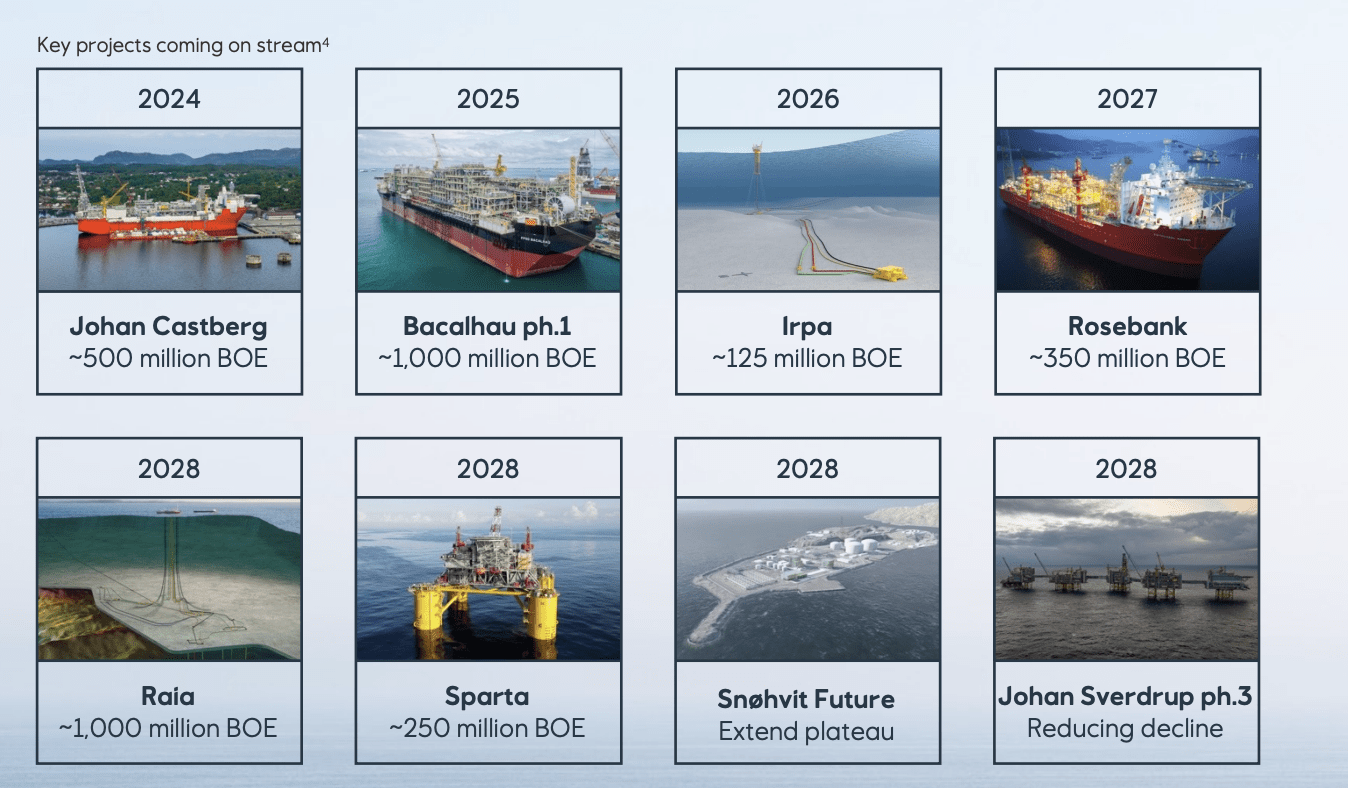

Let's look at the oil/gas portion of the portfolio first. The company is now at a break-even of $35/bbl, and while this is nowhere near some Middle Eastern or Russian producers, this company operates in a different scope and geography. The company also has several new projects coming online - so the notion that Equinor is somehow leaving this legacy behind is a false one.

Equinor IR (Equinor IR)

The company targets a 50% cash flow increase until 2030 combined with a decarbonization of its entire portfolio.

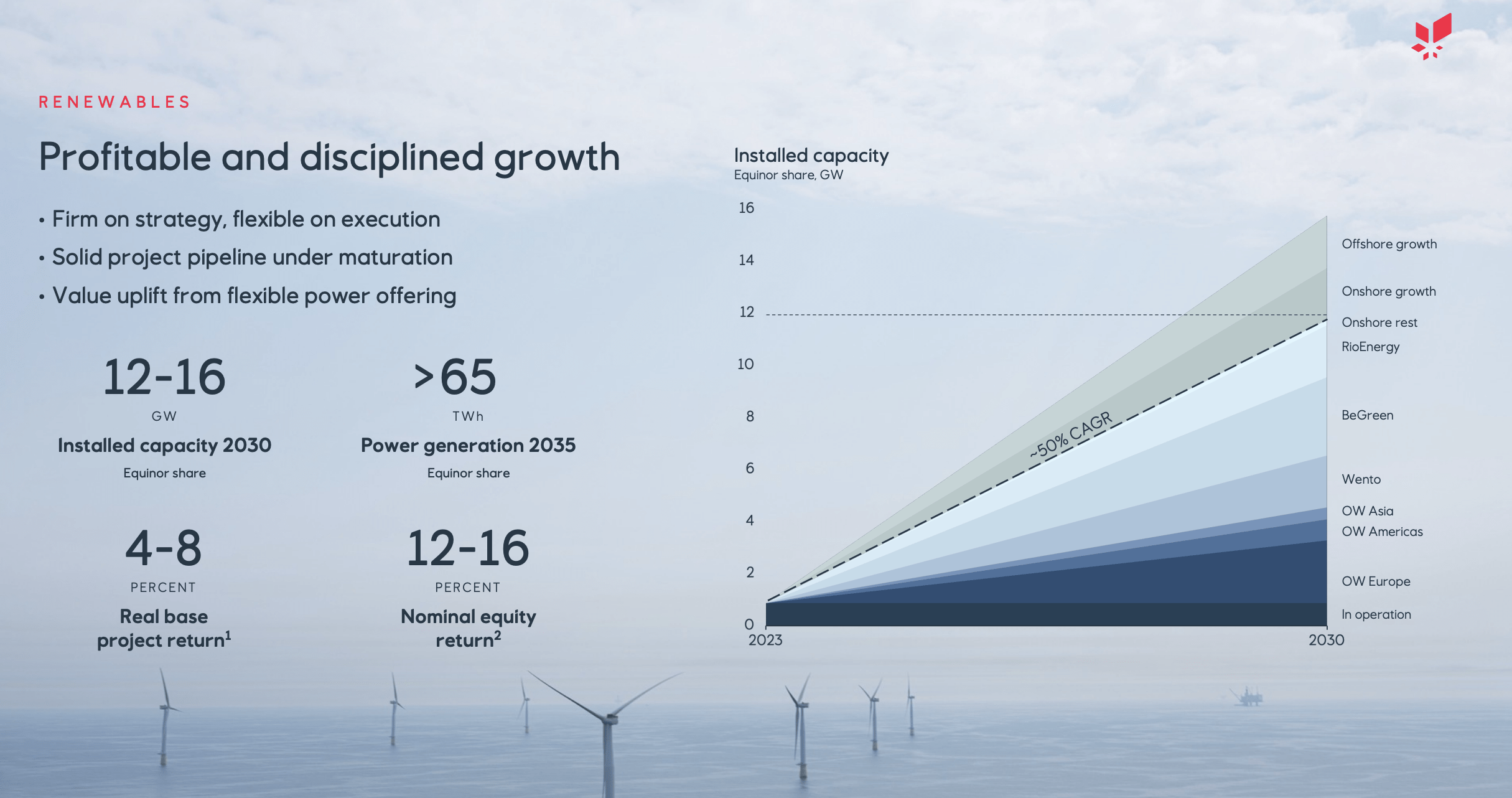

Moving to its renewables segment, the company is targeting significantly more installed capacity and generation, aiming for a 4-8% real base return, and a good nominal equity return in the 12-16% range. We'll see if this is possible, as I myself am somewhat dubious about the focus on offshore wind (plenty of problems, just look at Vestas), the company's plans are set.

Equinor IR (Equinor IR)

Most traditional analysts consider the company's strategy and generation mix to be an attractive one, and its acceleration into renewables for its 2050 net zero goal to be a good one. However, it is exactly the focus on the offshore wind segment that for me creates a risk consideration that I would only enter into at the right price - in layman's terms, I want it "cheap" because I do not believe offshore wind is as resilient or as good as it's made out to be. I'm talking about very volatile output levels due to wind speed inconsistencies, and even the environmental impact on marine species. It's one of those things that "sound" great, until you dig deeper into reliability as well, with many of them needing replacements after 20-25 years - These are not some negative numbers from doubters as well - these are the manufacturer's own numbers (Source). Meanwhile, any standard nuclear plant can easily operate three times that time span.

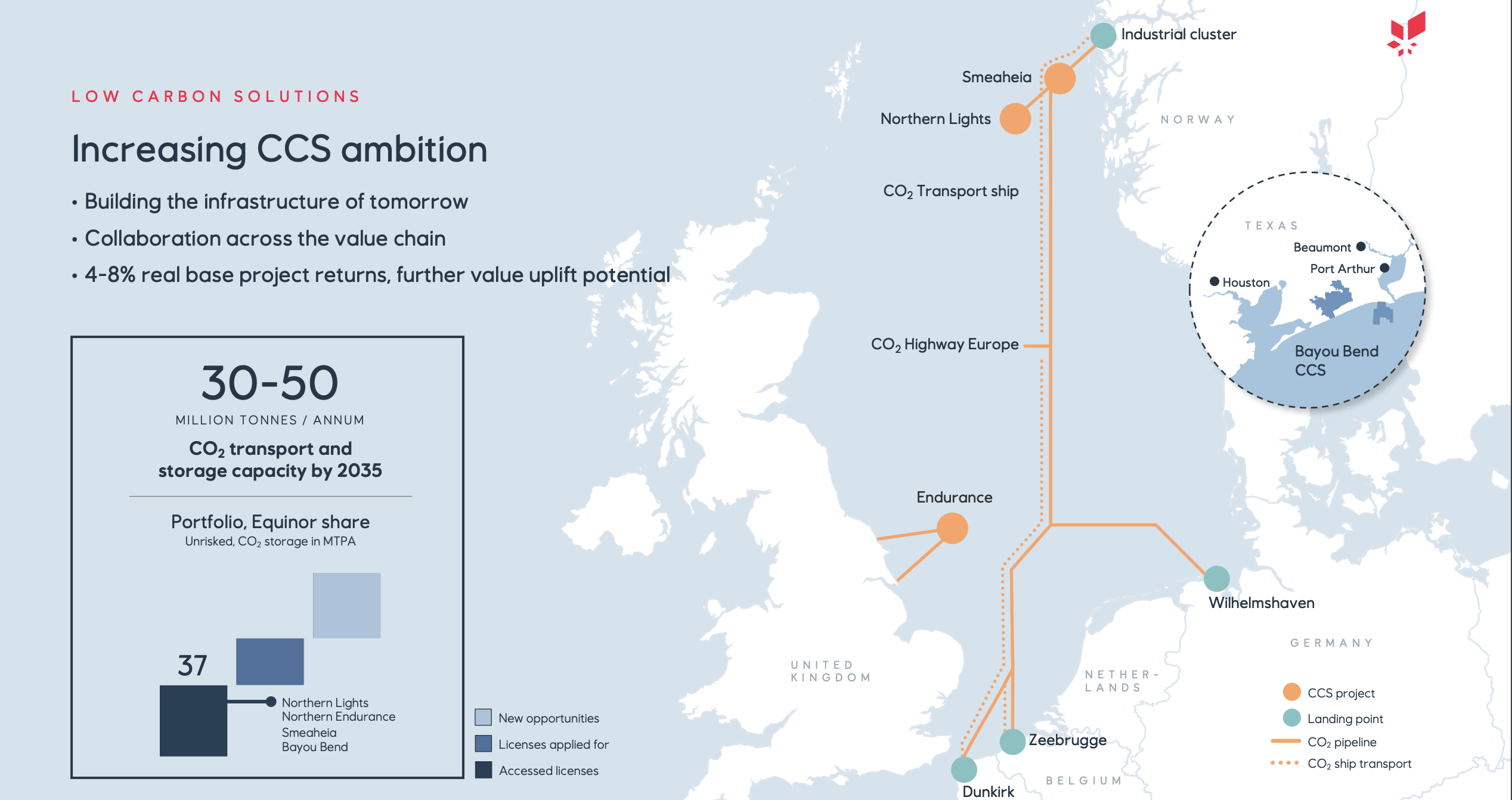

However, the company's low-carbon projects and legacy pushes, are what interest me here. Because these, I believe, are things that can really push the envelope for Equinor.

Equinor IR (Equinor IR)

On the capital distribution side, the company's drop in share price means that the yield for Equinor is now pushing toward the 7% mark, with a combined ordinary and extraordinary cash dividend that implies somewhere in the vicinity of 6-8% if it upheld for the coming quarters. Unlike its peers, Equinor follows a quarterly distribution model, which also makes it more attractive to international investors.

I believe the appeal in Equinor lies in some of the most qualitative legacy operations in Europe, coupled with decarbonization pushes and renewables - but for me, I view the renewables portfolio as a bit of a challenge and risk in addition to its upside given the specifics of offshore wind. I may be wrong here, and I am open to that.

But here are the future risks and upsides I see to Equinor.

The main risk is, as you might expect, the renewables sector of the company. While this is not a risk that I uniquely cover - it seems to me to in fact be the most commonly quoted risk to Equinor out there, it's worth mentioning nonetheless that Equinor historically has not seen the high returns from its renewables investments that it has expected. If those investments turn sour, it might not only dilute earnings - they could result in impairments, and it's not as though those impairments would in any way be strange or unheard of in this sector.

The company's stated introduction of exact power generation, CO2 reduction goals, and spending goals, I also view the risk as quite high that the companies that Equinor turns to for these pushes will keep this in mind. If you state that within 1 year, we're going to spend this amount of money - then I view it as a risk that you pay more than you should. Diligent capital allocation is in fact, to me, an exercise in patience, something I need to remind myself from time to time.

On the upside for Equinor, we have new discoveries of oil/gas that will allow Equinor to use most of its existing infrastructure, hence adding relatively cheap capacity to an already impressive portfolio. Unlike the Middle East, and Russia given their invasion of Ukraine, Equinor is close to Europe physically, meaning it can not only deliver easier in terms of oil but also take advantage of the European push to become less reliant on Russia as a source of energy.

Let's look at what this says for valuation.

Despite a significant drop in native share price, moving down 15% in less than 3 months, the company is not where I would consider it an absolute must-"BUY".

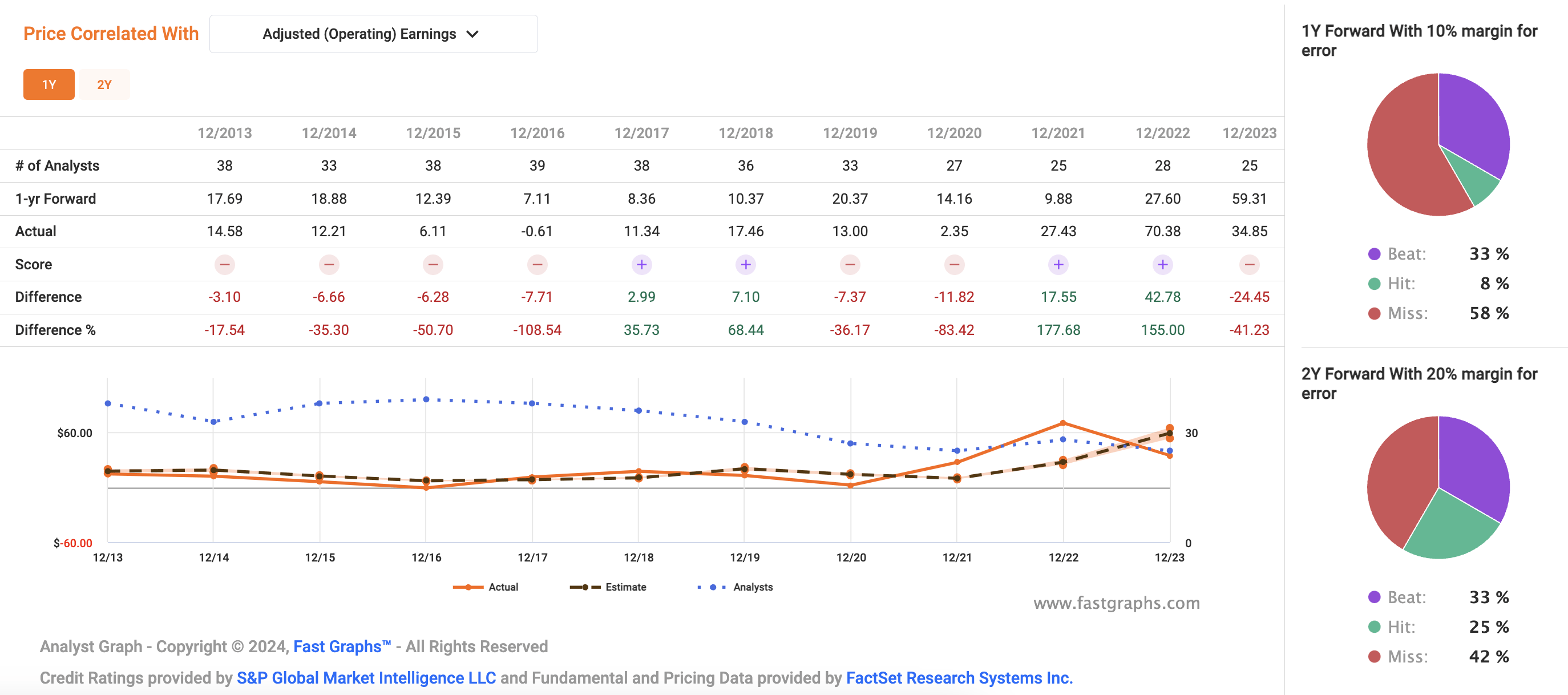

This is because while the company's adjusted earnings fell 50% to less than 35 NOK/share, and this does sound quite a bit (in fact, it is less than the company's dividends for the 2023 fiscal), those earnings are set to come down even further in 2024E. (Source: FactSet)

For now, the expectation is for Equinor to see a decline in its earnings of another 6% this year, both due to increased investments and less favorable markets. It's also worth mentioning that Equinor quite often does worse than expected.

Equinor Earnings Accuracy (F.A.S.T graphs)

This begs the question, what would be a suitable valuation and a suitable upside for this? At the heart of Equinor lies its dependence on the oil price. This will, without a doubt, continue for some time until the mix is more renewables-heavy than it is today. The oil price looks relatively stable today at over $60/share, but we also know that this can change quickly.

Also, beyond the oil price, Equinor's heavy investing means that not only are earnings or cash available for dividends likely to decrease, it's likely to decrease materially.

While earnings are expected to be mostly flat, around 0.3% growth until 2026E annually (Source: FactSet), the dividend in native NOK is expected to go from around 26 NOK/share this year to around 15 NOK in 2025E (Source: FactSet). That would imply a yield on the native share price of 277 NOK today of around 5.4% This is still an attractive dividend in its own right, but when compared to the veritable stability of one of my foremost energy investments, Enbridge (ENB), it falls short.

My position in Equinor is small - and its' in the negative. My position in Enbridge is very large - and it's up double digits. This is because I focus on valuation and quality. Both Equinor and Enbridge are qualitative plays in energy as well as renewables. Both are not expected to grow massively. However one has an outsized offshore risk and a lower dividend yield.

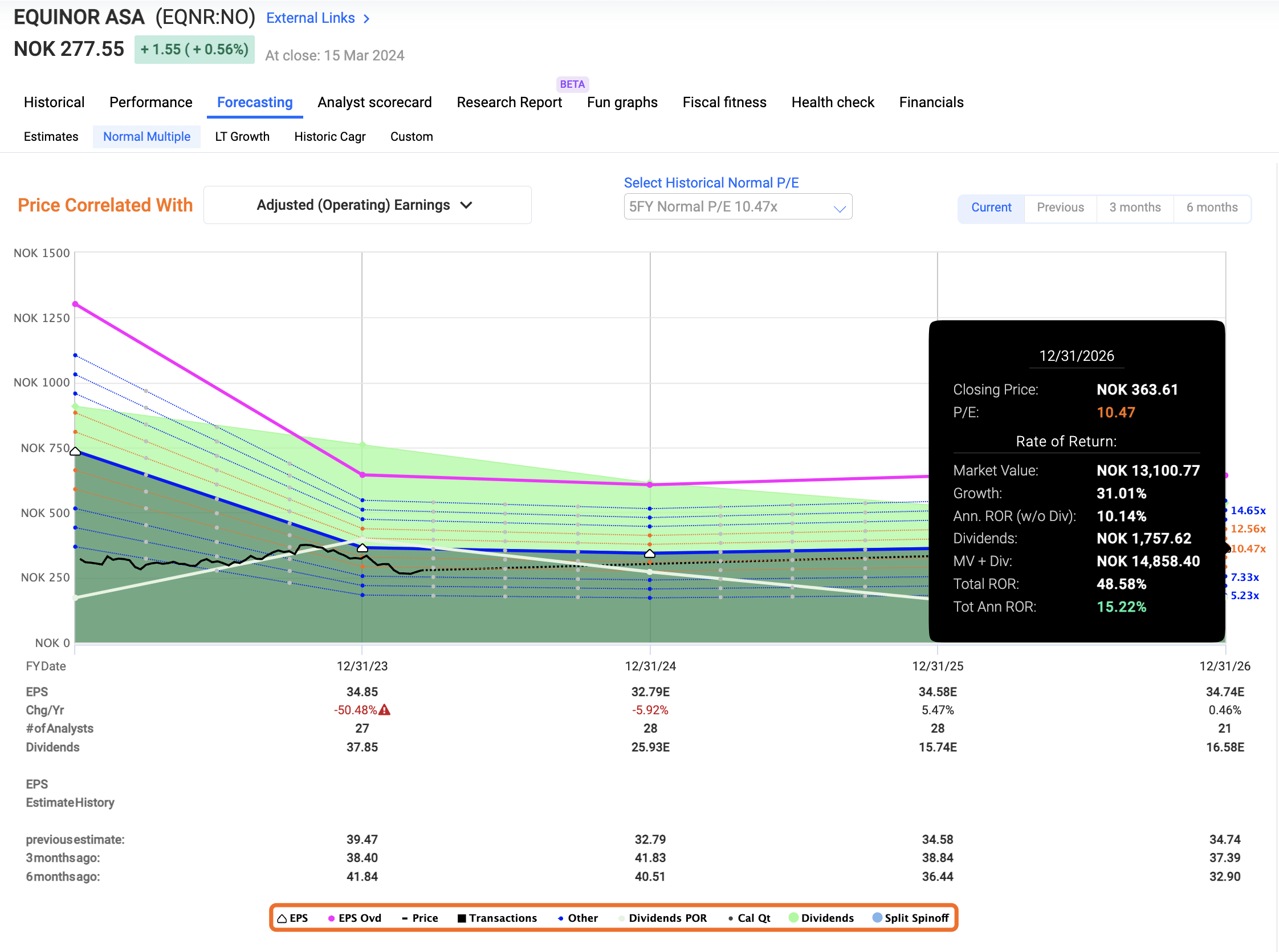

At a 10x P/E, which sounds decent enough for an oil major of this size, Equinor does have a 15%+ annualized upside. That would be the only reason why I could see an upside here for this company, and why I in fact change my rating to "BUY" here. I go by the numbers - and the numbers do speak of an upside.

Equinor Upside (F.A.S.T graphs)

But at the same time, the company is very tied to the success of its renewables portfolio, and I do not view that as all that attractive. The good thing I believe here is that you're very unlikely to lose money or go in the negative with Equinor. At below 280 NOK/share, you're buying the company quite cheaply. At the same time, most analysts are fairly uncertain about where this company should trade. We have 23 analysts, with the lowest targets starting at around 200 NOK, and the highest going to around 500 NOK. Even today, you're paying around 1.15x NAV, but I view buying the company below its NAV as something rare and often unlikely. The average target here comes to around 280 NOK/share, with most of the analysts following FY23 at either "HOLD" or a neutral rating.

I believe Enbridge, at a good price, is better than Equinor at a good price. Is Equinor undervalued and a "BUY" here? Yes, I believe that it is. But you need to realize that this company has a well-established history of valuation weakness, despite its impressive generation of cash - and if you invest, you should be okay with that.

Here is my thesis for Equinor as it stands going into 2024E.

Remember, I'm all about:

Here are my criteria and how the company fulfills them (italicized).