domin_domin/E+ via Getty Images

domin_domin/E+ via Getty Images

It's no secret that I'm very bullish on REITs and other commercial real estate stocks. I regularly write articles on my favorite REIT investment opportunities and some of you would probably describe me as a "REIT cheerleader."

But I am still objective enough to recognize that it's not all sunshine and rainbows in the REIT world.

On the contrary, many sub-sectors of the commercial real estate/CRE market are today facing significant challenges, and this could lead some REITs to underperform going forward.

I won't even discuss the office sector because we all already know about its challenges. Instead, I will focus on the often underreported challenges of the real estate sector.

Here's all the bad news that REIT investors are facing following the recent Q4 2023 results:

Apartment REITs did exceptionally well in 2021 and 2022 when inflation was hot, interest rates were low, and cap rates were compressing.

Property values surged and investors earned big returns.

But this then prompted a lot of developers to start building new apartment communities, especially in the sunbelt regions where demand was growing.

Austin, as an example, made a lot of headlines for its rapid rent growth as the entire country seemed to be moving there.

But now all of these development projects are coming online and it has put most markets, especially in the sunbelt, in a state of oversupply. It's leading to slightly declining occupancy rates and rents in most cases and landlords also need to increase leasing incentives as they face growing competition.

This is well reflected in the results in most apartment REITs. To give you a few examples, the biggest sunbelt apartment REIT, Mid-America (MAA), guided for a 0.7% drop in its same property NOI in 2024. The performance of apartment REITs that focus on coastal markets is a bit better because they're less impacted by oversupply, but their growth isn't something to celebrate either. AvalonBay (AVB) has guided for just 1% same property NOI growth in 2024.

Mid-America

The problem is that if there isn't much growth, then the low cap rates of this sector may need to expand further, leading to dropping property values.

Take the example of BSR REIT (OTCPK:BSRTF), which is an apartment REIT that focuses on Texas markets. It just released its Q4 results and its NAV per share dropped by 19% year-over-year because of expanding cap rates.

2024 should be another difficult year for the apartment sector, and while things should get better in 2025, some more patience will be needed.

Valuations are low for these apartment REITs, but being selective is key. We favor those REITs that focus on affordable, Class B communities that are less impacted by the oversupply.

I have warned about this quite a few times over the past year.

The pandemic was a huge tailwind for the self-storage sector because people were moving around, they needed to make space for a home office, and a lot of older generations passed away and left a lot of stuff behind. Moreover, many also decided to buy new toys for the outdoors that also needed to be stored elsewhere.

This led to rapidly growing rents, which then sparked the interest of a lot of developers who started building new storage facilities to cash in on this booming demand.

NAREIT

But now things are gradually going back to normal as we move past the pandemic. People are returning back to the office at least three days a week in most cases, people are moving less, and the vaccines are doing their job at reducing COVID-related deaths.

As a result, the demand for self storage is now moderating even as a lot of new supply is hitting the market, putting it in a state of oversupply.

The average occupancy rate of the sector has now declined to the low 90s, which is the lowest in a decade, and rental rates for new customers are down double digit.

Most storage REITs, including the big ones like Public Storage (PSA) and Extra Space (EXR) are guiding for slightly declining FFO per share in 2024, and while their share prices have declined a lot, their valuations still aren't low enough for us to invest in them.

However, I would note that there are some compelling opportunities abroad in this sector. To give you an example, the leader in the UK, Big Yellow Group (OTCPK:BYLOF / BYG), is down nearly as much, but it's not dealing with the same challenges. Today, there's still 10x less storage space per capita in the UK than in the US and the concept is still growing in popularity. This allowed Big Yellow to grow its FFO per share by 7.4% in 2023 and it expects more growth in 2024. We believe that this is a great buying opportunity because it has traded down with the rest of the sector, but there are material differences between the UK and US markets that have been overlooked.

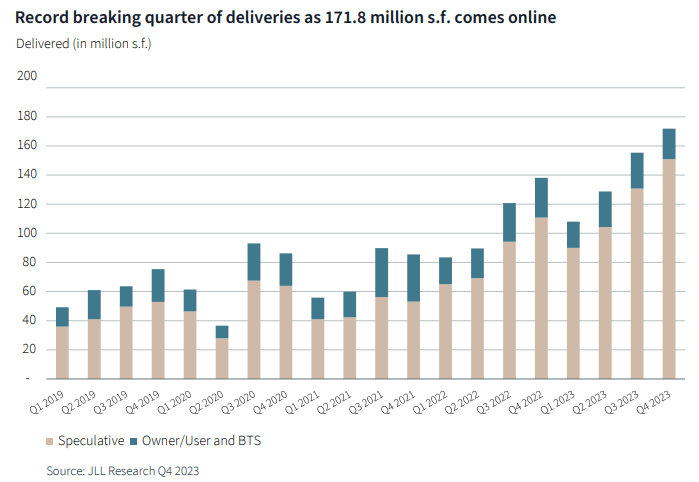

This was very much expected so this is not necessarily "bad news," but the rapid rent growth of warehouses and distribution centers is now coming back down to earth.

COVID-19 brought a huge shift to the consumption of goods instead of services, creating massive, unprecedented demand for industrial space. But that demand peaked early on in 2021 and has been receding since then.

To quote the Lee & Associates' Q4 2023 North America Market Report:

Demand for industrial space in North America sputtered in 2023, hobbled by a host of post-pandemic economic and supply-chain issues. Among them were declining imports, retailers caught with surplus inventories and slumping receipts for furniture, appliances and building materials from a 12-year low in home sales. Additionally, there were wide expectations for an economic recession.

Net absorption totaled 164.8 million SF in the United States in 2023, a 61% drop from the 422.7 million SF of tenant growth in 2022 and a 69% decline from the record 524.7 million SF in 2021. It was 32% less than the 242-million-SF average of the five years prior to the pandemic.

At the same time, the supply of industrial space is expected to grow this year at its highest rate in the last three decades.

JLL Research

The surge of industrial construction starts commenced in 2021 and 2022, when tenant demand was red hot and loan rates were ultra low, began coming online in 2023, but deliveries will peak this year.

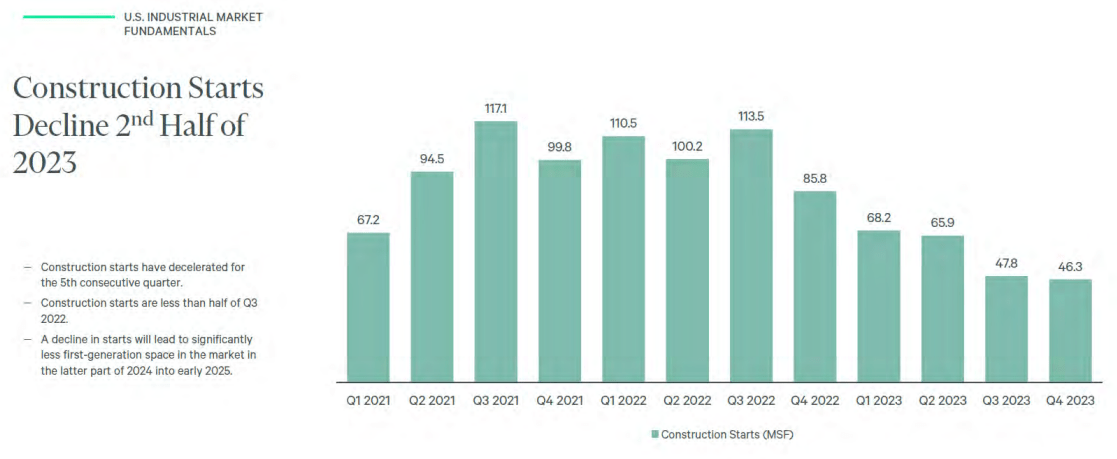

The good news is that construction starts for industrial properties have slumped considerably over the last year amid softening demand and higher interest rates.

EastGroup Properties

Construction starts in the second half of 2023 have returned to roughly the same level as the mid 2010s.

This results in a highly favorable long-term outlook for industrial real estate. While this year's performance should be much more modest than the last several years and represent the "trough" of this cycle, the coming years beyond 2024 should see the see-saw of supply and demand tilt back toward higher demand than supply.

The key again is to be selective as some industrial markets will do a lot better than others. For instance, we own a position in EastGroup Properties (EGP) because we think that its last-mile infill locations of rapidly growing sunbelt markets enjoy barriers to entry that should limit the impact of the new supply.

The last two inflation reports have suggested that headline inflation may be a bit sticker than what was previously expected.

As a result, the expectations for rate cuts also have been pushed a bit further into the future.

This is not the end of the world, but it's still bad news for REITs that are more sensitive to inflation and interest rates.

Net lease REITs are particularly sensitive because their properties are typically subject to 10-plus year-long leases with pre-determined rents and limited rent hikes of just 1-2% each year. Realty Income (O) is a good example of that.

Realty Income

Therefore, net leases are often seen as bond proxies and tend to trade up and down with interest rates. If you think that inflation and interest rates will remain higher for longer, you may want to avoid this sector because its market sentiment would likely remain challenged going forward. Many of them are struggling to grow due to their low rent escalations and the rising interest expense.

On the flip side, if like us you think that interest rates will go quite a bit lower later this year, then this recent dip could be a great buying opportunity.

The key here is to focus on net lease REITs that enjoy above-average rent escalations and are able to grow by acquiring new properties at a positive spread. To give you an example, Essential Properties Realty Trust (EPRT) grew its FFO per share by 8% in 2023 and it has guided for another 5% of growth in 2024. That's not too shabby.

One of the biggest losers of recent years has been the healthcare property sector. Hospitals have been especially hard hit by the pandemic because it led to a surge in healthcare labor costs even as a lot of the revenue coming from elective surgeries/treatments went missing. Moreover, many of the tenants of these properties were heavily leveraged private equity operators that were hit hard by the recent surge in interest rates.

As a result, some tenants are now struggling to pay their rent. The biggest hospital REIT in the world, Medical Properties Trust (MPW), is today in a very tough position with two of its big tenants only making partial payments and potentially facing bankruptcy.

Costar

Similarly, the medical office property sector also is facing a growing risk of oversupply as increasingly many traditional office buildings are developed into medical office buildings.

Once more, selectivity is key. We think that single-tenant medical office buildings that are in average locations could suffer. However, multi-tenant, modern, purpose-built properties that are located in medical clusters should do fine because they enjoy significant barriers to entry and the rapidly aging population is a long-term tailwind for them. For this reason, we think that Healthcare Realty (HR) is oversold right now.

Mortgage REITs lend money to other real estate investors who then make real estate investments.

The model works fine as long as rents and property values are stable and the borrower isn't overleveraged.

But quite a few mortgage REITs made the mistake in recent years of lending at relatively high LTVs (loan-to-value) despite the fact that we were in a very low interest rate / cap rate world.

Now, rates have surged, cap rates have expanded, and as a result, the LTVs have gone from "relatively high" to "way excessive."

Here's an example to illustrate this:

If a property earns $100 of NOI, and it is valued at a 4% cap rate, then it's worth $2,500. If a mortgage REIT lent against the property with a loan-to-value of 65%, it means that it financed $1,625 of the purchase.

But if now cap rates rise to 5.5%, the property is suddenly worth only $1,818, and the LTV surges to 90%, leaving very little margin of safety.

If the loan had a variable rate, the property owner may end up with negative cash flow, breach some covenants, and potentially face a default.

That's the issue that many mortgage REITs are today facing. They were too aggressive when interest rates and cap rates were low and they are now paying the price.

To give you an example, KKR Real Estate Finance (KREF) was recently forced to cut its dividend in half as it prepares to face some losses.

But even here there are some interesting opportunities if you go up the capital ladder. I think that the common equity of these mREITs is too risky, but we own positions in the preferred equity of some of these REITs. Interestingly, the preferred equity of these REITs often dropped just as much as their common equity, despite being a lot safer. As a result, they now offer 8-9% yields and 30%-plus upside to par value as things get better in the coming years.

Last year, REITs raised far less equity than in 2022.

That's because their equity was discounted and their cost of capital was too high to make new accretive investments.

This will slow down the growth of many REITs in 2024.

Realty Income (O), as an example, has historically been very successful at raising equity and making accretive investments that would grow its FFO per share. But this year, it expects to do very little of that because it just isn't able to earn a good spread over its cost of capital.

It has guided for just ~$2 billion worth of acquisitions, down from nearly $10 billion last year.

This will likely remain a headwind for REITs in 2024.

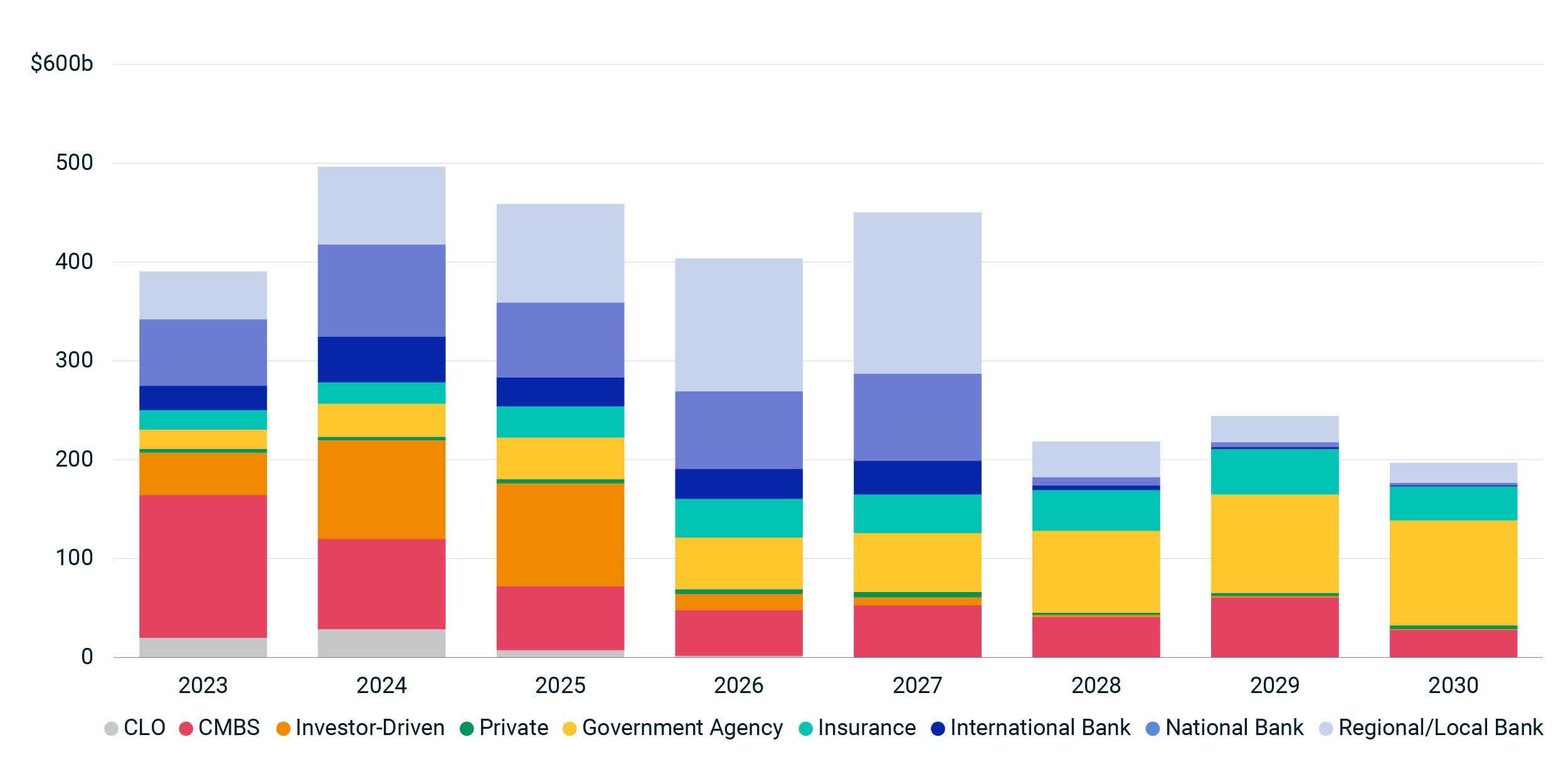

Finally, it has been widely reported in the mainstream media that there's a lot of debt that will mature in 2024 and 2025:

MCSI

This is a big issue for overleveraged private landlords that took on too much short-term debt in the years preceding this recent surge in interest rates.

However, most REITs should be fine. Leverage is today at an all-time low at ~35%, debt maturities are long at ~7 years, maturities are well-staggered, and REITs also retain a big chunk of their cash flow to gradually reduce their debt.

However, it could still impact them indirectly if many private landlords default on their loans as this could then lead to dropping property values and tighter lending conditions from banks.

The REIT sector is a vast and versatile world with more than 1,000 companies worldwide operating in 20-plus different sub-sectors.

There are always winners and losers.

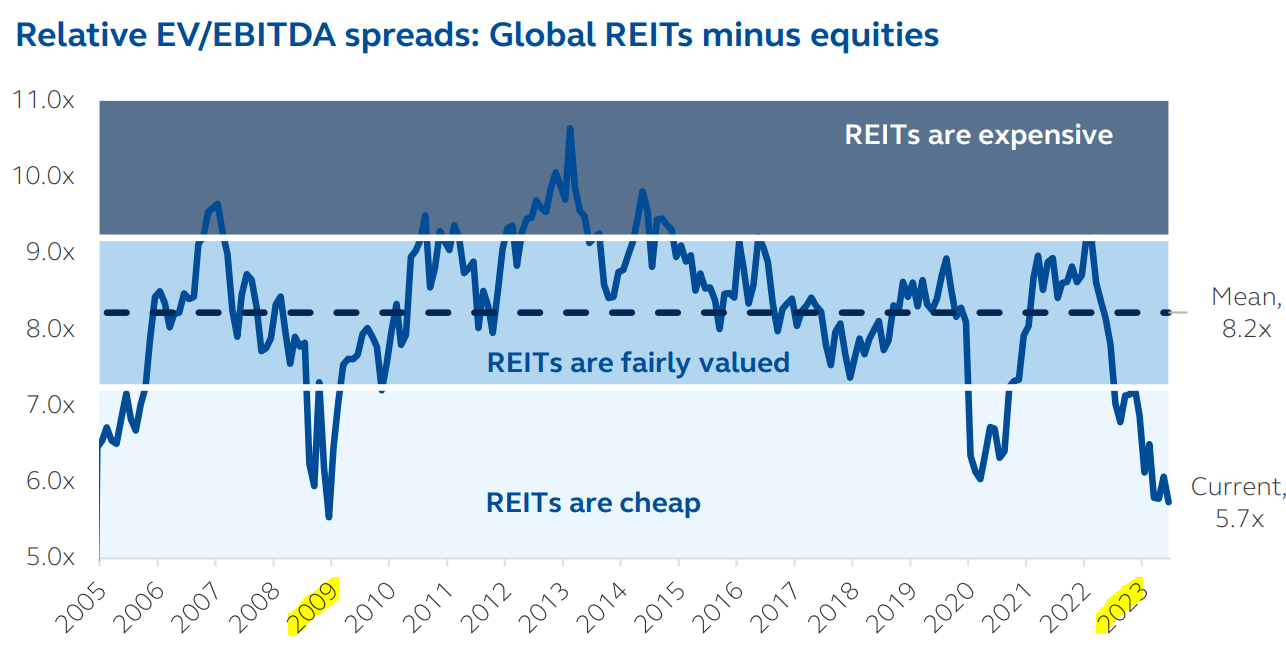

But today, the market appears to only focus on the losers and it's causing the entire REIT sector to trade at very low valuations.

According to a recent study of Principal Asset Management, REIT valuations are today near their lowest since the great financial crisis:

Principal Asset Management

There are vast differences from one property sector to another, and the best opportunities always emerge during times of crisis. The Global Head of real estate at Blackstone (BX) recently talked about this in a Bloomberg interview:

"Where you invest matters. There's a huge bifurcation across asset classes. We all know what's happening with office. Values are under pressure, rents are under pressure. In fact, US office represents only 1.5% of our global portfolio, because we were nervous about office.

On the flipside, look at data centers, which are our fastest growing asset class: 2% vacancy, 25% rent growth, 10 times the demand we saw only 5 years ago, and the AI revolution is just getting started." Nadeem Meghji

Even then, all REITs, even the good ones, are now discounted and we think that this is an opportunity. Just to give you a few examples:

But don't take it just from me.

Blackstone has bought $30-plus billion worth of REITs, often at large premiums over the past years, because they're priced at a discount relative to the fair value of their assets.

We're doing the same and investing while prices are down because we expect a strong recovery in the coming years as interest rates return to lower levels and oversupply turns back to undersupply in many property sectors.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.