Elena Noviello/Moment via Getty Images

Elena Noviello/Moment via Getty Images

Our current investment thesis is:

Edgewell Personal Care (NYSE:EPC) is a consumer products company, specializing in the manufacturing and marketing of personal care and beauty care products globally. Headquartered in the United States, Edgewell's portfolio includes well-known brands like Schick, Wilkinson Sword, and Banana Boat.

EPC’s share price performance has been disappointing, losing over 50% of its value during the last decade. This is a reflection of dire financial results, contributing to a decline in shareholder value.

Capital IQ

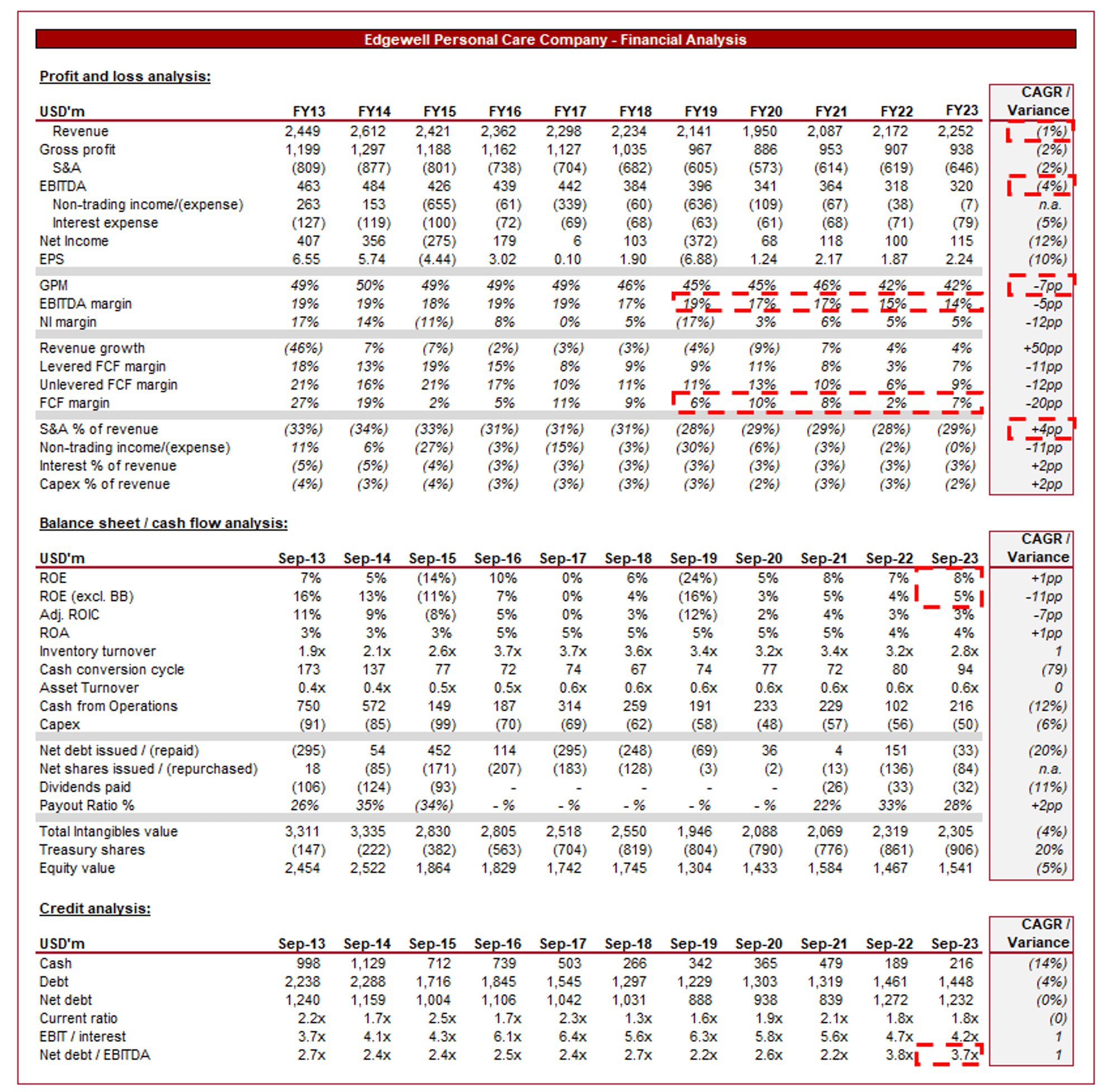

Presented above are EPC's financial results.

EPC’s revenue has declined at a CAGR of (1)% during the last decade, while margin contraction has contributed to a (4)% declining rate for EBITDA.

Business Model

EPC owns a diverse portfolio of global and national personal care brands, including Schick, Wilkinson Sword, Banana Boat, Hawaiian Tropic, and Playtex. This portfolio spans across different consumer needs, from shaving to sun protection and feminine care, although broadly covers specific segments.

The company has historically emphasized innovation in product development, introducing new and improved products to meet changing consumer preferences. This has allowed its brands to gain market share globally and consolidate a leading position.

Underwhelming growth

The company’s investment in marketing and advertising campaigns to build brand awareness has not been overly smart in our view, with the focus incorrectly on traditional channels. Its brands have struggled to resonate with consumers in the last decade, hindering brand growth. EPC’s competitors have innovated to gain market share, including operating loss-leader products and heavily investing in influencer marketing. EPC’s response has been non-existent, allowing for a continuous decline in market share. If we take the Wilkinson Sword brand as an example, EPC has experienced a persistent decline since prior to the GFC.

Google

EPC has failed to identify a shift in consumer preferences, with consumers far more influenced by branding and marketing rather than quality in its segment in particular. The rise of dollar shaving kits (and related products) has completely reshaped the industry.

Another factor negative impacting EPC’s growth is its limited e-commerce integration during a period of disruption in the market. Contrast this with its peers who utilized subscription-based models, free deliveries, etc. to entice customers with convenience and speed. These businesses are seeking to take EPC’s future customers, who are increasingly dependent on their devices for purchases.

EPC has overly relied on its retail partners to improve growth, which we concede is an unrivaled reach relative to its peers. The issue is that EPC’s retailers have come under pressure themselves from e-commerce, contributing to a retreat.

Innovation with customer loyalty programs or initiatives to retain customers has completely changed the industry, with businesses focusing on the low monthly cost to easily win customers. EPC’s response was slow, compounding its lost ground.

Further compounding these factors was the COVID-19 pandemic, which impacted consumer shopping behaviors. If a consumer needed a razer, they could either pay hefty delivery costs or bundle with other products from traditional retailers, or get a generous deal with many of the new market entrants.

These factors have contributed to a highly competitive industry with multiple well-established players. leading to limited scope for price action and greater elasticity.

If the company is heavily dependent on a few key products, which is the reason for its weak financial performance. Sufficient diversification is not present and so its declining brand presence has weighed heavily on the company.

Capital IQ

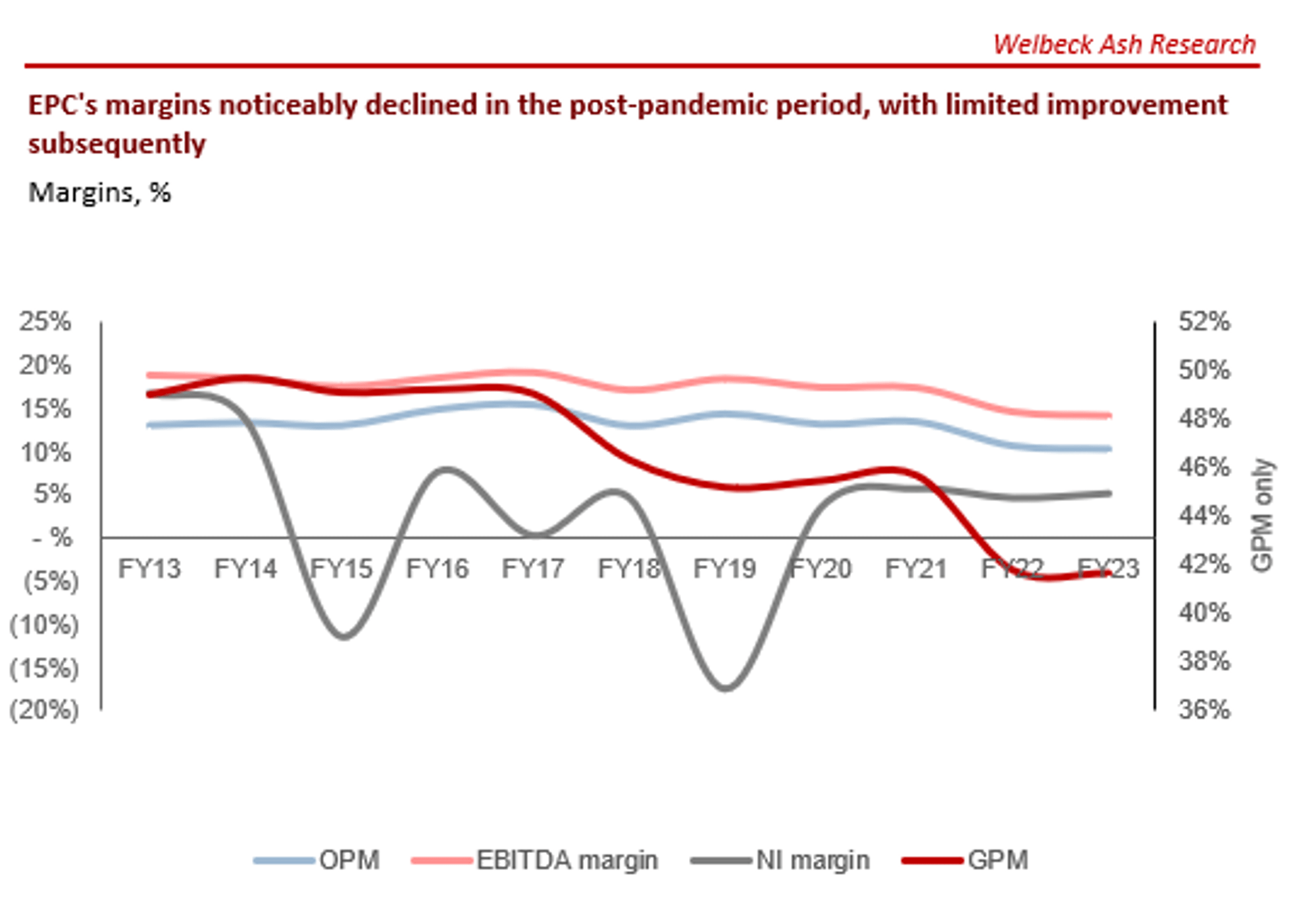

EPC’s EBITDA margin has declined from 19% in FY13 to 14% in FY23, primarily driven by a reduction in GPM (-7ppts), while S&A spending as a % of revenue has declined by 4ppts.

This is partially a reflection of a decline in the competitive position of its brands in our view, with pricing pressure increasingly influencing consumer decisions. Compounding this is supply-side overhang from the pandemic, with elevated transportation costs alongside higher commodity costs.

Although a degree of this is out of the control of Management, many of the companies within its industry have made meaningful progress toward reverting back to their pre-pandemic level. It is highly unusual to see EPC reach a new low in FY23 (following several quarters of disinflation). This implies EPC will normalize below its historical average level.

EPC’s recent performance has been mild, with top-line revenue growth of +1.3%, +9.3%, +4.2%, and (0.5)% in its last four quarters. In conjunction with this, margins have trended down, although are potentially stabilizing.

The company’s mild performance is a reflection of offsetting growth factors. Management’s strategy to revitalize EPC has involved increasing the retail presence of its brands further, contributing to greater sales. Offsetting this, however, is softening inventory demand for particular brands/products (Wet Shave in Japan).

Another indicator of EPC’s limited competitive position is observed in its growth. Many of its peers have outperformed from a growth perspective due to pricing, a key advantage of FMCGs businesses. EPC, however, has been unable to achieve this due to elasticity. In its most recent quarter, pricing drove a 3ppt increase in margins while inflationary pressure and negative mix wholly offset this by 40bpts (prior to productivity gains).

Management has sought to drive a revival of margins through productivity and rationalization in its cost base. We are generally hesitant to be supportive of such action given it usually limits future growth potential.

EPC’s debt balance is not immediately concerning in itself, however, its declining profitability is gradually making this an issue. Management appears shortsighted in its approach to capital allocation. Buybacks have protected returns to an extent, although Management has periodically raised debt to maintain this. This has been required due to a downward trend in FCF generation. Compounding this is the almost $0.9b spent on acquisitions, with limited top-line improvement.

Given the limited scope for commercial improvement, we suspect the business will face a continued decline in revenue generation / stagnation, contributing to a growing debt burden if Management seeks to maintain its distribution strategy.

Capital IQ

Capital IQ

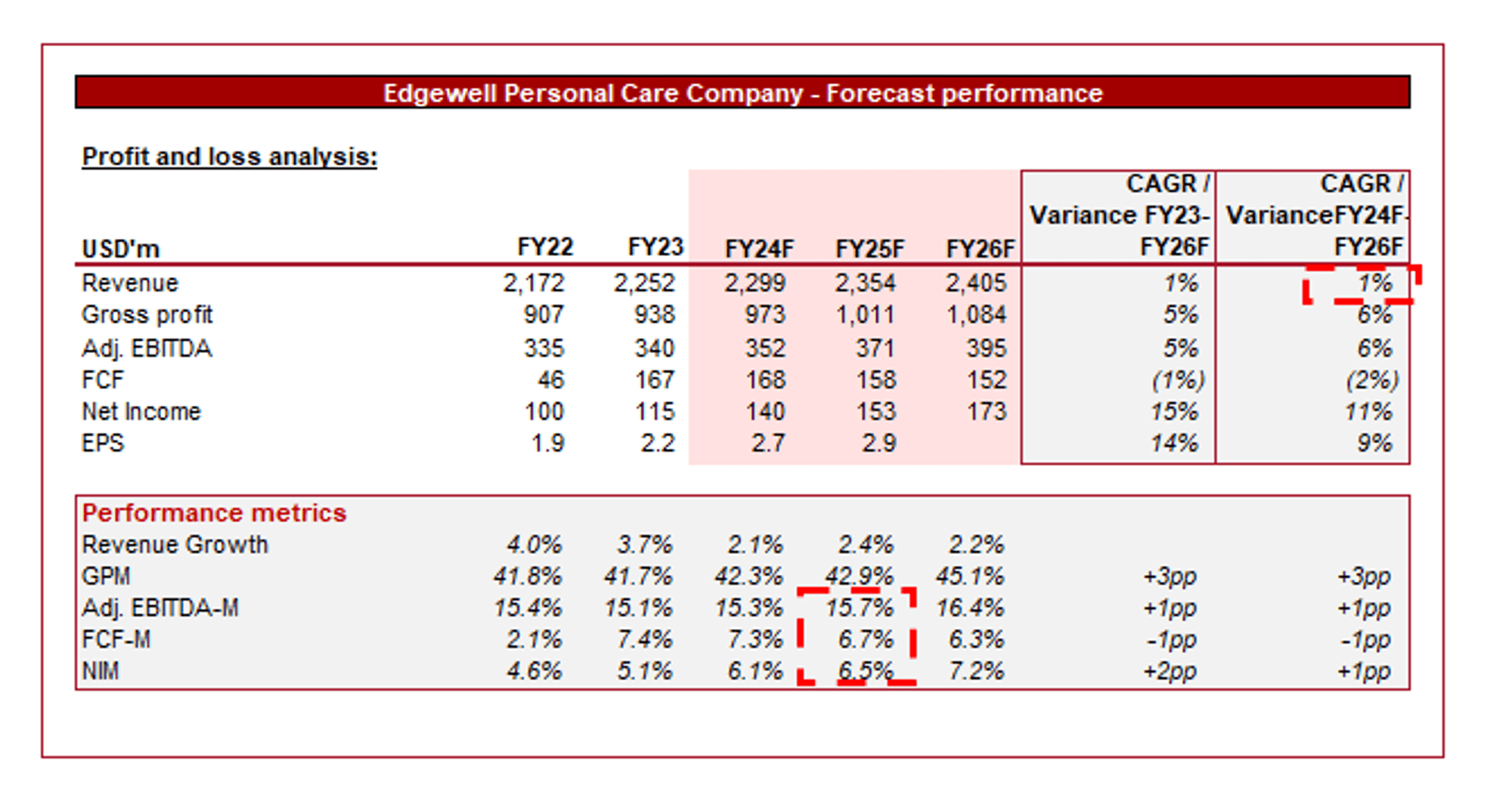

Presented above is Wall Street's consensus view on the coming years.

Analysts are forecasting a continued stagnation in revenue growth, with a CAGR of 1% into FY26F. In conjunction with this, margins are expected to slightly improve.

We broadly concur with this. With limited scope to improve its growth trajectory, the business will likely see limited improvement, lagging behind inflation. Further, with the business still suffering from subsiding inflationary pressures, some upside is possible.

Seeking Alpha

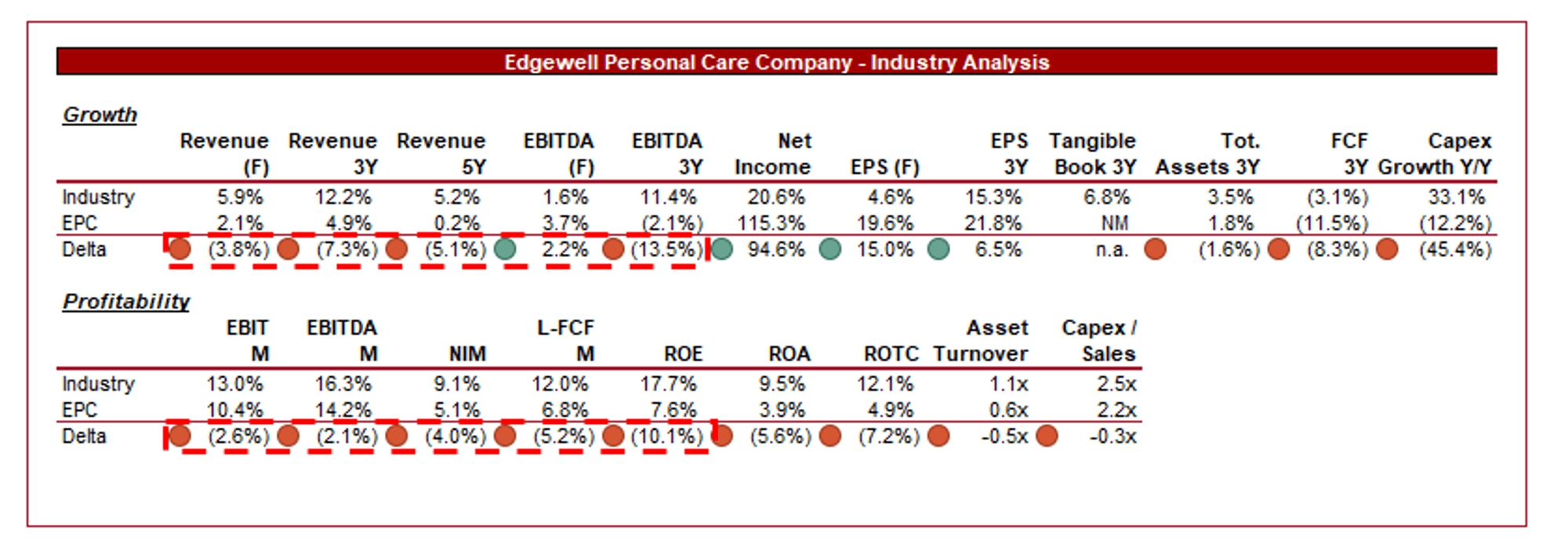

Presented above is a comparison of EPC's growth and profitability to the average of its industry, as defined by Seeking Alpha (19 companies).

EPC’s performance relative to its peers is disappointing, with lower growth and margins. We attribute this almost wholly to the decline in the competitive position of its brands. Innovation in approach and a better understanding of consumer trends have limited EPC’s ability to capture new customers, with this gradually transitioning to the loss in its core customer base. This has a compounding effect on margins.

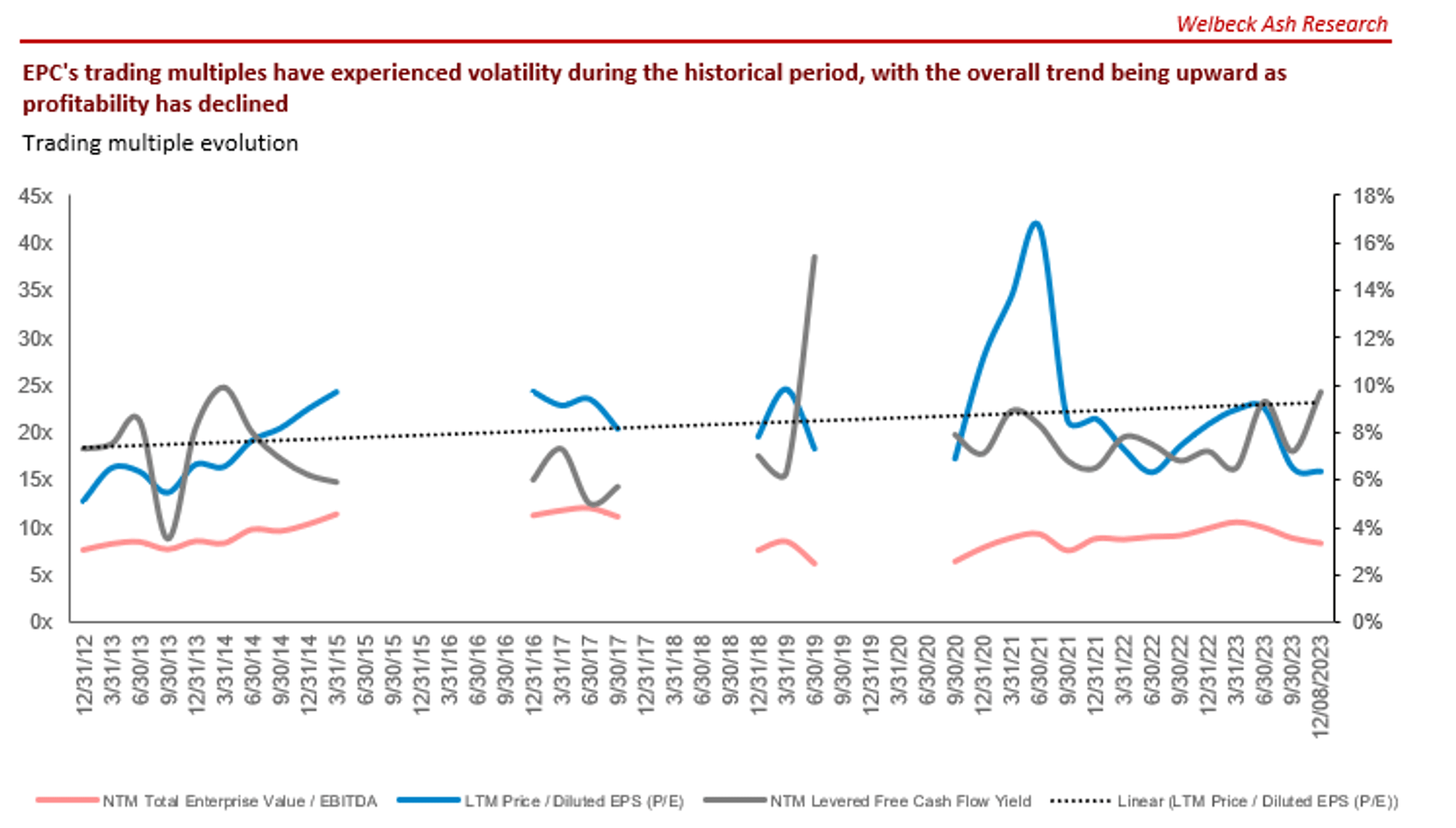

Capital IQ

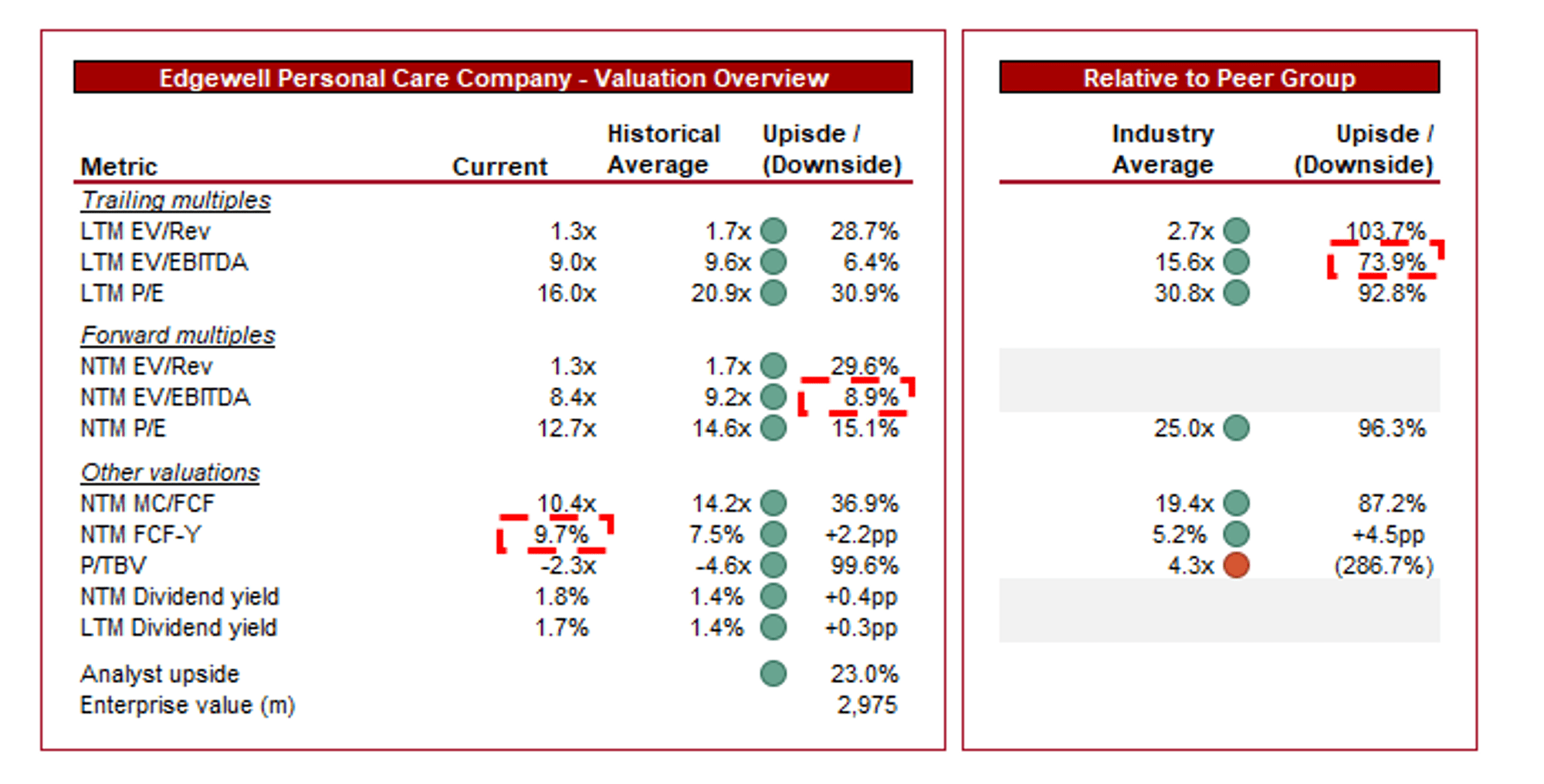

EPC is currently trading at 9x LTM EBITDA and 8x NTM EBITDA. This is a discount to its historical average.

A discount to its historical average is undoubtedly warranted in our view, owing to the company’s declining margins and competitive position, worsening its forward outlook and current financial returns for shareholders. At a discount of single-digits, we see further downside.

Further, EPC is trading at a ~74% discount on an LTM EBITDA basis to its peers and a ~96% discount on a P/E basis. This appears more reasonable compared to the historical average metric, as it correctly quantifies the delta in financial results.

At a FCF yield of ~10%, EPC may appear attractive to some. We would suggest hesitance given the transition to deleveraging required in the medium term, alongside the further risk of underwhelming M&A.

Capital IQ

The risks to our current thesis are:

EPC has quietly experienced a major shift during the last decade, observing a material decline in its competitive position and the subsequent erosion of financial performance that comes with this. We struggle to see how EPC can reverse its current fortunes, particularly given the level of competition and weaker brand value.