Gerasimov174

Gerasimov174

By now, I doubt anyone is surprised when I say I'm bullish on oil and gas (more on oil than gas).

I spent the first two months of this year aggressively buying stocks in this segment and believe high-quality oil and gas assets offer tremendous value in a market with an overall lofty valuation.

JPMorgan

One of the companies that readers keep bringing up is EOG Resources (NYSE:EOG), a company that is also on my buy list, as it's one of the super majors in the American onshore oil industry.

My most recent article on the stock was written on December 4, 2023, when I went with the title "Income And Growth: Why EOG Resources Is One Of My Favorite Oil Plays For 2024."

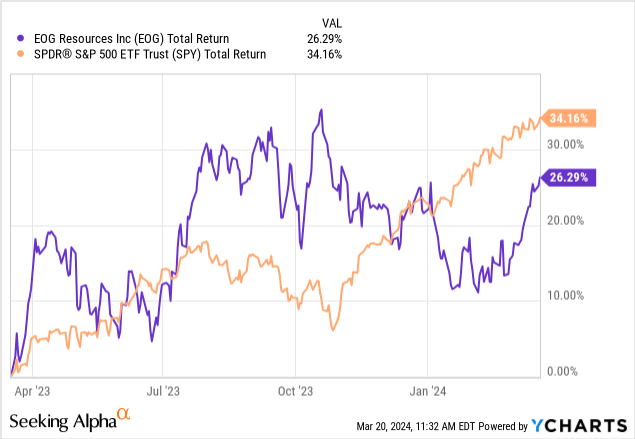

Since then, EOG shares have returned 3.5%, lagging the S&P 500 by roughly 13 points.

Over the past 12 months, EOG has returned 26%. The S&P 500 returned 34%.

The good news is that energy is gaining momentum again, backed by improving fundamentals.

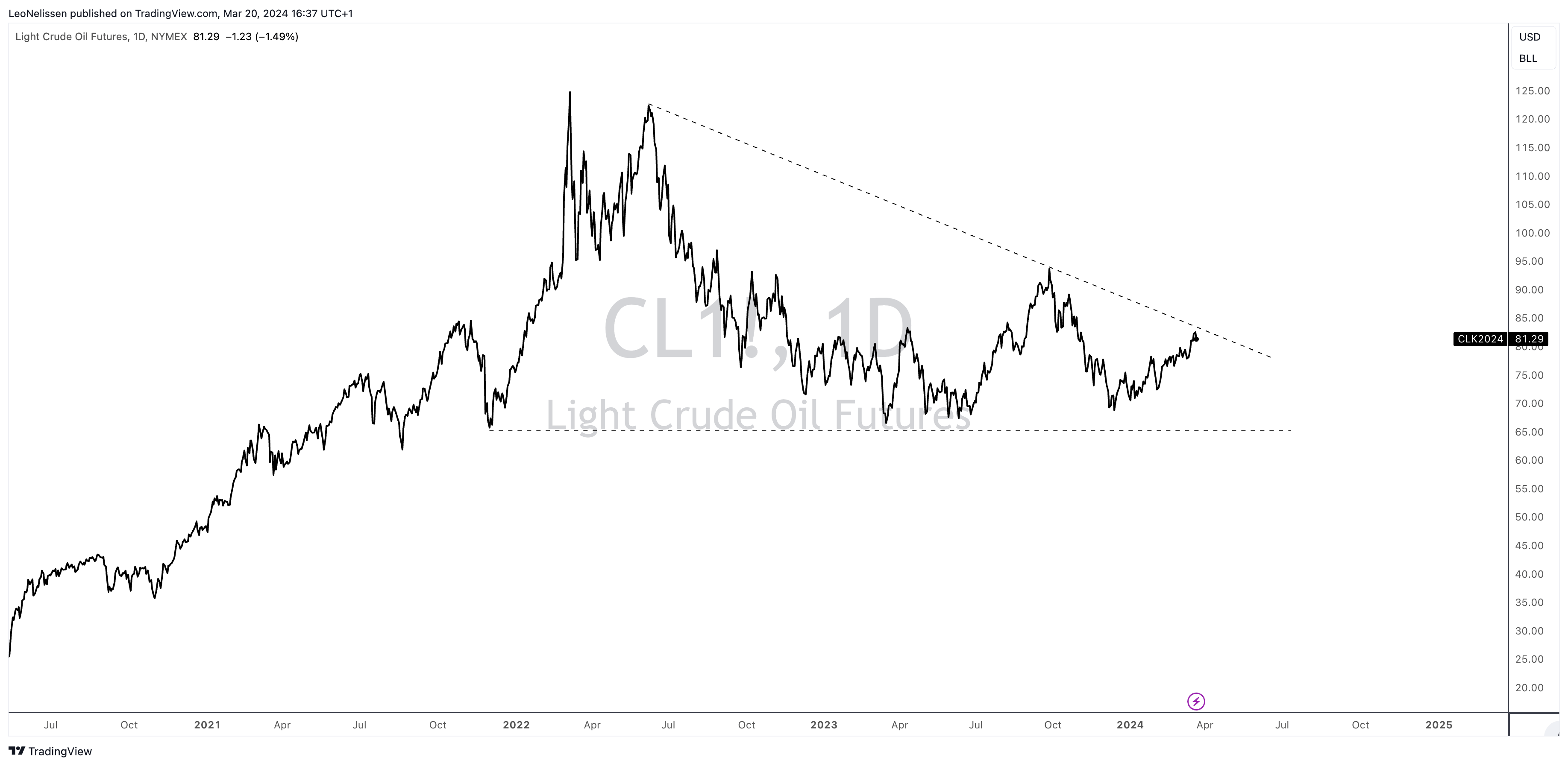

Although it looks like WTI crude oil is failing to break out, the price is close to $82, which is highly beneficial for most low-cost producers.

TradingView (NYMEX WTI Crude)

In this article, I'll explain why I have my eyes on EOG.

So, let's get to it!

Generally speaking, when it comes to oil and gas forecasts - or any forecasts - I'm extremely careful. After all, nobody knows what the future holds, including the smartest people in the world.

So, when it comes to guidance, I more often than not focus on the underlying drivers to build my own bull or bear case.

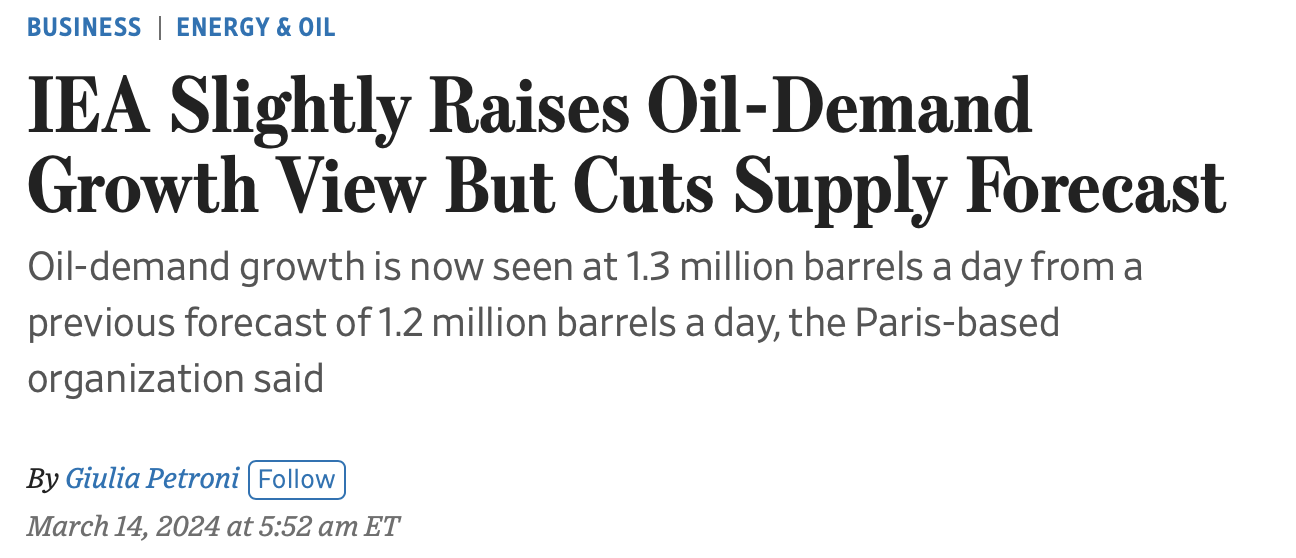

In this case, the IEA (do not confuse this with the EIA) came out, making the case for both stronger demand and weaker supply.

Wall Street Journal

As reported by the Wall Street Journal, the International Energy Agency has revised its oil demand growth. It now expects oil demand growth to reach 1.3 million barrels per day, up from a previous estimate of 1.2 million barrels per day.

As a result, total demand is expected to average 103.2 million barrels per day, slightly higher than the previous projection of 103 million barrels per day.

The revision was caused by several factors, including higher ethane demand in the U.S. for the petrochemical sector and increased use of bunker fuel due to disruptions in trade flows caused by Houthi attacks on Red Sea shipping.

Meanwhile, OPEC expects global oil demand growth of 2.2 million barrels per day this year and 1.8 million barrels per day next year.

The IEA also expects a supply of 102.9 million barrels per day, down from 103.8 million barrels. This is mainly due to OEPC refraining from hiking output.

While oil is dependent on many factors, this is largely in line with my own views on oil and gas, as I believe we are in a situation of favorable supply and demand developments - especially if cyclical growth indicators start to improve this year.

That's where EOG comes in.

There are many reasons to like EOG resources. Production growth, efficient operations, deep reserves, and an eye on shareholder distributions are just a few good reasons.

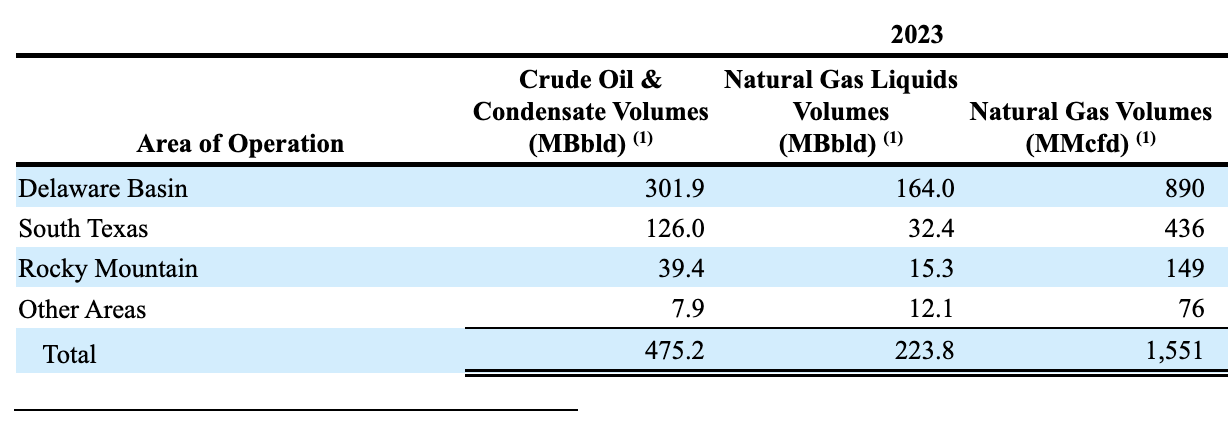

The company, which has a market cap north of $70 billion, broke its production target last year, as it produced more than 1 million barrels of oil equivalent per day.

Most of the company's production took place in the Delaware Basin, which is the second largest basin in the mighty Permian Basin and one of the go-to spot for oil production in the United States.

EOG Resources

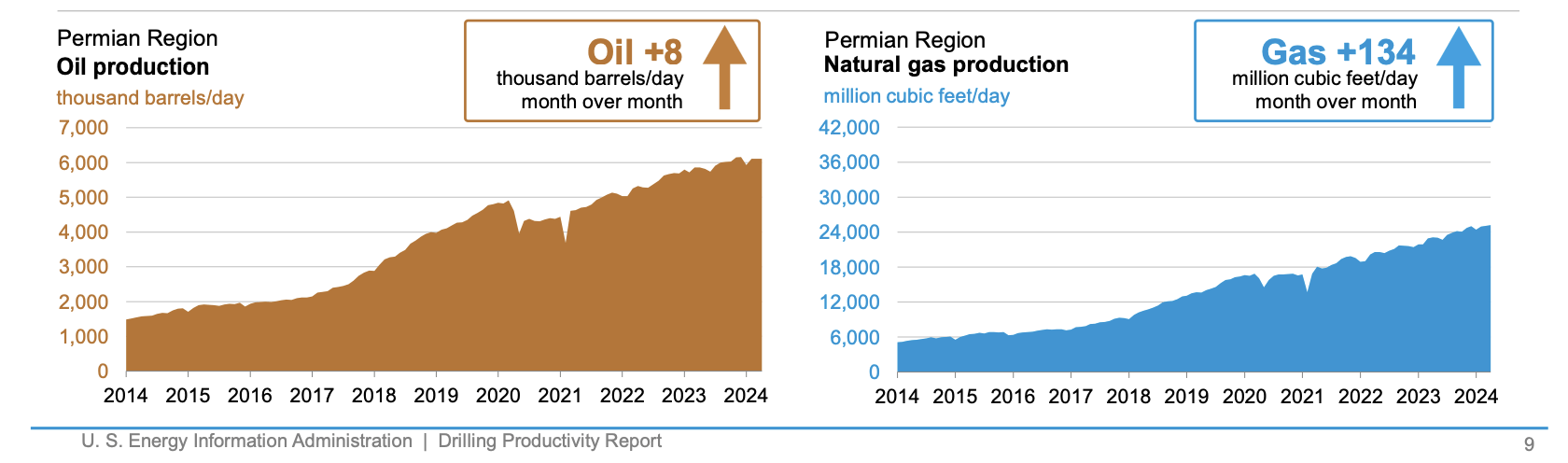

The Permian is also the only place capable of significantly growing the nation's total oil production.

As we can see below, production from new wells continues to offset the decline in legacy production, resulting in consistent output growth. The Permian currently produces close to 6 million barrels of oil per day. It also produces more than 24 billion cubic feet of natural gas per day. This uptrend is even faster, as the Permian is producing a lot more associated gas.

Energy Information Administration

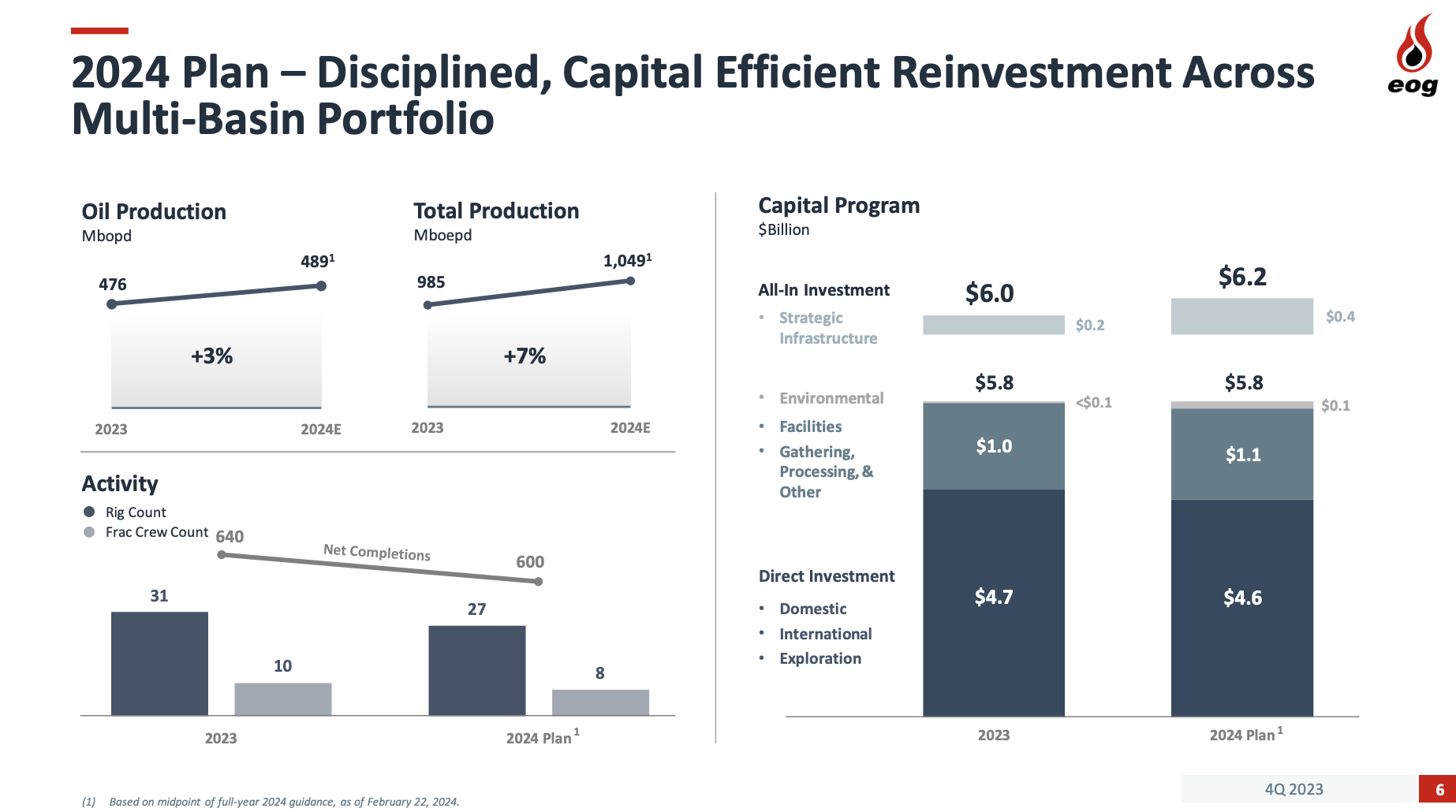

Going back to EOG, this year, it aims for 7% output growth, driven by an investment plan of $6.2 billion. Most of that consisted of direct investments.

Moreover, as we can see below, the company expects fewer fracking crews and a lower rig count in 2024, which is a clear sign of better operating efficiencies.

EOG Resources

Even better, the company is breakeven at $45 WTI.

At $75 WTI ($2.50 Henry Hub - natural gas), the company expects to generate $4.8 billion of free cash flow and a return of capital employed of more than 20%.

In other words, at $75 WTI, the company generates close to 7% of its current market cap in free cash flow!

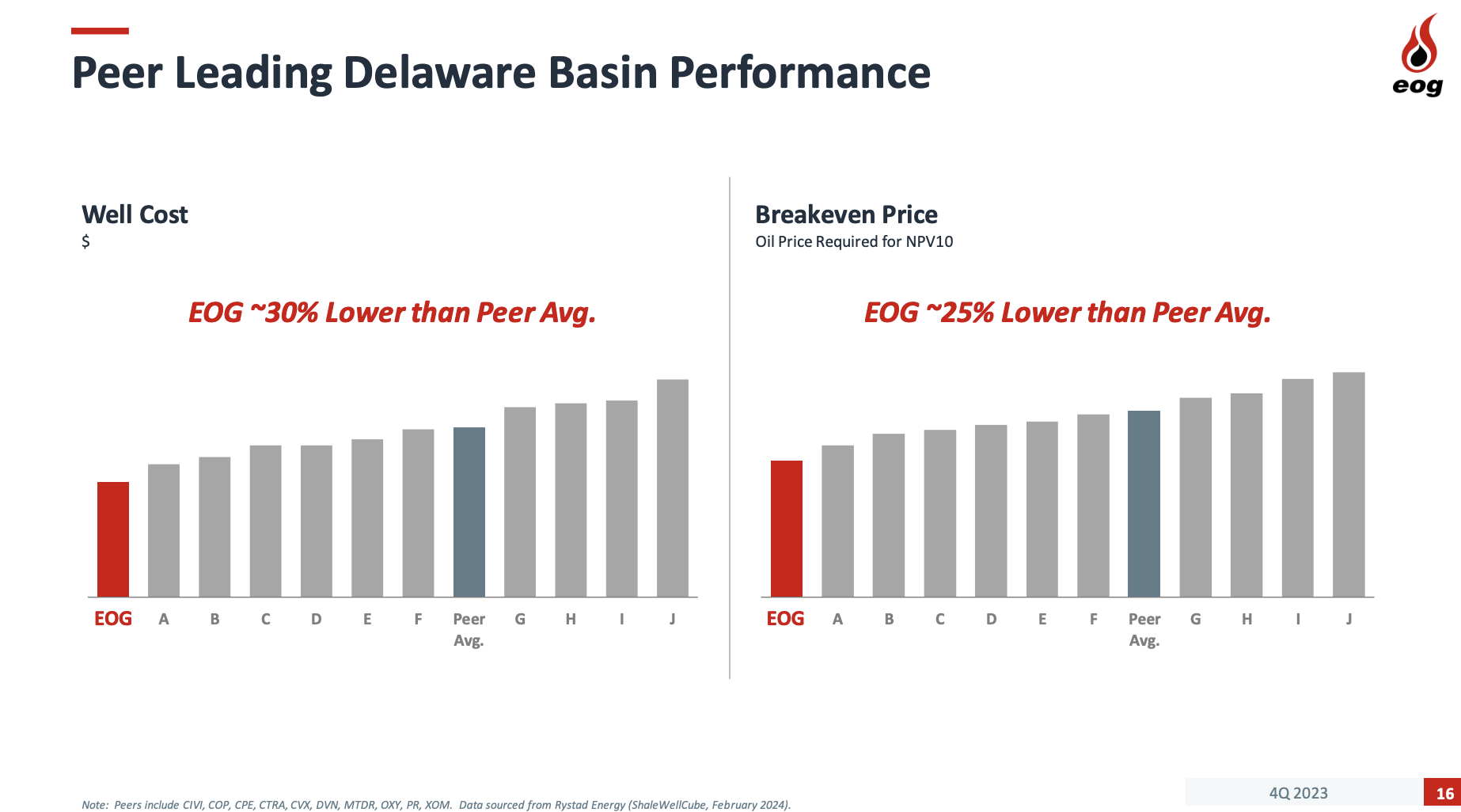

In general, the company is highly efficient, as its breakeven price is 25% below its peer average, supported by 30% lower average well costs.

EOG Resources

But wait, there's more!

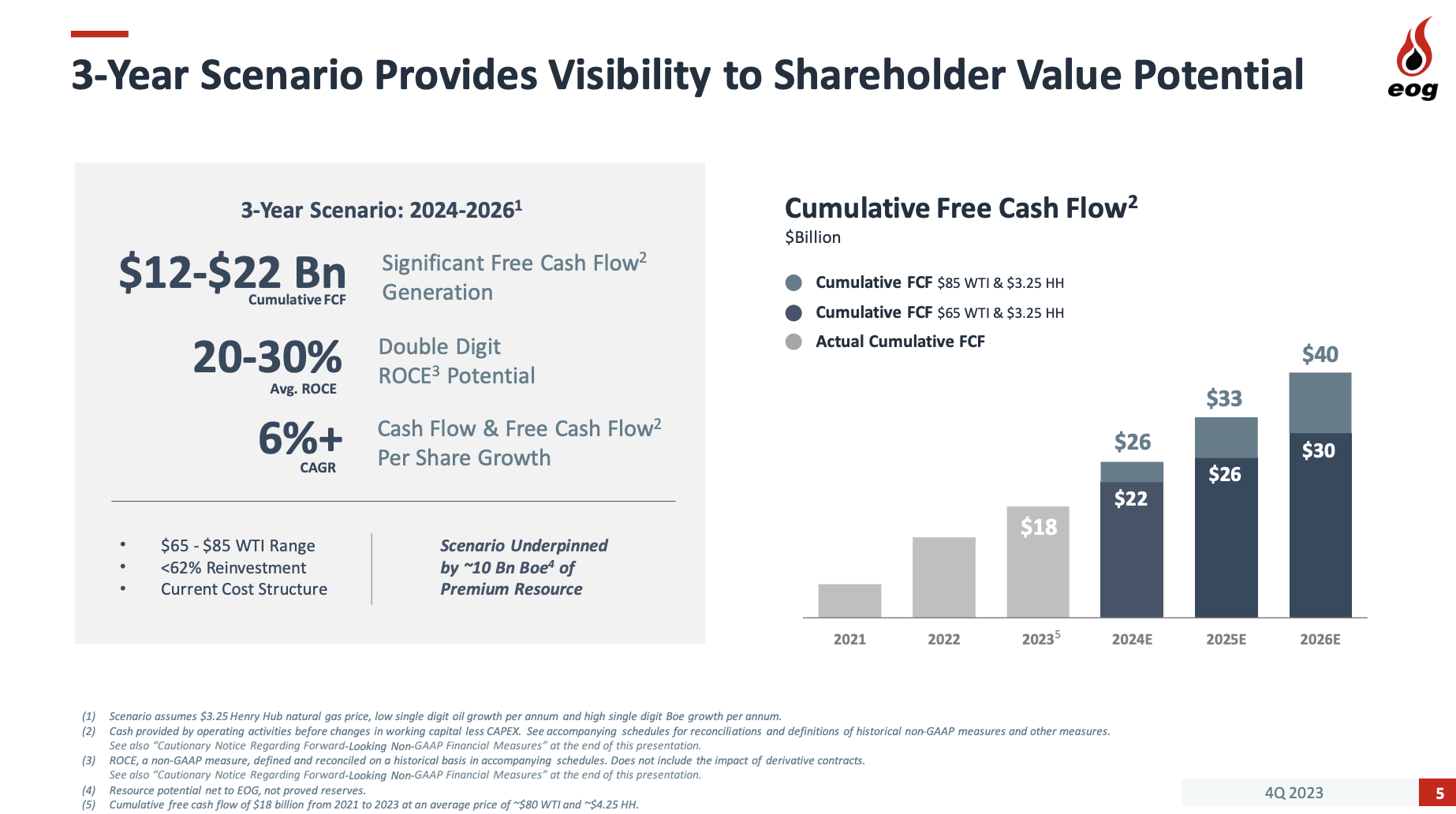

During its earnings call, the company highlighted its three-year outlook for shareholder value creation.

The company expects to generate between $12 billion and $22 billion in cumulative free cash flow, with an average return on capital employed ("ROCE") of 20% to 30%.

In this case, $22 billion is based on $40 billion in 2021-2026 cumulative free cash flow, which the company expects to achieve at $85 WTI and $3.25 Henry Hub. These numbers can be seen in the overview below.

As roughly half of its output consists of non-oil liquids and gas, it's important that Henry Hub prices recover as well. But that almost goes without saying.

EOG Resources

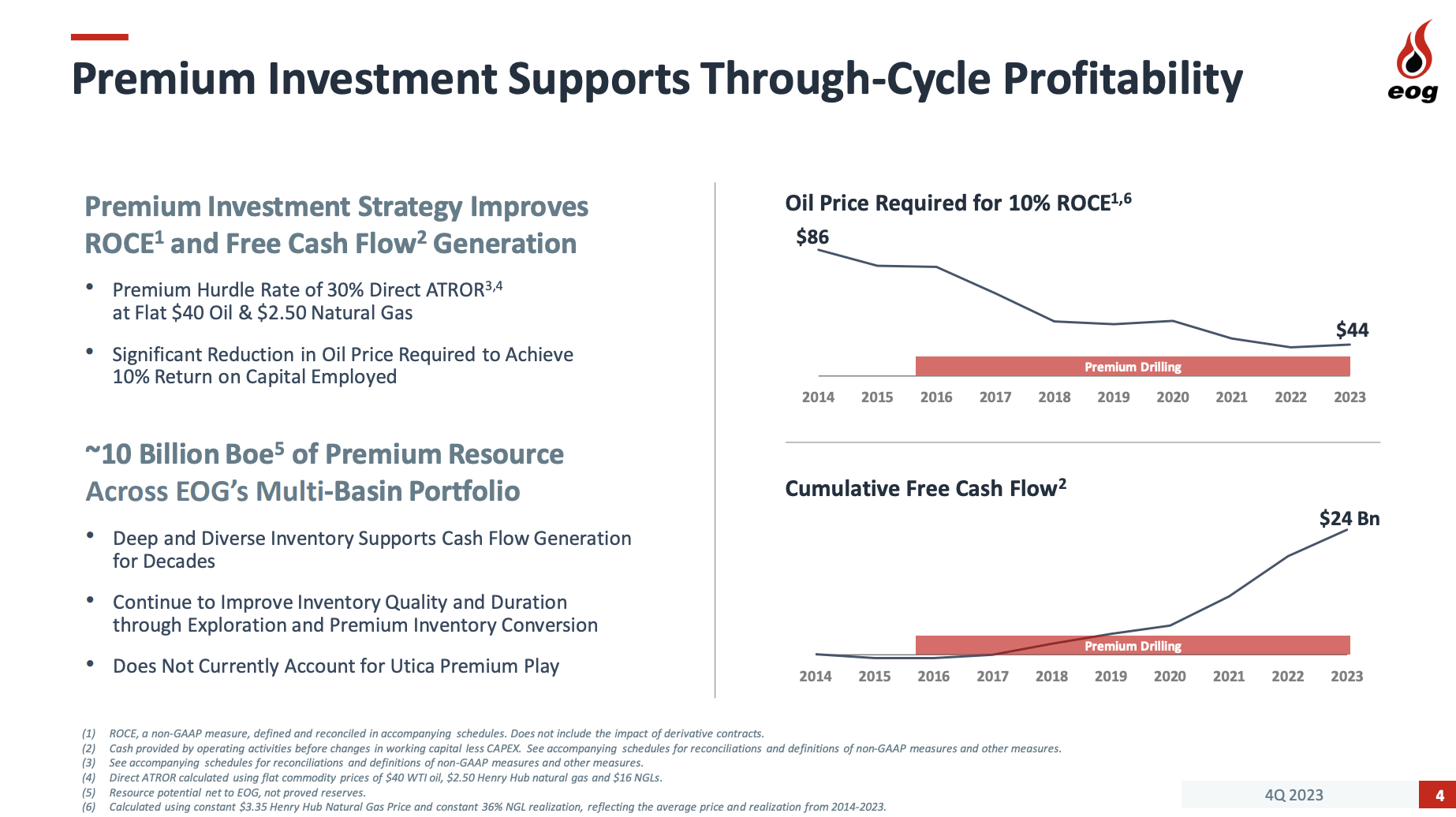

As we can see below, the start of "premium drilling" had a major impact on its ability to grow free cash flow. The company also requires WTI as low as $44 per barrel to reach a 10% ROCE. That's down from $86 in 2014!

EOG Resources

The company also increased its reserves, which bodes well for future growth, as it is not in a situation where it needs to start protecting Tier 1 reserves.

Last year, the proved reserve base increased by 260 million barrels of oil equivalent to almost 4.5 billion barrels of oil equivalent. This indicates a reserve replacement ratio of 202%, excluding price-related revisions.

Based on 2024E production numbers, this indicates roughly 12 years of high-quality production levels without the addition of a single drop of new reserves.

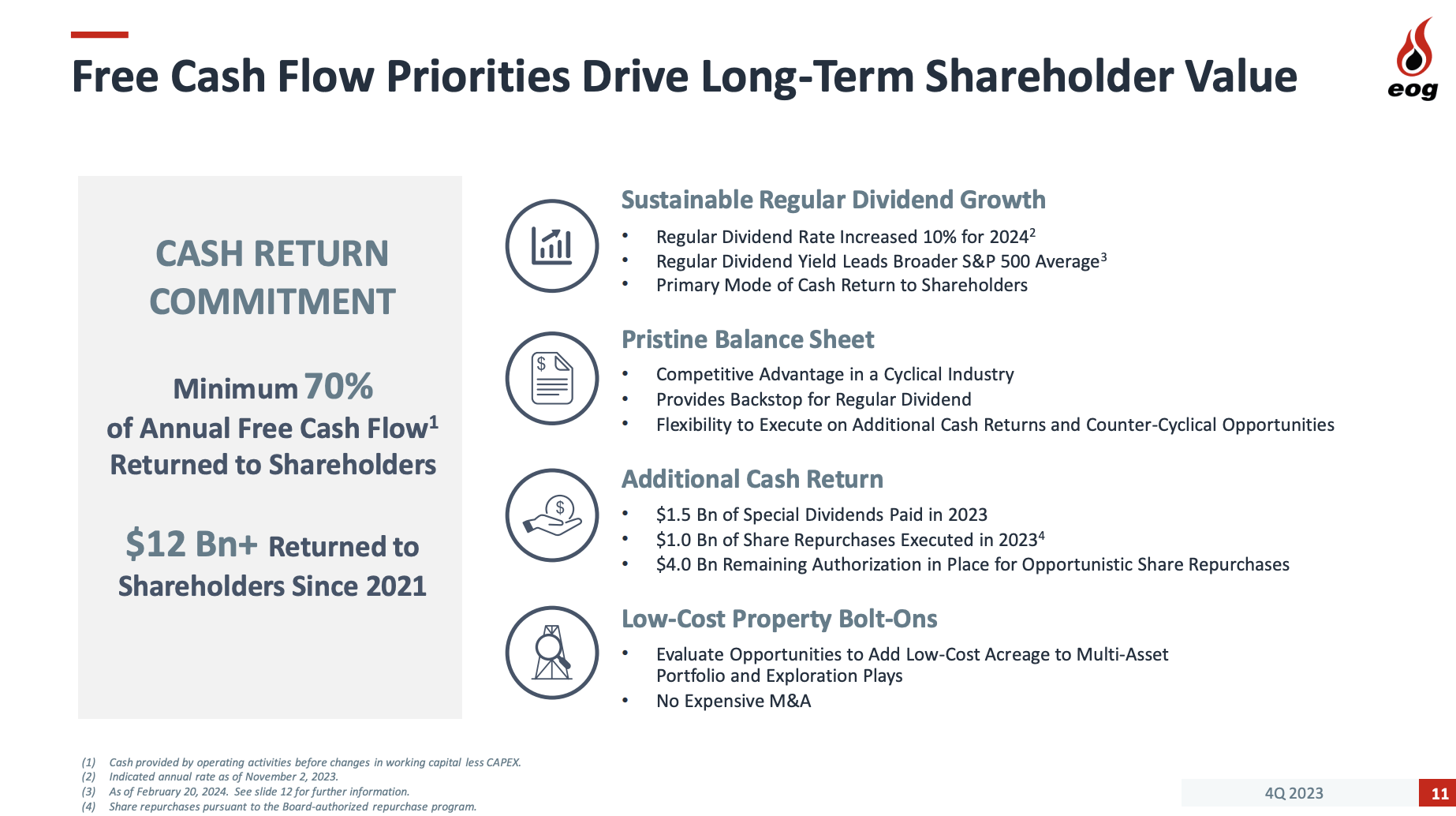

Thanks to ample reserves, a balance sheet with an A- rating, efficient operations, and a favorable environment, EOG is dedicated to letting shareholders benefit from its success.

The company ended last year with $7 billion in liquidity and just $3.8 billion in long-term debt.

Hence, it bought back shares worth $1 billion and stuck to its "promise" to return at least 70% of free cash flow to shareholders.

EOG Resources

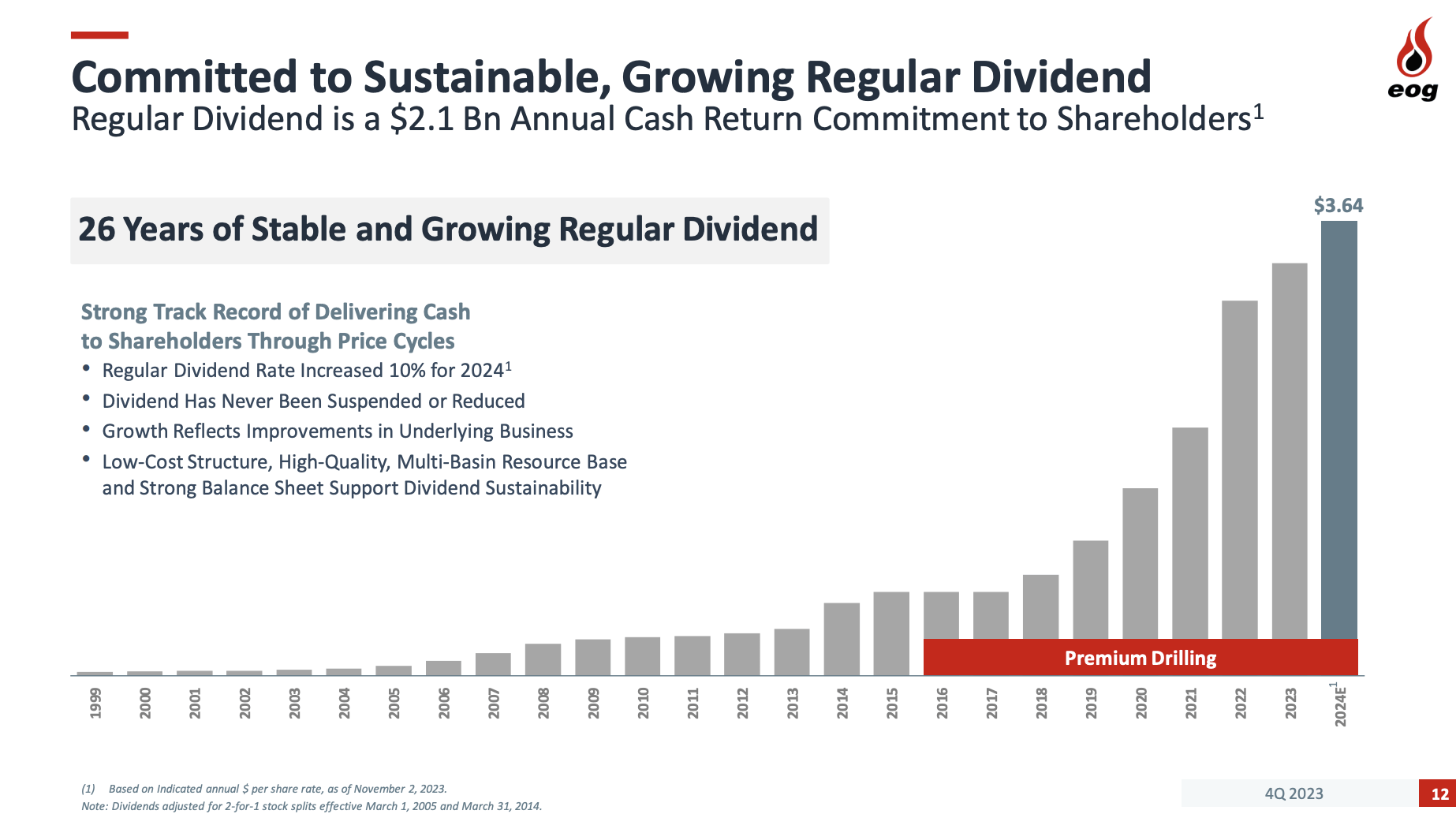

After hiking its base dividend by 10.3% on November 2, EOG currently pays an annualized base dividend of $3.64. This translates to a 2.9% yield.

This base dividend has never been cut and accelerated as soon as the company benefited from a mix of premium drilling and more favorable prices.

EOG Resources

Although I cannot predict what the distribution between buybacks and special dividends will look like in the future, it needs to be said that investors are in a great spot, as the company generates close to 7% of its current market cap in free cash flow at $75 WTI, as calculated in this article.

70% of that is roughly 5%.

Based on its estimates, it could return $3.4 billion this year. That's roughly in line with the estimates at $75 WTI.

Needless to say, these numbers are highly dependent on the price of oil and gas.

On a long-term basis, I expect the company to maintain elevated base dividend growth.

Moreover, as I expect WTI to cross $100 once we get a global growth rebound, I believe that EOG will turn into a cash cow for its investors.

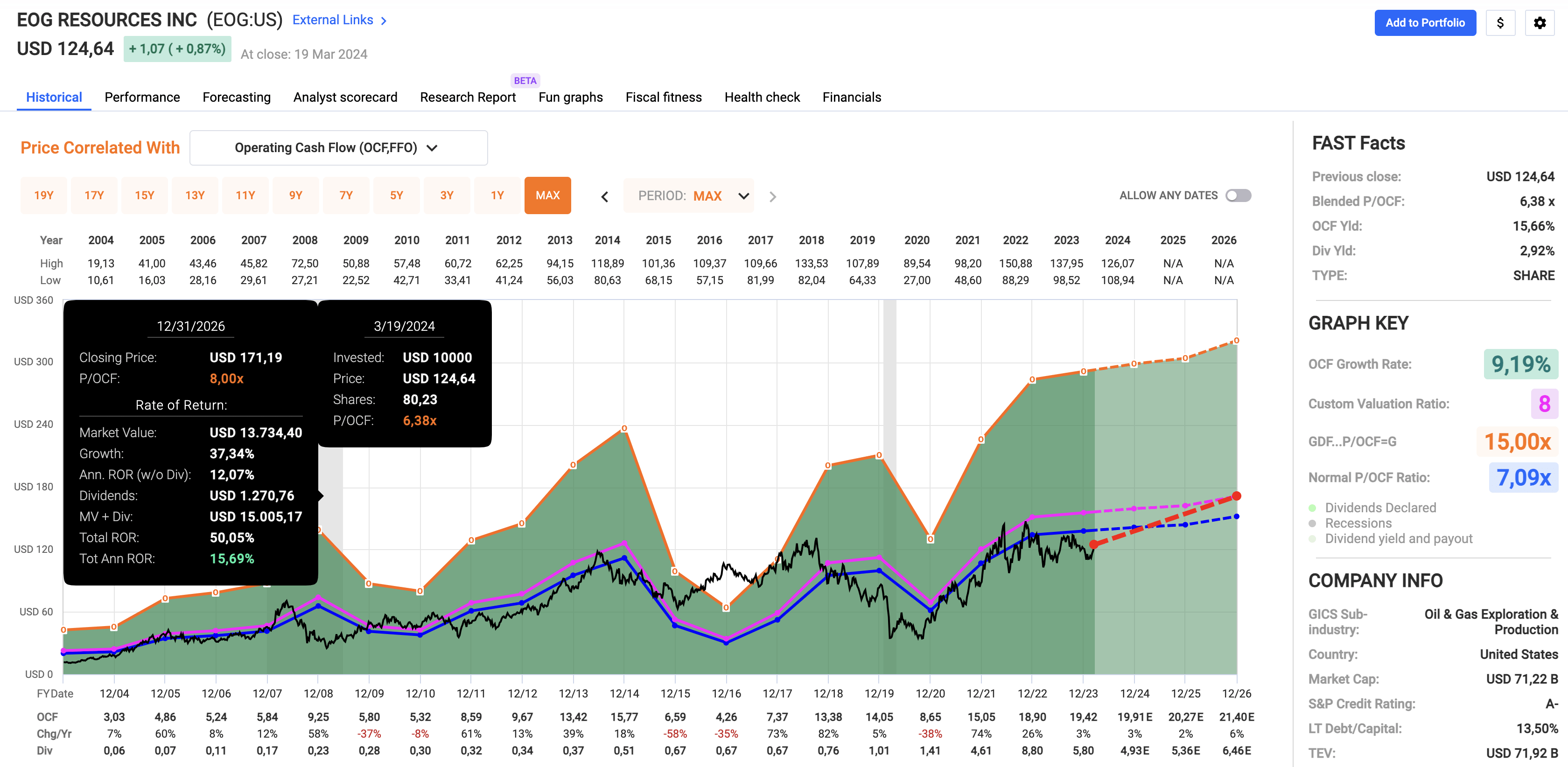

Valuation-wise, I believe EOG is very attractive. Based on the current environment, analysts expect the company to generate $21.40 in per-share operating cash flow ("OCF") in 2026. The number for this year is $19.91.

While these numbers are obviously highly dependent on the price of oil, EOG is attractively priced.

For example, the company currently trades at a blended 6.4x OCF multiple. Its normalized P/OCF multiple is 7.1x, which - I believe - is too low. High-quality companies like Exxon Mobil (XOM) tend to trade close to 9-10x OCF. Although EOG is a riskier stock than XOM due to less diversification and its smaller size, I do not believe it should trade below 8x OCF.

FAST Graphs

This implies a fair price target of roughly $171, which is 36% above the current price.

If oil breaks out, I expect that number to be much higher.

In the world of oil and gas investing, EOG Resources stands out as an attractive opportunity.

With its efficient operations, deep reserves, and commitment to shareholder value, EOG is poised for significant growth.

The company's ability to thrive even in volatile markets, combined with its dedication to returning at least 70% of free cash flow to shareholders, makes it an attractive opportunity for investors seeking long-term value in the energy sector.

Pros:

Cons: