Torsten Asmus

Torsten Asmus

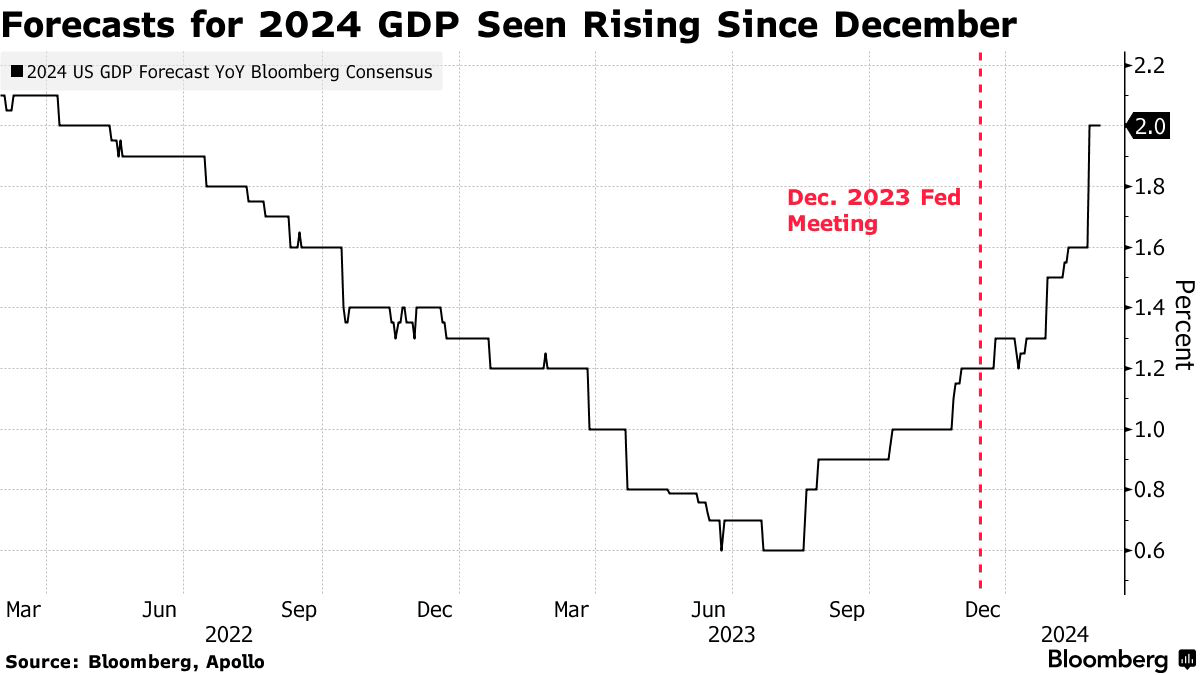

Markets were basically flat this week, but we have an important week coming up with the jobs report, PMIs, and the ECB meeting.

The big economic news was the Core PCE coming in as expected at +0.4% m/m and +3.8% y/y. Heading into the data, investors feared an upside surprise. Inflation hawks noted that the "supercore" measure (core services, ex housing) rose 0.6% on the month, a figure that could keep the Fed on the monetary sidelines, maintaining higher rates for longer.

In fact, we had several pundits come out and state that they think the Fed will not make any cuts this year based on the economic data. On Friday, Torsten Slok from Apollo Global said that the reaccelerating economy, coupled with a rise in underlying inflation, will prevent the Fed from cutting rates this year.

We have seen a massive shift in expectations, from as much as seven cuts to now just under 3 for 2024. That repricing occurred in less than two months.

Bloomberg

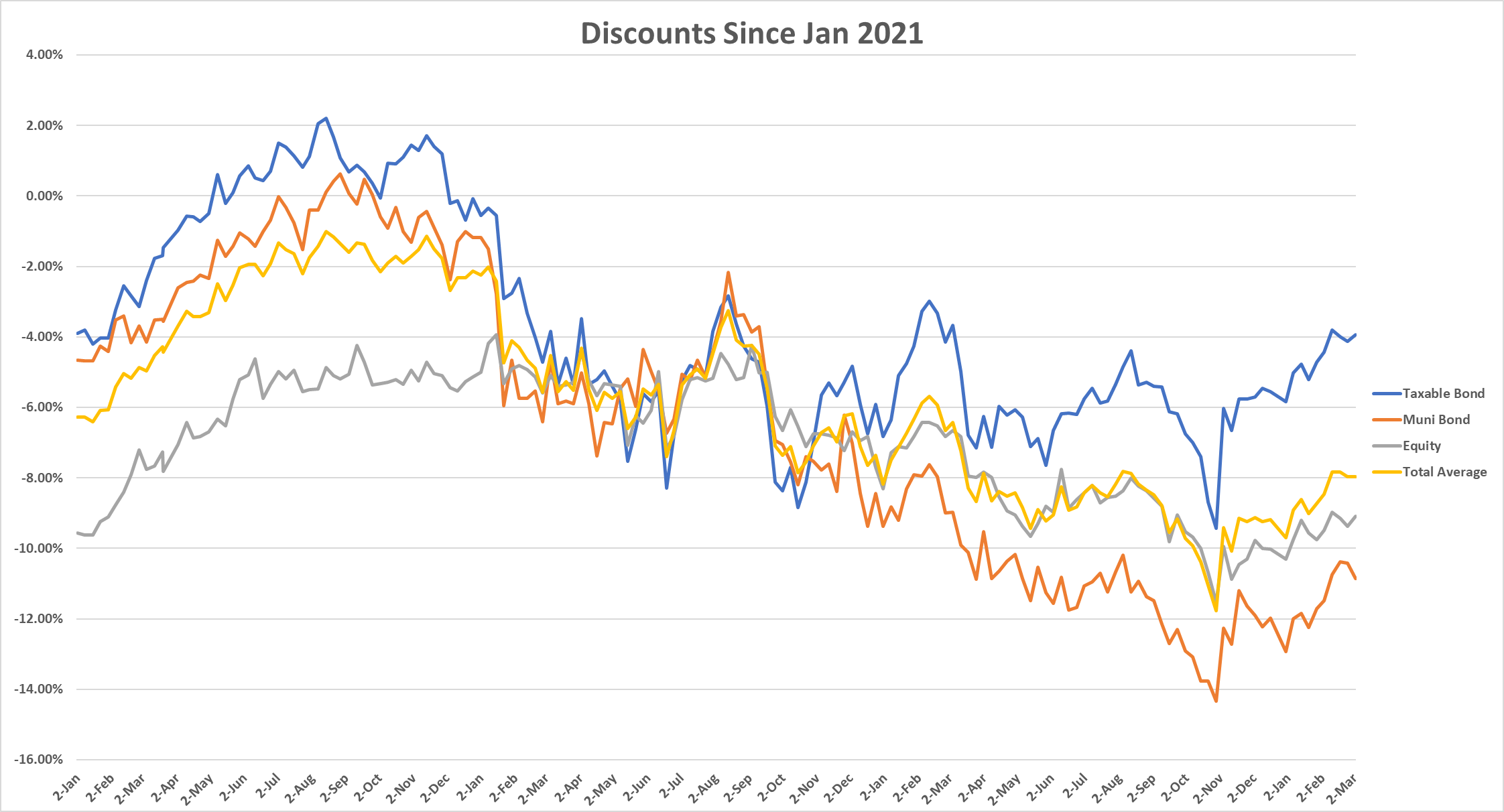

Alpha Gen Capital

Taxable bond CEFs broke back through the -4% discount level and ended the week at -3.9%. On a percentile level, that's about the long-term average. However, for most of that time, interest rates were zero so CEFs were the only game in town for bonds. Now that rates are at 5.5%, long-term average is a bit tight or above value.

Muni CEFs widened back out a bit and are back near -11% as interest rates rise. They are currently in the 97th percentile according to RiverNorth so they still represent a deep value sector.

However, if you look at the chart above, the orange line is munis. They went over -14% back in late October, so the current -10.9% is still 3.2 points tighter than a few months ago.

Given the movement of the taxable space, most of the richest sectors are from that sector. Among the categories, senior loans and high yield are the most expensive CEF categories. Covered call and government are among the cheapest.

Alpha Gen Capital

PIMCO Dynamic Income Strategy (PDX) finally did what we said they would do, shift the distribution to a monthly payout schedule as well as raise the rate significantly.

The fund was currently paying $0.22 per quarter. For March, they increased the 'quarterly' payment to $0.26, an increase of +18.2%. Starting in April, the fund will pay monthly at a rate of $0.1133 per share. That is equivalent to $0.34 per quarter. The prior quarterly rate of $0.22 is the same as $.0733 per month. The new rate of $0.1133 is an increase of 54.5% over the prior 22c per month rate.

The discount as of Friday was -13.7% and the new yield, come April, will by 6.7%. Still, that's about half of the rest of the PIMCO taxables. PDI, for example, is up near 14%.

With the portfolio about 67% equity as of the end of January, clearly they have some way to go before they are a mostly bond portfolio like the rest of the taxable PIMCO funds. I would expect a few more bumps over the coming year or so as they migrate the portfolio.

I think PDX is a solid buy here, especially with oil breaching $80/bl again.

The First Trust MLP CEFs will now convert to open-end exchange-traded funds ("ETFs"). The First Trust Energy Income and Growth (FEN), First Trust MLP and Energy Inc (FEI), First Trust New Opps MLP & Energy (FPL), and First Trust Energy Infrastructure (FIF) will be merged into the First Trust Energy Partners Enhanced Income ETF (EIPI). This is a newly formed and actively managed ETF.

There is a small amount of juice left since you would then be able to sell at NAV, eliminating the discount. On Feb 29th, the funds were trading at mid-single digit discount. For example, FEN was at a -6.2% discount. It rallied 4.3% on March 1st after the new release, leaving approximately -1.9% discount.

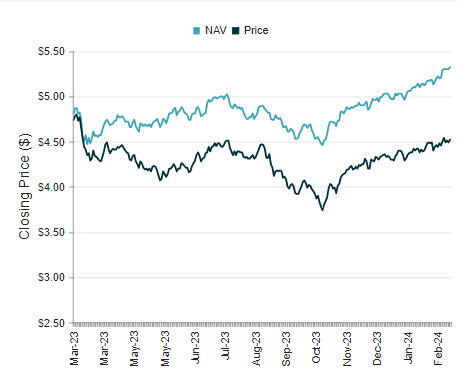

I had Allspring Global Div (EOD) as one of my top picks in the higher-risk category this month. The fund is a mix of big tech (MSFT, AAPL, NVDA, GOOGL, AMZN along with global companies like KLA Corp, Hitachi Ltd, and Broadcom. It is 77.5% stocks and 19% bonds.

The fund recently pays a quarterly distribution, but it's set at over 9.5% per annum. The fund doesn't earn that, so it's partially capital gains and a return of capital. The current discount is near its all-time wides at -15.1%. The long-term average is approximately -7%, so there's quite a bit of juice to potentially squeeze. I like this as a general equity fund (with a tech skew) that pays a higher yield.

CEFConnect

There was a new 13D filed by Saba for the Macquarie/First Trust Global Infrastructure Utility Div & Inc (MFD). Saba currently owns 436K shares or 5.1% of the total shares of the fund.

Staying with the activism, Karpus sent a letter to Blackrock's board on the Blackrock Muni Inc fund (MUI) where they own $152mm of the fund or 18.13% of all shares. The letter stated that they intend to nominate two people for the fund's board at the 2024 annual meeting plus two proposals for shareholder consideration.

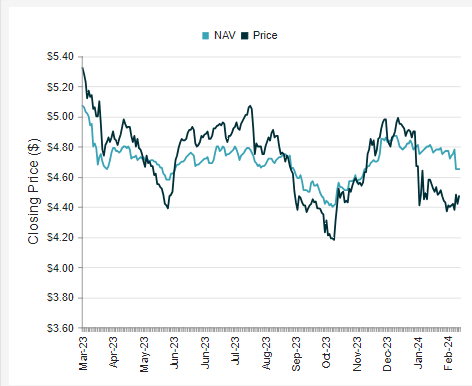

Western Asset High Income Fund II (HIX) completed their rights offering this past week, adding 22.57 million shares of stock to the 67.27 million shares that they had outstanding. The shares will be issued at $4.30 (90% of NAV on Feb. 26) and should hit accounts on March 4th. This is an additional $96mm in gross proceeds for the fund.

The resulting share issuance had the effect of reducing the NAV by 13c per share, or about -2.7%. The discount went from -8.4% to -3.7% in one day as the NAV fell and price rallied by a dime from $4.38 to $4.48.

CEFConnect

My dilution calculator showed about 13c of NAV loss or about -2.9%. That extra 3c could have been offset, at least partially, by the day's move in the asset values since Feb. 26th was a nice up day for the markets and credit spreads tightened.

The last several rights offerings that I've followed, the day of the rights offering expiration or the day or two following has been the time to buy. But this shouldn't be an all-or-nothing type of binary analysis. In other words, the opportunity on discount shouldn't eliminate the rest of your due diligence.

--------------------------------

There has been a lot of movement both to the upside and some to the downside in the taxable CEF sector. I would take a hard look at the Core Top 10 Z-Score list for some ideas on a few trims/sells and a few potential buys.

Alpha Gen Capital Alpha Gen Capital

The left side - the expensive CEFs - are mostly loan funds, which seem to be catching a bid as the narrative shifts back to a hawkish Fed who will be keeping rates up for longer.

The right side is the funds that have sold off and are cheaper relative to their average over the last year. For those looking for a very risk averse fund, check out the MFS Government Markets Inc (MGF) that invests mostly in mortgaged backed securities, government agencies and treasury bonds. It's similar to Blackrock Income (BKT).

The long-term average for MGF is about -4.5% and the discount has widened out to -7.0%. There's no leverage in the fund, so the 8% yield is a bit of a mirage and a chunk of your own money coming back to you. The distribution is set as a managed payout at 7.5% on NAV.

Nuveen PA Quality Muni Inc (NQP): +40% to $0.0455

Nuveen NJ Quality Muni Inc (NXJ): +34.8% to $0.0465

Nuveen MA Quality Muni Inc (NMT): +33.9% to $0.0415

Nuveen MO Quality Muni Inc (NOM): +25.4% to $0.0395

Nuveen VA Quality Muni Inc (NPV): +23.3% to $0.045

Nuveen MN Quality Muni Inc (NMS): +22% to $0.05

Nuveen AZ Quality Muni Inc (NZX): +21.4% to $0.0425

Nuveen AMT-Free Quality Muni Inc (NEA): +18.8% to $0.0505

Nuveen Quality Muni Inc (NAD): +18.2% to $0.052

PIMCO Dynamic Inc Strategy (PDX): +18.2% to $0.26

Virtus Div, Int & Prem Strategy (NFJ): +14.3% to $0.28

Nuveen AMT-free Muni Credit Inc (NVG): +13.9% to $0.0575

Nuveen NY AMT Free Quality Muni (NRK): +13.4% to $0.0465

Nuveen NY Quality Muni Inc (NAN): +12.8% to $0.0485

Nuveen CA Quality Muni Inc (NAC): +12.6% to $0.049

Nuveen CA AMT Free Quality Muni Inc (NKX): +12.1% to $0.051

Nuveen Muni High Income Opp (NMZ): +11.8% to $0.0475

Nuveen Muni Credit Inc (NZF): +11.65% to $0.0575

Nuveen Muni Credit Opp (NMCO): +9.9% to $0.05

MFS Inv Grade Muni (CXH): +8.5% to $0.0255

MFS High Yield Muni (CMU): +8% to $0.0135

MFS High Income Muni (CXE): +7.1% to $0.015

Nuveen Muni Income (NMI): +5.9% to $0.036

MFS Muni Income (MFM): +5.1% to $0.0205

DWS Muni Income (KTF): Distribution increased by 25% to $0.049

PIMCO Dynamic Inc Strategy (PDX): Distribution increased by 18.9% to $0.01133

BNY Mellon High Yield Strat (DHF): Distribution increased by 16.7% to $0.0175

Carlyle Credit Inc Fund (CCIF): Distribution increased by 5.6% to $0.105

Virtus Conv & Inc 2024 Target Term (CBH): -41.3% to $0.027

JH Investors Tr (JHI): -23.9% to $0.2014

JH Income Sec (JHS): -14.25% to $0.1095

Tri-Continental Corp (TY): -7.4% to $0.256

Royce Value Tr (RVT): -6.9% to $0.27

Western Asset High Income II (HIX): The announced completion of the rights offering was made on Feb 26th. The subscription price was $4.30 per share, 90% of the fund's NAV.

Virtus Convt & Income 2024 Target Term (CBH): The fund entered its wind down phase and will noted that they are on target to cease investment operations. In anticipation of its upcoming termination date, the Fund has been shifting its portfolio to shorter duration securities and has paid off its borrowings. As a result, the Fund's yield has decreased. The reduction in the monthly distribution rate will allow the Fund to pay out an amount closer to its expected earnings. A portion of your distribution may be a return of capital.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.